- Summary

- Table Of Content

- Methodology

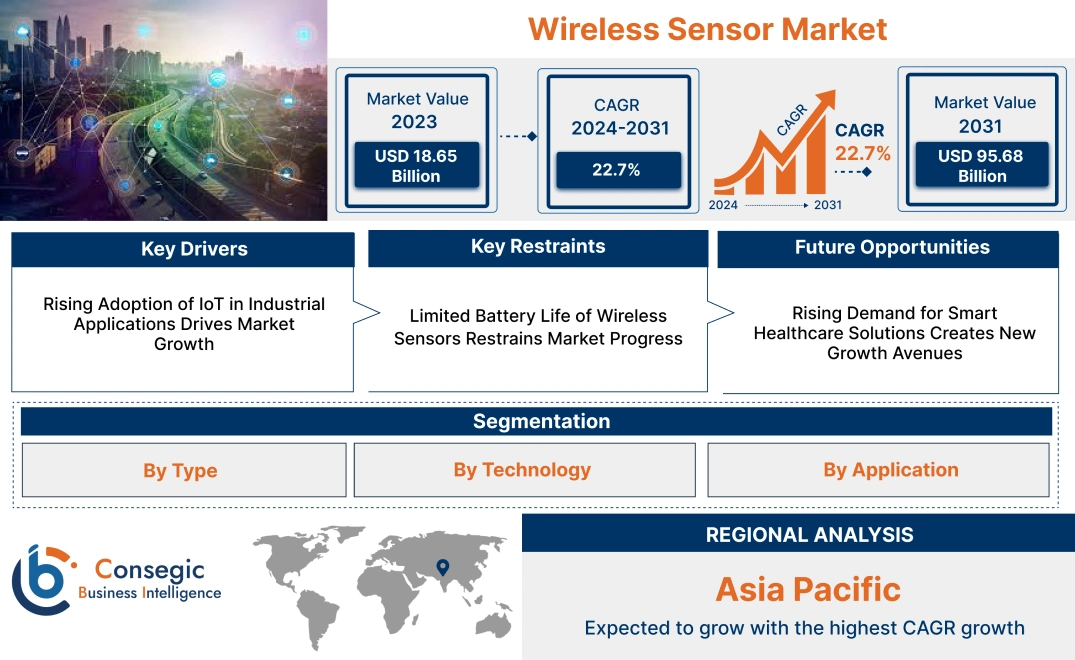

Wireless Sensor Market Size:

Wireless Sensor Market size is estimated to reach over USD 95.68 Billion by 2031 from a value of USD 18.65 Billion in 2023 and is projected to grow by USD 22.55 Billion in 2024, growing at a CAGR of 22.7% from 2024 to 2031.

Wireless Sensor Market Scope & Overview:

Wireless sensors are advanced devices designed to monitor and transmit data about environmental or physical conditions such as temperature, pressure, motion, or humidity without the need for physical connections. These sensors rely on wireless communication technologies like Bluetooth, Wi-Fi, Zigbee, and LoRaWAN to deliver real-time data to centralized systems or cloud platforms. They are widely utilized in industries including healthcare, automotive, manufacturing, and agriculture, where remote monitoring and automation are essential.

These sensors are available in various configurations, including battery-powered, energy-harvesting, and network-integrated models, catering to diverse operational requirements. They are engineered to function reliably in harsh environments, offering features such as durability, compact designs, and extended battery life. Advanced sensors also incorporate smart technologies to enable seamless integration with IoT ecosystems and provide actionable insights through data analytics.

End-users of these devices include industrial facilities, healthcare providers, smart home system integrators, and agricultural operators. Wireless sensors are critical for ensuring operational efficiency, enhancing safety, and enabling automation across a wide range of applications.

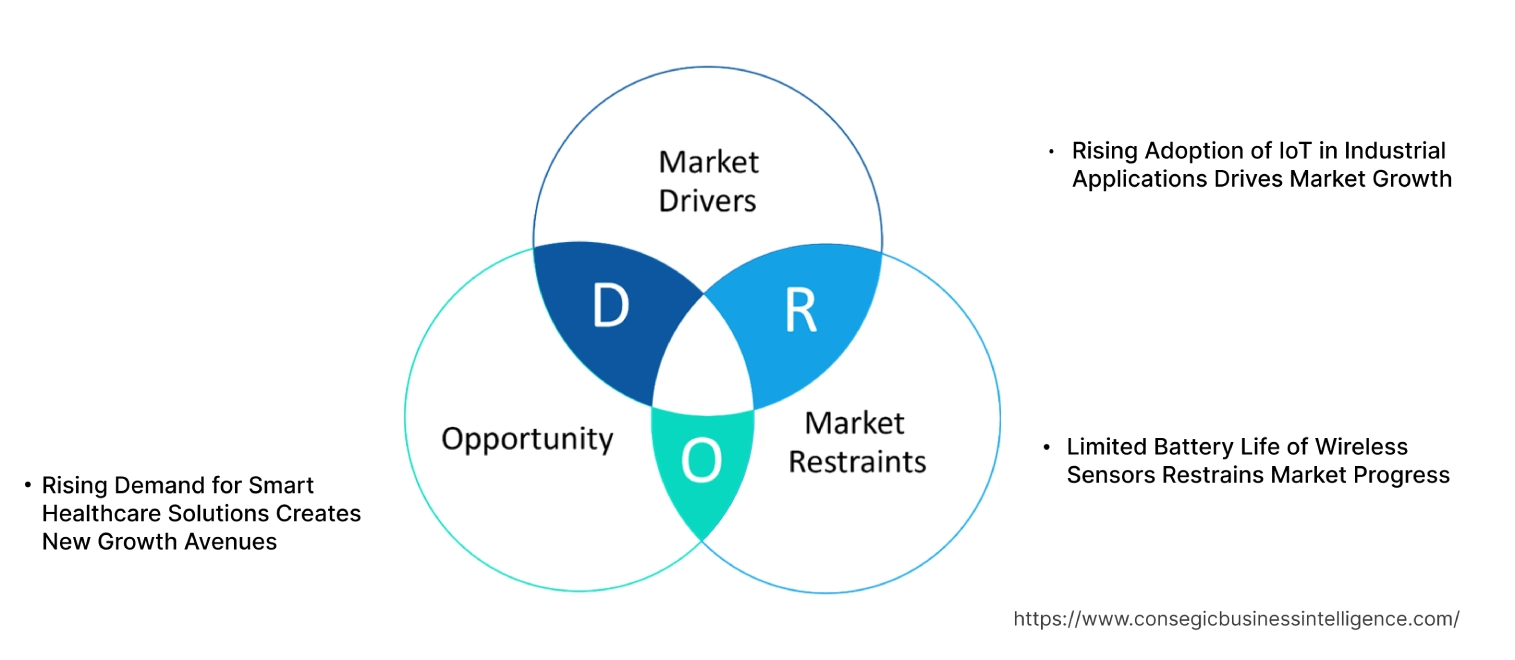

Wireless Sensor MarketDynamics - (DRO) :

Key Drivers:

Rising Adoption of IoT in Industrial Applications Drives Market Growth

The integration of IoT (Internet of Things) into industrial operations is revolutionizing efficiency, making wireless sensors a critical component. Industries like manufacturing, oil & gas, and utilities are deploying IoT-enabled sensors for real-time monitoring of machinery performance, environmental conditions, and operational metrics. These sensors eliminate the need for complex wiring, enabling seamless data transmission even in challenging industrial environments. They play a key role in predictive maintenance, allowing operators to identify potential equipment failures before they occur, reducing downtime and maintenance costs.

Additionally, they support smart manufacturing initiatives, where real-time data drives automation and process optimization. As IoT applications expand, trends such as remote monitoring and digital twins are further accelerating demand for wireless sensors, positioning them as essential tools for achieving operational excellence in modern industrial ecosystems. This growth is expected to intensify as industries prioritize data-driven decision-making and connectivity, contributing to the wireless sensor market demand.

Key Restraints :

Limited Battery Life of Wireless Sensors Restrains Market Progress

The reliance on batteries for powering wireless sensors presents significant constraints, especially in remote or inaccessible locations where regular maintenance is difficult and costly. Frequent battery replacements or recharging disrupt operations, particularly in industries such as oil & gas, agriculture, and infrastructure monitoring, where continuous functionality is critical. These disruptions increase operational costs and reduce the overall efficiency of sensor networks.

Although advancements in low-power consumption technologies and energy harvesting solutions are improving battery life, current energy efficiency levels still fall short for applications demanding extended operational lifetimes. For instance, long-term environmental monitoring or industrial IoT systems often require sensors to function autonomously for years, a goal that remains difficult to achieve with existing battery technologies. These limitations in power efficiency restrict the scalability and adoption of wireless sensors in large-scale or long-duration deployments, particularly in cost-sensitive or resource-constrained applications, hampering the wireless sensor market growth.

Future Opportunities :

Rising Demand for Smart Healthcare Solutions Creates New Growth Avenues

Wireless sensors are transforming the healthcare sector by enabling real-time health tracking, remote patient monitoring, and seamless data transmission to healthcare providers. These sensors are critical for applications such as wearable health devices, implantable sensors, and diagnostic tools, providing continuous monitoring of vital signs like heart rate, blood pressure, and glucose levels. Their ability to transmit data in real time enhances patient outcomes by allowing timely medical intervention and personalized care.

The growing adoption of telehealth services further drives the demand for sensors, as they facilitate remote consultations and chronic disease management. Additionally, in hospital settings, these sensors are used for equipment monitoring and environmental control, improving operational efficiency and reducing manual intervention. As the healthcare sector embraces digital transformation, wireless sensors are becoming indispensable for modern healthcare systems, meeting the rising demand for advanced, connected, and patient-centric solutions, creating significant wireless sensor market opportunities.

Wireless Sensor Market Segmental Analysis :

By Type:

Based on type, the market is segmented into Temperature Sensors, Pressure Sensors, Level Sensors, Motion Sensors, Gas Sensors, and Others.

The Temperature Sensors segment held the largest revenue of the total wireless sensor market share in 2023.

- Temperature sensors are extensively used in industrial automation, HVAC systems, and healthcare monitoring, where precise temperature regulation is critical.

- These sensors play a vital role in cold chain monitoring for food storage and pharmaceuticals, ensuring product safety and compliance.

- Technological advancements in wireless temperature sensors, including energy-efficient designs, are driving their adoption in smart home devices.

- As per the market analysis, trends indicate that increased integration of temperature sensors in IoT-based solutions across various sectors drives the wireless sensor market expansion.

The Motion Sensors segment is expected to register the fastest CAGR during the forecast period.

- Motion sensors are widely utilized in security systems, automotive applications, and smart home automation to detect movement and enhance safety.

- The rising adoption of wireless motion sensors in fitness wearables and gaming devices is boosting their usage in consumer electronics.

- These sensors enable touchless interfaces and gesture controls, supporting innovative applications in healthcare and retail environments.

- As per wireless sensor market analysis, the rapid growth of this segment reflects its importance in applications requiring real-time movement detection and precision.

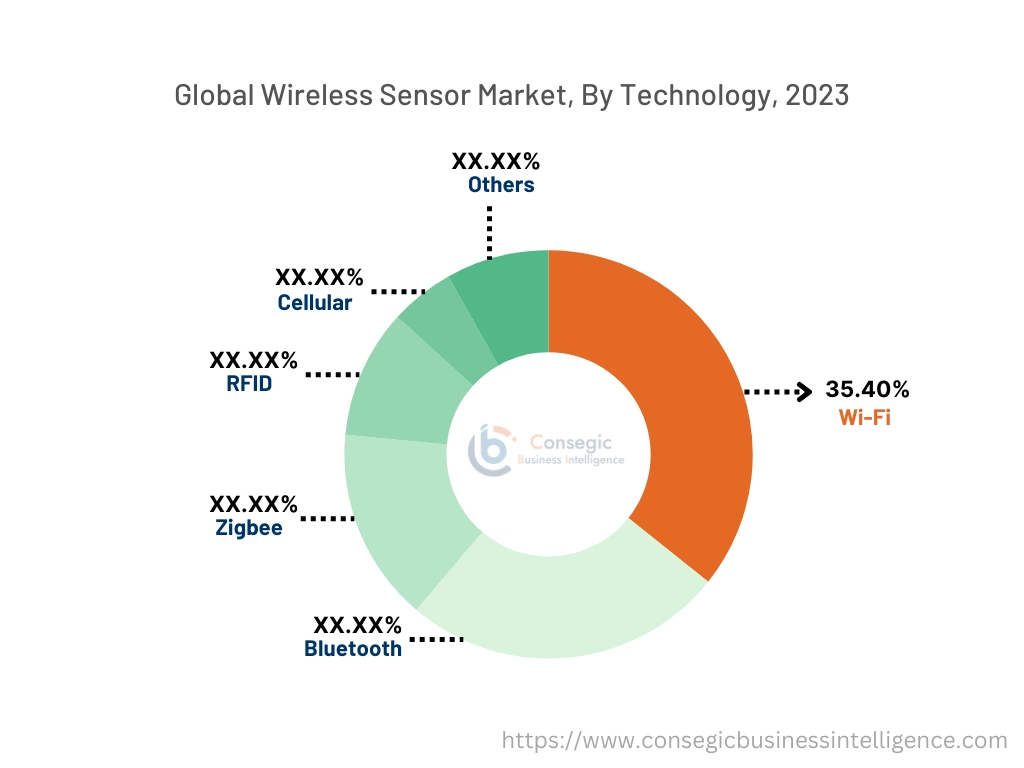

By Technology:

Based on technology, the market is segmented into Bluetooth, Wi-Fi, Zigbee, RFID, Cellular, and Others.

The Wi-Fi segment held the largest revenue of 35.40% of the total wireless sensor market share in 2023.

- Wi-Fi-enabled sensors provide high-speed and reliable connectivity, making them ideal for industrial monitoring, environmental control, and smart buildings.

- These sensors are widely used in applications requiring continuous data transmission, such as healthcare monitoring and smart grid systems.

- Trends in IoT adoption and the increasing need for centralized control systems are driving the preference for Wi-Fi-based wireless sensors.

- As per wireless sensor market trends, the dominance of this segment is attributed to its ability to integrate seamlessly with existing networks, enabling efficient data management.

The Bluetooth segment is expected to register the fastest CAGR during the forecast period.

- Bluetooth-based sensors are known for their low power consumption and short-range communication, making them ideal for wearables and personal healthcare devices.

- These sensors are increasingly integrated into fitness trackers, smartwatches, and hearing aids, supporting advancements in consumer health and wellness.

- The rapid adoption of Bluetooth technology in home automation systems is driving the development of compact and energy-efficient sensors.

- As per market trends, Bluetooth technology continues to gain traction in applications requiring lightweight, portable, and user-friendly solutions further fueling the wireless sensor market growth.

By Application:

Based on application, the market is segmented into Industrial Automation, Environmental Monitoring, Healthcare Monitoring, Home Automation, Security Systems, and Others.

The Industrial Automation segment accounted for the largest revenue share in 2023.

- Wireless sensors are essential in industrial automation for monitoring equipment performance, detecting faults, and ensuring operational efficiency.

- These sensors enable predictive maintenance and real-time process control, reducing downtime and enhancing productivity in manufacturing facilities.

- Trends in Industry 4.0 and smart factory initiatives are driving the integration of these sensors in industrial systems.

- The dominance of this segment highlights its critical role in supporting automated workflows and data-driven decision-making boosting the wireless sensor market demand.

The Healthcare Monitoring segment is expected to register the fastest CAGR during the forecast period.

- Wireless sensors are widely used in healthcare applications, including patient monitoring, wearable devices, and diagnostic tools, to ensure accurate and real-time data collection.

- These sensors enable remote health monitoring, reducing the need for frequent hospital visits and improving patient outcomes.

- The segment's steady growth is supported by the increasing adoption of telemedicine and IoT-enabled medical devices in healthcare systems.

- Therefore, the market analysis emphasizes the role of wireless sensors in advancing personalized medicine and improving healthcare accessibility, which drives the wireless sensor market expansion.

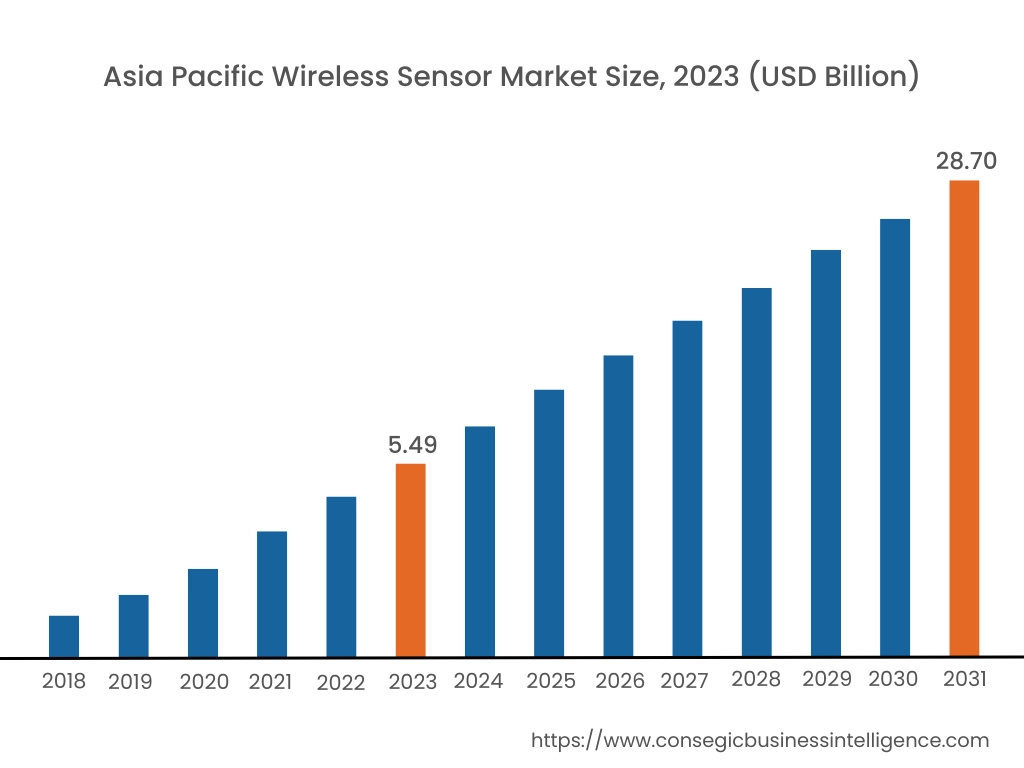

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

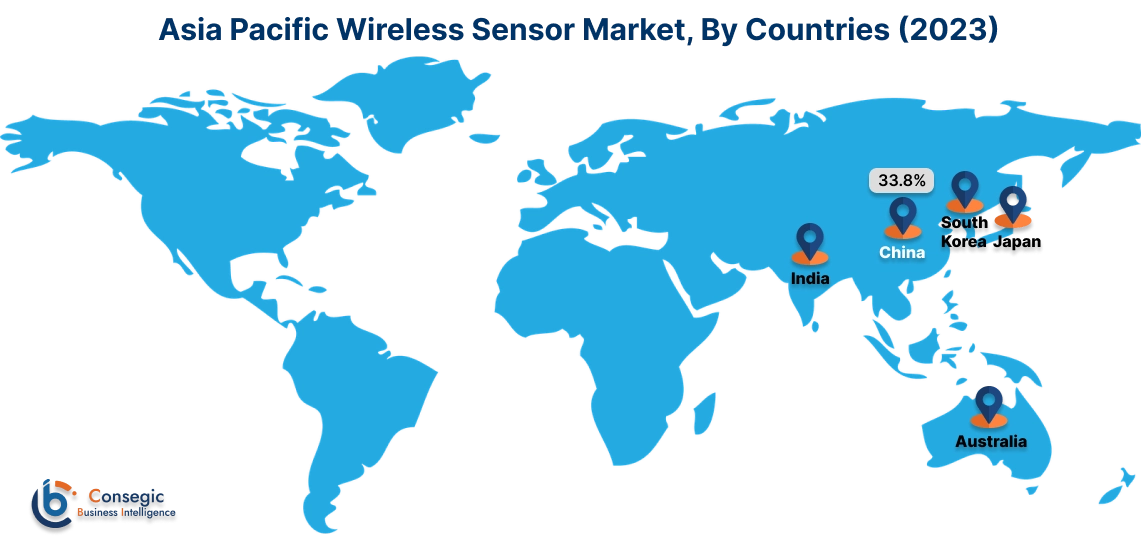

Asia Pacific region was valued at USD 5.49 Billion in 2023. Moreover, it is projected to grow by USD 6.64 Billion in 2024 and reach over USD 28.70 Billion by 2031. Out of these, China accounted for the largest share of 33.8% in 2023. The Asia-Pacific region is experiencing rapid advancements in the wireless sensor market, driven by industrialization and infrastructural development in countries like China, India, and Japan. The expansion of consumer electronics, automotive industries, and smart city projects has led to increased adoption of wireless sensors to ensure connectivity and efficiency. Technological advancements and government initiatives promoting digitalization further influence wireless sensor market opportunities.

North America is estimated to reach over USD 31.48 Billion by 2031 from a value of USD 6.20 Billion in 2023 and is projected to grow by USD 7.49 Billion in 2024. This region maintains a significant position in the wireless sensor market, primarily due to the early adoption of innovative technologies and a robust industrial sector. The United States, in particular, has integrated wireless sensors extensively across industries such as manufacturing, healthcare, and automotive. The trend towards the Internet of Things (IoT) and smart infrastructure has further propelled the utilization of these sensors for enhanced operational efficiency and data analytics.

Europe represents a substantial share of the global wireless sensor market, with countries like Germany, France, and the United Kingdom at the forefront. The region's strong emphasis on sustainability and energy efficiency has driven the adoption of wireless sensors in applications such as smart grids, environmental monitoring, and building automation. The wireless sensor market analysis indicates a growing inclination towards wireless sensor networks that support Industry 4.0 initiatives, aiming for increased automation and data exchange in manufacturing technologies.

The Middle East & Africa region shows a growing interest in wireless sensor technologies, particularly in the oil & gas, construction, and healthcare sectors. Countries like Saudi Arabia and the United Arab Emirates are investing in smart infrastructure projects, necessitating the use of wireless sensors for monitoring and automation. The analysis suggests that the adoption of wireless sensor networks is gradually increasing, supported by technological advancements and a focus on operational excellence.

Latin America is an emerging market for wireless sensors, with Brazil and Mexico being key contributors. The region's industrial sector, including manufacturing and agriculture, is adopting these technologies to enhance productivity and sustainability. As per wireless sensor market trends, government initiatives aimed at modernizing industrial operations and improving infrastructure influence market trends.

Top Key Players & Market Share Insights:

The Wireless Sensor market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Wireless Sensor market. Key players in the Wireless Sensor industry include –

- Honeywell International Inc. (USA)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- Emerson Electric Co. (USA)

- General Electric Company (USA)

- Bosch Sensortec GmbH (Germany)

- TE Connectivity Ltd. (Switzerland)

- Analog Devices, Inc. (USA)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

Recent Industry Developments :

Product Launches:

- In January 2024, Nozomi Networks launched the industry's first multi-spectrum wireless security sensor, designed for operational technology (OT) and Internet of Things (IoT) environments. This innovation provides comprehensive visibility and enhanced threat detection across global industrial and IoT networks. The sensor combines multi-band monitoring capabilities to detect and analyze wireless threats, ensuring robust security in critical infrastructure. It supports deployment in diverse environments, aligning with Nozomi's focus on advanced cybersecurity solutions tailored for OT and IoT landscapes.

- In February 2024, A2Z Imaging unveiled its DUO Wireless-Ready Sensor, aimed at improving dental x-ray quality, convenience, and patient comfort. This sensor offers both direct-connected and wireless capabilities, with the unique QuickSwap™ Replaceable Cable, allowing easy replacement of damaged cables to reduce repair costs. The sensor is available in two sizes, ensuring comfort for all patients, and features a durable design with advanced CMOS technology for detailed imaging.

Wireless Sensor Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 95.68 Billion |

| CAGR (2024-2031) | 22.7% |

| By Type |

|

| By Technology |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Wireless Sensor Market? +

Wireless Sensor Market size is estimated to reach over USD 95.68 Billion by 2031 from a value of USD 18.65 Billion in 2023 and is projected to grow by USD 22.55 Billion in 2024, growing at a CAGR of 22.7% from 2024 to 2031.

What specific segmentation details are covered in the Wireless Sensor Market report? +

The Wireless Sensor Market report includes segmentation details by type (Temperature Sensors, Pressure Sensors, Level Sensors, Motion Sensors, Gas Sensors, Others), technology (Bluetooth, Wi-Fi, Zigbee, RFID, Cellular, Others), Application (Industrial Automation, Environmental Monitoring, Healthcare Monitoring, Home Automation, Security Systems, Others), and region (Asia-Pacific, Europe, North America, Latin America, Middle East & Africa).

Which is the fastest-growing segment in the Wireless Sensor Market? +

The Bluetooth segment is expected to register the fastest CAGR during the forecast period. Bluetooth-based sensors are increasingly integrated into wearables, smartwatches, and healthcare devices due to their low power consumption and short-range communication capabilities.

Who are the major players in the Wireless Sensor Market? +

The major players in the Wireless Sensor Market include Honeywell International Inc. (USA), Siemens AG (Germany), Schneider Electric SE (France), Emerson Electric Co. (USA), General Electric Company (USA), Bosch Sensortec GmbH (Germany), TE Connectivity Ltd. (Switzerland), Analog Devices, Inc. (USA), NXP Semiconductors N.V. (Netherlands), and STMicroelectronics N.V. (Switzerland).