- Summary

- Table Of Content

- Methodology

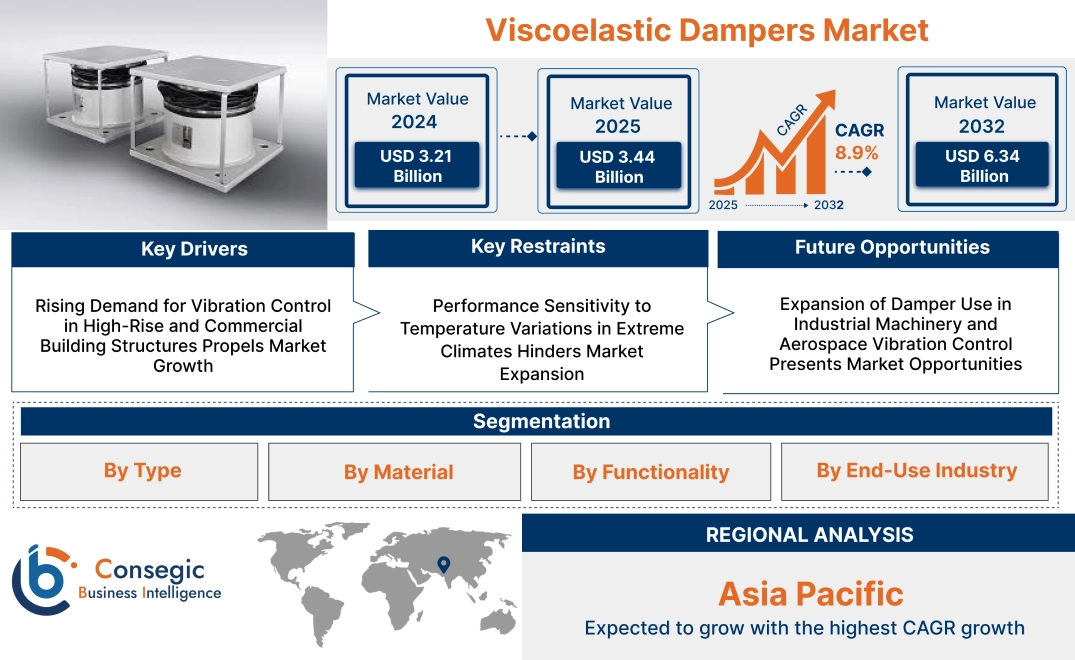

Viscoelastic Dampers Market Size:

Viscoelastic Dampers Market size is estimated to reach over USD 6.34 Billion by 2032 from a value of USD 3.21 Billion in 2024 and is projected to grow by USD 3.44 Billion in 2025, growing at a CAGR of 8.9% from 2025 to 2032.

Viscoelastic Dampers Market Scope & Overview:

Viscoelastic dampers are passive energy dissipation devices engineered to absorb and reduce vibrational energy in structures subjected to dynamic forces such as wind, seismic activity, or mechanical loads. These dampers utilize viscoelastic materials that exhibit both viscous and elastic properties, converting kinetic energy into heat to minimize structural displacement and stress.

Commonly integrated into building frames, bridges, and industrial equipment, viscoelastic dampers are designed with steel plates bonded by viscoelastic layers. They perform consistently over a wide temperature and frequency range, ensuring effective damping during both minor and extreme events.

Benefits include enhanced occupant comfort, reduced maintenance costs, and extended structural lifespan. Their low-maintenance nature and compatibility with both new construction and retrofitting projects make them a versatile solution for improving structural performance. Additionally, they play a vital role in supporting resilient design practices, helping structures maintain stability and serviceability under variable dynamic loading conditions.

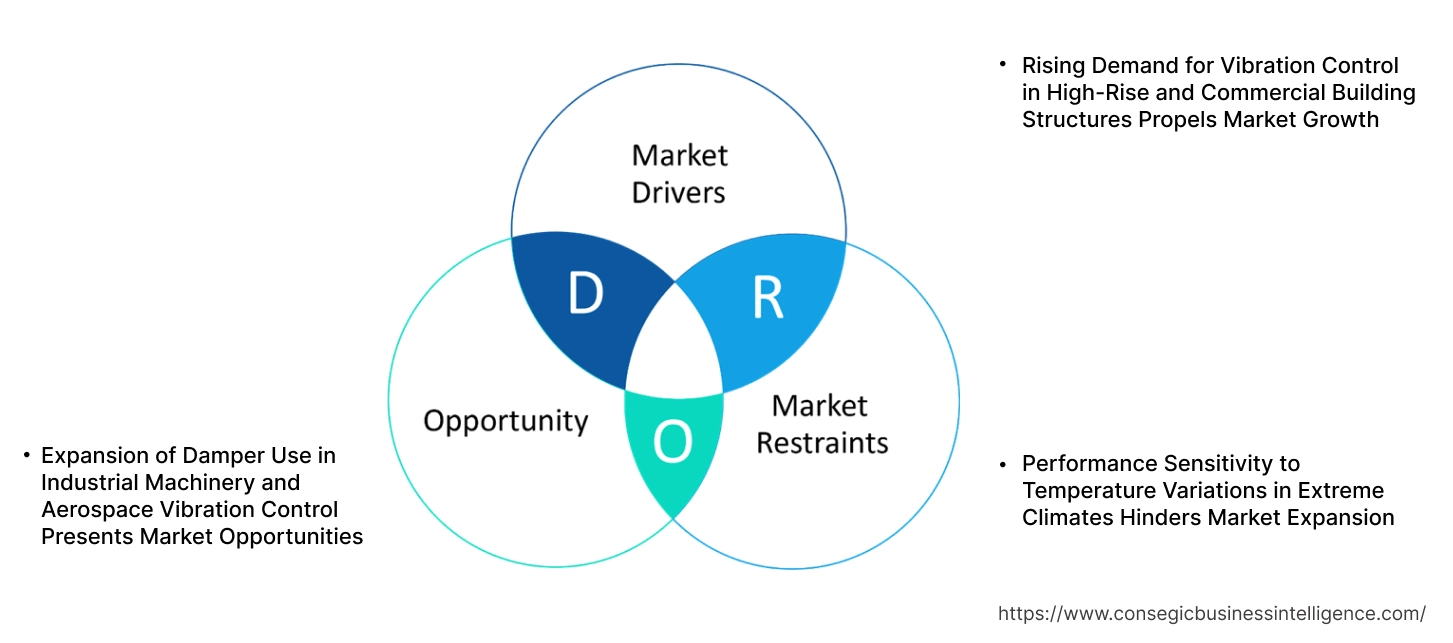

Viscoelastic Dampers Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Vibration Control in High-Rise and Commercial Building Structures Propels Market Growth

The increasing height and flexibility of modern high-rise and commercial buildings have intensified the need for advanced vibration control systems. Viscoelastic dampers are widely adopted in such structures to dissipate dynamic energy caused by wind loads, seismic activity, and occupant motion. These dampers enhance occupant comfort, protect structural elements, and reduce fatigue in key components over time. Their compact design and ability to provide simultaneous stiffness and damping make them highly effective for retrofitting and new construction alike. Urban development trends, particularly in seismic and wind-prone regions, are accelerating the integration of damping solutions in high-value real estate and institutional buildings. With engineers and architects prioritizing building resilience and performance-based design, the need for passive control technologies is steadily rising. The growing need for structural stability and motion reduction is driving consistent viscoelastic dampers market expansion.

Key Restraints:

Performance Sensitivity to Temperature Variations in Extreme Climates Hinders Market Expansion

The damping characteristics of viscoelastic materials are strongly influenced by ambient temperature. In extreme climates—such as arid deserts or polar regions—the materials may soften or harden, altering the intended damping performance. Such variations affect the consistency of energy dissipation and compromise the structural protection provided by the system. Engineers often require supplementary modeling or material calibration to maintain reliability across wide thermal ranges, which increases project complexity and cost. Additionally, temperature-sensitive behavior reduces user confidence in regions where climate conditions fluctuate significantly throughout the year. Despite growing demand for vibration control technologies, this thermal limitation remains a significant challenge—restricting wider adoption in harsh environments and slowing viscoelastic dampers market growth in climate-sensitive infrastructure.

Future Opportunities :

Expansion of Damper Use in Industrial Machinery and Aerospace Vibration Control Presents Market Opportunities

Beyond buildings and infrastructure, viscoelastic dampers are gaining traction in precision-driven sectors such as industrial automation and aerospace. In industrial settings, these dampers are used to isolate sensitive equipment from floor vibrations, reduce machinery wear, and minimize acoustic emissions. In aerospace, they play a critical role in controlling airframe vibrations, protecting avionics, and enhancing passenger comfort. The rising demand for vibration mitigation in high-speed, high-precision systems is expanding the scope of application beyond conventional construction. Growth in advanced manufacturing and aerospace innovation is fueling interest in lightweight, durable, and temperature-tolerant damping materials. With product development focused on tailored formulations and modular designs, they are finding new relevance across dynamic environments. As requirement increases for mechanical stability and equipment protection, these emerging applications are unlocking strong viscoelastic dampers market opportunities driven by cross-sector growth and functional diversification.

Viscoelastic Dampers Market Segmental Analysis :

By Type:

Based on type, the viscoelastic dampers market is divided into linear, non-linear, and others.

The linear segment accounted for the largest revenue share in 2024.

- Linear dampers are widely used due to their predictable and stable performance under constant loading conditions, making them ideal for infrastructure and automotive applications.

- These dampers provide reliable damping in both low and high-frequency vibration control applications.

- They are commonly utilized in bridges, buildings, and other structures to mitigate vibration-induced stresses, ensuring safety and longevity.

- As per viscoelastic dampers market analysis, linear dampers dominate due to their widespread use in construction projects that require constant vibration control.

The non-linear segment is expected to witness the fastest CAGR during the forecast period.

- Non-linear versions offer superior energy dissipation capabilities, making them ideal for high-stress applications such as seismic protection.

- These dampers perform better in dynamic loading scenarios and are widely adopted in earthquake-resistant infrastructure.

- Their ability to adapt to varying forces provides enhanced safety and flexibility, especially in regions prone to seismic activity.

- According to viscoelastic dampers market trends, the increasing frequency of seismic events and natural disasters is pushing the need for non-linear damping solutions in infrastructure projects.

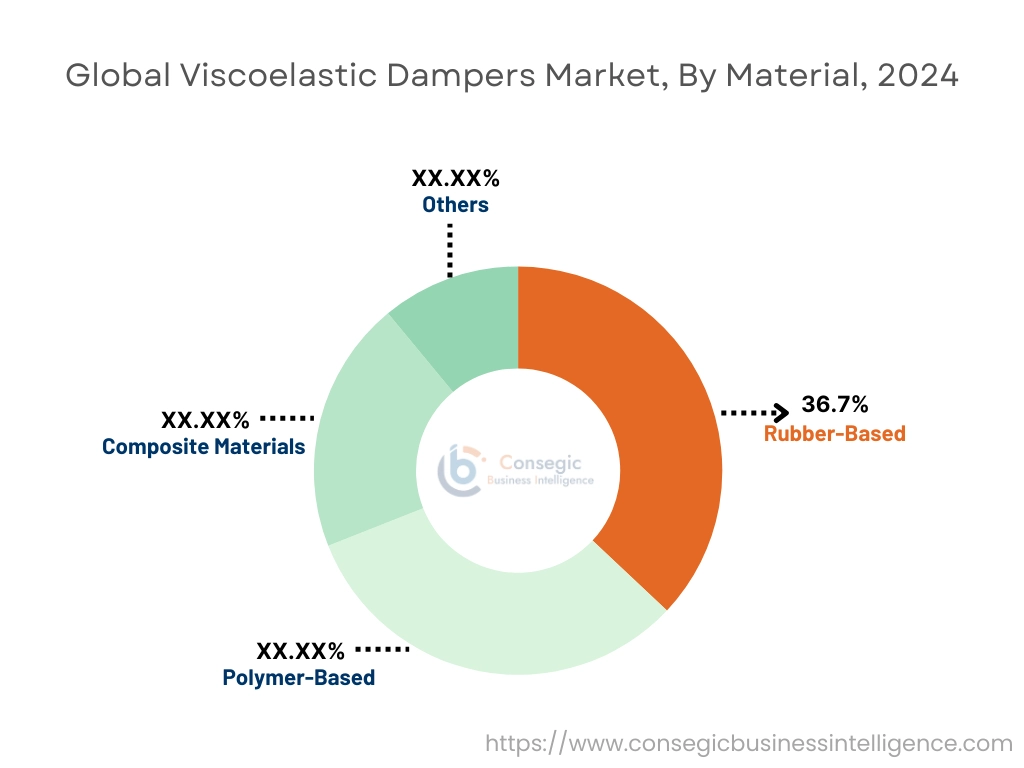

By Material:

Based on material, the market is segmented into rubber-based, polymer-based, composite materials, and others.

The rubber-based segment held the largest viscoelastic dampers market share of 36.7% in 2024.

- Rubber-based dampers are commonly used for vibration isolation and shock absorption, particularly in buildings, machinery, and transportation systems.

- Rubber dampers are cost-effective, durable, and provide excellent performance in moderate to low-frequency vibrations.

- These dampers are particularly favored in the automotive and construction sectors due to their affordability and high durability.

- As per viscoelastic dampers market analysis, the rubber-based segment remains dominant due to its balance of performance and cost-effectiveness in various applications.

The composite materials segment is projected to register the fastest CAGR.

- Composite materials, such as carbon fiber and fiberglass-based dampers, offer superior strength-to-weight ratios, making them ideal for high-performance applications in aerospace and energy sectors.

- These materials provide better damping performance, longer lifespan, and reduced weight compared to traditional rubber dampers, especially in high-demand applications.

- Their adoption is increasing in industries that require lightweight and durable components for vibration control and energy dissipation.

- Thus, the shift towards high-performance materials is expected to drive the viscoelastic dampers market growth via the composite materials segment.

By Functionality:

Based on functionality, the market is segmented into vibration control, seismic protection, noise reduction, and energy dissipation.

The vibration control segment accounted for the largest revenue share in 2024.

- Vibration control is essential in various industries, including construction, automotive, and manufacturing, to prevent damage to structures and machinery.

- Viscoelastic dampers used for vibration control are crucial in reducing mechanical fatigue and ensuring smoother operations in equipment and buildings.

- The need to protect sensitive equipment from mechanical vibrations drives consistent need in industrial sectors.

- As per viscoelastic dampers market trend, the vibration control segment continues to dominate due to its critical role in infrastructure, automotive, and manufacturing applications.

The seismic protection segment is expected to experience the fastest CAGR.

- Seismic protection dampers are increasingly used in earthquake-prone regions to protect buildings, bridges, and other critical infrastructure from seismic forces.

- These dampers help reduce building displacement, providing enhanced safety during seismic events.

- The increasing frequency of earthquakes and stringent regulations on earthquake-resistant buildings are driving the adoption of seismic protection systems.

- Hence, the growing investment in earthquake-resilient infrastructure and urban development is boosting the viscoelastic dampers market demand.

By End-Use Industry:

Based on end-use industry, the market is segmented into infrastructure, aerospace, automotive, energy, manufacturing, and others.

The infrastructure segment held the largest viscoelastic dampers market share in 2024.

- They are widely used in infrastructure applications, including bridges, high-rise buildings, and tunnels, to reduce vibrations and increase structural integrity.

- The need to enhance the resilience of buildings against earthquakes, wind-induced oscillations, and traffic vibrations drives its adoption.

- With increasing urbanization and the expansion of infrastructure projects globally, the need for these dampers remains robust.

- Thus, the infrastructure sector continues to be the dominant end-user industry due to the rising viscoelastic dampers market demand for durable, safe, and sustainable construction.

The aerospace segment is projected to grow at the fastest CAGR during the forecast period.

- Aerospace applications require viscoelastic dampers for vibration isolation in both aircraft and spacecraft to protect sensitive equipment and improve passenger comfort.

- The increasing requirement for quieter, more efficient aircraft and space vehicles is fueling the adoption of advanced damping systems.

- Aerospace engineers are increasingly incorporating them in both commercial and military aviation to reduce noise and improve operational efficiency.

- Additionally, the aerospace sector is expected to drive the viscoelastic dampers market expansion as the need for lightweight, high-performance components increases.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

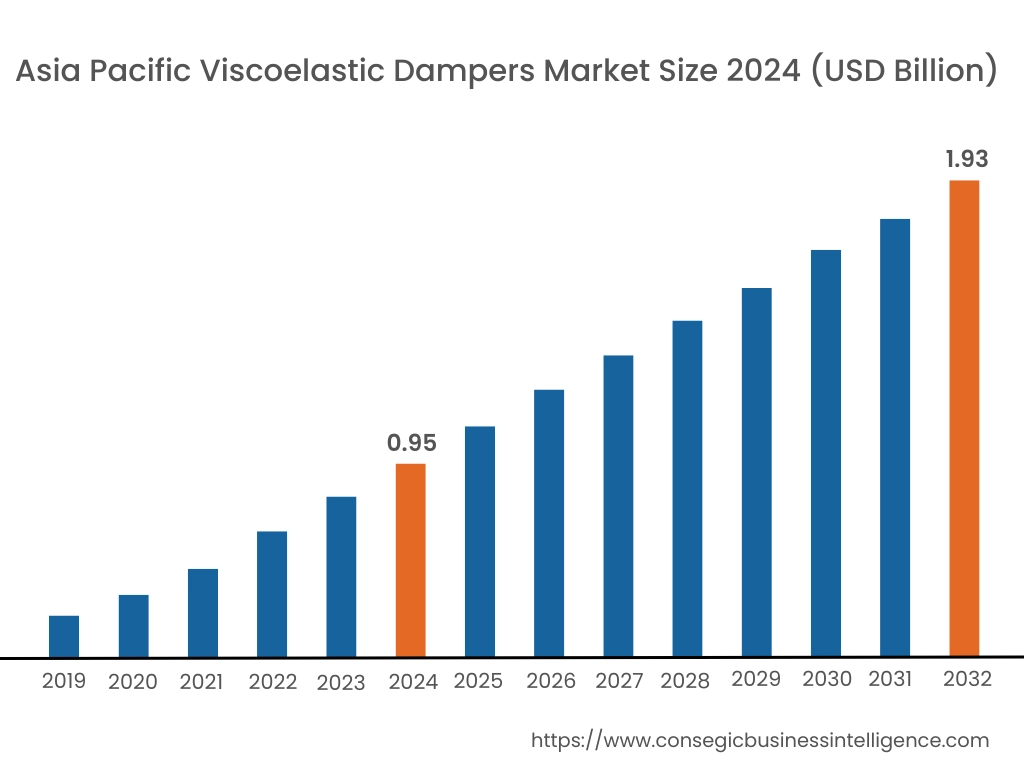

Asia Pacific region was valued at USD 0.95 Billion in 2024. Moreover, it is projected to grow by USD 1.02 Billion in 2025 and reach over USD 1.93 Billion by 2032. Out of this, China accounted for the maximum revenue share of 38.2%. Asia-Pacific demonstrates the highest rate of implementation, underpinned by frequent seismic activity and extensive vertical development. Japan, South Korea, and Taiwan lead regional usage, with widespread deployment of viscoelastic dampers in mid- to high-rise buildings, commercial complexes, and transportation infrastructure. Market analysis reveals a strong push for integrated structural systems that combine damping devices with smart monitoring solutions. In emerging economies such as China and India, urban expansion and new building codes are creating momentum for wider adoption. Continued growth is reinforced by public-private partnerships, expanding construction volumes, and growing awareness of long-term cost savings through damage mitigation.

North America is estimated to reach over USD 2.05 Billion by 2032 from a value of USD 1.06 Billion in 2024 and is projected to grow by USD 1.14 Billion in 2025. In North America, adoption of viscoelastic dampers is notably advancing across seismic zones, particularly in the western United States and parts of Canada. Market analysis indicates strong demand in the commercial and institutional sectors, where retrofitting of aging infrastructure and high-performance building standards requires advanced damping systems. Application in high-rise towers, hospitals, and cultural landmarks is expanding, as these systems help meet performance-based design codes. Growth in this region is supported by increasing government investment in resilient infrastructure and a well-established engineering ecosystem focused on passive energy dissipation technologies.

Europe represents a steadily developing market, particularly in earthquake-prone southern countries like Italy, Greece, and Turkey. Market analysis shows that they are being integrated into public facilities and historical structures where traditional base isolation is not feasible. In northern regions, application is expanding in vibration-sensitive buildings such as laboratories and transportation hubs. The market opportunity in Europe is boosted by renovation of heritage infrastructure, alignment with EU seismic mitigation initiatives, and the need for building materials that contribute to lifecycle durability and occupant safety during dynamic loads.

Latin America is observing gradual adoption, primarily in countries such as Mexico, Chile, and Peru, where seismic risk is high and urban development is expanding. Market analysis indicates that government-led infrastructure projects and select private developments are beginning to specify damping systems to enhance structural safety. Although cost sensitivity remains a consideration, increased attention to earthquake damage reduction is encouraging adoption in hospitals, schools, and commercial towers. The viscoelastic dampers market opportunity in the region lies in integrating damping solutions within regional building codes and showcasing their performance in local seismic retrofitting projects.

In the Middle East and Africa, the use of viscoelastic dampers is emerging, especially in high-rise developments and critical infrastructure projects. The UAE and Saudi Arabia are incorporating damping technologies into modern architectural designs for towers, airports, and cultural centers. Market analysis shows that while seismic vulnerability is lower in many parts of the region, the demand for wind-induced vibration control and structural comfort is increasing. In select African nations with seismic activity, early-stage projects are exploring damping solutions in bridge and institutional building construction. Growth is expected as regional standards evolve and the benefits of structural damping are demonstrated through flagship developments.

Top Key Players and Market Share Insights:

The viscoelastic dampers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global viscoelastic dampers market. Key players in the viscoelastic dampers industry include -

- Taylor Devices, Inc. (USA)

- FIP Industriale S.p.A. (Italy)

- Kinetics Noise Control, Inc. (USA)

- GERB Vibration Control Systems (Germany)

- Toyo Tire Corporation (Japan)

- Maurer SE (Germany)

- Sumitomo Rubber Industries, Ltd. (Japan)

- Taylor Devices Asia Ltd. (China)

- Nippon Steel Engineering Co., Ltd. (Japan)

- Mageba SA (Switzerland)

Viscoelastic Dampers Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6.34 Billion |

| CAGR (2025-2032) | 8.9% |

| By Type |

|

| By Material |

|

| By Functionality |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Viscoelastic Dampers Market? +

Viscoelastic Dampers Market size is estimated to reach over USD 6.34 Billion by 2032 from a value of USD 3.21 Billion in 2024 and is projected to grow by USD 3.44 Billion in 2025, growing at a CAGR of 8.9% from 2025 to 2032.

What specific segmentation details are covered in the Viscoelastic Dampers Market report? +

The Viscoelastic Dampers market report includes specific segmentation details for type, material, functionality and end-use industry.

What are the end-use industries of the Viscoelastic Dampers Market? +

The end-use industries of the Viscoelastic Dampers Market are infrastructure, aerospace, automotive, energy, manufacturing, and others.

Who are the major players in the Viscoelastic Dampers Market? +

The key participants in the Viscoelastic Dampers market are Taylor Devices, Inc. (USA), FIP Industriale S.p.A. (Italy), Maurer SE (Germany), Sumitomo Rubber Industries, Ltd. (Japan), Taylor Devices Asia Ltd. (China), Nippon Steel Engineering Co., Ltd. (Japan), Mageba SA (Switzerland), Kinetics Noise Control, Inc. (USA), GERB Vibration Control Systems (Germany) and Toyo Tire Corporation (Japan).