- Summary

- Table Of Content

- Methodology

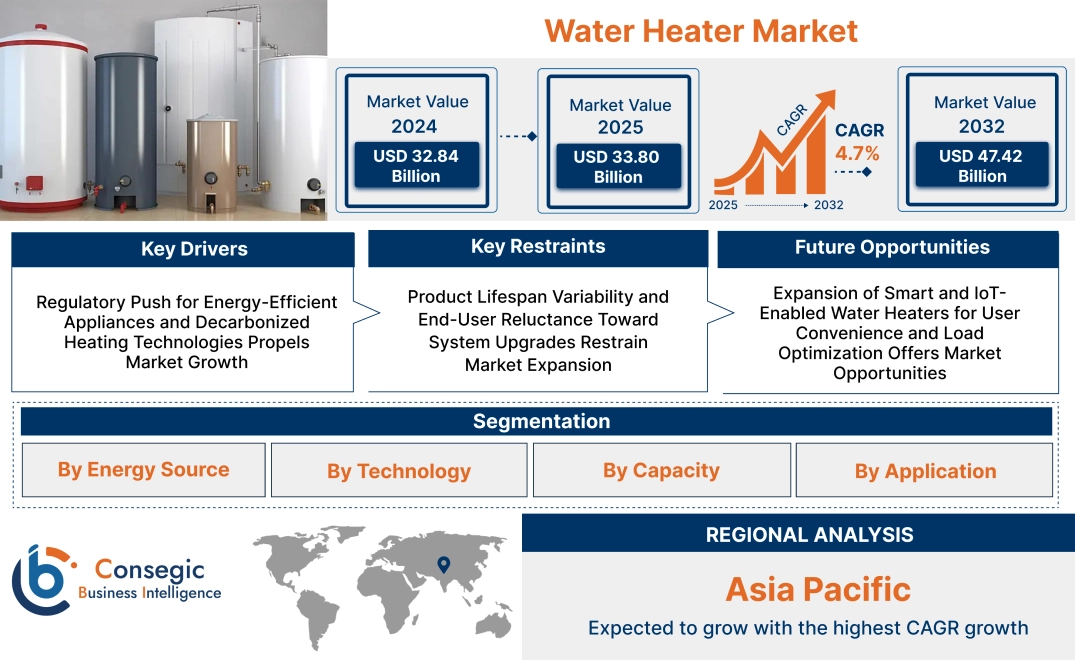

Water Heater Market Size:

Water Heater Market size is estimated to reach over USD 47.42 Billion by 2032 from a value of USD 32.84 Billion in 2024 and is projected to grow by USD 33.80 Billion in 2025, growing at a CAGR of 4.7% from 2025 to 2032.

Water Heater Market Scope & Overview:

Water heater is an appliance engineered to heat and store water for domestic, commercial, and industrial use. Available in tank-type, tankless, hybrid, and solar-integrated models, it delivers hot water for applications including bathing, cleaning, and space heating. Units vary in capacity, energy source, and mounting configuration to suit different user environments and consumption patterns.

Key features include adjustable thermostats, corrosion-resistant linings, safety valves, and energy efficiency controls. Advanced systems incorporate smart connectivity, temperature presets, and compact footprints to optimize space utilization and user experience.

Water heater systems provide convenience, consistent hot water availability, and reduced wait times. Their integration with renewable energy and high-efficiency components further supports sustainable usage. Applicable across residential buildings, hospitality facilities, healthcare institutions, and commercial kitchens, these systems remain essential for modern infrastructure focused on thermal comfort, sanitation, and operational efficiency.

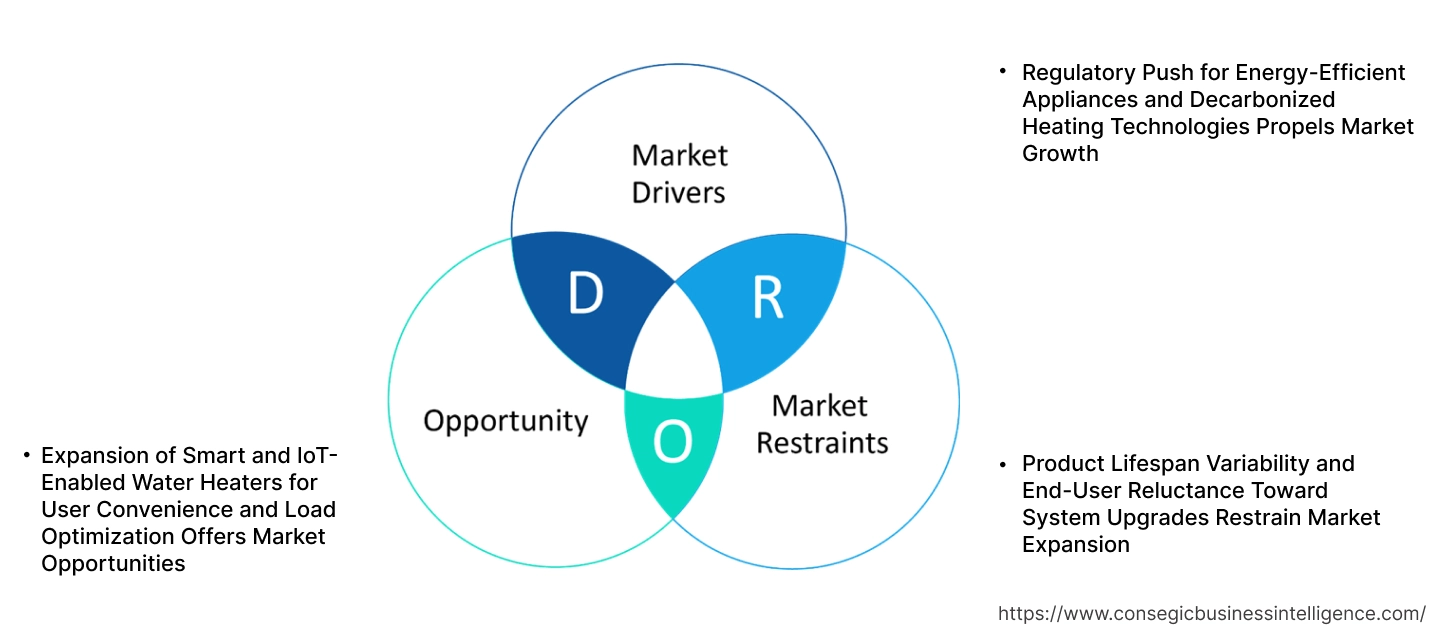

Water Heater Market Dynamics - (DRO) :

Key Drivers:

Regulatory Push for Energy-Efficient Appliances and Decarbonized Heating Technologies Propels Market Growth

Governments across North America, Europe, and Asia-Pacific are strengthening energy efficiency mandates to reduce emissions and accelerate decarbonization in building systems. Regulatory frameworks such as ENERGY STAR, Ecodesign Directive, and regional building codes are setting higher efficiency thresholds for water heating systems. These standards are phasing out low-performing units and incentivizing adoption of condensing, heat pump, and solar-assisted models. Financial support in the form of rebates, tax credits, and low-interest financing is encouraging both residential and commercial users to upgrade to high-efficiency systems. As developers, institutional buyers, and homeowners align with net-zero energy goals and climate targets, demand for sustainable heating appliances is rising.

- For instance, in April 2023, LG Electronics USA launched the much-anticipated LG Inverter Heat Pump Water Heater to assist homeowners in saving money and reducing energy usage as well as their carbon footprint. Certified by ENERGY STAR, the heater delivers a Uniform Energy Factor of 3.75 UEF and provides users with energy savings of up to 70%.

This policy-driven transition is significantly boosting replacement and new installations, contributing to long-term water heater market expansion.

Key Restraints:

Product Lifespan Variability and End-User Reluctance Toward System Upgrades Restrain Market Expansion

Many users view water heating systems as long-term appliances and defer replacement until failure, often beyond their optimal service life. Product longevity varies significantly depending on technology type, usage patterns, and water quality, but users frequently prioritize repair over proactive upgrades. Even with higher energy costs and efficiency gains offered by newer models, the perceived benefit is not always immediate or well understood by end users. In regions where replacement involves significant capital expenditure or labor disruption, adoption of advanced systems is further delayed. The lack of awareness around operating cost savings and the absence of mandated upgrade cycles lead to slow turnover rates. Despite growing demand for energy-efficient and smart appliances, behavioral inertia and low system visibility continue to hinder water heater market growth across both residential and light commercial segments.

Future Opportunities :

Expansion of Smart and IoT-Enabled Water Heaters for User Convenience and Load Optimization Offers Market Opportunities

The integration of smart controls and IoT capabilities in water heaters is transforming user experience and operational efficiency. Smart models allow remote temperature control, usage monitoring, and scheduling through mobile applications or home automation platforms. These systems help users optimize energy consumption based on occupancy patterns and time-of-use electricity pricing. Utilities are also integrating them into demand response programs to shift heating loads during peak hours and reduce grid stress. The need for connected appliances is growing in both residential and commercial sectors, driven by consumer preference for convenience and energy awareness. As smart home ecosystems become more prevalent, manufacturers offering Wi-Fi-enabled and app-controlled heaters with diagnostic alerts and energy reports are gaining market traction.

- For instance, in September 2023, Midea launched the latest breakthrough in water heating solutions, the Smart Wi-Fi Storage Water Heater. The heater provides remote control through the SmartHome app, intuitive scheduling features to customize heating and conserve energy, voice control through Alexa and Google Home, and a 5-star BEE energy rating.

These innovations are creating strong water heater market opportunities supported by technology-driven growth and user-centric product evolution.

Water Heater Market Segmental Analysis :

By Energy Source:

Based on energy source, the water heater market is segmented into electric, gas, solar, hybrid, and others.

The electric segment accounted for the largest revenue share in 2024.

- Electric models are widely used in residential and commercial applications due to their ease of installation, low maintenance, and compatibility with urban infrastructure.

- These systems are cost-effective for small-to-medium capacity needs, especially in regions with stable and affordable electricity supply.

- Technological advancements in heating elements and energy-saving modes have improved efficiency and performance.

- As per water heater market analysis, electric heaters dominate due to their availability and regulatory preference for clean energy sources.

The solar segment is projected to witness the fastest CAGR during the forecast period.

- Solar heaters utilize solar collectors and thermal storage tanks, reducing reliance on grid electricity or fossil fuels.

- Adoption is increasing in sun-rich regions and in countries offering incentives for renewable energy solutions.

- These systems support carbon reduction goals and help in achieving green building certifications.

- As per water heater market trends, solar-based systems are driving innovation and expansion in sustainable residential and commercial projects.

By Technology:

Based on technology, the market is segmented into storage, tankless (on-demand), and hybrid systems.

The storage segment held the largest water heater market share in 2024.

- Storage types use insulated tanks to retain heated water, ensuring availability at all times for household and light commercial needs.

- These systems are ideal in areas with high hot water consumption or where water pressure is inconsistent.

- With improvements in tank insulation and energy recovery mechanisms, modern storage systems offer better thermal efficiency.

- For instance, in August 2024, Symphony launched three ranges of geysers – Spa, Sauna and Soul, equipped with advanced features like Symphony PuroPod, a 9-layer water filtration cartridge that softens hard water, reducing hair damage and providing skincare benefits. The storage water heater is available in 10, 15, and 25-liter capacities.

- Water heater market demand for storage systems continues to grow in suburban and rural regions with high usage patterns.

The tankless (on-demand) segment is projected to grow at the fastest CAGR.

- Tankless systems heat water only when needed, reducing standby energy losses and offering space-saving advantages.

- These units are particularly popular in urban apartments, hotels, and institutional facilities with limited installation space.

- Smart controls, variable flow adjustments, and quick recovery features are increasing consumer preference.

- According to water heater market trends, tankless adoption is rising due to its operational efficiency and eco-friendly profile.

By Capacity:

Based on capacity, the market is segmented into below 30 liters, 30–100 liters, 100–250 liters, and above 250 liters.

The 30–100 liters segment accounted for the largest water heater market share in 2024.

- This capacity range is ideal for small households and compact commercial facilities, providing a balance between volume and energy efficiency.

- Systems in this range are highly versatile, supporting both wall-mounted and under-sink configurations.

- Manufacturers are offering feature-rich products in this segment with digital displays, thermostats, and safety mechanisms.

- As per water heater market analysis, increasing urban housing and small office developments fuel segment stability.

The above 250 liters segment is expected to witness the fastest CAGR.

- Large-capacity models are essential for industrial and institutional applications requiring continuous hot water supply.

- These systems are used in hospitals, hotels, and manufacturing units where process and sanitation requirements are high.

- They often integrate with solar or hybrid energy sources to manage operating costs effectively.

- Water heater market expansion in commercial infrastructure drives the need for high-capacity systems with robust safety and automation.

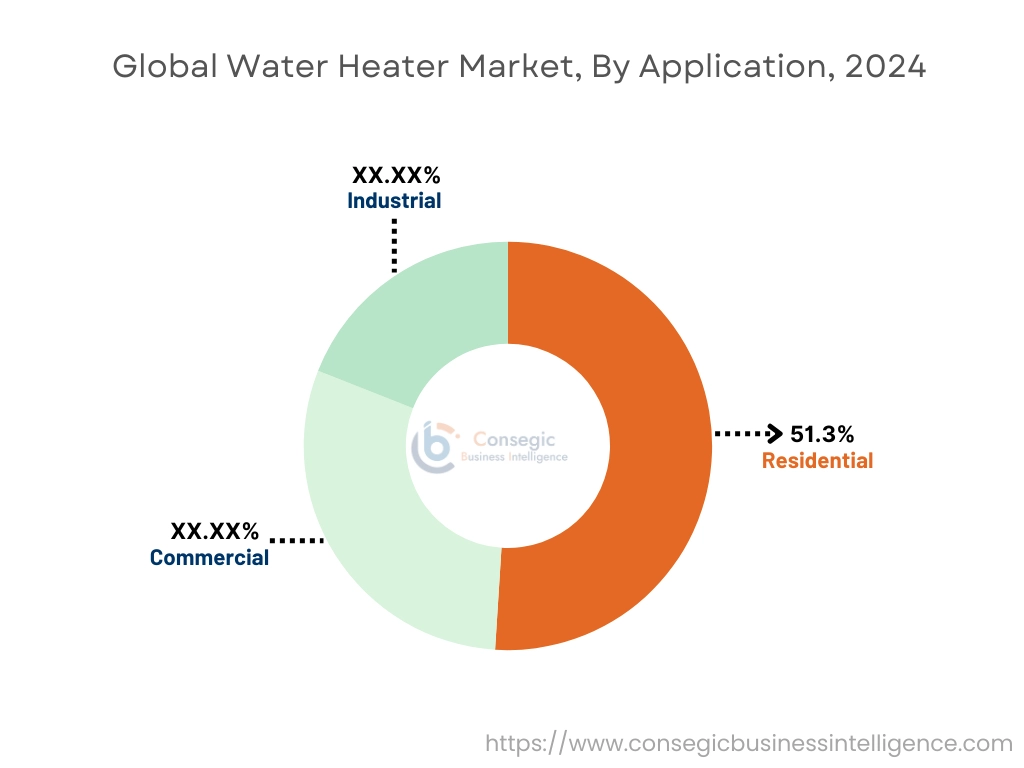

By Application:

Based on application, the water heater market is divided into residential, commercial, and industrial.

The residential segment held the largest revenue share of 51.3% in 2024.

- Homeowners prioritize energy efficiency, compactness, and cost-effectiveness in water heating systems.

- Government energy labeling programs and rebates are promoting the switch to modern, efficient units.

- The rise of smart homes and connected appliances supports the adoption of intelligent heaters with app-based control.

- Water heater market demand in this segment is propelled by the construction of new housing and the renovation of older infrastructure.

The commercial segment is projected to register the fastest CAGR.

- Commercial users require high-performance, durable systems to meet constant hot water needs in hotels, gyms, hospitals, and institutions.

- Energy optimization and compliance with environmental standards are primary drivers for heater upgrades in this sector.

- Modular systems and centralized heating solutions are gaining traction for scalable operations.

- As per water heater market growth forecasts, urbanization and tourism infrastructure development fuel segment advancement.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

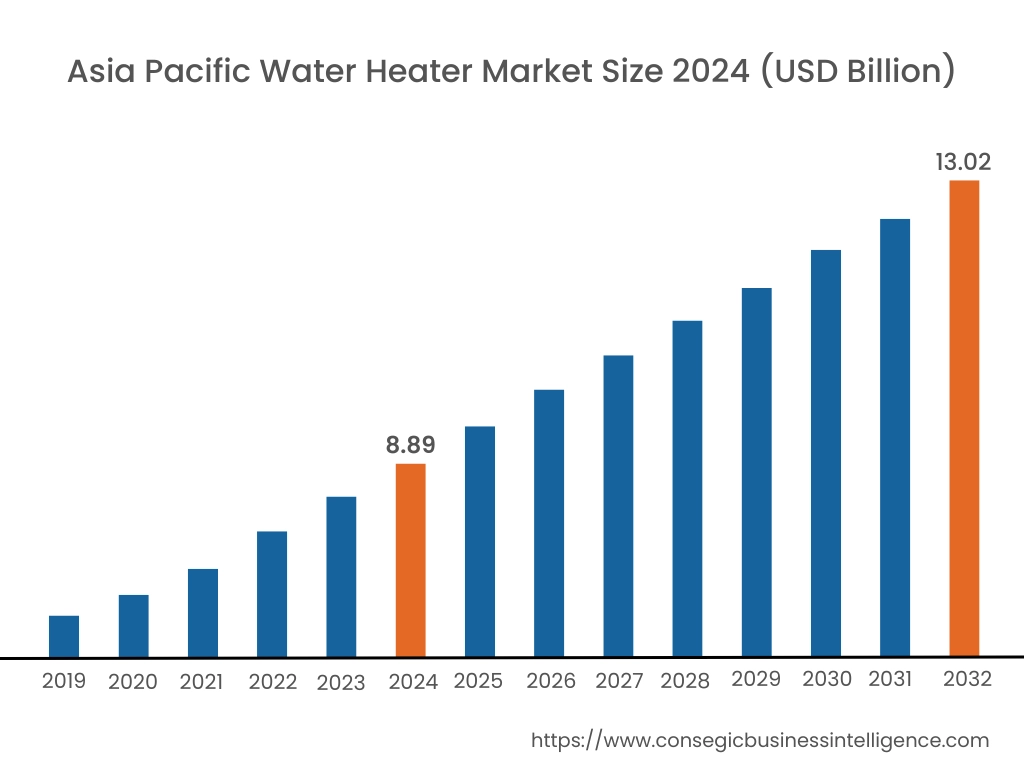

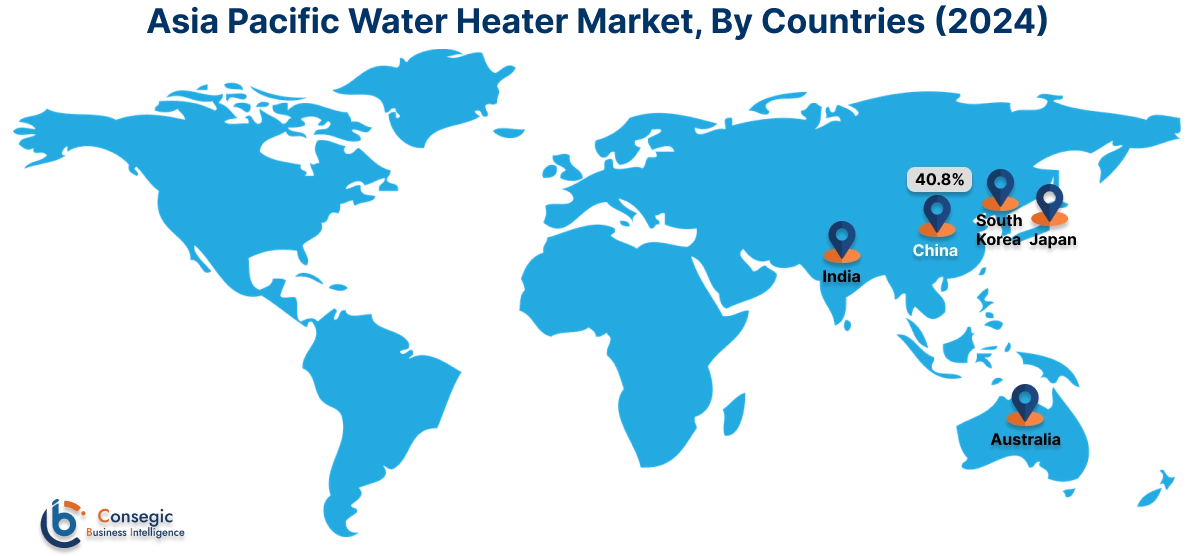

Asia Pacific region was valued at USD 8.89 Billion in 2024. Moreover, it is projected to grow by USD 9.16 Billion in 2025 and reach over USD 13.02 Billion by 2032. Out of this, China accounted for the maximum revenue share of 40.8%. Asia-Pacific is experiencing rapid growth in the global water heater market, driven by rapid urbanization, rising income levels, and expanding construction of multifamily housing across emerging economies. In countries like China, India, Japan, and South Korea, demand is increasing for both instantaneous and storage-based systems, supported by government initiatives to improve energy access and living standards. Market analysis shows growing interest in solar heaters in rural and peri-urban areas, while heat pump and high-efficiency electric models are gaining momentum in modern urban projects. The shift toward electric units is also being propelled by grid modernization and stricter energy usage norms, creating significant potential for long-term adoption across residential and small commercial sectors.

North America is estimated to reach over USD 15.80 Billion by 2032 from a value of USD 10.92 Billion in 2024 and is projected to grow by USD 11.24 Billion in 2025. In North America, requirement remains strong due to ongoing construction activities, increasing consumer preference for energy-efficient appliances, and the replacement of aging heating systems. In the United States and Canada, residential and light commercial segments continue to adopt both tank and tankless systems, with a growing shift toward electric and hybrid heat pump units. Market analysis highlights that rising electricity costs and stricter energy efficiency regulations are prompting homeowners and developers to invest in ENERGY STAR-certified solutions. Moreover, the integration of smart thermostats and Wi-Fi-enabled controls is boosting product appeal. Growth is also supported by government rebates and utility-based incentive programs encouraging the transition away from conventional models.

Europe exhibits a regulation-driven water heater industry, with demand centered on compact, energy-efficient systems aligned with the EU’s energy labeling directives and carbon neutrality goals. Countries such as Germany, France, and the United Kingdom are emphasizing the use of heat pump-based and solar-assisted water heating solutions, particularly in low-energy homes and retrofitted apartment buildings. Market analysis reveals that the electrification of heating systems is gaining traction due to policy efforts to phase out gas-fired units. Additionally, smart home integration and the need for space-saving wall-mounted units are reinforcing growth in urban residential settings. The opportunity in Europe is expanding through mandates tied to new construction efficiency targets and increased adoption of eco-friendly building standards.

Latin America displays a developing yet growing market, with increasing adoption in Brazil, Mexico, and Chile. Need is driven by urban housing expansion, climate variability, and regional electrification trends. Market analysis indicates that residential installations dominate, with rising interest in electric and solar-assisted systems in areas where gas infrastructure is limited. The preference for affordable and low-maintenance units is shaping product selection, particularly among middle-income households. In addition, sustainable building initiatives and awareness of renewable energy are opening new channels for energy-efficient and solar-integrated heating systems. The water heater market opportunity in this region lies in expanding localized manufacturing, improved distribution networks, and public awareness campaigns.

The Middle East and Africa are emerging markets for water heating systems, with increased activity in countries like the UAE, Saudi Arabia, South Africa, and Egypt. In the Gulf region, centralized electric and solar-assisted heating solutions are increasingly used in high-end residential and hospitality developments. Market analysis shows that in Africa, limited access to grid electricity and affordability constraints have slowed widespread adoption, though small-scale solar heaters are gaining traction in off-grid communities. Government-backed energy access programs and donor-led electrification initiatives are expected to fuel future requirements. Long-term growth in this region depends on enhancing local supply chains and addressing cost and maintenance barriers.

Top Key Players and Market Share Insights:

The water heater market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global water heater market. Key players in the water heater industry include -

- Bosch Thermotechnology (Germany)

- Ariston Thermo Group (Italy)

- Bajaj Electricals Ltd. (India)

- Vaillant Group (Germany)

- John Wood Water Heaters (Canada)

- Rinnai Corporation (Japan)

- Noritz Corporation (Japan)

- Panasonic Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- Haier Group Corporation (China)

Recent Industry Developments :

Product Launches:

- In February 2023, Rheem, a leading global manufacturer of water heating and HVACR products, launched the Rheem® Maximus™, a smart, sustainable and high-efficiency gas water heater. With an ENERGY STAR® certification, it reduces energy use and carbon emissions by up to 36% and NOx emissions by up to 75% and features 100% recyclable packaging.

Acquisitions:

- In April 2025, Bradford White Corporation, a leading provider of water heating solutions, acquired Universal Technologies of Wisconsin, Inc., Bock Water Heaters, Inc., and Tank Technology, Inc. (collectively known as Bock Water Heaters). The companies have had a longstanding relationship extending back to three decades, with Bock serving as both an important supplier and a valued customer, enabling a natural evolution through this acquisition.

Water Heater Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 47.42 Billion |

| CAGR (2025-2032) | 4.7% |

| By Energy Source |

|

| By Technology |

|

| By Capacity |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Water Heater Market? +

Water Heater Market size is estimated to reach over USD 47.42 Billion by 2032 from a value of USD 32.84 Billion in 2024 and is projected to grow by USD 33.80 Billion in 2025, growing at a CAGR of 4.7% from 2025 to 2032.

What specific segmentation details are covered in the Water Heater Market report? +

The Water Heater market report includes specific segmentation details for energy source, technology, capacity and application.

What are the applications of the Water Heater Market? +

The application of the Water Heater Market are residential, commercial, and industrial.

Who are the major players in the Water Heater Market? +

The key participants in the Water Heater market are Bosch Thermotechnology (Germany), Ariston Thermo Group (Italy), Rinnai Corporation (Japan), Noritz Corporation (Japan), Panasonic Corporation (Japan), Mitsubishi Electric Corporation (Japan), Haier Group Corporation (China), Bajaj Electricals Ltd. (India), Vaillant Group (Germany) and John Wood Water Heaters (Canada).