- Summary

- Table Of Content

- Methodology

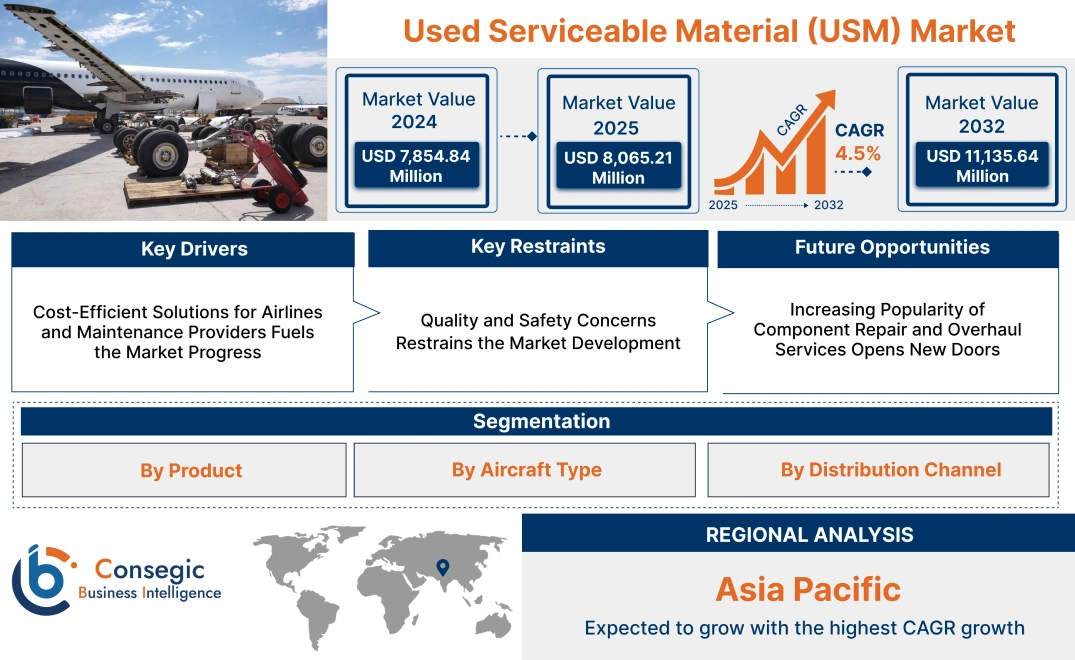

Used Serviceable Material (USM) Market Size:

Used Serviceable Material (USM) Market size is estimated to reach over USD 11,135.64 Million by 2032 from a value of USD 7,854.84 Million in 2024 and is projected to grow by USD 8,065.21 Million in 2025, growing at a CAGR of 4.5% from 2025 to 2032.

Used Serviceable Material (USM) Market Scope & Overview:

Used Serviceable Material (USM) refers to pre-owned aircraft components that have been inspected, tested, and certified as fit for reuse in aviation maintenance and repair activities. These materials include a wide range of parts, such as engines, landing gear, avionics, and structural components, sourced from retired or dismantled aircraft. USM offers a cost-effective solution for maintaining and repairing aircraft fleets while ensuring compliance with aviation safety standards.

USM is extensively used in the maintenance, repair, and overhaul (MRO) sector, where it provides an economical alternative to new parts without compromising reliability or performance. These materials undergo rigorous inspection and certification processes to ensure airworthiness, meeting the stringent requirements of the aviation industry. USM solutions are compatible with various aircraft models, making them versatile for both commercial and military aviation applications.

End-users include airlines, MRO providers, and aircraft leasing companies seeking efficient and affordable maintenance solutions to support fleet operations. Used Serviceable Material plays a critical role in optimizing maintenance costs while maintaining operational reliability across the aviation sector.

Used Serviceable Material (USM) Market Dynamics - (DRO) :

Key Drivers:

Cost-Efficient Solutions for Airlines and Maintenance Providers Fuels the Market Progress

The significant cost savings offered by Used Serviceable Material (USM) is the primary driver for its adoption in the aviation industry. Airlines, MRO providers, and OEMs increasingly opt for USM as it provides a more affordable alternative to purchasing new components. USM, including critical parts like engines, landing gear, and avionics, allows companies to significantly reduce their operational expenses while maintaining the performance and safety standards required for aircraft operations. By using serviceable parts from decommissioned or retired aircraft, airlines can extend the lifespan of their fleets without incurring the high costs associated with brand-new components. This is particularly beneficial for smaller airlines, low-cost carriers, and MRO providers who need to manage tight budgets while maintaining fleet efficiency. The ability to source high-quality, certified USM reduces overall maintenance costs, enabling businesses to reinvest savings into other operational areas, enhancing the profitability of aviation operations. Thus, the aforementioned factors are driving the used serviceable material market growth.

Key Restraints:

Quality and Safety Concerns Restrains the Market Development

One of the key restraints in the Used Serviceable Material (USM) market is the concern regarding the quality and safety of used parts. Since USM involves reusing components from decommissioned aircraft, ensuring that these parts meet rigorous safety standards and regulatory requirements is crucial. Parts must undergo thorough inspection, testing, and certification processes to guarantee they are serviceable and safe for use. Improperly certified or substandard parts can jeopardize the safety and performance of aircraft, leading to potential failures or accidents. Additionally, the lack of uniformity in the condition of used parts, along with the risk of hidden defects, can raise safety concerns. Regulatory bodies, such as the FAA and EASA, impose stringent guidelines to ensure compliance, but ensuring consistency and reliability in every component remains a challenge. This restraint limits the used serviceable material market demand, especially in high-stakes operations like military or commercial aviation.

Future Opportunities :

Increasing Popularity of Component Repair and Overhaul Services Opens New Doors

The growth in requirement for component repair and overhaul services is a key factor driving the USM market. MRO providers and airlines are increasingly opting to repair and refurbish existing parts rather than purchasing new components, as this approach offers significant cost savings. By using USM, airlines can extend the life of their aircraft while avoiding the high costs of new parts. This trend is particularly pronounced in light of the rising operational costs and the need to optimize maintenance budgets. As a result, MRO providers are turning to USM suppliers to source serviceable parts for repairs and refurbishments, further driving the market. Additionally, the focus on sustainability in aviation is pushing operators to reuse parts, reducing waste and promoting a circular economy within the aerospace sector. This growing preference for component repair and overhaul services creates new used serviceable material market opportunities for USM suppliers to expand their role in the aviation maintenance ecosystem.

Used Serviceable Material (USM) Market Segmental Analysis :

By Product:

Based on product, the market is segmented into engine, airframe, landing gear, avionics, and others.

The engine segment accounted for the largest revenue of the total used serviceable material market share in 2024.

- The increasing need for cost-efficient engine replacements and repairs in both commercial and military aircraft drives the dominance of this segment.

- High operational efficiency and extended lifecycle offered by refurbished engine components contribute to their widespread adoption.

- As per market trends, need for certified and inspected used engine parts continues to rise, ensuring compliance with aviation safety standards.

- The growing adoption of USM for engines reflects its role in reducing maintenance costs while maintaining aircraft performance, further contributing to the used serviceable material market expansion.

The avionics segment is expected to register the fastest CAGR during the forecast period.

- Enhanced technological advancements and frequent upgrades in avionics systems are propelling the segment’s extension.

- The increasing need for reliable navigation, communication, and control systems supports the adoption of refurbished avionics.

- The segment’s growth is further bolstered by the availability of certified avionics components at competitive prices.

- As per the used serviceable material market analysis, rising demand from both commercial and military aviation sectors for high-performing avionics systems fosters its rapid growth.

By Aircraft Type:

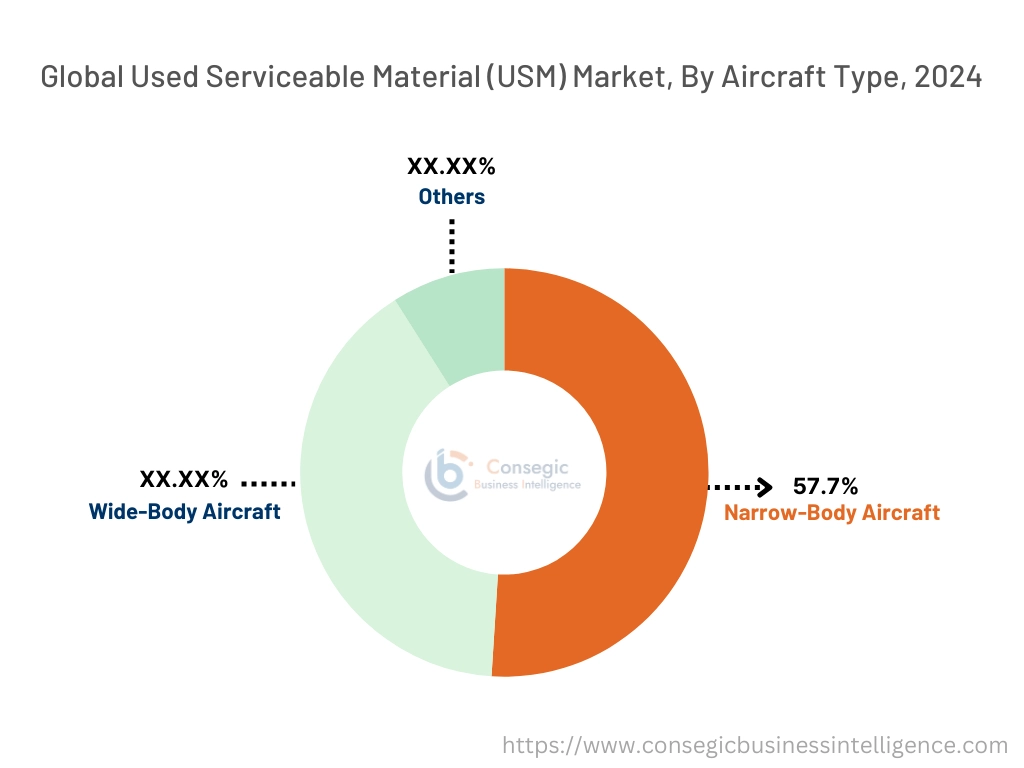

Based on aircraft type, the market is segmented into narrow-body aircraft, wide-body aircraft, and others.

The narrow-body aircraft segment accounted for the largest revenue of 57.7% of the total used serviceable material market share in 2024.

- The dominance is attributed to the high volume of narrow-body aircraft in global fleets, particularly in commercial aviation.

- Cost-saving initiatives by airlines operating narrow-body aircraft further encourage the adoption of USM.

- The frequent demand for engine and airframe replacements in this aircraft category drives the segment’s prominence.

- As per the used serviceable material market trends, narrow-body aircraft offer a significant scope for used material integration, reducing operational expenses.

The wide-body aircraft segment is anticipated to grow at the fastest CAGR during the forecast period.

- Increasing maintenance and repair requirements for long-haul wide-body aircraft support the rapid growth of this segment.

- Rising international and cargo operations utilizing wide-body fleets contribute to higher adoption of USM.

- Enhanced availability of certified wide-body components ensures safe and efficient integration in this aircraft category.

- As global trade and passenger traffic grow, airlines increasingly seek cost-effective maintenance solutions for wide-body fleets, further fueling the used serviceable material market growth.

By Distribution Channel:

Based on the distribution channel, the market is segmented into OEM and aftermarket.

The aftermarket segment accounted for the largest revenue share in 2024.

- The aftermarket offers a broad range of refurbished and inspected components, ensuring widespread accessibility for operators.

- Cost savings achieved through aftermarket channels make them highly attractive to airlines and maintenance organizations.

- Increasing partnerships between USM providers and aftermarket distributors ensure a steady supply of high-quality materials.

- Thus, the segment’s dominance is driven by its ability to cater to diverse aircraft models and component requirements, boosting the used serviceable material market demand.

The OEM segment is expected to grow at the fastest CAGR during the forecast period.

- OEMs are expanding their service offerings to include certified used components, ensuring compliance and reliability.

- Airlines and MROs increasingly prefer OEM-certified materials to ensure compatibility and safety.

- Rising collaborations between OEMs and USM providers enhance the availability of high-quality refurbished parts.

- As per the used serviceable material market trends, the segment’s growth reflects the growing trust in OEM-backed solutions for critical aircraft maintenance needs.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

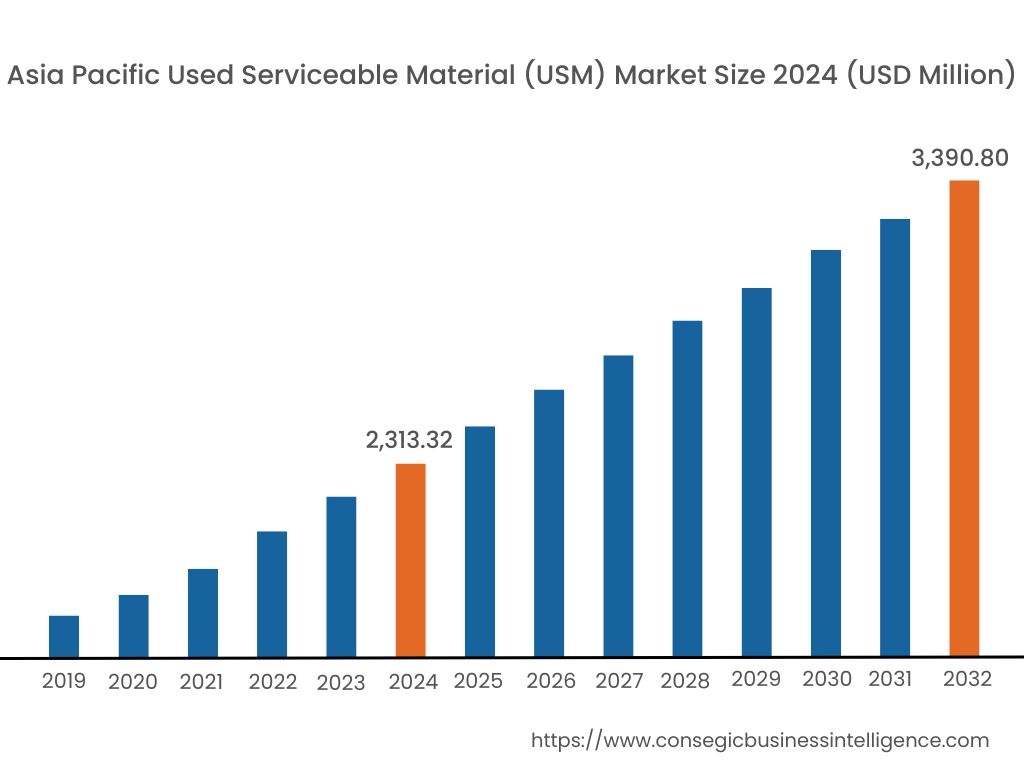

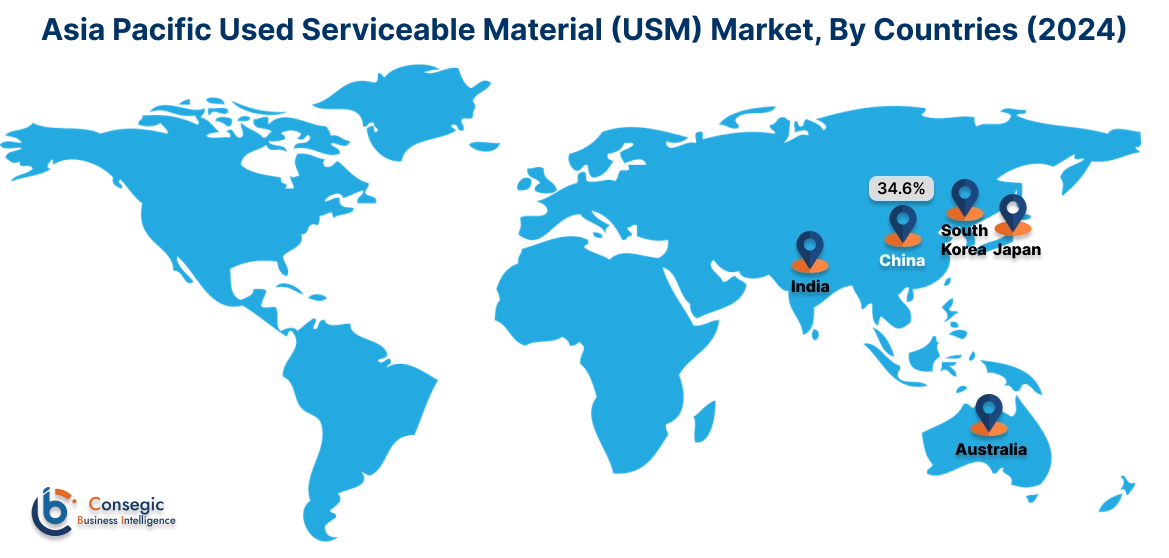

Asia Pacific region was valued at USD 2,313.32 Million in 2024. Moreover, it is projected to grow by USD 2,381.99 Million in 2025 and reach over USD 3,390.80 Million by 2032. Out of this, China accounted for the maximum revenue share of 34.6%. The Asia-Pacific region is witnessing increased demand for cost-effective aircraft maintenance solutions, especially in countries like China and India. A prominent trend is the rapid extension of the commercial aviation sector, leading to a growing need for USM to support fleet maintenance. Analysis indicates that the enlargement of commercial aircraft fleets and the presence of emerging economies with increasing air travel demand are key factors influencing the used serviceable material market expansion in this area.

North America is estimated to reach over USD 3,609.06 Million by 2032 from a value of USD 2,605.52 Million in 2024 and is projected to grow by USD 2,670.18 Million in 2025. This region holds a significant share of the USM market, primarily due to its well-established aviation sector and a substantial number of retired aircraft. A notable trend is the increasing adoption of USM to reduce maintenance costs and enhance operational efficiency. Analysis indicates that the U.S. government's investments in USM infrastructure for both commercial and defense applications are driving used serviceable material market opportunities.

European countries, including Germany, France, and the UK, are key players in the USM market, with a strong focus on sustainable aviation practices and aircraft maintenance services. A significant trend is the collaboration among airlines and MRO providers to incorporate USM into maintenance strategies, aiming to reduce operational costs and promote sustainability. Analysis suggests that the rise in commercial aircraft production and the increase in aftermarket MRO providers are contributing to market dynamics in this region.

In the Middle East, countries are focusing on aircraft fleet expansion and maintenance, driving the demand for USM solutions. The emphasis is on enhancing operational efficiency and reducing maintenance costs through the adoption of USM. In Africa, the market is gradually evolving, with efforts to build local MRO capabilities to support the aviation sector. The used serviceable material market analysis suggests that investments in aviation infrastructure and the development of regional MRO services are crucial for market progression in these regions.

Latin American airlines are increasingly recognizing the benefits of USM in maintaining their fleets cost-effectively. A notable trend is the incorporation of USM into maintenance programs to extend the service life of existing aircraft. However, economic constraints and limited technological infrastructure may impact the pace of adoption. Analysis indicates that collaborations with international MRO providers and investments in aviation infrastructure could play a pivotal role in advancing the USM market in this region.

Top Key Players and Market Share Insights:

The Used Serviceable Material (USM) market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Used Serviceable Material (USM) market. Key players in the Used Serviceable Material (USM) industry include -

- AAR Corp. (USA)

- GA Telesis, LLC (USA)

- AFI KLM E&M (France)

- STS Aviation Group (USA)

- SR Technics (Switzerland)

- AJW Group (UK)

- Liebherr-Aerospace (Germany)

- Delta TechOps (USA)

- AerSale, Inc. (USA)

Used Serviceable Material (USM) Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 11,135.64 Million |

| CAGR (2025-2032) | 4.5% |

| By Product |

|

| By Aircraft Type |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Used Serviceable Material (USM) Market? +

Used Serviceable Material (USM) Market size is estimated to reach over USD 11,135.64 Million by 2032 from a value of USD 7,854.84 Million in 2024 and is projected to grow by USD 8,065.21 Million in 2025, growing at a CAGR of 4.5% from 2025 to 2032.

What are the key segments in the Used Serviceable Material (USM) Market? +

The market is segmented by product (engine, airframe, landing gear, avionics, and others), aircraft type (narrow-body aircraft, wide-body aircraft, and others), and distribution channel (OEM and aftermarket).

Which segment is expected to grow the fastest in the Used Serviceable Material (USM) Market? +

The avionics segment is expected to register the fastest CAGR during the forecast period, driven by technological advancements and the increasing need for reliable and affordable avionics systems.

Who are the major players in the Used Serviceable Material (USM) Market? +

Key players in the Used Serviceable Material (USM) market include AAR Corp. (USA), GA Telesis, LLC (USA), AJW Group (UK), Liebherr-Aerospace (Germany), Delta TechOps (USA), AerSale, Inc. (USA), AFI KLM E&M (France), STS Aviation Group (USA), and SR Technics (Switzerland).