- Summary

- Table Of Content

- Methodology

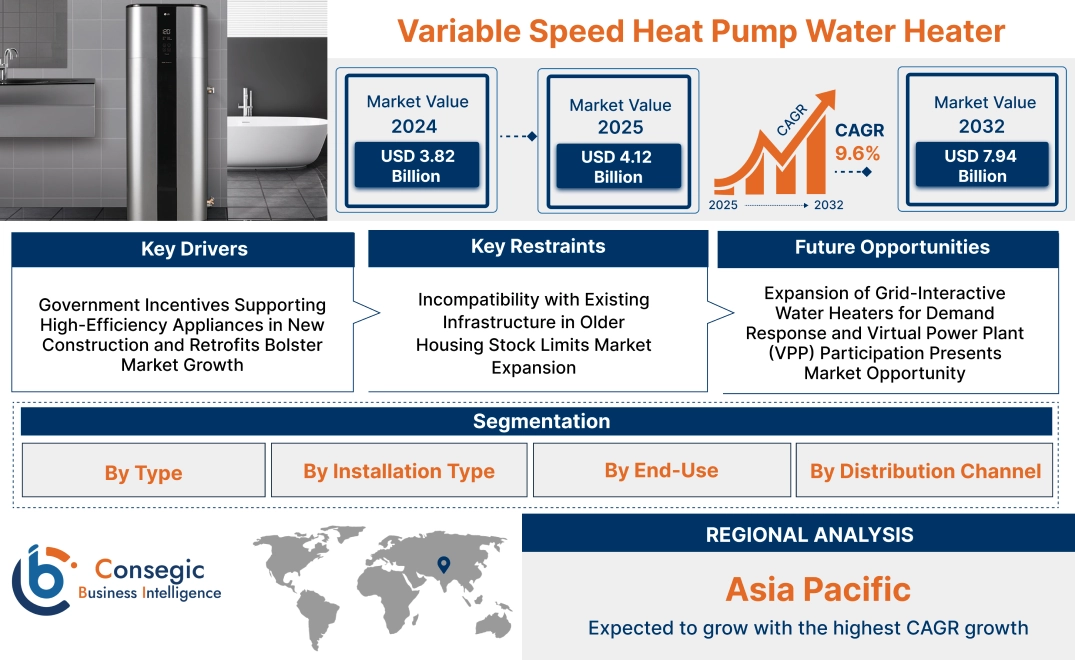

Variable Speed Heat Pump Water Heater Market Size:

Variable Speed Heat Pump Water Heater Market size is estimated to reach over USD 7.94 Billion by 2032 from a value of USD 3.82 Billion in 2024 and is projected to grow by USD 4.12 Billion in 2025, growing at a CAGR of 9.6% from 2025 to 2032.

Variable Speed Heat Pump Water Heater Market Scope & Overview:

Variable speed heat pump water heater is a high-efficiency water heating system that features a variable-speed compressor to dynamically adjust performance in accordance with real-time need. In contrast to single-speed units, it modulates output to provide consistent temperature while optimizing energy use. It is designed to support both residential and light commercial applications that require dependable hot water supply.

Integral to these are built-in smart controls, multi-speed fans, and insulated storage tanks. Adaptive operation, quieting, and Wi-Fi monitoring increase user convenience and system responsiveness. The design optimizes load matching, minimizes cycling, and extends component life.

By varying output based on usage, variable speed heat pump water heater provides accurate thermal regulation, reduced operating expense, and less environmental footprint. Its adaptability to renewable energy systems and installed plumbing base makes it a universal application for contemporary, efficiency-oriented water heating systems in varied installation environments.

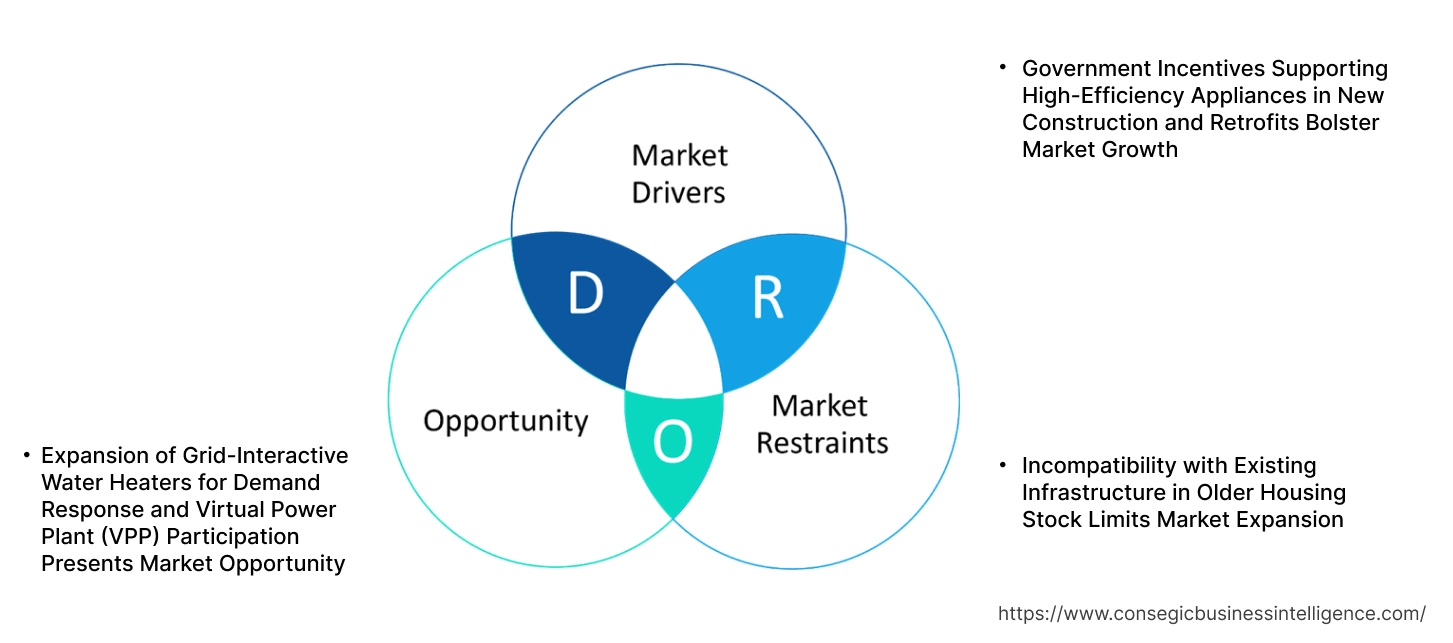

Variable Speed Heat Pump Water Heater Market Dynamics - (DRO) :

Key Drivers:

Government Incentives Supporting High-Efficiency Appliances in New Construction and Retrofits Bolster Market Growth

National and regional governments are actively encouraging the use of high-efficiency water heating systems through special rebate programs, tax credits, and regulatory requirements. Variable speed heat pump water heaters are frequently given priority under these programs because they are energy-sipping and have higher seasonal efficiency ratings. In the U.S., Canada, Germany, and Australia markets, incentives are provided for both new green building construction and residential retrofits. These products reduce the cost of effective purchase, and higher-end systems are thus made affordable to a larger group of consumers. Most building codes increasingly include minimum energy performance requirements, which encourage builders to specify heat pump-based solutions at the time of construction.

- For instance, in May 2024, New York, USA launched new heat pump rebates as part of the Department of Energy (DOE) Home Energy Rebates Program. Expected to be rolled out in other states as well, the program offers direct-to-consumer rebates for the purchase of qualifying appliances. An ENERGY STAR®-certified electric heat pump water heater receives up to $1,750 in rebate.

As environmental concerns mount and economic incentives follow performance objectives, demand for these products keeps increasing, favoring long-term variable speed heat pump water heater market expansion.

Key Restraints:

Incompatibility with Existing Infrastructure in Older Housing Stock Limits Market Expansion

One of the most significant obstacles to adoption of high-end water heating systems is the absence of physical and electrical infrastructure in traditional residential structures. Heat pump water heaters with variable speed commonly need proper ventilation, generous clearance, and separate electrical circuits for safe and optimal operation. Numerous pre-1980 homes, especially those in central city areas and rural areas, do not have the structural provisions or panel capacity for installation with minimal changes. Retrofitting of such buildings adds installation time, expense, and complexity to the process, thereby reducing the appeal of replacement to cost-conscious homeowners. Where housing inventory remains unelectrified or contractor networks are not built to handle such retrofits, the rate of conversion is limited. Even with increasing demand for high-efficiency appliances, infrastructure limitations continue to limit variable speed heat pump water heater market growth.

Future Opportunities :

Expansion of Grid-Interactive Water Heaters for Demand Response and Virtual Power Plant (VPP) Participation Presents Market Opportunity

Utilities and energy aggregators are increasingly looking to smart appliances as a means of load balancing and grid stability. Grid-interactive variable speed heat pump water heaters provide thermal storage and operational flexibility, allowing them to react to time-of-use pricing and real-time signals. When combined with demand response platforms or virtual power plant ecosystems, these systems enable grid-friendly load shifting without user discomfort. This is a win-win situation—reduced operation costs for customers and enhanced peak need management for utilities. Companies that include open communication protocols, cloud-based control systems, and API-compatible energy dashboards in their products are well-placed to dominate this segment.

- For instance, in March 2025, PG&E launched the Seasonal Aggregation of Versatile Energy (SAVE), an Electric Program Investment Charge (EPIC) demonstration and the first virtual power plant program (VPP) which utilizes residential distributed energy to lower local grid constraints. This program includes 1,500 electric residential customers with battery energy storage systems and 400 smart electric panel customers. This contributes heavily to a clean energy future.

As grid modernization initiatives gain speed globally, the intersection of HVAC and energy markets is generating robust variable speed heat pump water heater market opportunities with roots in growth and innovation.

Variable Speed Heat Pump Water Heater Market Segmental Analysis :

By Type:

Based on type, the market is segmented into integrated (all-in-one) systems and split systems.

The integrated (all-in-one) systems segment accounted for the largest variable speed heat pump water heater market share in 2024.

- These systems combine the tank and compressor into a single unit, simplifying installation and reducing space requirements in residential and light commercial applications.

- Their compact design and plug-and-play capability make them ideal for retrofits, particularly in homes with limited mechanical space.

- Integrated units are also favored for their quieter operation and factory-sealed components, which reduce on-site labor and leakage risks.

- As per variable speed heat pump water heater market analysis, the segment leads due to its suitability for domestic hot water needs and ease of deployment across diverse climates.

The split systems segment is projected to witness the fastest CAGR during the forecast period.

- Split systems separate the compressor from the storage tank, allowing for more flexible placement and improved thermal efficiency in larger-scale setups.

- These systems are widely used in commercial and multifamily residential buildings where outdoor space for the compressor is available.

- Their modularity supports energy optimization and integration with building-wide HVAC systems or solar thermal support.

- According to variable speed heat pump water heater market trends, growing adoption in commercial retrofitting projects is accelerating the segment’s expansion.

By Installation Type:

Based on installation type, the market is categorized into indoor installation and outdoor installation.

The indoor installation segment accounted for the largest revenue share in 2024.

- Indoor installations are prevalent in cold and moderate climates where maintaining operational efficiency is essential regardless of external temperature fluctuations.

- These setups often leverage ambient air from mechanical rooms or basements, ensuring consistent performance throughout the year.

- Builders prefer indoor installations for integrated systems in new housing developments to streamline mechanical layout and plumbing.

- For instance, in January 2023, Bosch Thermotechnology launched two additions to its electric tankless water heater lineup to provide customers new levels of efficiency regarding on-demand hot water.

- According to variable speed heat pump water heater market analysis, the dominance of indoor systems reflects both climate constraints and regulatory energy efficiency requirements.

The outdoor installation segment is anticipated to register the fastest CAGR during the forecast period.

- Outdoor installations offer noise isolation and better airflow, making them suitable for large commercial or split-system residential applications.

- These systems enable easy retrofitting without altering internal building layouts or disturbing indoor aesthetics.

- Markets in Asia-Pacific and Southern Europe, with favorable year-round temperatures, are driving the need for outdoor-configured units.

- As per variable speed heat pump water heater market trends, growing product innovation in weatherproofing and frost-resistant technologies supports this segment’s rapid acceleration.

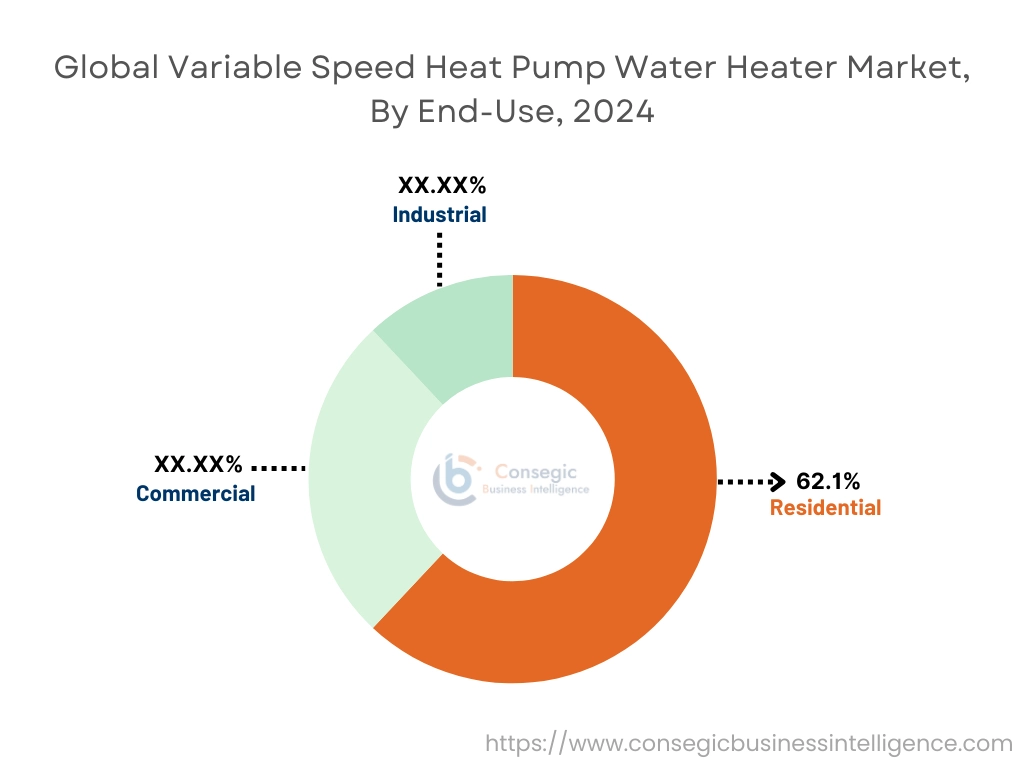

By End-Use:

Based on end-use, the market is segmented into residential, commercial, and industrial.

The residential segment held the largest variable speed heat pump water heater market share of 62.1% in 2024.

- Households increasingly prefer variable speed systems for energy savings, especially in regions with time-of-use electricity pricing.

- Smart home integration and remote operation features enhance user experience and encourage residential uptake.

- Energy-efficient housing policies and incentive programs in North America and Europe contribute significantly to this segment’s expansion.

- For instance, in December 2024, Samsung unveiled new residential air-to-water heat pumps for heating and domestic hot water (DHW) in multi-unit homes, apartments, new builds and retrofits. Integrated with AI Home, users can monitor the status and energy usage of other solar photovoltaic (PV) devices using the zone overview, as well as control other SmartThings-connected appliances.

- Hence, consistent requirement from new residential construction and retrofits sustains the variable speed heat pump water heater market growth.

The commercial segment is projected to grow at the fastest CAGR during the forecast period.

- Commercial buildings such as hotels, hospitals, and educational institutions require large volumes of hot water throughout the day, making them ideal candidates for efficient heat pump systems.

- Split system configurations are increasingly deployed in commercial facilities to meet zoning and thermal load distribution needs.

- This segment is further driven by rising energy costs and strict emissions regulations, prompting businesses to switch from gas to electric water heating systems.

- As per market strategies, scalability and compatibility with renewable energy sources make these systems a strong fit for commercial operators.

By Distribution Channel:

Based on distribution channel, the market is divided into online retail and offline retail (distributors, dealers, installers).

The offline retail segment held the largest revenue share in 2024.

- Most heat pump water heaters are sold through installer networks and HVAC distributors who offer product consultation, system design, and professional installation.

- Offline channels provide after-sales support, maintenance packages, and system integration services, which are critical for end-user confidence and satisfaction.

- Builder partnerships and supplier relationships in new construction projects further reinforce the importance of offline distribution.

- Thus, the value-added services and supply chain control provided in offline retail contribute significantly to the variable speed heat pump water heater market demand.

The online retail segment is projected to grow at the fastest CAGR during the forecast period.

- Online platforms offer a wide selection of product models, technical specifications, and price comparisons, empowering educated buyers.

- The DIY and prosumer segments are expanding, with users purchasing equipment for guided or self-installation supported by virtual assistance.

- E-commerce is particularly effective in reaching customers in remote locations or underserved regions without a strong distributor network.

- Hence, rising digital adoption across construction sectors supports rapid online retail penetration and, in turn, drives variable speed heat pump water heater market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

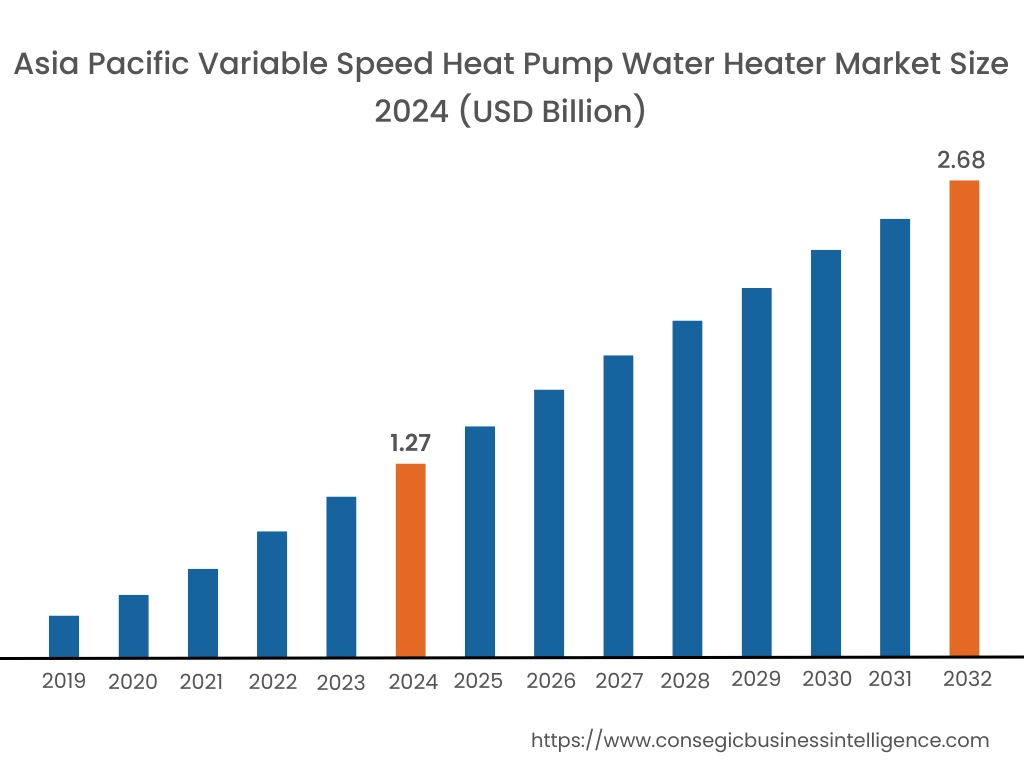

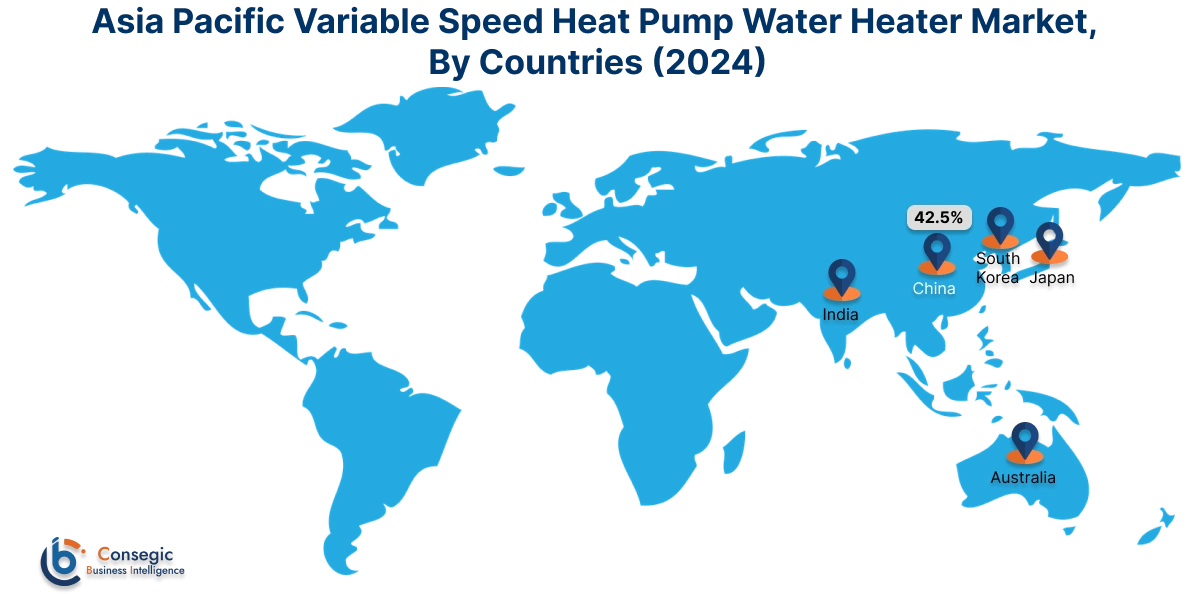

The Asia Pacific region was valued at USD 1.27 Billion in 2024. Moreover, it is projected to grow by USD 1.37 Billion in 2025 and reach over USD 2.68 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.5%. Asia-Pacific is experiencing robust momentum in the variable speed heat pump water heater industry, driven by rapid urbanization, growing energy cost sensitivity, and government-supported clean energy policies. China, Japan, South Korea, and Australia are leading regional adoption. Market research indicates increased installation of variable speed units in multifamily buildings and mid-sized commercial buildings as a result of their flexibility to changing climatic conditions. Compact, low-noise units in high-density areas drive the variable speed heat pump water heater market demand in Japan and South Korea. At the same time, national electrification masterplans and green building codes are fueling interest in energy-efficient water heating solutions for new buildings and retrofitting schemes.

North America is estimated to reach over USD 2.34 Billion by 2032 from a value of USD 1.12 Billion in 2024 and is projected to grow by USD 1.21 Billion in 2025. North America is the early adopter leader because of high regulatory support, decarbonization goals, and increasing consumer consciousness of energy-efficient technologies. Installations are led by the United States and Canada in both light commercial and residential markets, particularly in areas concentrated on the electrification of domestic heating systems. Market research identifies increased need for ENERGY STAR-certified models and systems that can accept time-of-use electricity rate plans. Integration with smart home systems and qualification for federal or state-level incentives also increases adoption. Moreover, the region's aging water heater stock ensures steady replacement demand for high-efficiency replacements.

Europe is a regulation-heavy market, where strict emissions standards and building performance regulations continue to drive consumer and institutional decisions. Nations like Germany, France, the Netherlands, and the Nordic countries are focusing on making the shift from gas-based systems to electrically driven heat pumps. Market trends indicate that variable speed technology is gaining popularity due to its accuracy in temperature control and low sound during operation, especially in urban apartments and energy-efficient homes. The increase in passive house building and EU Green Deal subsidy schemes also lends further support to the replacement of traditional boilers and traditional electric water heaters with high-tech heat pump solutions.

Latin America has nascent potential, and Brazil, Chile, and Mexico are leading the way towards greater energy efficiency in water heating systems. Market analysis suggests that while conventional electric heaters prevail at present, increasing electricity tariffs and the desire for integration of renewables are driving a steady move towards heat pump-based solutions. Education of consumers, training of installers, and financing availability are key to large-scale adoption. The variable speed heat pump water heater market opportunity here is highly connected to efforts of carbon reduction in residential energy consumption and the modernization of the urban housing stock.

Adoption here is limited in the Middle East and Africa region, but it is expanding in construction activities and sustainability initiatives. In Saudi Arabia, South Africa, and the UAE, high-efficiency water heating systems are being driven by demand from premium residential projects and green building regulations. Market research indicates that the variable speed function is becoming a popular choice with its capacity to work efficiently in varying ambient temperatures, a feature relevant in both desert regions and temperate climates. Product affordability and grid reliability issues persist, but increasing electricity prices and international development initiatives could spur greater requirement for energy-saving technologies.

Top Key Players and Market Share Insights:

The variable speed heat pump water heater market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global variable speed heat pump water heater market. Key players in the variable speed heat pump water heater industry include -

- Advantix S.p.A. (Italy)

- Ariston Holding N.V. (Italy)

- Nihon Itomic Co., Ltd. (Japan)

- Panasonic Corporation (Japan)

- Rinnai Corporation (Japan)

- Daikin Industries, Ltd. (Japan)

- Guangzhou Sprsun New Energy Technology Development Co., Ltd. (China)

- Glen Dimplex Group (Ireland).

- LG Electronics (South Korea)

- Mitsubishi Electric Trane HVAC US LLC (Japan)

Variable Speed Heat Pump Water Heater Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 7.94 Billion |

| CAGR (2025-2032) | 9.6% |

| By Type |

|

| By Installation Type |

|

| By End-Use |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Variable Speed Heat Pump Water Heater Market? +

Variable Speed Heat Pump Water Heater Market size is estimated to reach over USD 7.94 Billion by 2032 from a value of USD 3.82 Billion in 2024 and is projected to grow by USD 4.12 Billion in 2025, growing at a CAGR of 9.6% from 2025 to 2032.

What specific segmentation details are covered in the Variable Speed Heat Pump Water Heater Market report? +

The Variable Speed Heat Pump Water Heater market report includes specific segmentation details for type, installation type, end-use and distribution channel.

What are the end-use of the Variable Speed Heat Pump Water Heater Market? +

The end-use of the Variable Speed Heat Pump Water Heater Market is commercial, residential and industrial.

Who are the major players in the Variable Speed Heat Pump Water Heater Market? +

The key participants in the Variable Speed Heat Pump Water Heater market are Advantix S.p.A. (Italy), Ariston Holding N.V. (Italy), DAIKIN INDUSTRIES, Ltd. (Japan), Guangzhou Sprsun New Energy Technology Development Co., Ltd. (China), Glen Dimplex Group (Ireland)., LG Electronics (South Korea), Mitsubishi Electric Trane HVAC US LLC (Japan), Nihon Itomic Co., Ltd. (Japan), Panasonic Corporation (Japan) and Rinnai Corporation (Japan).