- Summary

- Table Of Content

- Methodology

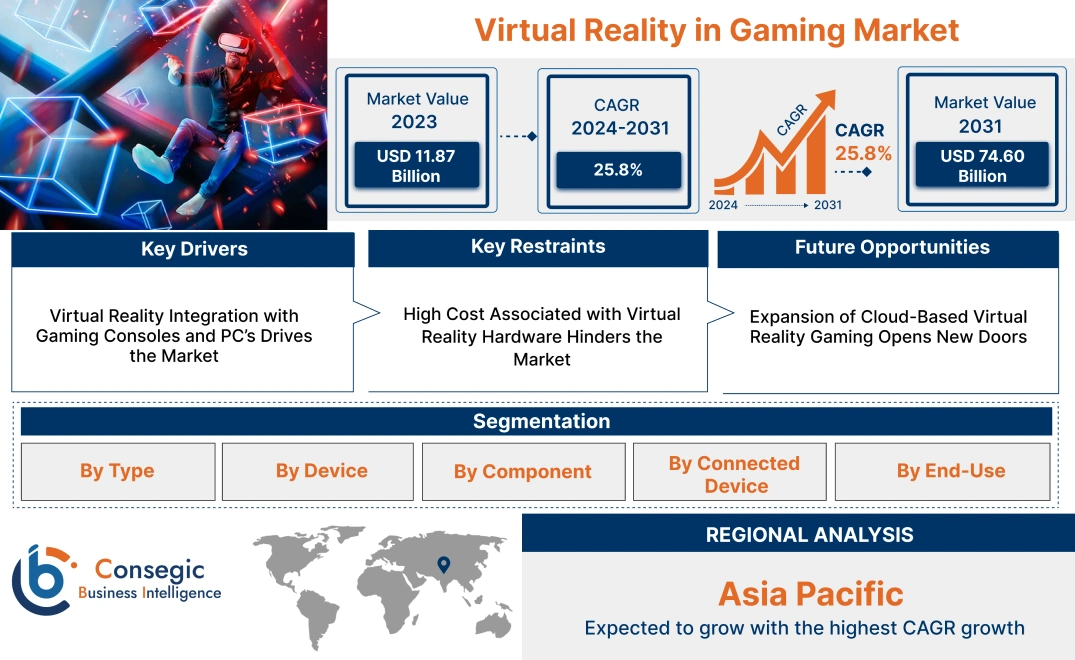

Virtual Reality in Gaming Market Size:

Virtual Reality in Gaming Market size is estimated to reach over USD 74.60 Billion by 2031 from a value of USD 11.87 Billion in 2023, and is projected to reach over USD 14.73 Billion, growing at a CAGR of 25.8% from 2024 to 2031.

Virtual Reality in Gaming Market Scope & Overview:

Virtual reality refers to a technology that uses a near-eye display device to create a simulated environment. It gives the illusion of being physically present in that environment and offers a 360-degree view. Virtual reality is versatile and can be used for distance education, games, surveys, healthcare, and others. Moreover, virtual reality offers a range of benefits including experiential learning, increased learner attention, a safe and controlled environment, and others. The above benefits of virtual reality are primary determinants for driving the market.

For instance, in February 2023 Sony Interactive Entertainment (SIE) released a new model of PlayStation VR2 and it represents the next level of virtual reality gaming. The PlayStation VR2 Sense controller has haptic feedback, adaptive triggers, and finger sensing, while headset feedback uses vibrations to create the feeling of being inside the game which makes it exciting.

Virtual Reality in Gaming Market Insights:

Virtual Reality in Gaming Market Dynamics - (DRO) :

Key Drivers:

Virtual Reality Integration with Gaming Consoles and PC's Drives the Market

A key driver of this shift is the rising popularity of virtual reality (VR), as an increasing number of consumers adopt VR headsets. Additionally, VR systems now include complementary accessories such as motion controllers, designed to enhance user interaction and engagement. These components, alongside VR headsets, cater to the demand for fully immersive live-action gaming and media experiences. Furthermore, continuous advancements in compact VR gaming devices contribute to ongoing innovation within the video game industry.

- For instance, Every Oculus Rift package includes the Xbox One controller, which can make the gaming experience more cohesive across Xbox One and Windows 10 devices. The gaming experience can be heightened through fine-tuned impulse triggers and responsive controls. Moreover, Windows 10 allows streaming of Xbox One games to the Rift giving users an opportunity to replay favorites such as Halo and Forza from a virtual cinema screen. Windows 10, combined with DirectX 12, provides optimal performance for VR gaming on the Rift.

Thus, as per the market trends analysis, the expanding adoption of VR technology, supported by advanced accessories and compact device innovations, is significantly driving transformation within the video game industry, driving the virtual reality in gaming market demand.

Key Restraints :

High Cost Associated with Virtual Reality Hardware Hinders the Market

The high cost associated with virtual reality (VR) hardware, including expensive VR headsets and the requirement of powerful gaming PCs, poses a significant barrier to the widespread adoption of VR gaming. A significant proportion of potential buyers are no longer interested in purchasing VR equipment because they are costly. Moreover, developing attractive games for VR technology is quite challenging and costly, which contributes to the high expenses for consumers when utilizing it.

For instance, in March 2024 Sony reportedly paused production of the PlayStation VR2 due to unsold inventory. Despite initially strong sales, the lack of compelling content and a higher price point compared to the PS5 have impacted its performance. Sony's decision reflects the challenges faced by VR hardware in the gaming market.

Therefore, the analysis of market trends depicts that the high costs of VR hardware and the substantial investment required to develop engaging VR content remain major obstacles to the broader adoption of VR gaming, hindering the virtual reality in gaming market growth.

Future Opportunities :

Expansion of Cloud-Based Virtual Reality Gaming Opens New Doors

The integration of cloud-based virtual reality gaming presents a significant opportunity in the VR gaming market. By leveraging cloud technology, companies can reduce the dependency on high-end hardware, enabling users to access immersive VR experiences through streaming rather than requiring powerful gaming PCs or expensive VR headsets. This approach not only lowers costs for consumers but also expands accessibility, making VR gaming more attainable for a broader audience. With advancements in 5G and high-speed internet, cloud-based VR gaming has the potential to drive a substantial surge and attract new users to the market.

Thus, the market trends analysis depicts that the adoption of cloud-based VR gaming holds considerable potential to reshape the market by minimizing hardware costs and increasing accessibility, creating lucrative virtual reality in gaming market opportunities.

Virtual Reality in Gaming Market Segmental Analysis :

By Type:

Based on the type, the market is segmented into Fully Immersive, Semi Immersive, and Non-Immersive, Augmented and Collaborative VR.

The Fully Immersive segment accounted for the largest revenue share of the total virtual reality in gaming market share in the year 2023.

- A Fully Immersive VR device refers to a gadget that provides complete involvement, they address every neural sense by making the user feel somewhere else.

- Moreover, Fully Immersive offers a range of benefits including enhanced engagement, improved cognitive processing, and potential applications in healthcare.

- For instance, in May 2024 The Sandbox VR, a premium destination for VR experiences, partnered with Apparel Group, the fashion and lifestyle retailing global leader. This franchise partnership is intended to bring the latest virtual reality technology to the Middle East since it intends to open 25 locations by the end of 2028. They are taking advantage of a collaboration between Apparel Group and its 2,200 stores within 14 countries and 85 brands under its name through this cooperation.

- Thus, segmental trends analysis shows that the fully immersive segment leads the market, driven by enhanced engagement and strategic partnerships, expanding VR's reach and applications globally, and driving the virtual reality in gaming market demand.

The semi-immersive segment is anticipated to register the fastest CAGR during the forecast period.

- A semi-immersive VR device refers to a gadget that lets users experience both realities at once, they mix the light of the real world with virtual light resulting in coexistence during use.

- Moreover, the primary benefits of semi-immersive devices include a balance between realism and digital immersion, suitability for educational or training purposes, and easier implementation on existing equipment.

- For instance, in January 2024, Sony Corporation revealed its plans to develop an immersive spatial content creation system with a 4K OLED microdisplay-fitted XR head-mounted display that can do video see-through plus 3D interaction controllers for simulating an intuitive environment. The technologically advanced 3D content creators will be supported by the system in their work. Siemens, being an industrial firm will be the only company that will be partnered with at the time of introducing this new product.

- Hence, analysis of segmental trends depicts that the semi-immersive segment is poised for growth due to its balance of realism and immersion, boosting the virtual reality in gaming market trends.

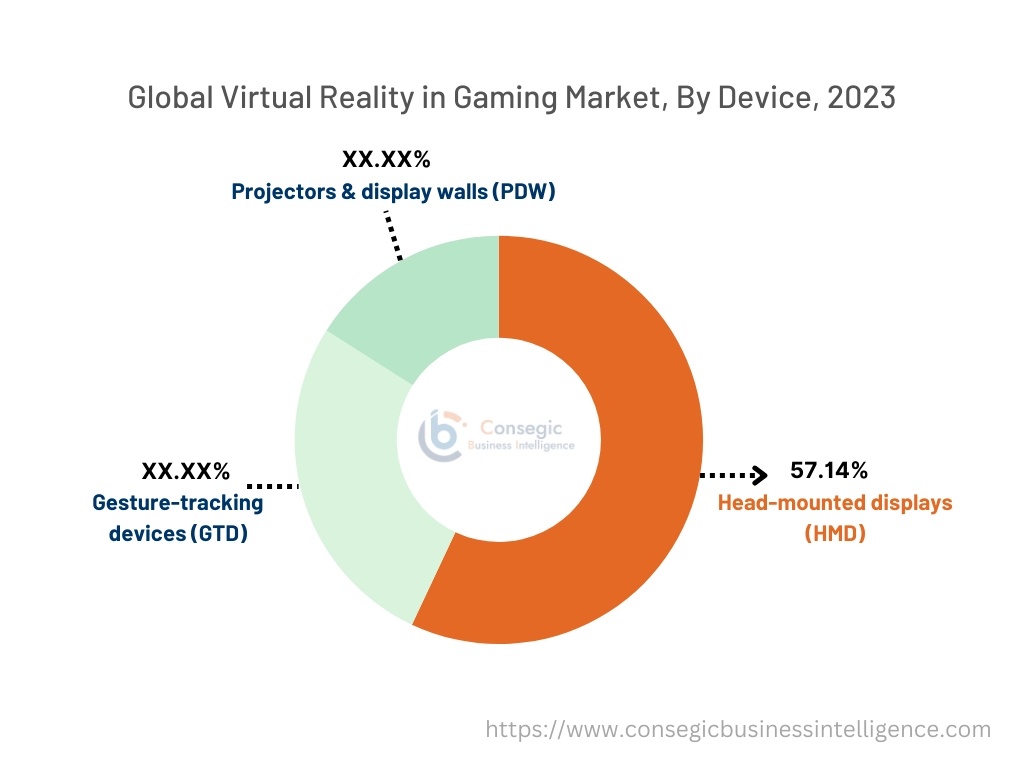

By Device:

Based on the device, the market is segregated into head-mounted displays (HMD), gesture-tracking devices (GTD), and projectors & display walls (PDW).

The head-mounted display (HMD) segment accounted for the largest revenue share of 57.14% in the year 2023.

- Factors including affordable HMDs, increased use of AR and VR devices, technological development, and increased digitalization as well as cheap microdisplays are key aspects driving the segment.

- For instance, in January 2023, Sharp Corporation developed a prototype for a lightweight VR head-mounted display that connects to smartphones and has a high resolution. In addition, it has an autofocus RGB color camera module and can run 120 Hz display refresh rates per second with 4K resolutions. The device has a display function that shows images from reality in color and a pop-up image function that displays reality in a separate VR space window. Furthermore, two B/W cameras for hand-tracking make up the headset so that it operates much more easily without controllers. Its lightweight design in addition to the compact size is another factor that contributes towards it being more fatigue resistant during prolonged use.

- Thus, the HMD segment leads the VR market, driven by technological advancements, affordability, and increasing adoption across multiple sectors, driving the virtual reality in gaming market growth.

Gesture-tracking device (GTD) segment is expected to witness the fastest CAGR during the forecast period.

- Gesture-tracking devices (GTD) offer a range of features, including 3D object manipulation, real-time motion capture, and multi-touch recognition.

- Moreover, these devices provide multiple benefits including enhanced user interaction, improved accessibility, and intuitive control in virtual environments.

- For instance, in May 2023 Ultraleap revealed the second-generation hand-tracking camera called the Leap Motion Controller 2 that enables users to interact naturally with 3D digital content using their hands. The new controller boasts improved features, such as the cameras that have higher resolution and a wider angle but consume 25% less power, and all these are contained in a design that is 30% smaller to get a good fit. The Leap Motion Controller 2 is the most versatile camera from Ultraleap that is able to work with different platforms and devices, which include virtual reality (VR), mixed reality (MR), augmented reality (AR) headsets, personal computers, and holographic displays.

- Thus, as per the segmental trends analysis, the GTD segment is projected for rapid growth due to its advanced features in user interaction and accessibility, boosting the virtual reality in gaming market trends.

By Component:

Based on the component, the market is segregated into hardware and software.

The hardware segment accounted for the largest revenue share of the overall virtual reality in gaming market share in the year 2023.

- Factors including advances in VR device capabilities, elevated consumer need for immersive technologies, and speedier internet connections are key aspects driving the segment.

- For instance, in April 2024 Meta is growing its VR universe by partnering with external hardware companies, such as iPhone and Android. It wants to have many VR devices powered by its OS, versus Apple's closed system and by offering an alternative to the App Store, Meta is giving developers and users more flexibility, and that will drive innovation in the VR hardware space.

- Thus, the hardware segment dominates the VR market, fueled by advancements in VR device capabilities and consumer demand for immersive experiences, driving the virtual reality in gaming market expansion.

The software segment is expected to witness the fastest CAGR during the forecast period.

- Factors including increased demand for realistic virtual environments, advancements in VR software development tools, and the rise of cloud-based VR applications are key aspects driving the segment.

- For instance, Trium Design Company from India is dedicated to developing augmented and virtual realities (AR / VR) technology that deals with consumer-oriented computer vision products that are aimed at enhancing human reality. Trium Designs has come up with a GPS-based AR display system that allows low-cost smartphones to show immersive AR and VR experiences without requiring any other hardware or software components as a way of making mixed reality more accessible.

- Hence, the software segment is expected to grow fastest, driven by demand for realistic VR environments, advancements in development tools, and cloud-based VR solutions, boosting the virtual reality in gaming market opportunities.

By Connected Device:

Based on the connected device, the market is segregated into Gaming Console, PC/ Desktop, and Smartphones.

The gaming consoles segment accounted for the largest revenue share in the year 2023.

- Factors including integration of VR technology with gaming consoles, availability of exclusive VR gaming content, advancements in VR hardware and accessories, and others are key aspects driving the segment.

- For instance, according to Apple, the Apple Vision Pro is compatible with PlayStation DualSense and Xbox Wireless controllers, which enables users to explore thousands of fun games.

- Thus, the gaming consoles lead the connected device market in VR, bolstered by exclusive VR gaming content and compatibility with popular controllers.

The PC and Desktop segment is expected to witness significant CAGR during the forecast period.

- The growth of the PC and Desktop segment is attributed to several factors. For the PC segment, the availability of high-performance gaming PCs with superior hardware specifications facilitates a more immersive and fluid VR gaming experience.

- On the other hand, the growth of the desktop segment is driven by major hardware and software companies investing heavily in the creation of VR-compatible technologies and content.

- These investments are fueling the advancement of this segment in the VR gaming market.

- For instance, according to NVIDIA, Virtual reality (VR) gaming demands powerful GPUs due to high display resolutions, fast refresh rates, and low latency requirements. This level of performance can only be provided by NVIDIA's GeForce RTX GPUs which are ideal for making the latest PC-based VR titles more exciting. They also work well with common systems such as Oculus Quest, Valve Index, and HTC VIVE.

- Hence, the PC and desktop segment is set for significant growth, supported by high-performance hardware and major investments in VR-compatible technology, boosting the virtual reality in gaming market expansion.

By End User:

Based on the end use, the market is segregated into Individual and Commercial.

The individual segment accounted for the largest revenue share in the year 2023 and is expected to witness the fastest CAGR during the forecast period.

- Factors including the availability of various VR games, Social and Multiplayer VR gaming experiences, and increased adoption of VR systems among gamers are key aspects driving the growth of the individual segment.

- For instance, in March 2022 Armature Studio, Oculus Studios, and Capcom clinched the top honor in the VR category at the SXSW Gaming Awards by securing Resident Evil 4's win for Best VR Game of the Year. The game had sold 7 million units by March 2024.

- Therefore, as per the analysis of segmental trends the individual end-use segment dominates, driven by a wide range of VR games and social gaming experiences.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

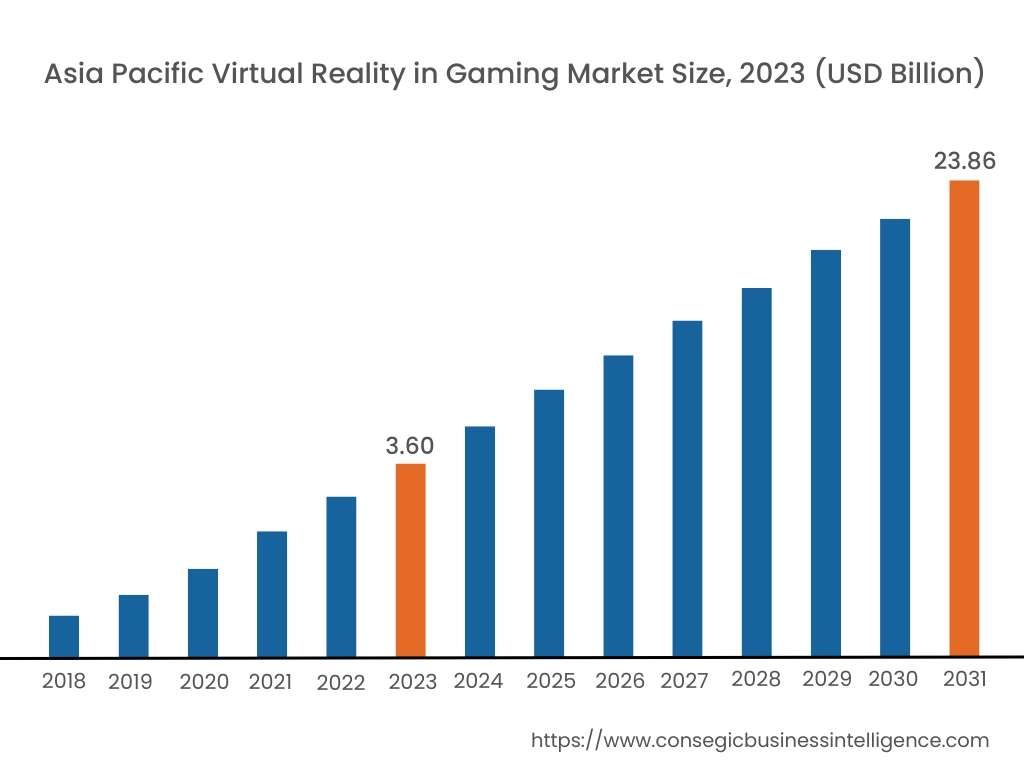

Asia Pacific region was valued at USD 3.60 Billion in 2023. Moreover, it is projected to grow by USD 4.48 Billion in 2024 and reach over USD 23.86 Billion by 2031. Out of this, China accounted for the maximum revenue of 31.8%. The market in the Asia Pacific is primarily driven by the prevalence of engaging and interactive gaming experiences in the region including the demand for VR gaming. Moreover, the rapid rise of the overall gaming industry in countries such as China, Japan, and South Korea has been a prevalent factor for market development in the region.

- For instance, in June 2024 Dream Technology entered the Asia-Pacific market with its first Android-based spatial computer, the Play for Dream MR. In partnership with IMAX and DTS, the Play for Dream MR was created to give IMAX-type visuals alongside customized spatial sound effects. Featuring 8K Micro-OLED displays and driven by the Qualcomm Snapdragon XR2+ Gen 2 platform, it provides an outstanding MR performance. Partnerships with key players in the market guarantee superior user experiences.

North America is estimated to reach over USD 23.87 Billion by 2031 from a value of USD 3.86 Billion in 2023 and is projected to grow by USD 4.79 Billion in 2024. As per the virtual reality in gaming market analysis, the development of increasingly immersive gaming experiences is providing lucrative development prospects for the market in the region. In addition, factors including investments and strategic collaborations in VR gaming and seamless integration of VR technology with gaming consoles are driving the market in the North American region.

- For instance, in March 2024 The Premier League entered a four-year partnership with Rezzil, a Manchester-based virtual reality (VR) software developer known for creating sports gaming software. The goal of this community effort is to invent a VR game in which supporters can feel themselves on the field where they are playing together with their popular players of the Premier League.

Top Key Players & Market Share Insights:

The virtual reality in gaming market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-use launches to hold a strong position in the global virtual reality in gaming market. Key players in the virtual reality gaming industry include-

- Microsoft Corporation (United States)

- Meta Platforms, Inc. (United States)

- HTC Corporation (Taiwan)

- NVIDIA Corporation (United States)

- Unity Technologies Inc. (United States)

- Sony Corporation (Japan)

- Ubisoft Entertainment S.A. (France)

- Google LLC (United States)

- Lenovo Group Limited (China)

- Samsung Electronics Co., Ltd. (South Korea)

Recent Industry Developments :

- In 2024, three major franchises have announced VR-exclusive titles. These include "Alien: Rogue Incursion", a new alien adventure by Survios, "Batman: Arkham Shadow", the first major Batman game in years, and "Metro: Awakening", the latest in the Metro series by Vertigo Games, all offering unique experiences in their respective universes.

Virtual Reality in Gaming Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 74.60 Billion |

| CAGR (2024-2031) | 25.8% |

| By Type |

|

| By Device |

|

| By Component |

|

| By Connected Device |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Virtual Reality in Gaming Market? +

In 2023, the virtual reality in gaming market was USD 11.87 billion.

What will be the potential market valuation for Virtual Reality in Gaming by 2031? +

In 2031, the market size of Virtual Reality in Gaming is expected to reach USD 74.60 billion.

What are the segments covered in the virtual reality in gaming market report? +

Their types, devices, components connected devices, and end uses are the segments covered in this report.

Who are the major players in the virtual reality in gaming market? +

Microsoft Corporation (United States), Meta Platforms, Inc. (United States), HTC Corporation (Taiwan), NVIDIA Corporation (United States), Unity Technologies Inc. (United States), Sony Corporation (Japan), Ubisoft Entertainment S.A. (France), Google LLC (United States), Lenovo Group Limited (China), Samsung Electronics Co., Ltd. (South Korea) are the major players in the virtual reality in gaming market.