- Summary

- Table Of Content

- Methodology

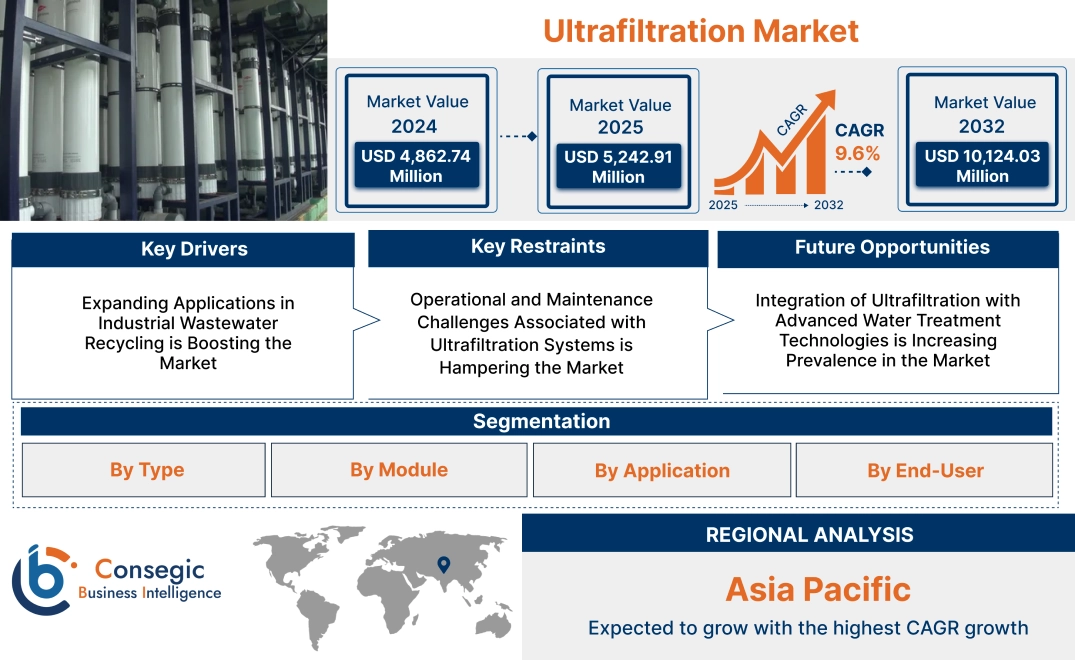

Ultrafiltration Market Size:

Ultrafiltration Market size is estimated to reach over USD 10,124.03 Million by 2032 from a value of USD 4,862.74 Million in 2024 and is projected to grow by USD 5,242.91 Million in 2025, growing at a CAGR of 9.6% from 2025 to 2032.

Ultrafiltration Market Scope & Overview:

Ultrafiltration is an advanced filtration technique that utilizes semi-permeable membranes to separate particles, bacteria, and macromolecules from liquids. These systems are widely used in water purification, wastewater treatment, and industrial processes for their ability to achieve high filtration precision and efficiency. Key characteristics of the process include low energy consumption, high removal efficiency, and the ability to operate under low pressure. The benefits include superior water quality, reduced environmental impact, and extended service life of downstream equipment. Applications span municipal water treatment, pharmaceutical manufacturing, food and beverage processing, and chemical processing. End-users include municipalities, industrial facilities, and commercial operations, driven by increasing ultrafiltration market demand for clean water, stringent environmental regulations, and advancements in membrane filtration technologies.

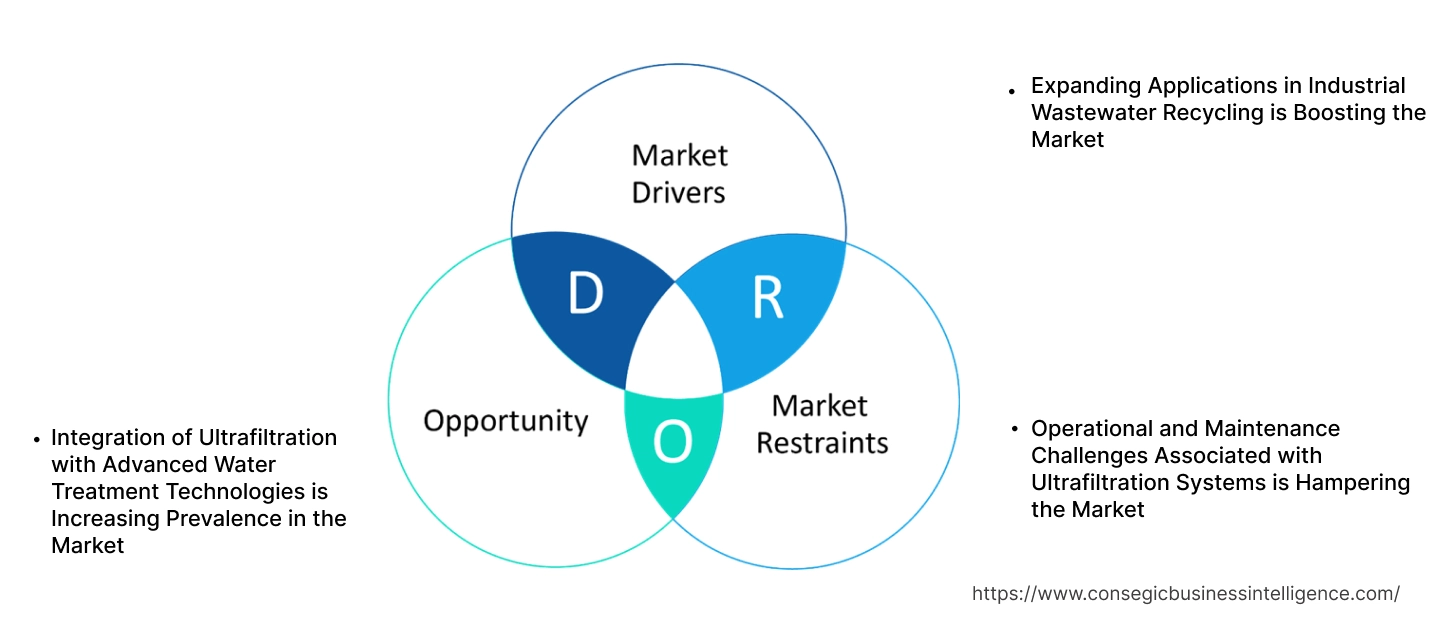

Ultrafiltration Market Dynamics - (DRO) :

Key Drivers:

Expanding Applications in Industrial Wastewater Recycling is Boosting the Market

The growing emphasis on sustainable industrial practices is driving the adoption of these systems in wastewater recycling applications. Industries such as textiles, chemicals, and food processing produce significant volumes of wastewater that require advanced treatment to meet environmental compliance standards. The systems efficiently remove suspended solids, bacteria, and other impurities, enabling the recovery of reusable water from industrial effluents. This not only reduces freshwater consumption but also helps industries lower operational costs and minimize environmental impact.

Moreover, the integration of these systems with other treatment processes, such as reverse osmosis or advanced oxidation, enhances their effectiveness in recycling challenging wastewater streams. With stricter regulations on industrial wastewater discharge and increasing water scarcity concerns, it is becoming a vital component of circular economy practices. Industries focusing on resource efficiency and sustainable operations are leveraging this technology to align with these trends, creating significant opportunities for the market.

Key Restraints:

Operational and Maintenance Challenges Associated with Ultrafiltration Systems is Hampering the Market

While the systems offer high efficiency in water and wastewater treatment, their operational reliability is often hampered by maintenance challenges. A key issue is membrane fouling, caused by the accumulation of particulates, biofilms, and scaling on the membrane surface, which reduces system performance and increases energy requirements. Regular cleaning protocols, including backwashing and chemical cleaning, are essential but add to the operational complexity and costs.

Additionally, membrane replacement is a recurring expense, particularly in applications involving high concentrations of pollutants. Skilled personnel are required to monitor system performance, address technical issues, and implement effective maintenance schedules, which can be challenging for industries with limited access to trained professionals. Furthermore, improper or delayed maintenance can lead to system downtime, shortened lifespan of components, and compromised water quality. These challenges emphasize the need for innovative maintenance solutions and advanced fouling-resistant membranes to improve the long-term efficiency of these systems.

Future Opportunities :

Integration of Ultrafiltration with Advanced Water Treatment Technologies is Increasing Prevalence in the Market

The integration of these systems with advanced water treatment technologies is creating new possibilities for addressing complex water purification and wastewater treatment needs. Combining it with processes such as reverse osmosis, UV disinfection, and advanced oxidation enhances the overall treatment efficiency and expands the range of treatable water sources. For instance, it serves as a pre-treatment step, removing suspended solids and microorganisms, which protects downstream equipment and improves the performance of reverse osmosis systems.

These hybrid solutions are particularly valuable in high-purity applications such as pharmaceuticals, microelectronics, and power generation, where stringent water quality standards must be met. Additionally, integrated systems reduce operational costs by optimizing energy usage and minimizing maintenance requirements. The ultrafiltration market trends toward modular and scalable systems further supports the adoption of ultrafiltration-based hybrid technologies, positioning them as a key solution for industries requiring advanced water treatment capabilities. As opportunities for sustainable and efficient water treatment continues to grow, the integration of ultrafiltration with other technologies is expected to redefine the market landscape.

Ultrafiltration Market Segmental Analysis :

By Type:

Based on type, the ultrafiltration market is segmented into polymeric and ceramic.

The polymeric segment accounted for the largest revenue in ultrafiltration market share in 2024.

- Polymeric ultrafiltration membranes are widely used due to their affordability, high flexibility, and efficiency in various water treatment applications.

- Their extensive adoption in municipal and industrial water treatment plants is supported by the rising applications of using cost-effective solutions for water purification.

- Additionally, advancements in polymeric membrane technology have enhanced their durability and resistance to fouling, further driving demand.

- Polymeric membranes dominate the market due to their versatility, cost-effectiveness, and increased adoption in water treatment applications.

The ceramic segment is anticipated to register the fastest CAGR during the forecast period.

- Ceramic ultrafiltration membranes are preferred in applications requiring high thermal and chemical resistance, such as industrial wastewater treatment and food processing.

- The growing trends of adopting durable and long-lasting filtration solutions in harsh operating environments is driving the need for ceramic membranes.

- Additionally, increasing ultrafiltration market opportunities in pharmaceutical processing, where stringent purification standards are required, supports this segment’s rapid growth.

- According to the market analysis, ceramic membranes are expected to grow rapidly, driven by their durability and increasing demand in industrial and pharmaceutical applications.

By Module:

Based on module, the market is segmented into hollow fiber, plate and frame, and tubular.

The hollow fiber segment accounted for the largest revenue share in 2024.

- Hollow fiber modules are extensively used in municipal and industrial water treatment due to their high surface area and efficiency in filtering large volumes of water.

- The growth of adopting compact and energy-efficient filtration solutions has further propelled the use of hollow fiber modules across various applications.

- Their lightweight design and ease of scalability make them a preferred choice in large-scale operations.

- According to the segmental analysis, hollow fiber leads the market due to their high filtration efficiency and adaptability to large-scale water treatment applications.

The tubular segment is anticipated to register the fastest CAGR during the forecast period.

- Tubular modules are gaining popularity in applications involving high-viscosity liquids, such as industrial wastewater and food & beverage processing.

- The trends of using robust and easy-to-clean filtration modules in industries handling challenging fluids has boosted the adoption of tubular systems.

- Additionally, their ability to handle high solid content supports their growing requirement.

- Tubular modules are expected to grow rapidly, driven by their capability to process high-viscosity fluids and increasing use in industrial wastewater treatment.

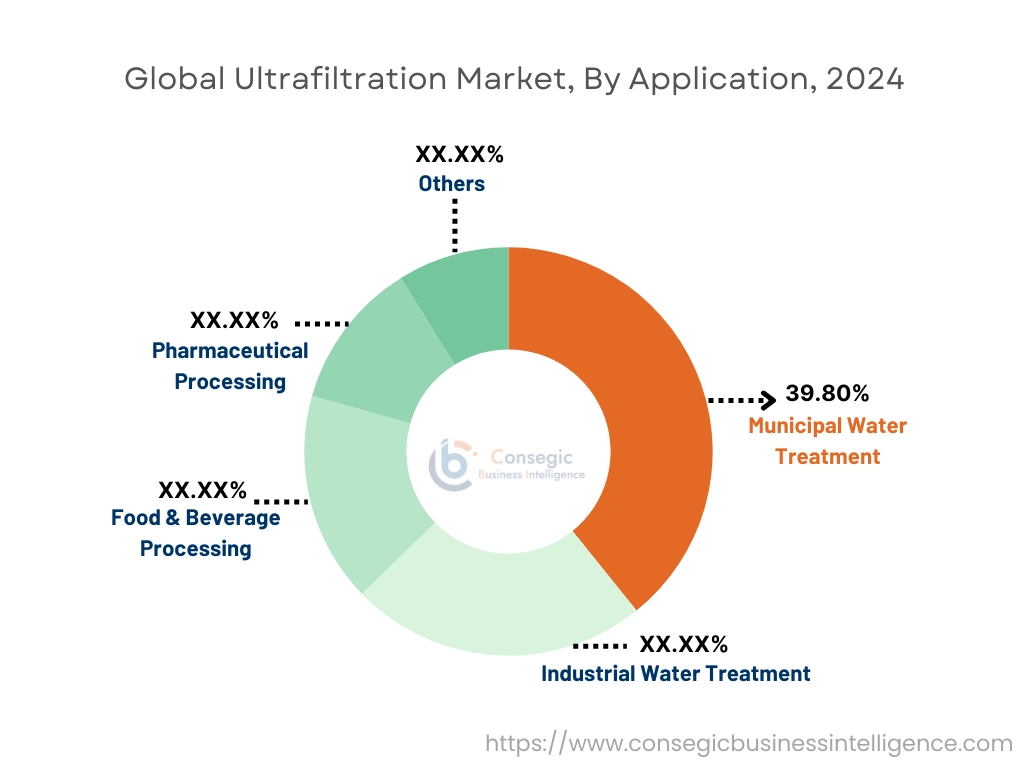

By Application:

Based on application, the market is segmented into municipal water treatment, industrial water treatment, food & beverage processing, pharmaceutical processing, and others.

The municipal water treatment segment accounted for the largest revenue share of 39.80% in 2024.

- Ultrafiltration systems are extensively used in municipal water treatment for removing pathogens, suspended solids, and other impurities.

- The trends of adopting advanced filtration technologies to ensure safe and clean drinking water has driven the need in this segment.

- Additionally, government initiatives to upgrade water treatment infrastructure in urban and rural areas further support the segment’s dominance.

- Municipal water treatment dominates the market due to increasing investments in clean water infrastructure and the rising demand for advanced filtration technologies.

The pharmaceutical processing segment is anticipated to register the fastest CAGR during the forecast period.

- Ultrafiltration is critical in pharmaceutical processing for achieving high purity levels in drug formulations and biological products.

- The growing ultrafiltration market trends of adopting stringent purification standards to meet regulatory requirements has driven need in this segment.

- Additionally, the rising focus on biopharmaceutical production and the need for contamination-free processing support rapid ultrafiltration market growth in pharmaceutical applications.

- Pharmaceutical processing is expected to grow rapidly, driven by stringent purity requirements and increasing adoption of it in biopharmaceutical production.

By End-User:

Based on end-user, the market is segmented into industrial, municipal, and commercial.

The municipal segment accounted for the largest revenue in ultrafiltration market share in 2024.

- Municipalities rely heavily on these systems to provide clean and safe drinking water to growing urban populations.

- The growth of modernizing municipal water treatment plants with energy-efficient and low-maintenance technologies has boosted ultrafiltration market demand in this segment.

- Additionally, increasing concerns about water scarcity and contamination are driving municipalities to adopt advanced ultrafiltration solutions.

- Municipal end-users lead the market, driven by the increasing need for clean water and modernization of water treatment infrastructure.

The industrial segment is anticipated to register the fastest CAGR during the forecast period.

- Industries such as food & beverage, pharmaceuticals, and chemicals are increasingly adopting it for wastewater treatment and process water recycling.

- The trends of embracing sustainable practices to reduce environmental impact has driven surge in this segment.

- Additionally, strict environmental regulations mandating efficient wastewater treatment support the growth of industrial systems.

- The industrial segment is expected to grow rapidly, supported by rising environmental concerns and the trends toward sustainable water management practices.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

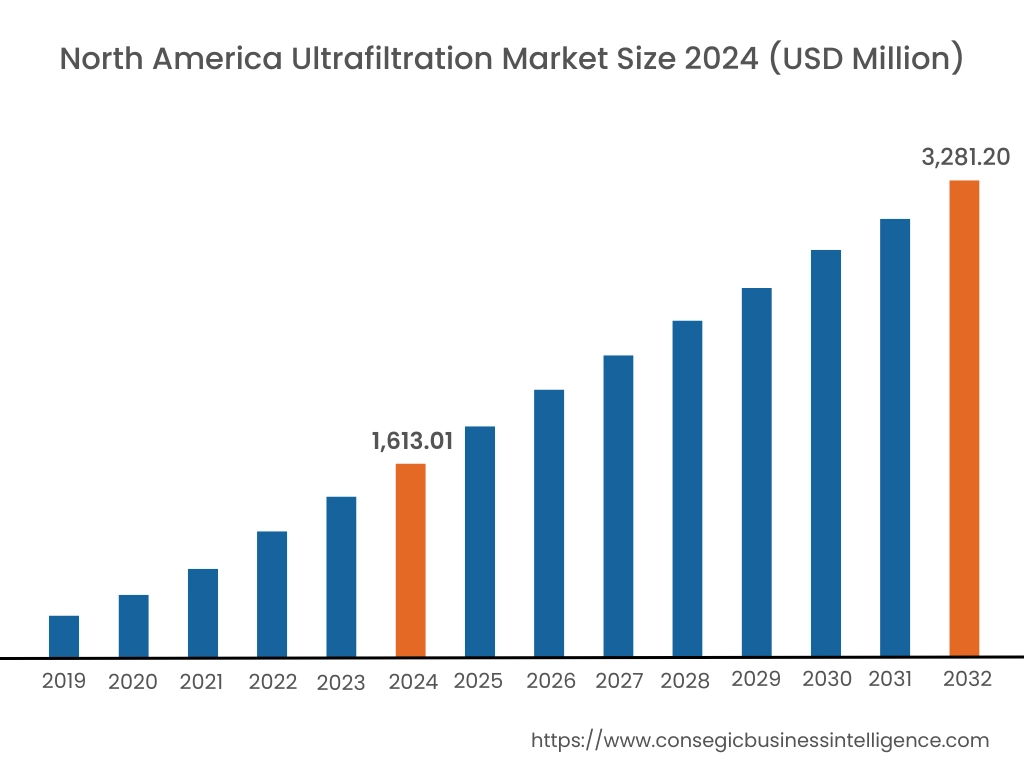

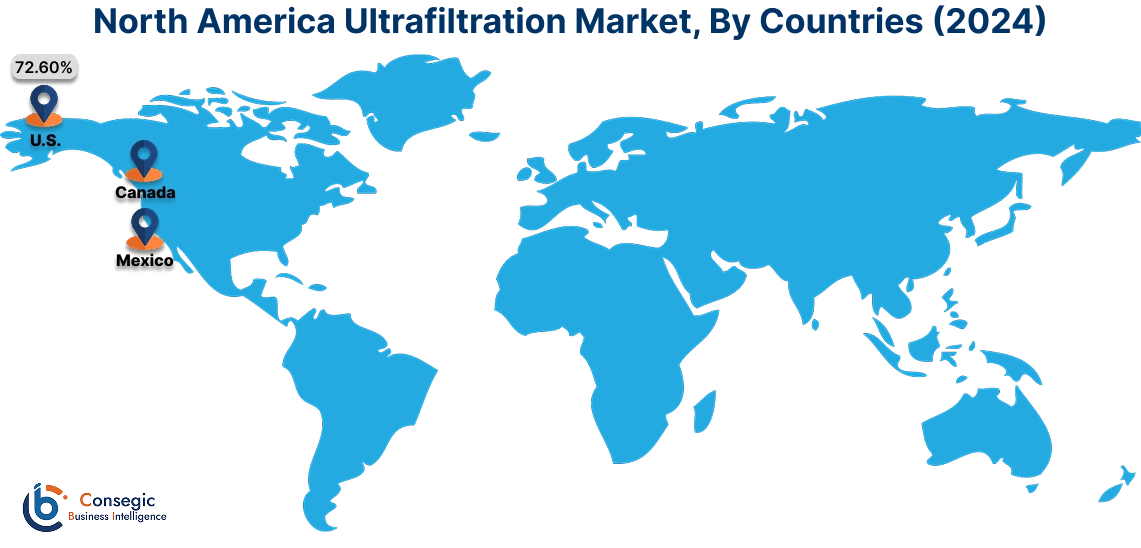

In 2024, North America was valued at USD 1,613.01 Million and is expected to reach USD 3,281.20 Million in 2032. In North America, the U.S. accounted for the highest share of 72.60% during the base year of 2024. North America holds a significant stake in the ultrafiltration market analysis, driven by rising awareness of water quality and stringent government regulations on wastewater treatment. The U.S. leads the region due to extensive use of these systems in industrial processes, municipal water treatment, and the food and beverage sector. The increasing focus on sustainable water management and advancements in membrane technology further enhance the adoption of these systems. Canada contributes through its emphasis on clean water initiatives and the deployment of advanced filtration systems in industrial applications. However, the high installation and operational costs can pose challenges for ultrafiltration market expansion in some sectors.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 10.1% over the forecast period. Asia-Pacific is the fastest-growing region in the ultrafiltration market analysis, driven by rapid industrialization, urbanization, and increasing water scarcity in China, India, and Southeast Asia. China leads the region with significant investments in water treatment infrastructure and the adoption of these systems for industrial and municipal applications. India’s growing population and emphasis on improving access to clean drinking water are driving the implementation of them in municipal and residential sectors. In Southeast Asia, countries like Indonesia and Vietnam are adopting it to address water quality challenges in agricultural and industrial activities. However, lack of awareness about advanced filtration technologies and limited infrastructure in rural areas can hinder ultrafiltration market growth in some parts of the region.

Europe is a prominent market for the systems, supported by stringent environmental regulations and growing adoption of advanced filtration technologies. Countries like Germany, France, and the UK are key contributors, with high utilization of ultrafiltration in wastewater treatment, food processing, and pharmaceutical applications. Germany’s focus on industrial sustainability and wastewater reuse drives the adoption of ultrafiltration systems, while France emphasizes clean water solutions in the municipal sector. The UK is leveraging ultrafiltration in the food and beverage industry to ensure product quality and compliance with safety standards. However, the market faces challenges such as high energy costs and regulatory complexities for new installations.

The Middle East & Africa region is witnessing steady advancements as per the analysis with regards to the ultrafiltration market expansion, primarily driven by increasing investments in desalination plants and wastewater treatment projects. Saudi Arabia and the UAE are leading markets, leveraging ultrafiltration for water reuse and seawater desalination to combat water scarcity. In Africa, South Africa is utilizing ultrafiltration systems to address water contamination issues and improve access to potable water in urban and rural areas. However, challenges such as high capital costs and limited technical expertise can restrict the adoption of ultrafiltration systems in some areas of the region.

Latin America analysis portrays it is an emerging market for ultrafiltration, with Brazil and Mexico being key contributors. Brazil’s focus on improving water quality and wastewater management, particularly in urban areas, drives the adoption of ultrafiltration systems. Mexico is leveraging ultrafiltration in industrial applications, especially in the food and beverage and pharmaceutical sectors. The region is also exploring ultrafiltration solutions for agricultural irrigation and water reuse. However, inconsistent regulations and limited investment in water infrastructure in some countries may slow the market growth.

Top Key Players & Market Share Insights:

The ultrafiltration market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global ultrafiltration market. Key players in the ultrafiltration industry include -

- Pentair plc (United States)

- DuPont Water Solutions (United States)

- Alfa Laval AB (Sweden)

- Toray Industries, Inc. (Japan)

- Asahi Kasei Corporation (Japan)

- 3M Purification (United States)

- Pall Corporation (United States)

- SUEZ Water Technologies & Solutions (France)

- Koch Membrane Systems (United States)

- Hydranautics (United States)

Recent Industry Developments :

Business Expansion:

- In April 2024, QUA inaugurated a new state-of-the-art membrane manufacturing facility in Pune, India, significantly expanding its production capacity by four times. This facility will support the production of a diverse range of membrane products, including FEDI GIGA fractional electrodeionization, EnviQ RF submerged ultrafiltration membranes, and Q-SEP Q-Connect hollow fiber ultrafiltration membranes. The expansion comes in response to the growing international demand for high-performance membrane solutions. The facility also incorporates a zero-discharge system, promoting sustainability by recycling wastewater from its operations. This development underscores QUA's commitment to innovation, efficiency, and environmental sustainability in the ultrafiltration market.

Ultrafiltration Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 10,124.03 Million |

| CAGR (2025-2032) | 9.6% |

| By Type |

|

| By Module |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the expected size of the Ultrafiltration Market by 2032? +

The market is projected to exceed USD 10,124.03 Million by 2032.

What is ultrafiltration, and how does it work? +

Ultrafiltration uses semi-permeable membranes to separate particles, bacteria, and macromolecules from liquids, achieving precise filtration with low energy consumption.

What are the main applications of ultrafiltration systems? +

Key applications include municipal water treatment, industrial wastewater treatment, food and beverage processing, and pharmaceutical manufacturing.

Which industries are the primary end-users of ultrafiltration systems? +

Industries such as municipal water facilities, industrial operations, and commercial enterprises utilize ultrafiltration systems extensively.

What are the main advantages of ultrafiltration technology? +

Ultrafiltration provides superior water quality, reduces environmental impact, and ensures low-pressure operation with high filtration efficiency.