- Summary

- Table Of Content

- Methodology

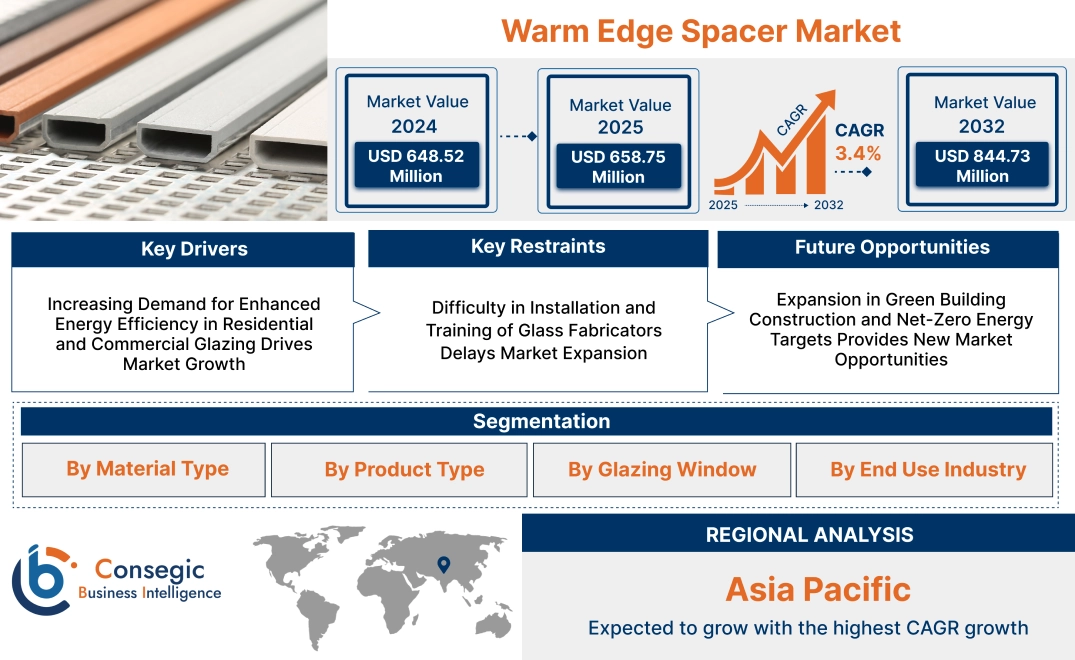

Warm Edge Spacer Market Size:

Warm Edge Spacer Market size is estimated to reach over USD 844.73 Million by 2032 from a value of USD 648.52 Million in 2024 and is projected to grow by USD 658.75 Million in 2025, growing at a CAGR of 3.4% from 2025 to 2032.

Warm Edge Spacer Market Scope & Overview:

Warm edge spacer is a thermally engineered component inserted between panes in insulating glass units to enhance energy performance and minimize heat transfer at the window edge. It differs from conventional aluminum spacers in that it is constructed of composite materials or thermoplastics that reduce thermal bridging and condensation potential.

These spacers have low thermal conductivity, structural stability, and compatibility with different glazing systems. They accommodate better insulation values, improve the window system's lifespan, and help to maintain interior comfort by avoiding edge temperature drops.

Widely used in residential, commercial, and industrial fenestration systems, it improves overall energy efficiency and enables compliance with contemporary building standards. Its contribution to ensuring consistent thermal performance and edge durability makes it an ideal component in high-performance glazing technologies, enabling long-term building performance in different climate conditions.

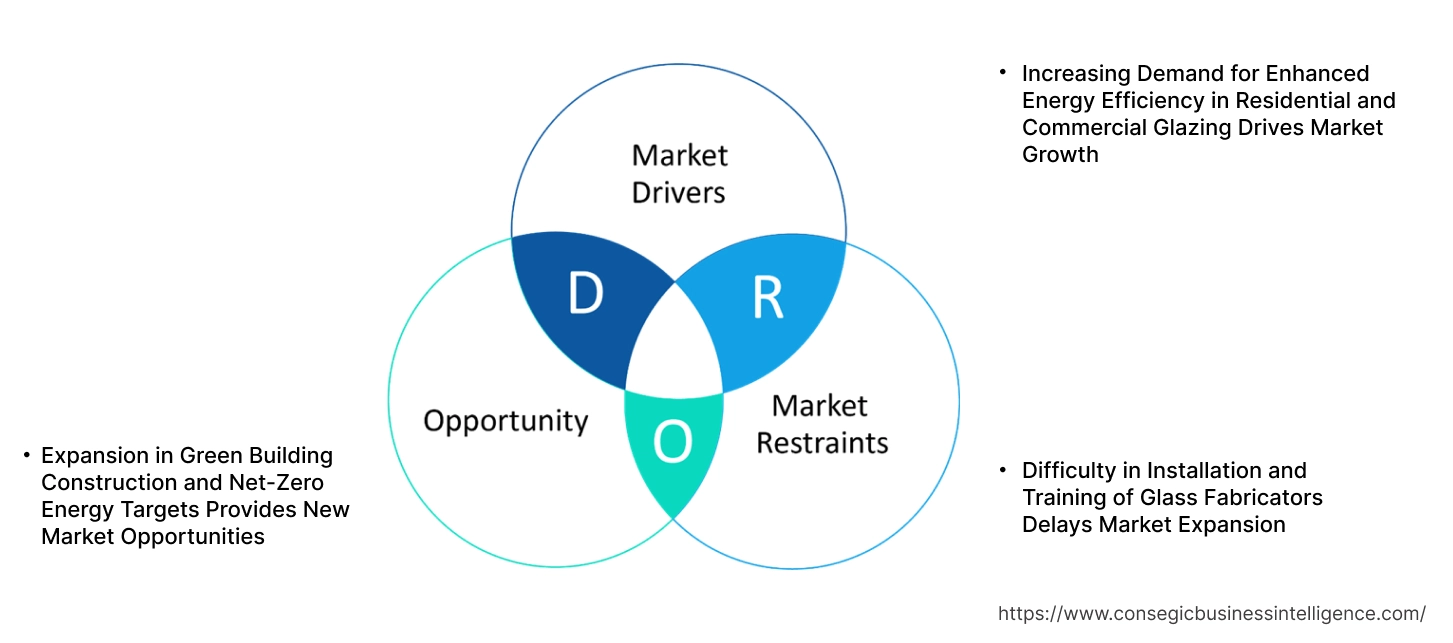

Warm Edge Spacer Market Dynamics - (DRO):

Key Drivers:

Increasing Demand for Enhanced Energy Efficiency in Residential and Commercial Glazing Drives Market Growth

The requirement for improved thermal insulation in building envelopes has led to a growing emphasis on the performance of insulating glass units (IGUs). Warm edge spacers are important in minimizing thermal bridging at the IGU edge, directly contributing to enhanced U-values and reduced heating and cooling loads. As energy codes become increasingly stringent throughout residential and commercial markets, architects and contractors are placing greater emphasis on fenestration technologies that enable sustainability certifications and future cost savings. Nations throughout Europe and North America are requiring enhanced levels of building energy efficiency, driving the transition to high-efficiency glazing. Warm edge technology also resolves condensation control and indoor comfort—untold performance metrics throughout residential retrofits and new buildings. These efficiency gains, alongside regulatory requirements and sustainability considerations, are fueling demand for high-performance IGUs. Synergy between efficiency regulations and design expectations is causing persistent warm edge spacer market growth.

Key Restraints:

Difficulty in Installation and Training of Glass Fabricators Delays Market Expansion

Shifting away from standard aluminum spacers towards sophisticated insulating systems creates processing complexity. Handling, alignment, and sealing procedures for warm edge spacers, especially thermoplastic or hybrid types, call for high levels of precision in order to provide structural integrity as well as thermal performance. Numerous small- and mid-sized IGU manufacturers are running legacy machines or semi-automated systems, which do not accommodate modern spacer integration capabilities. This incongruity translates into the demand for advanced training and capital replacement, driving higher onboarding costs and operational hazards. Inconsistent sealing or assembly habits affect spacer life and lower end-user satisfaction, causing some fabricators to hold out. The absence of uniform training programs and disparate technical awareness in different regions also constrains effective deployment. These hurdles raise the difficulty of scaling adoption among decentralized producers. Consequently, installation and readiness among the workforce remain key challenges to uniform warm edge spacer market growth.

Future Opportunities:

Expansion in Green Building Construction and Net-Zero Energy Targets Provides New Market Opportunities

Sustainability objectives are changing the way buildings are designed, with developers and architects now ordering energy-efficient products from the initial planning phase. In this scenario, warm edge spacers are becoming part of window assemblies designed for green-certified and net-zero buildings. Their role in minimizing heating and cooling loads aids passive design and facilitates compliance with initiatives such as LEED, BREEAM, and Passive House. Demand for sustainable construction is gaining pace in institutional, residential, and commercial market segments, mostly in Europe and North America. Beyond performance, warm edge solutions are also consistent with lifecycle energy modeling and reducing embodied carbon in façade systems. As ESG targets become a primary metric for both real estate developers and tenants, producers of thermally efficient spacer systems are well-placed to benefit.

- For instance, in February 2025, Technoform collaborated with Northwestern Industries (NWI) Seattle and Oldcastle BuildingEnvelope (OBE) to design a complete architectural glazing solution. Technoform supplied the plastic hybrid stainless steel warm edge spacer for the insulating glass to develop one of the first commercial projects designed and certified to fulfill Seattle’s Living Building Pilot Program (LBPP), as per the International Living Future Institute (ILFI) Living Building Challenge.

These evolving market preferences and policy adjustments are generating considerable warm edge spacer market opportunities driven by both demand and growth.

Warm Edge Spacer Market Segmental Analysis :

By Material Type:

Based on material type, the warm edge spacer market is segmented into stainless steel, foam, thermoplastic, silicone, and hybrid materials.

The stainless steel segment accounted for the leading market share in 2024.

- Stainless steel provides low thermal conductivity while providing structural stiffness in insulated glass units (IGUs).

- It provides excellent durability and long-term gas retention in residential and commercial glazing.

- The material is corrosion-resistant and facilitates compliance with energy efficiency standards in several regions.

- According to the warm edge spacer market analysis, stainless steel spacers are ideal for high-volume IGU production because of their stable performance.

Thermoplastic is anticipated to record the highest CAGR over the forecast period.

- Thermoplastic spacers provide greater flexibility, ease of production, and improved moisture resistance.

- This segment is driven by rising retrofitting projects that favor thermally efficient window systems.

- Segmental trends show an increased demand for single-seal thermoplastic systems to minimize production costs.

- Therefore, the increased construction activity in colder climates is responsible for the warm edge spacer market expansion in this material category.

By Product Type:

Based on product type, the market is divided into flexible spacer and rigid spacer.

The flexible spacer segment held the dominant warm edge spacer market share in 2024.

- They are ideal for offering great thermal insulation and allowing window expansion or contraction due to changes in temperature.

- They are widely used in residential window installation to enhance energy efficiency and comfort.

- As an energy-saving measure, flexible systems minimize condensation and U-values.

- In addition, warm edge spacer market demand for flexible spacers keeps increasing, propelled by green building certification trends.

The rigid spacer segment is expected to grow at the fastest CAGR during the forecast period.

- Dimensional stability is provided by rigid spacers, which is essential in structural glazing and commercial facades.

- They are designed with greater mechanical stress tolerance without sacrificing gas barrier properties.

- This section is prospering with rising investment in intelligent and large-format glass installations.

- As per the warm edge spacer market analysis, the manufacturers are advancing rigid spacer designs to accommodate high-load applications.

By Glazing Window:

On the basis of glazing window, the warm edge spacer market is segmented into double glazing and triple low-E.

The double glazing segment held the largest market share in 2024.

- Double-glazed windows offer a cost–benefit trade-off in terms of thermal insulation for mass applications.

- Warm edge spacers applied in this setup minimize edge-seal heat loss considerably.

- Urbanization and energy policies of emerging economies drive this segment's leadership.

- According to warm edge spacer market trends, the demand for double-glazing in mid-range residential and office buildings keeps growing..

Triple Low-E is the fastest-growing segment during the forecast period.

- Triple low-E windows use multiple chambers and coatings to achieve maximum energy performance.

- This arrangement is popularly used in Northern Europe, Canada, and the U.S. for zero-energy and passive buildings.

- Segmental trends highlight triple glazing as essential for net-zero building compliance.

- Rising need for more performance windows is driving warm edge spacer market growth in this segment.

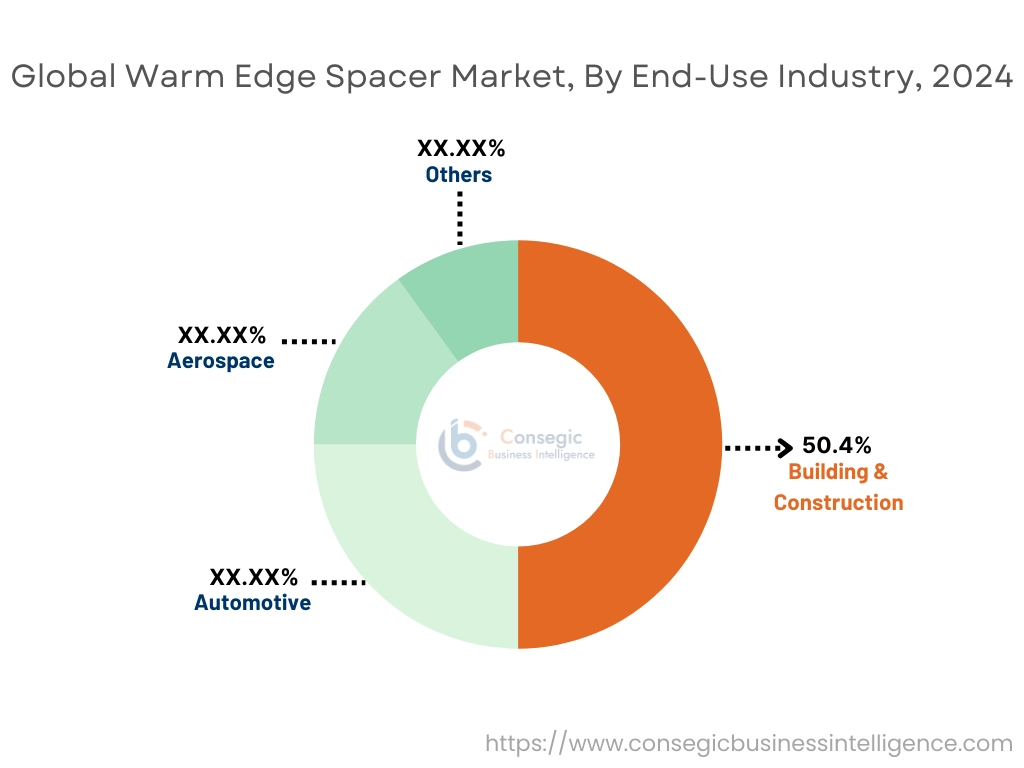

By End Use Industry:

Based on end-use industry, the warm edge spacer market is segmented into building & construction, automotive, aerospace, marine, and others.

The building & construction segment accounted for the largest revenue of the total warm edge spacer market share of 50.4% in 2024.

- The industry is the key consumer for insulated glass units, especially in energy-efficient building construction.

- Building regulations and requirements in Europe and North America have boosted its use.

- Technological advancements in facade technologies and net-zero buildings fuel this segment's revenue.

- According to warm edge spacer market trends, replacement activity in residential remodels is further fueling its requirement.

Automotive is anticipated to be the fastest CAGR during the forecast period.

- Car manufacturers are using warm edge spacers more in sunroofs and side glazing for thermal performance.

- Electric vehicles take advantage of sophisticated IGUs that minimize heating and cooling loads, which improve battery efficiency.

- Segmental analysis indicates that car manufacturers are investing in lightweight, insulating glazing systems.

- For instance, in July 2023, the Beekman Group announced the successful recapitalization of GED, a leading provider of automation equipment. Beekman Group initially invested in GED in 2020 due to its market leadership and ongoing product innovation, which caused it to grow.

- The increasing fleet of electric vehicles globally supports the warm edge spacer market demand in the automotive industry.

Regional Analysis:

The regions included are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

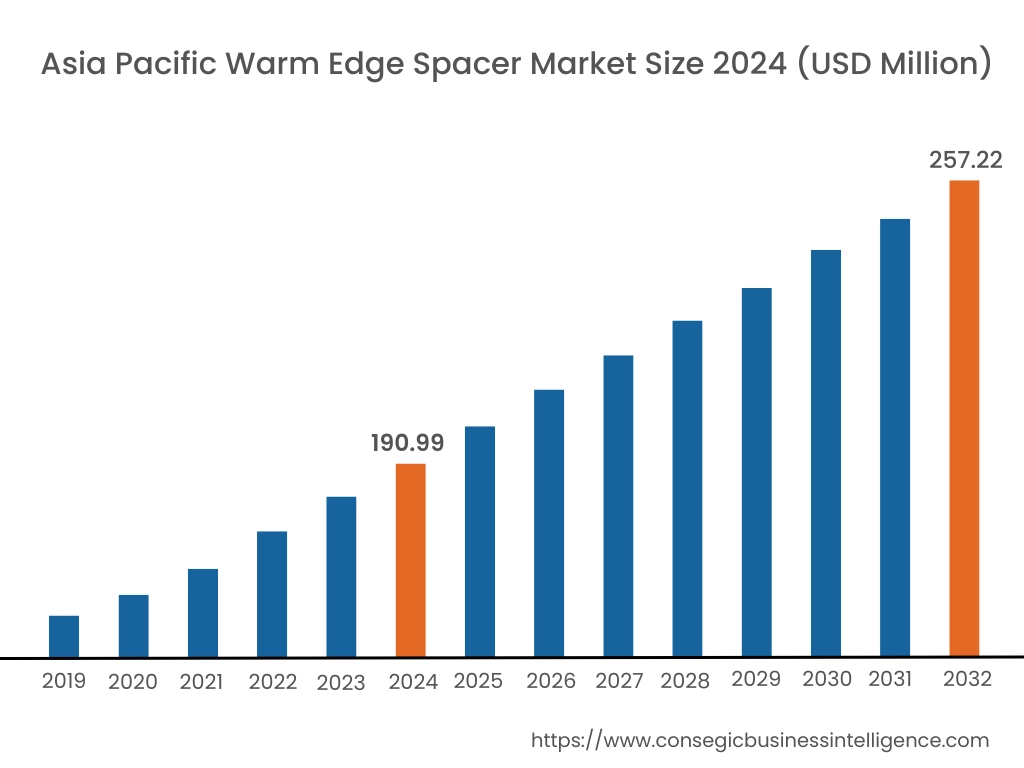

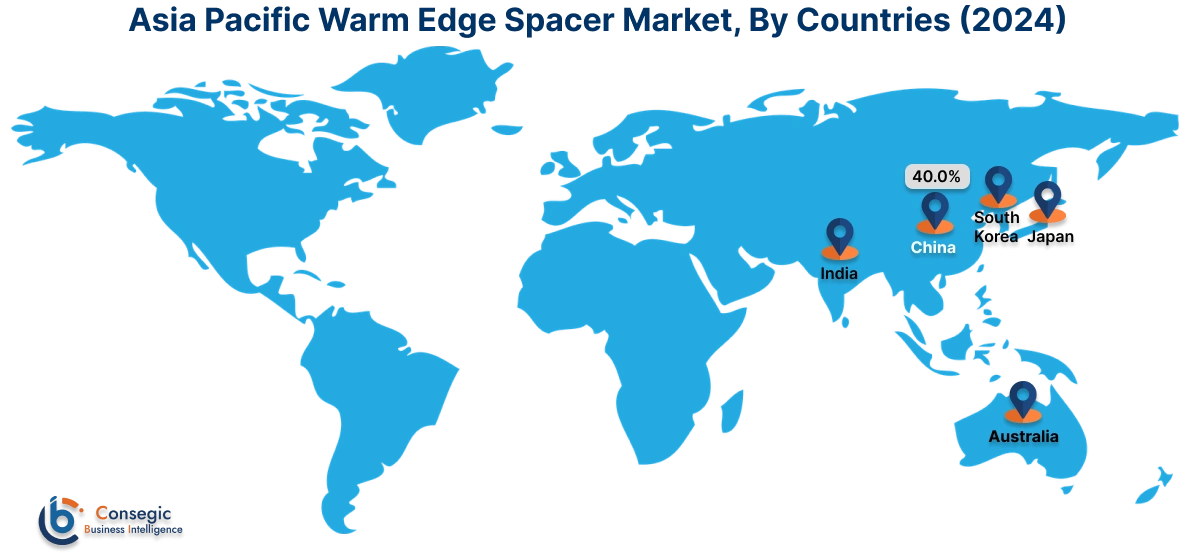

Asia Pacific region was valued at USD 190.99 Million in 2024. Moreover, it is projected to grow by USD 194.56 Million in 2025 and reach over USD 257.22 Million by 2032. Out of this, China accounted for the maximum revenue share of 40.0%. Asia-Pacific is experiencing growth with accelerated urbanization, infrastructure growth, and an increased focus on green building certification. Regions like China, Japan, South Korea, and Australia are witnessing a transition in building preferences towards insulated glazing units that enhance occupant comfort and energy efficiency. According to market analysis, growing urban residential housing, commercial skyscrapers, and government-imposed sustainability requirements are driving the demand for high-performance window solutions. Local producers are also coming together with international companies to introduce these technologies and enhance competitiveness. This offers a sound warm edge spacer market opportunity as long-term energy cost savings awareness continues to increase.

North America is estimated to reach over USD 231.71 Million by 2032 from a value of USD 175.57 Million in 2024 and is projected to grow by USD 178.54 Million in 2025. North America is a leading region for the market, driven by mounting attention towards sustainable building methods and growing use of energy-efficient fenestration technology.

In the United States and Canada, regulatory requirements with respect to building insulation and heat transfer have further pushed the market towards a decline in conventional aluminum spacers to newer hybrid and polymer-based versions. Analysis based on regional trends shows increasing demand from both domestic and commercial constructions, especially for colder climate areas where heat transfer needs to be minimized. Also, increased knowledge of carbon reduction targets is stimulating demand for triple-glazed and low-emissivity window systems, in which warm edge technology has an important role.

- For instance, in September 2024, Swisspacer opened its first North American distribution center in Closter, New Jersey, near New York City. This expansion enables the company to streamline the availability and delivery of its products to the North American construction market. This is a move that allows the company to simplify the availability and supply of its products to the North American construction market. It was also spurred by the subsidy programs and tax incentives provided to the construction sector by the United States government and increasing awareness on sustainability.

Europe is a front-runner in regulatory compliance and technology advancement in warm edge spacer industry.

Germany, the UK, France, and the Nordic nations have been pioneer adopters supported by decades of energy building codes that focus on minimized thermal bridging and higher U-value performance. Market assessment indicates that the region is marked by high-quality manufacturing capacity and a dominant role of industry innovators. In addition, European Union-funded building renovation programs are increasing the range of its applications, especially in the renovation of historic buildings for energy standards. Continuing innovation in spacer material and integral sealant systems also supports Europe's dominance in product innovation.

Latin America is a developing region for warm edge technology, with significant activity in Brazil, Mexico, and Chile. Growth in the region is underpinned by growing construction markets and rising awareness of the advantages of thermal insulation in contemporary building design. Analysis identifies that although existing market penetration is low, take-up is slowly rising among high-end real estate developments and environmentally accredited buildings. The region provides long-term potential as energy codes change and consumer preference moves toward energy-efficient glazing solutions.

The Middle East and Africa are still in the early stages of warm edge spacer uptake, yet urban development and an increasing interest in sustainable building are starting to impact product demand. The UAE, Saudi Arabia, and South Africa are all investing in smart city projects and high-performance buildings where thermal control and solar control are critical. Based on regional analysis, companies bringing forth affordable and climate-friendly spacer solutions will have substantial space for growth, especially as energy consumption issues become more prevalent in hot-weather regions.

Top Key Players & Market Share Insights:

The warm edge spacer market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global warm edge spacer market. Key players in the warm edge spacer industry include -

- Swisspacer (Switzerland)

- Ensinger GmbH (Germany)

- Glas Trösch Group (Switzerland)

- Alu-Pro Srl (Italy)

- B. Fuller Company (United States)

- Technoform Glass Insulation GmbH (Germany)

- Saint-Gobain S.A. (France)

- Fenzi Group (Italy)

- AGC Inc. (Japan)

- TGI-Spacer (Technoform Glass Insulation) (Germany)

Recent Industry Developments :

Product Launches:

- In February 2025, Milgard Windows and Doors launched the new AX450 aluminum moving glass wall, which includes a warm-edge spacer system as well as a thermally improved aluminum frame to ensure energy efficiency. Optional upgrades consisting of low-emissivity glass and gas between the panes are also available.

Acquisitions:

- In July 2024, Fenzi Group acquired Thermoseal and expanded its Spacer range of products. Thermoseal’s wide product portfolio, especially the Thermoflex flexible spacer product, will enable Fenzi Group to expand their sales internationally.

Warm Edge Spacer Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 844.73 Million |

| CAGR (2025-2032) | 3.4% |

| By Material Type |

|

| By Product Type |

|

| By Glazing Window |

|

| By End Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Warm Edge Spacer Market? +

Warm Edge Spacer Market size is estimated to reach over USD 844.73 Million by 2032 from a value of USD 648.52 Million in 2024 and is projected to grow by USD 658.75 Million in 2025, growing at a CAGR of 3.4% from 2025 to 2032.

What specific segmentation details are covered in the Warm Edge Spacer Market report? +

The Warm Edge Spacer market report includes specific segmentation details for material type, product type, glazing window and end-use industry.

What are the end-use industry in the Warm Edge Spacer Market? +

The end-use industry of the Warm Edge Spacer market is building & construction, automotive, aerospace, and marine and others.

Who are the major players in the Warm Edge Spacer Market? +

The key participants in the Warm Edge Spacer market are Swisspacer (Switzerland), Ensinger GmbH (Germany), Technoform Glass Insulation GmbH (Germany), Saint-Gobain S.A. (France), Fenzi Group (Italy), AGC Inc. (Japan), TGI-Spacer (Technoform Glass Insulation) (Germany), Glas Trösch Group (Switzerland), Alu-Pro Srl (Italy) and H.B. Fuller Company (United States).