- Summary

- Table Of Content

- Methodology

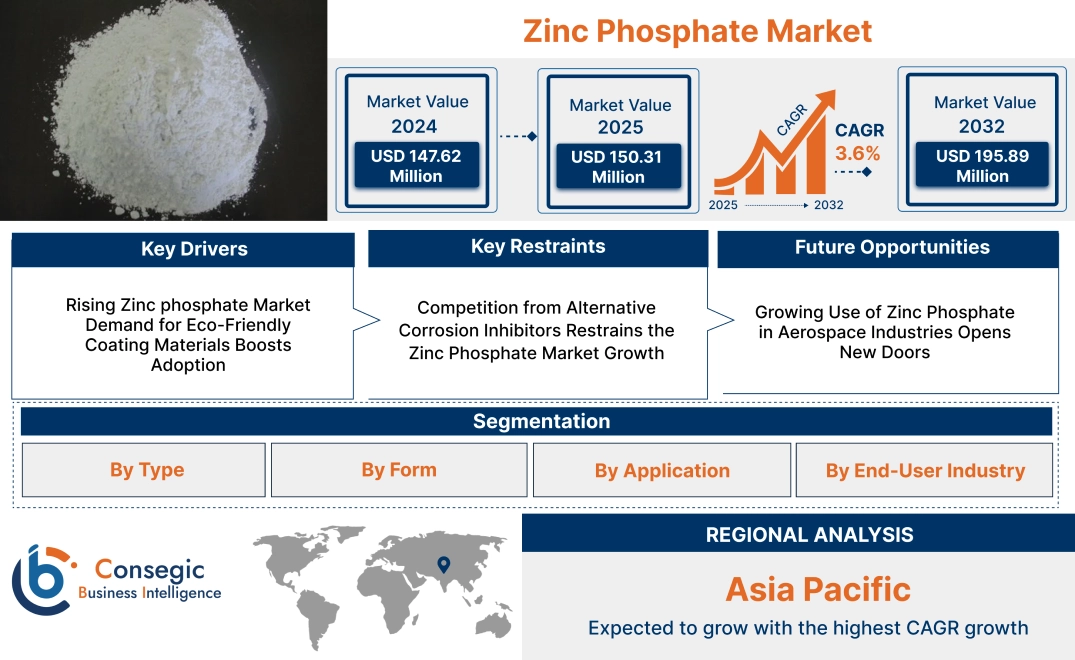

Zinc Phosphate Market Size:

Zinc Phosphate Market size is estimated to reach over USD 195.89 Million by 2032 from a value of USD 147.62 Million in 2024 and is projected to grow by USD 150.31 Million in 2025, growing at a CAGR of 3.6% from 2025 to 2032.

Zinc Phosphate Market Scope & Overview:

The zinc phosphate focuses on the production and application of zinc phosphate, a chemical compound primarily used as an anti-corrosion coating for metals and as a key component in industrial processes. This compound is widely recognized for its exceptional corrosion resistance and strong adhesion properties, making it a preferred choice in surface treatment and protective coatings. Key characteristics of this compound include its ability to enhance paint adhesion, prevent metal oxidation, and provide a durable, long-lasting finish. The benefits include extended lifespan of metal components, reduced maintenance costs, and improved product performance. Applications span automotive coatings, construction materials, industrial machinery, and marine equipment. End-users include industries such as automotive, construction, and aerospace, driven by increasing zinc phosphate market opportunities for advanced anti-corrosion solutions, expanding infrastructure projects, and advancements in coating technologies.

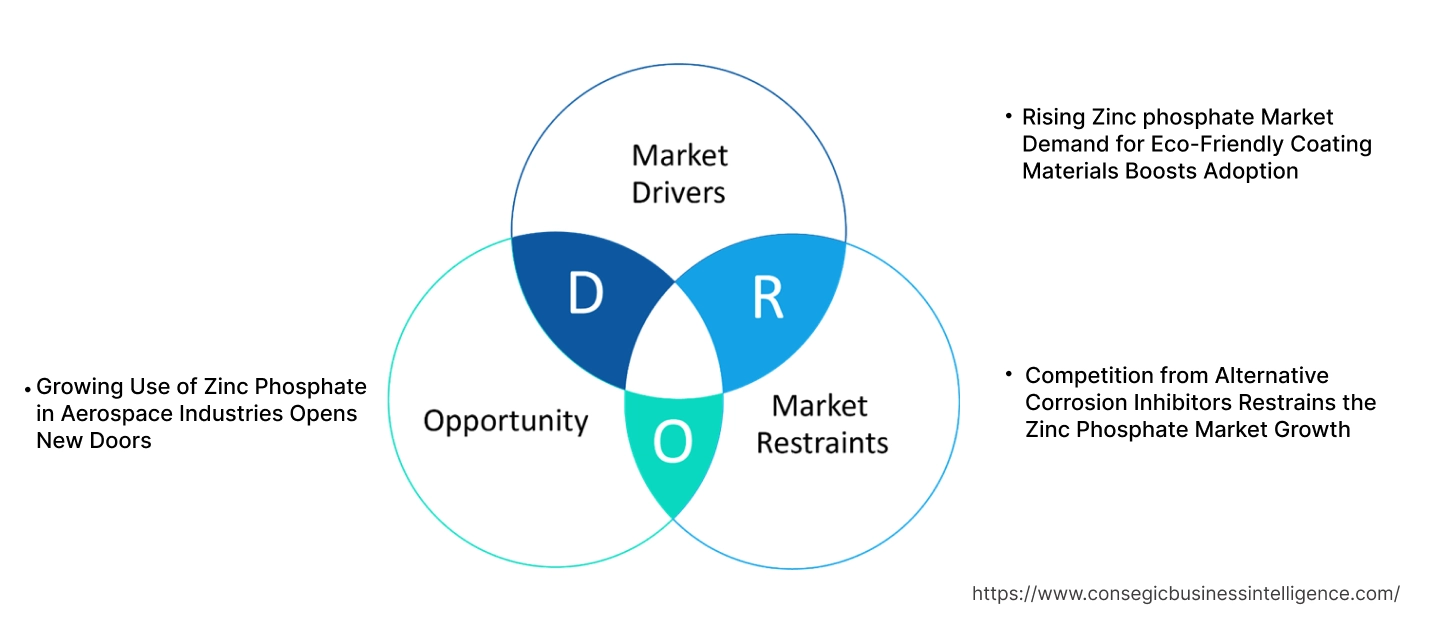

Zinc Phosphate Market Dynamics - (DRO) :

Key Drivers:

Rising Zinc phosphate Market Demand for Eco-Friendly Coating Materials Boosts Adoption

The increasing focus on environmentally sustainable practices has significantly influenced the adoption of eco-friendly coating materials, including zinc phosphate. As regulatory frameworks tighten globally to reduce the environmental impact of industrial processes, manufacturers are transitioning toward non-toxic and sustainable solutions for corrosion resistance. It is also known for its superior performance and minimal environmental footprint, aligns with these trends, particularly in industries such as automotive, construction, and marine.

Its compatibility with water-based coatings enhances its appeal, as waterborne formulations are increasingly replacing solvent-based counterparts to comply with volatile organic compound (VOC) emission standards. By offering effective corrosion prevention while adhering to environmental regulations, zinc phosphate is becoming a preferred choice for industries seeking sustainable alternatives without compromising on performance. This shift toward eco-friendly solutions is driving innovation in formulations, further strengthening its role in the coatings industry.

Key Restraints:

Competition from Alternative Corrosion Inhibitors Restrains the Zinc Phosphate Market Growth

Despite its advantages, zinc phosphate faces stiff competition from alternative corrosion inhibitors, which presents a challenge to its wider adoption. Substitutes such as calcium phosphate, modified silicates, and zinc-free coatings offer cost-effective solutions for corrosion prevention, particularly in applications where the superior properties of zinc phosphate are not essential. These alternatives are also gaining traction due to their perceived environmental benefits and lower production costs.

Industries operating under tight budget constraints often prioritize affordability over performance, opting for these alternatives to reduce overall expenses. Additionally, advancements in alternative technologies, such as graphene-based and nano-coatings, are further intensifying competition in the corrosion prevention sector. While this compound remains a benchmark for performance, its higher costs and the availability of substitutes continue to restrict its zinc phosphate market share in certain applications.

Future Opportunities:

Growing Use of Zinc Phosphate in Aerospace Industries Opens New Doors

The aerospace sector’s increasing reliance on zinc phosphate for corrosion-resistant coatings highlights its critical role in ensuring the longevity and durability of high-performance components. Aircraft structures and engine components are exposed to extreme environmental conditions, including high temperatures, humidity, and corrosive elements, necessitating robust protective solutions. Its exceptional ability to form a durable, anti-corrosive barrier on metal surfaces makes it a preferred choice for aerospace coatings.

Furthermore, the push for lightweight materials in aerospace design has amplified the need for effective coatings to protect advanced alloys and composites. Zinc phosphate’s compatibility with these materials, coupled with its performance under challenging conditions, makes it indispensable in ensuring operational safety and efficiency. As the aerospace industry continues to prioritize long-term reliability and compliance with environmental regulations, the adoption of this compound in protective coatings is expected to drive the zinc phosphate market growth.

Zinc Phosphate Market Segmental Analysis :

By Type:

Based on type, the zinc phosphate market is segmented into high zinc containing phosphate and low zinc containing phosphate.

The high zinc containing phosphate segment accounted for the largest revenue share in 2024.

- High zinc containing phosphate is extensively used in industrial coatings due to its superior corrosion resistance.

- It is preferred in applications such as automotive underbody coatings, marine coatings, and heavy machinery protection.

- The increasing trend of adopting high-performance anticorrosive solutions to extend the lifespan of assets in harsh environments is driving the demand for this segment.

- Furthermore, industries such as construction and marine are increasingly focusing on advanced coatings to meet stringent safety and durability standards.

- High zinc containing phosphate dominates the market expansion due to its excellent corrosion resistance and increasing zinc phosphate market opportunities in the adoption in industries requiring long-term asset protection.

The low zinc containing phosphate segment is anticipated to register the fastest CAGR during the forecast period.

- Low zinc containing phosphate is widely used in cost-sensitive applications where moderate corrosion protection suffices.

- Its application in general manufacturing and small-scale industrial projects supports its growth.

- The zinc phosphate market trend of balancing performance and cost in coatings is driving the use of low zinc formulations in economically driven markets.

- Low zinc containing phosphate serves cost-sensitive applications, making it a viable option for industries prioritizing affordability alongside moderate corrosion protection.

By Form:

Based on form, the market is segmented into powder and liquid.

The powder segment accounted for the largest revenue in zinc phosphate market share in 2024.

- Powdered zinc phosphate is widely utilized due to its ease of handling, storage, and application across various coating formulations.

- Its high stability and compatibility with multiple binder systems make it ideal for manufacturing anticorrosive coatings.

- The increasing advancement in powder coatings, driven by the zinc phosphate market trend of adopting eco-friendly, solvent-free coatings, has further supported this segment.

- Additionally, powdered zinc phosphate’s ability to disperse evenly in coatings enhances its effectiveness.

- According to the market analysis, powdered zinc phosphate leads the market expansion due to its compatibility with eco-friendly coatings and its extensive use in industrial applications.

The liquid segment is anticipated to register the fastest CAGR during the forecast period.

- Liquid zinc phosphate is preferred for its easy application and uniform coverage, particularly in water-based coatings.

- The rising trend of adopting water-based coatings to comply with environmental regulations and reduce volatile organic compound (VOC) emissions is driving the surge for liquid zinc phosphate.

- Its use in applications such as spray coatings and dip coating systems further highlights its versatility.

- According to the market analysis, liquid zinc phosphate is expected to grow rapidly, supported by its compatibility with water-based coatings and the increasing focus on sustainable coating solutions.

By Application:

Based on application, the market is segmented into water-based anticorrosive coatings, solvent-based anticorrosive coatings, and others.

The water-based anticorrosive coatings segment accounted for the largest revenue share in 2024.

- Water-based coatings are increasingly being adopted due to their environmental benefits, including low VOC emissions and reduced toxicity.

- Zinc phosphate plays a crucial role in enhancing the corrosion resistance of water-based coatings, making it a preferred choice for industries such as automotive and construction.

- The trend of adopting sustainable coatings to meet regulatory requirements and environmental standards is driving the appeal for zinc phosphate in water-based formulations.

- Water-based anticorrosive coatings dominate the zinc phosphate market expansion, driven by their environmental benefits and increasing adoption in sustainable industrial practices.

The solvent-based anticorrosive coatings segment is anticipated to register the fastest CAGR during the forecast period.

- Solvent-based coatings, known for their robust performance in extreme environments, continue to be used in applications such as marine and heavy machinery.

- Its ability to enhance the durability of these coatings makes it indispensable in harsh operating conditions.

- However, the shift toward environmentally friendly alternatives is gradually influencing the dynamics of this segment.

- Solvent-based coatings remain essential for extreme environments, though their zinc phosphate market demand faces gradual shifts toward sustainable alternatives.

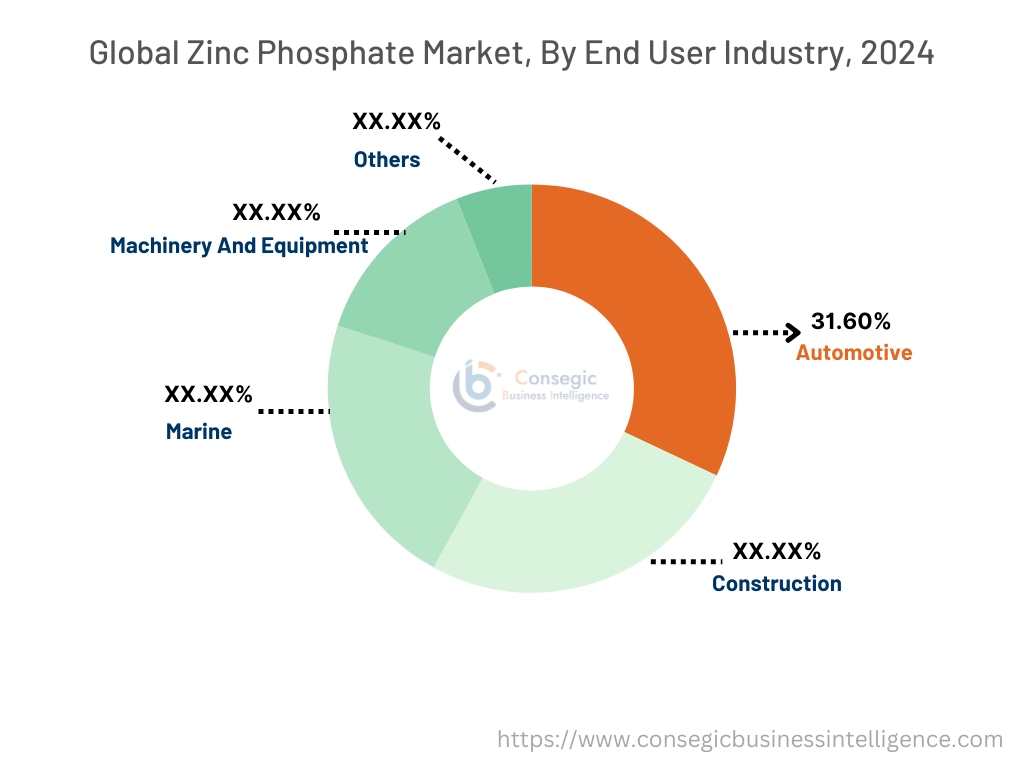

By End-User Industry:

Based on end-user industry, the market is segmented into automotive, construction, marine, machinery and equipment, and others.

The automotive segment accounted for the largest revenue share of 31.60% in 2024.

- The automotive companies relies heavily on zinc phosphate coatings to protect vehicle components from corrosion, particularly in underbody and chassis applications.

- The increasing trend of using lightweight materials such as aluminum and high-strength steel in vehicle manufacturing has further driven the need for advanced anticorrosive coatings.

- Additionally, the demand for durable coatings to meet the longevity requirements of electric vehicles (EVs) is boosting the adoption of this compound in automotive applications.

- Automotive leads the market due to the rising application for advanced corrosion protection in conventional and electric vehicle manufacturing.

The marine segment is anticipated to register the fastest CAGR during the forecast period.

- The marine sectors requires high-performance coatings to protect vessels and offshore structures from corrosion in saline environments.

- Zinc phosphate’s effectiveness in providing long-term corrosion resistance under harsh conditions makes it a critical component in marine coatings.

- The growth in trend of expanding offshore infrastructure and shipbuilding projects further supports the demand for zinc phosphate in this segment.

- The marine segment is expected to grow rapidly, driven by the increasing need for durable corrosion-resistant coatings in offshore and shipbuilding projects.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

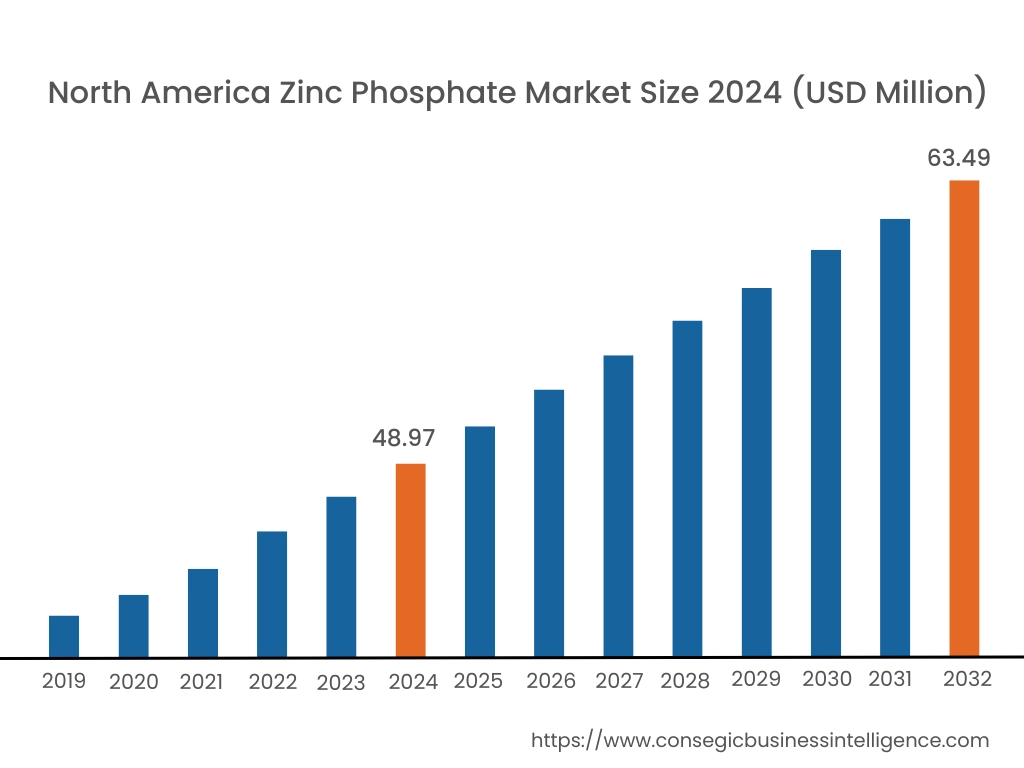

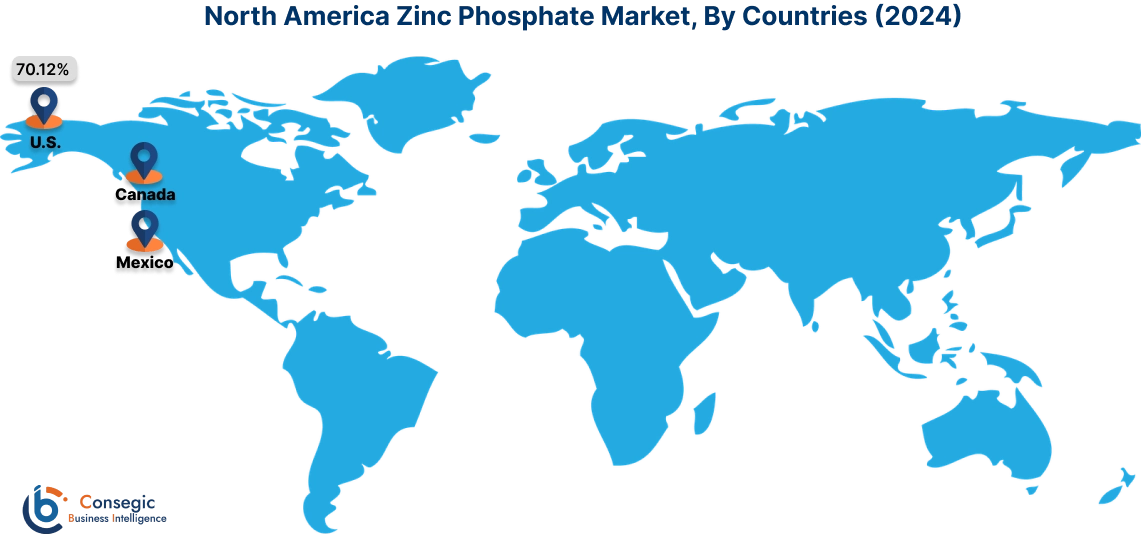

In 2024, North America was valued at USD 48.97 Million and is expected to reach USD 63.49 Million in 2032. In North America, the U.S. accounted for the highest share of 70.12% during the base year of 2024. According to the zinc phosphate market analysis, North America accounts for a substantial stake of the market, driven by its extensive application in corrosion-resistant coatings for automotive, construction, and industrial sectors. The U.S. leads the region due to widespread use in protective coatings that enhance the durability of metal components in vehicles and infrastructure. Canada contributes significantly through the utilization of this compound in the oil & gas and construction industries to safeguard metal structures. However, stringent environmental regulations surrounding phosphate-based materials present challenges to market players.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 4.0% over the forecast period. Asia-Pacific analysis depicts it is the largest and fastest-expanding region in the zinc phosphate market expansion, propelled by industrialization and the growth of automotive and construction activities in China, India, and Japan. China leads with extensive utilization in coatings for automotive production and infrastructure projects. India’s construction boom and growing preference for long-lasting, corrosion-resistant solutions boost the market’s performance. In Japan, advanced manufacturing industries and high-quality coatings for automotive and electronics applications further enhance market potential. However, environmental concerns and fluctuations in raw material availability can pose challenges in the region.

As per the zinc phosphate market analysis Europe is a prominent region, supported by its well-developed automotive and construction industries. Germany, the UK, and France are major contributors, with extensive use in protective coatings for automobiles and architectural structures. Germany’s strong automotive sector relies heavily on zinc phosphate for rust prevention, while the UK’s infrastructure modernization efforts incorporate these materials in coatings for structural longevity. France’s increasing use of eco-friendly and waterborne coatings aligns with the EU’s regulations on volatile organic compounds (VOCs). Rising costs of raw materials and strict phosphate regulations remain hurdles for manufacturers.

The Middle East & Africa region shows steady advancements in the market analysis, particularly in sectors such as oil & gas, construction, and mining. Saudi Arabia and the UAE stand out due to large-scale infrastructure projects and the need for protective coatings in harsh environments. In South Africa, mining and industrial applications are key contributors, where zinc phosphate is used to safeguard equipment and infrastructure from corrosion. Limited domestic manufacturing capabilities and reliance on imported raw materials are challenges faced by the region.

Latin America is emerging as a growing market as per the analysis, with Brazil and Mexico being key contributors. Brazil’s focus on construction and automotive industries drives the use of zinc phosphate coatings for enhancing structural durability. Mexico leverages its expanding industrial base, particularly in automotive manufacturing, where protective coatings are crucial for metal components. The region is also exploring sustainable alternatives to align with global environmental standards. Economic uncertainties and inconsistent regulatory policies in some countries, however, create barriers for market progress.

Top Key Players and Market Share Insights:

The Zinc Phosphate market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Zinc Phosphate market. Key players in the Zinc Phosphate industry include -

- Changsha Latian Chemicals Co., Ltd. (China)

- Rech Chemical Co. Ltd (China)

- Tianjin Xinxin Chemical Factory (China)

- Alpha Chemicals Private Limited (India)

- Zinc Nacional (Mexico)

- Ravi Chem Industries (India)

- Balaji Industries (India)

- Tianjin Topfert Agrochemical Co. Limited (China)

- Old Bridge Chemical, Inc. (United States)

- China Bohigh (China)

Recent Industry Developments :

Development:

- In August 2024, Henkel launched an advanced zinc phosphating technology designed to enhance corrosion resistance and improve the durability of metal coatings. This development targets industries like automotive and manufacturing, where long-lasting, rust-resistant finishes are critical. The new process provides superior performance by reducing environmental impact and increasing efficiency during application. By optimizing the phosphating treatment, Henkel's innovation supports the growing demand for sustainable and high-quality surface finishes, ensuring improved product longevity without compromising on coating effectiveness.

Zinc Phosphate Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 195.89 Million |

| CAGR (2025-2032) | 3.6% |

| By Type |

|

| By Form |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Zinc Sulfate Market by 2031? +

Zinc Phosphate Market size is estimated to reach over USD 195.89 Million by 2032 from a value of USD 147.62 Million in 2024 and is projected to grow by USD 150.31 Million in 2025, growing at a CAGR of 3.6% from 2025 to 2032.

What are the key segments in the market? +

The key segments in the Zinc Phosphate market are based on type, form, application, and end-user industry. By type, the market includes high zinc containing phosphate and low zinc containing phosphate. By form, the market is divided into powder and liquid. The application segment consists of water-based anticorrosive coatings, solvent-based anticorrosive coatings, and others. The end-user industries include automotive, construction, marine, machinery and equipment, and others.

Which segment is expected to grow the fastest in the market? +

The low zinc containing phosphate segment is anticipated to register the fastest CAGR during the forecast period. It is widely used in cost-sensitive applications where moderate corrosion protection suffices, such as general manufacturing and small-scale industrial projects, driven by the growing trend of balancing performance and cost in coatings.

Who are the major players in the market? +

Major players in the Zinc Phosphate market include Changsha Latian Chemicals Co., Ltd. (China), Rech Chemical Co. Ltd (China), Tianjin Xinxin Chemical Factory (China), Alpha Chemicals Private Limited (India), Zinc Nacional (Mexico), Ravi Chem Industries (India), Balaji Industries (India), Tianjin Topfert Agrochemical Co. Limited (China), Old Bridge Chemical, Inc. (United States), and China Bohigh (China).