- Summary

- Table Of Content

- Methodology

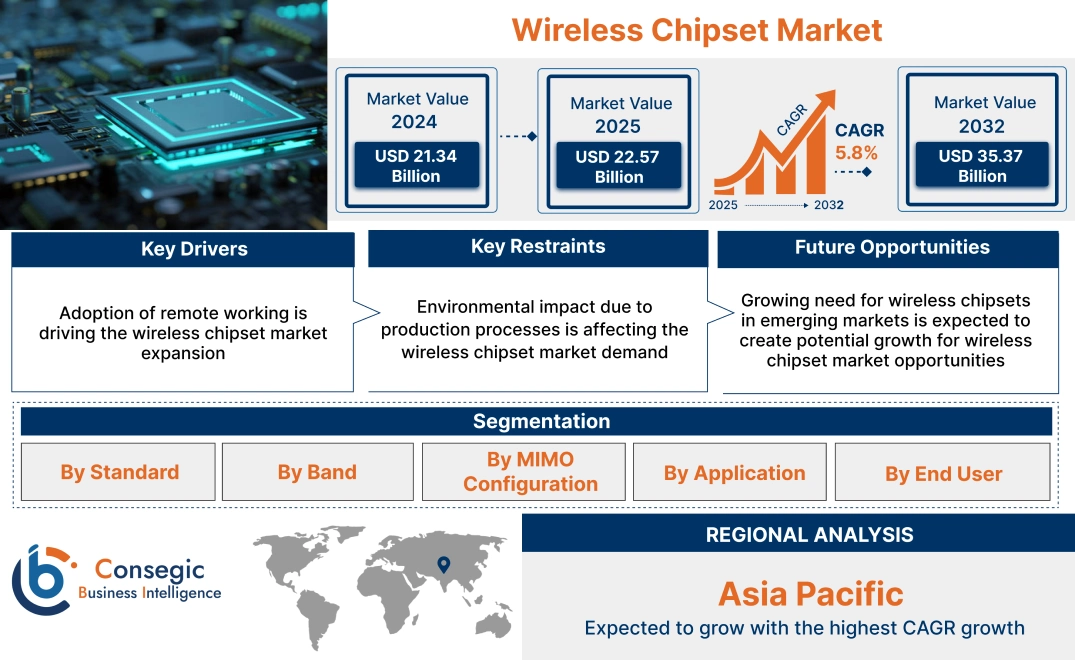

Wireless Chipset Market Size:

Wireless Chipset Market Size is estimated to reach over USD 35.37 Billion by 2032 from a value of USD 21.34 Billion in 2024 and is projected to grow by USD 22.57 Billion in 2025, growing at a CAGR of 5.8% from 2025 to 2032.

Wireless Chipset Market Scope & Overview:

Wireless chipsets are essential components that facilitate wireless communication in devices such as smartphones, tablets, laptops, and IoT devices. The rapid growth of IoT devices significantly contributes to market expansion, as these devices rely on wireless connectivity for communication and data sharing. This reliance creates a demand for reliable and power-efficient chipsets that support their functionality. Various industries, including healthcare and automotive, are adopting IoT solutions, increasing the need for specialized wireless chipsets that meet their specific requirements. A key factor driving market growth is the rising demand for high-speed internet and seamless connectivity, leading to the development of advanced wireless standards like Wi-Fi 6 and 5G. These standards demand sophisticated chipsets capable of efficiently managing complex data transmission and reception tasks. Consequently, semiconductor manufacturers are continually innovating to create chipsets that provide enhanced performance, reduced power consumption, and compatibility with multiple frequency bands.

Wireless Chipset Market Dynamics - (DRO) :

Key Drivers:

Adoption of remote working is driving the wireless chipset market expansion

The global market has experienced substantial growth, largely driven by the widespread adoption of remote work trends. As businesses and individuals increasingly depend on wireless connectivity for effective communication and productivity, the demand for efficient, high-performance wireless chipsets has risen significantly. These chipsets are essential for various wireless devices, including smartphones, laptops, routers, and IoT devices, enabling reliable connections to Wi-Fi, Bluetooth, and other wireless networks. The progression of the wireless chipset market is further fueled by the rise of smart devices and the introduction of 5G technology. As industries undergo digital transformation and IoT ecosystems expand, the need for advanced wireless connectivity solutions that support higher data speeds and more connected devices simultaneously is growing. Consequently, companies in the wireless chipset sector are heavily investing in research and development to meet these evolving needs and take advantage of the market opportunities generated by remote work and digitalization trends.

- For instance, in December 2024, Apple planned to switch to a home-based chip for Wi-Fi connections for its devices. The chip, named Proxima, will be slated into smart home devices and iPhones. In addition to this, the chips will be developed by Taiwan Semiconductor Manufacturing Co in 2025.

Thus, according to the wireless chipset market analysis and trends, the growing adoption of remote working is driving the wireless chipset market size and industry.

Key Restraints:

Environmental impact due to production processes is affecting the wireless chipset market demand

The production of wireless chipsets entails various resource-intensive processes, particularly semiconductor manufacturing. This sector is notable for its significant energy consumption and dependence on rare earth metals and other raw materials. Extracting and processing these resources can result in environmental degradation and increased carbon emissions. The growing number of wireless devices utilizing these chipsets generates more electronic waste (e-waste). As new technologies rapidly replace older ones, outdated devices frequently end up in landfills or are improperly recycled, which poses risks of chemical leaching and environmental contamination. Additionally, the operational phase of wireless devices, powered by these chipsets, results in energy consumption that includes not just the devices but also the necessary infrastructure to support wireless networks. The continuous energy demands for network operation and data transmission further contribute to the overall environmental impact of the wireless chipset industry. Thus, the above factors are affecting the wireless chipset market.

Future Opportunities :

Growing need for wireless chipsets in emerging markets is expected to create potential growth for wireless chipset market opportunities

Emerging markets are essential to the growth of the global market. These areas, marked by rapid urbanization, rising disposable incomes, and developing digital infrastructure, are experiencing a significant increase in smart device adoption. As more consumers in these regions gain access to affordable smartphones and other connected devices, the need for efficient and cost-effective Wi-Fi chipsets grows. Additionally, government initiatives aimed at enhancing internet connectivity and digital literacy further support market development. The ongoing rollout of 5G networks and the growing ecosystem of IoT devices are anticipated to sustain this growth, positioning wireless chipsets as a critical element in the future of global connectivity.

- For instance, in January 2025, C-DOT announced the collaboration with IIT Bombay, to develop chipsets for high-bandwidth 6G wireless links. This technology seeks to improve India’s status in last-mile network connectivity in areas with limited network access, such as mountains, rugged terrains, and rural regions. It will deliver seamless and uninterrupted high-bandwidth communication links to remote locations through satellite technology. This will be particularly beneficial in scenarios where deploying or laying optical fibers is difficult. The agreement has been signed under the Telecom Technology Development Fund (TTDF).

Thus, based on the above analysis and trends, growing need for Wi-Fi chipset in emerging economies are driving the wireless chipset market opportunities.

Wireless Chipset Market Segmental Analysis :

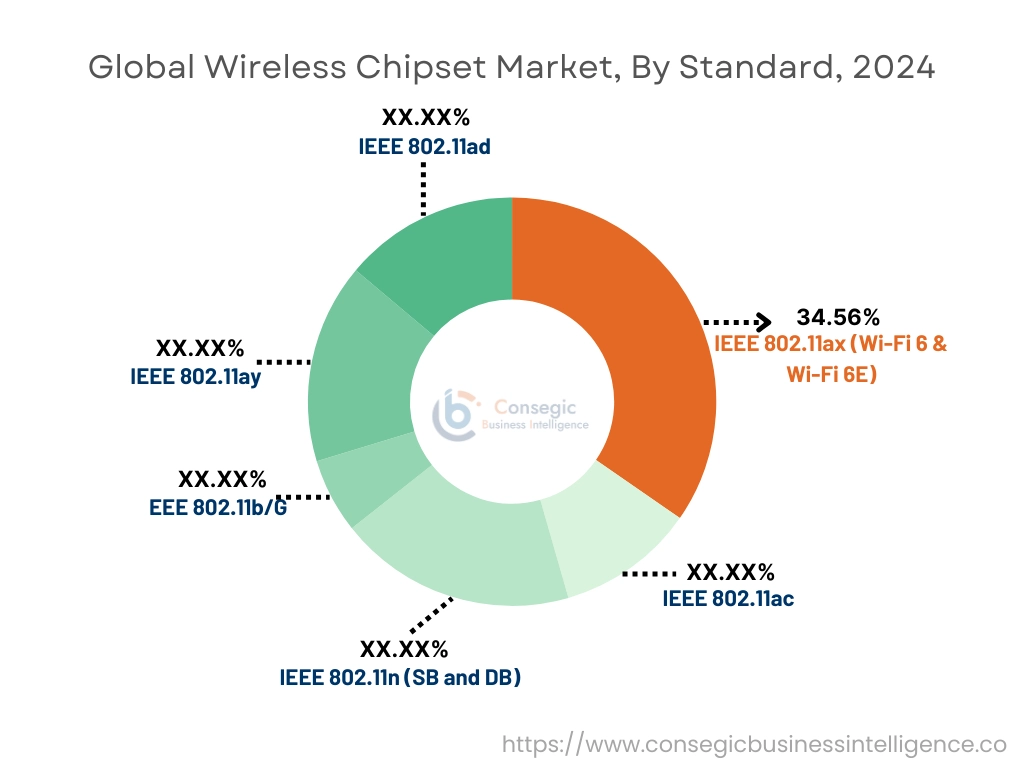

By Standard:

Based on standard, the wireless chipset market is segmented into IEEE 802.11ay, IEEE 802.11ad, IEEE 802.11ax (Wi-Fi 6 & Wi-Fi 6E), IEEE 802.11ac, IEEE 802.11n (SB and DB), and EEE 802.11b/G.

Trends in the standard:

- Wi-Fi, the leading technology in local wireless networking, has become a standard for internet access in homes, offices, and public areas. Its development has seen considerable advancements in speed, capacity, and efficiency.

- The anticipation for Wi-Fi 7 is growing, with expectations of even greater speeds and enhanced performance. This will increase the need for new chipsets that accommodate the latest standard.

- The deployment of 5G networks is ongoing, with attention now directed towards expanding coverage, enhancing performance, and investigating future developments in cellular technology, like 6G.

The IEEE 802.11ax (Wi-Fi 6 & Wi-Fi 6E) segment accounted for the largest share of 34.56% in the year 2024 and is expected to register the highest CAGR during the forecast period.

- Wi-Fi 6/6E brings significant enhancements compared to earlier generations, such as increased speeds, greater capacity, lower latency, and improved performance in crowded settings. These benefits are accelerating adoption across multiple sectors.

- The number of Wi-Fi 6/6E certified devices, including smartphones, laptops, tablets, access points, and routers, is rapidly growing, further driving the global market.

- Wi-Fi 6E operates on the 6 GHz band, which provides much more spectrum than the 2. 4 GHz and 5 GHz bands used by prior Wi-Fi generations. This additional spectrum results in higher speeds, less congestion, and better performance, especially in densely populated areas.

- For instance, Wi-Fi 6 routers enhance wireless performance in various scenarios, including homes with smart devices (such as thermostats and security cameras) or older equipment that may hinder network speed, as well as households experiencing streaming issues or those situated near many other routers and devices.

- Thus, based on aforementioned trends and advancements in Wi-Fi 6 technology would further drive the wireless chipset market size and industry during the forecast period.

By Band:

Based on band, the market is segmented into thermal single, dual, and tri.

Trends in band:

- The availability of the 6 GHz band is revolutionary, particularly for Wi-Fi 6E. It offers essential spectrum relief and facilitates new applications.

- There is a notable trend towards combining various wireless technologies (Wi-Fi, Bluetooth, Zigbee/Thread) into a single chip to lower cost and power consumption.

The dual band segment accounted for the largest revenue in the year 2024 and is expected to register the highest CAGR during the forecast period.

- Dual-band Wi-Fi routers represent the largest value share in the global Wi-Fi chipset market due to their extensive coverage, capacity to connect multiple devices, exceptional performance, and flexibility across two independent networks 2. 4 GHz and 5 GHz. Their lower interference with devices on different networks minimizes the likelihood of disruptions, facilitated by the use of 11 channels on the 2. 4 GHz band and 23 channels on the 5 GHz band.

- Dual-band Wi-Fi routers offer a combined bandwidth of 1.9 Gbps, comprising 600 Mbps from the 2. 4 GHz band and 1. 3 Gbps from the 5 GHz band. The IEEE 802. 11n (Wi-Fi 4) standard introduced the 5 GHz frequency band to enhance wireless speeds to a minimum of 450 Mbps while ensuring backward compatibility. Furthermore, the advent of IEEE 802. 11ac (Wi-Fi 5) has enabled data transmission speeds of up to 1.3 Gbps.

- Thus, the need for high-definition streaming services grows, the need for a stable and high-performance Wi-Fi connection also rises, reinforcing the necessity for dual-band Wi-Fi and driving the wireless chipset market growth.

By MIMO Configuration:

Based on the MIMO configuration, the wireless chipset market is segmented into SU-MIMO and MU-MIMO

Trends in the MIMO configuration:

- Modern chipsets consolidate multiple functions, including Wi-Fi, Bluetooth, and cellular connectivity, onto a single chip. This leads to lower costs, reduced volume, and decreased power consumption.

- The advancements in chip design, antenna technology, and signal processing are facilitating the creation of more powerful and efficient wireless systems.

The MU-MIMO segment accounted for the largest revenue share in the year 2024 and is expected to register the highest CAGR during the forecast period.

- The integration and use of MU-MIMO have been key differentiators in the Wi-Fi IEEE 802. 11ac Wave 1 and Wave 2 standards. This configuration allows multiple users to connect to Wi-Fi simultaneously and provides high-capacity internet access from fixed networks. The technology is designed to transmit multiple streams to various Wi-Fi devices (with single or multiple antennas), enabling connections to both small and large devices.

- Contemporary chipsets are incorporating MU-MIMO along with other features such as Wi-Fi 6/6E, Bluetooth, and cellular connectivity. This combination reduced power consumption, while enhancing the accessibility of MU-MIMO in diverse devices.

- MU-MIMO depends significantly on beamforming to send signals to specific devices. Chipsets are now employing more sophisticated beamforming algorithms to boost accuracy and efficiency, particularly in challenging environments.

- Users expect dependable and consistent Wi-Fi performance throughout their homes or offices. MU-MIMO contributes to this by alleviating congestion and latency.

- These needs for high bandwidth and exploding number of connected devices would further drive the wireless chipset market share during the forecast period.

By Application:

Based on the application, the market is segmented into smartphones, tablet, desktops, laptop, connected home devices, image processing, mobile robots, medical systems, data systems, in-vehicle infotainment, and others.

Trends in the application:

- Ongoing advancements in semiconductor technology, including smaller process nodes and new materials, are facilitating the creation of more powerful and efficient chipsets.

- The rapid development of IoT devices is significantly driving innovation in Wi-Fi chipsets. These chipsets are being tailored to fulfill the specific requirements of IoT applications, such as low power consumption, extended range, and compatibility with various communication protocols.

The smartphone segment accounted for the largest revenue share in the year 2024.

- The increase in global smartphone adoption and the spread of high-speed internet connectivity is anticipated to fuel the progression of Wi-Fi chipsets for smartphone applications.

- According to GSMA, global smartphone adoption is projected to rise to over 91% by 2030, up from over 78% in 2023. As consumers seek reliable and fast wireless communication for their smartphones, the market for Wi-Fi chipsets will see substantial development during the forecast period. Emerging markets, where smartphones are becoming the main sources of internet access, are also contributing to the rising need for Wi-Fi chipsets.

- For instance, in February 2024, Qualcomm launched Wi-Fi7 chip for smartphones. The chip achieved an impressive peak data rate of 5. 8 Gbps. Additionally, it features proximity capabilities with Wi-Fi, Bluetooth audio, and ultra-wideband.

- Thus, based on the above factors and analysis, the market will grow during the forecast period.

The medical system segment is anticipated to register the fastest CAGR during the forecast period.

- Medical devices are shrinking in size and becoming more portable, necessitating highly integrated and energy-efficient Wi-Fi chipsets.

- Numerous medical applications require real-time data transmission for prompt diagnosis and intervention. Chipsets are being developed to reduce latency and guarantee reliable data delivery.

- Medical devices and systems must communicate flawlessly. Chipsets are facilitating standard communication protocols to ensure interoperability and data exchange.

- The rising need for remote patient monitoring and telemedicine is propelling the creation of Wi-Fi chipsets tailored for these applications.

- Thus, based on the above factors and developments, the market will grow during the forecast period.

By End Use:

Based on end use, the wireless chipset market is segmented into consumer electronics, automotive, healthcare, BFSI, retail, education, and others.

Trends in the end use:

- The growing consumer need for online gaming and video streaming leading to a heightened need for high-speed Wi-Fi services. Wi-Fi chipsets can enable smooth data transfer for online gaming and high-definition streaming, thereby fostering market during the forecast period.

- Wi-Fi chipset manufacturers should develop latency-optimized chipsets aimed specifically at gaming console and AR/VR device manufacturers, as the adoption of AR/VR devices is anticipated to rise in the coming years.

- These factors, analysis, and advancements in the applications of Wi-Fi chipsets would further drive the market trends during the forecast period.

The consumer electronics segment accounted for the largest revenue share in the year 2024 and is expected to register the highest CAGR during the forecast period.

- Corporate employees are engaging with clients and colleagues through video meetings, learning via streaming videos, and utilizing various cloud applications. This necessitates high-speed internet connectivity, leading to an increased adoption of Wi-Fi routers and Wi-Fi 6, 6E, and 7 enabled devices like laptops.

- The rapidly rising requirement for modern devices that support new wireless frequency bands, including 2. 4GHz, 5GHz, and 6GHz, is expected to further drive the adoption of Wi-Fi 6 chipsets. Additionally, incorporating BSS coloring features in chipset technology will improve network reliability in densely populated environments by allowing frames from neighbouring networks, which helps reduce interference and enhance network speed.

- For instance, Broadcom’s BCM4389 provides real-world speeds exceeding 2 Gbps and offers up to 5 times improved battery efficiency, making it an outstanding option for future Augmented Reality/Virtual Reality (AR/VR) devices and premium smartphones. The advantages of this new chipset technology over older wireless standards are anticipated to drive its significant adoption in the coming years.

- These advancements in consumer electronics segment would further drive the market during the forecast period.

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

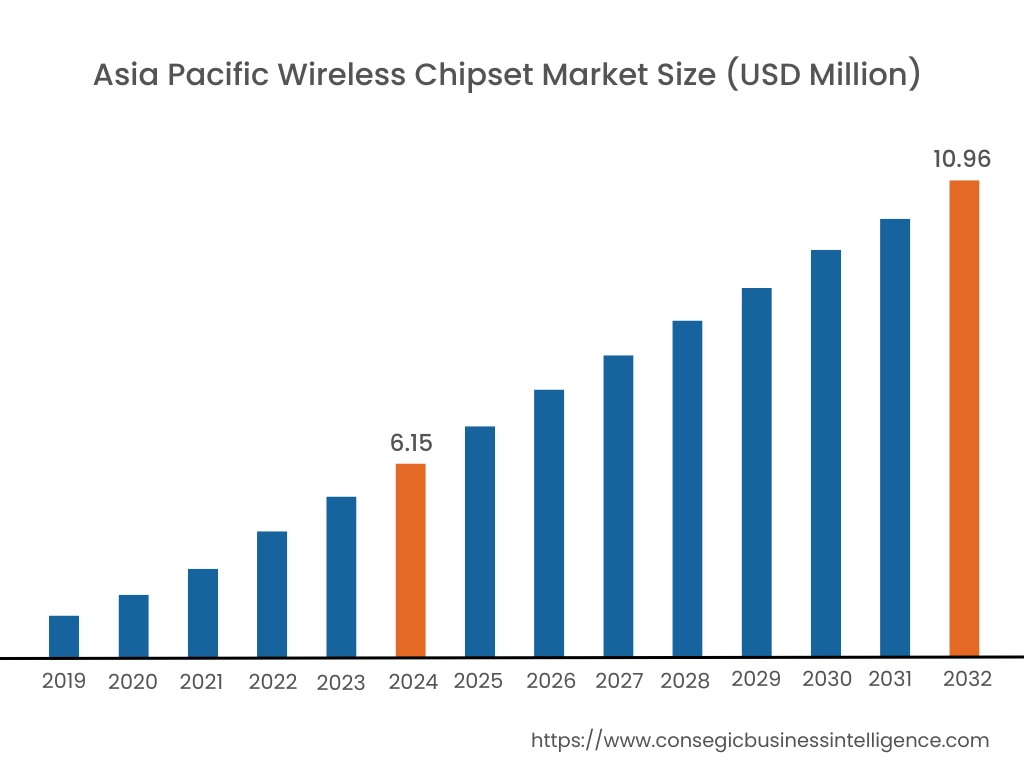

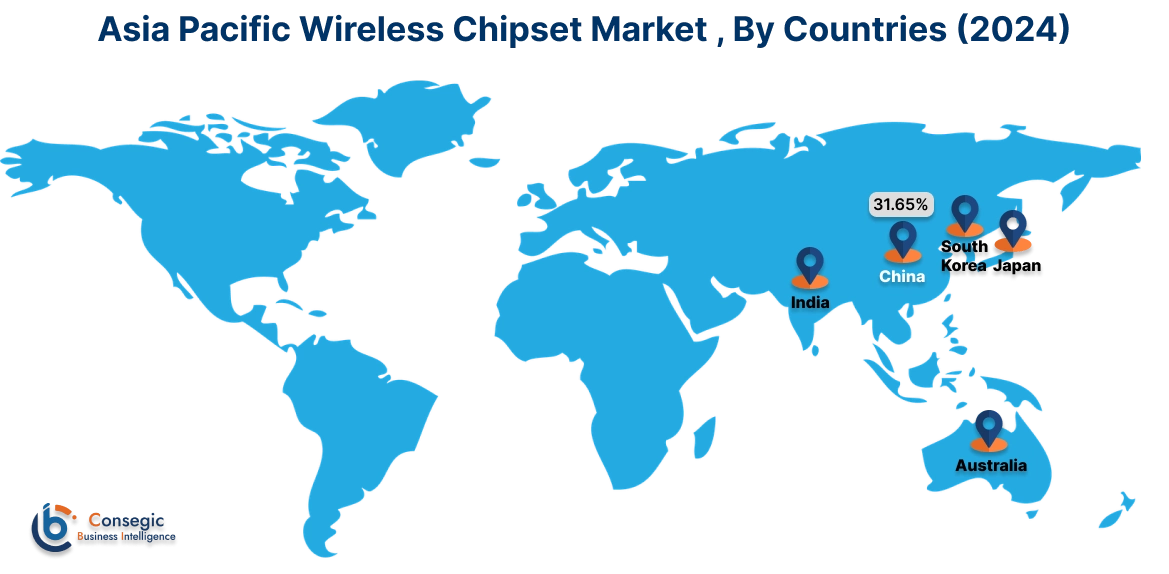

Asia Pacific wireless chipset market expansion is estimated to reach over USD 10.96 billion by 2032 from a value of USD 6.15 billion in 2024 and is projected to grow by USD 6.55 billion in 2025. Out of this, the China’s market accounted for the maximum revenue split of 31.65%. Asia-Pacific remains the largest revenue contributor in the global market, driven by a rising need for smartphones and connected devices. The region's progression is supported by favorable technical infrastructure, cost-effective manufacturing, and a plentiful supply of affordable labor in countries like Japan, South Korea, China, and India. As of 2022, Asia-Pacific comprises about 62.3% of the global population plays a significant role in global trade and consumer electronics consumption. According to the report Asia-Pacific Trade and Investment Trends 2023 from the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), Asia-Pacific was responsible for 36% of global trade in 2021–2022. Additionally, advancements in digitalization have accelerated smartphone adoption in the region. The 'Mobile Economy 2022' report by the GSM Association indicates that smartphone adoption rates in Asia-Pacific and Greater China were approximately 76% and 81%, respectively, in 2022. These factors and analysis would further drive the regional wireless chipset market growth during the forecast period.

- For instance, in November 2024, Millennium Semiconductors launched Nordic semiconductor nRF54L15, featuring wireless System-on-Chip (SoC). This cost-effective, all-inclusive development kit is created for developers looking to explore the complete functionalities of the nRF54L15, nRF54L10, and nRF54L05 SoCs on one board.

North America market is estimated to reach over USD 12.81 billion by 2032 from a value of USD 7.83 billion in 2024 and is projected to grow by USD 8.27 billion in 2025. The market is witnessing a development, fueled by the rising need for faster, more reliable internet connections in consumer, enterprise, and industrial sectors. As businesses and consumers enhance their networks to accommodate high-bandwidth applications such as video streaming, gaming, and IoT devices, the adoption of Wi-Fi 6 and Wi-Fi 6E technologies is accelerating, providing improved performance and lower latency through wider channels and better spectrum utilization. The upcoming Wi-Fi 7 standard, which promises even faster speeds and reduced latency, is set to further propel innovation in the chipset market. With significant investments from leading chipset manufacturers and expanding infrastructure deployment, the region is on track for a dynamic evolution in wireless connectivity technologies, with Wi-Fi 7 anticipated to be crucial in future-proofing networks for the next generation of digital services. These factors and developments would further drive the regional wireless chipset market share during the forecast period.

- For instance, in September 2023, Intel Corporation launched two new networking chipsets, the Wi-Fi 7 BE200 and BE202, compliant with the IEEE 802. 11be (Wi-Fi 7) specification. The Wi-Fi 7 standard supports data rates of up to 40 Gbit/s, with the BE200 chipset employing 2x2 TX/RX streams across the 2. 4 GHz, 5 GHz, and 6 GHz frequency bands to improve connectivity and performance.

According to the wireless chipset market, the European market has seen robust progression in the coming years. As European businesses and consumers progressively embrace next-generation networking solutions, Wi-Fi 7 is anticipated to play a crucial role in facilitating advanced use cases, such as immersive technologies like AR/VR. The market benefits from EU regulations that encourage the allocation of spectrum for Wi-Fi innovations, and top chipset manufacturers are making substantial investments in R&D to address the region's need for state-of-the-art wireless solutions. Additionally, the rising affordability of smartphones and the progression of mobile networks are boosting smartphone adoption throughout Latin America. This surge in adoption is increasing the need for Wi-Fi chipsets that facilitate connectivity in these devices. Additionally, the expanding internet penetration, both mobile and fixed broadband, is generating a larger market for connected devices and applications, thereby heightening the need for Wi-Fi chipsets. Furthermore, the need for connected devices, such as smart home devices, wearables, and IoT devices, is increasing in MEA, leading to a greater need for Wi-Fi chipsets to facilitate their connectivity. Additionally, governments in the MEA region are investing in digital infrastructure, including the deployment of 4G and 5G networks, which is opening up opportunities for Wi-Fi chipset manufacturers. Thus, on the above wireless chipset market analysis, these factors would further drive the regional market during the forecast period.

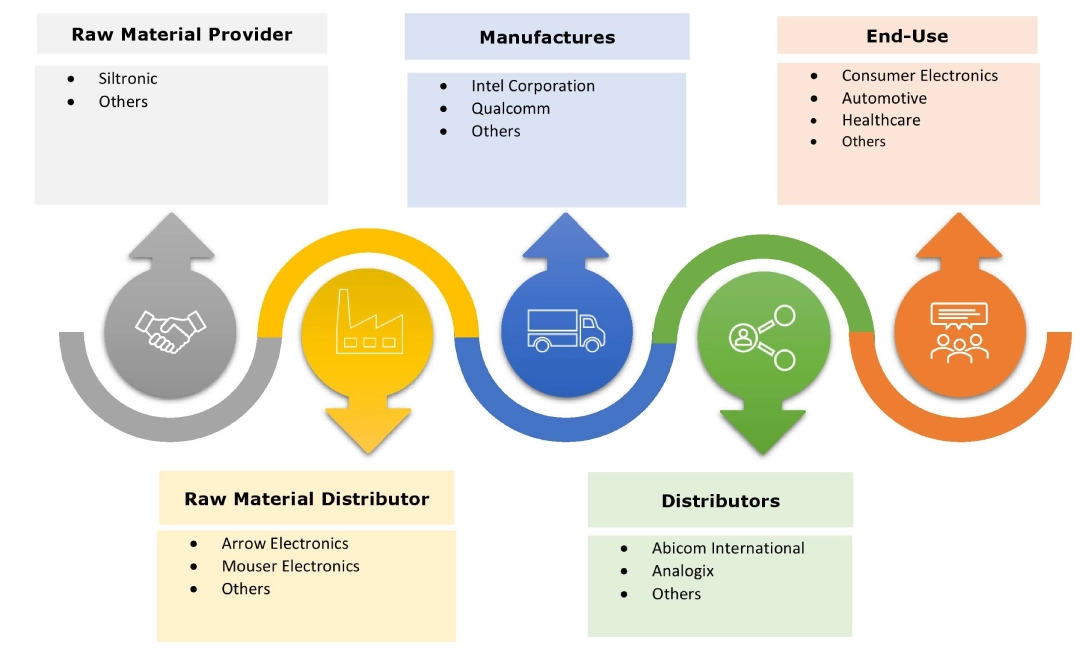

Top Key Players and Market Share Insights:

The global wireless chipset market is highly competitive with major players providing Wi-Fi chipset solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the wireless chipset industry include-

- Intel Corporation (U.S.)

- Qualcomm (U.S.)

- NXP Semiconductors (The Netherlands)

- Micron Technology, Inc. (US)

- Taiwan Semiconductor Manufacturing Company (Taiwan)

- Broadcom (U.S.)

- Texas Instruments (U.S.)

- Media Tek Inc (Taiwan)

- NVIDIA (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

Recent Industry Developments :

Product Launch:

- In October 2024, Silicon Labs introduced the SiWx917 Wi-Fi 6 chipset platform, tailored for IoT applications. This ultra-low power chipset provides up to two years of battery life, making it suitable for various IoT scenarios in residential and industrial environments. Intended home applications include smart locks, cameras, HVAC systems, sensors, and appliances, while its industrial uses encompass predictive maintenance, smart meters, asset tracking, and other sensor-based solutions.

Wireless Chipset Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 35.37 Billion |

| CAGR (2025-2032) | 5.8% |

| By Standard |

|

| By Band |

|

| By MIMO Configuration |

|

| By Application |

|

| By End Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Wireless Chipset market? +

Wireless Chipset Market Size is estimated to reach over USD 35.37 Billion by 2032 from a value of USD 21.34 Billion in 2024 and is projected to grow by USD 22.57 Billion in 2025, growing at a CAGR of 5.8% from 2025 to 2032.

Which is the fastest-growing region in the Wireless Chipset market? +

Asia-Pacific is the region experiencing the most rapid growth in the market. The Asia Pacific Wi-Fi chipset market is mainly propelled by the growing adoption of the internet and smartphones, as well as rapid urbanization and improving living standards. Additionally, governments in several countries are initiating the development of smart cities to enhance Wi-Fi accessibility, particularly to support the healthcare and education sectors.

What specific segmentation details are covered in the Wireless Chipset report? +

The wireless chipset report includes specific segmentation details for standard, band, MIMO configuration, application, end use, and region.

Who are the major players in the Wireless Chipset market? +

The key participants in the market are Intel Corporation (U.S.), Qualcomm (U.S.), Broadcom (U.S.), Texas Instruments (U.S.), Media Tek Inc (Taiwan), NVIDIA (U.S.), Advanced Micro Devices, Inc. (U.S.), NXP Semiconductors (The Netherlands), Micron Technology, Inc. (US), Taiwan Semiconductor Manufacturing Company (Taiwan), and others.