- Summary

- Table Of Content

- Methodology

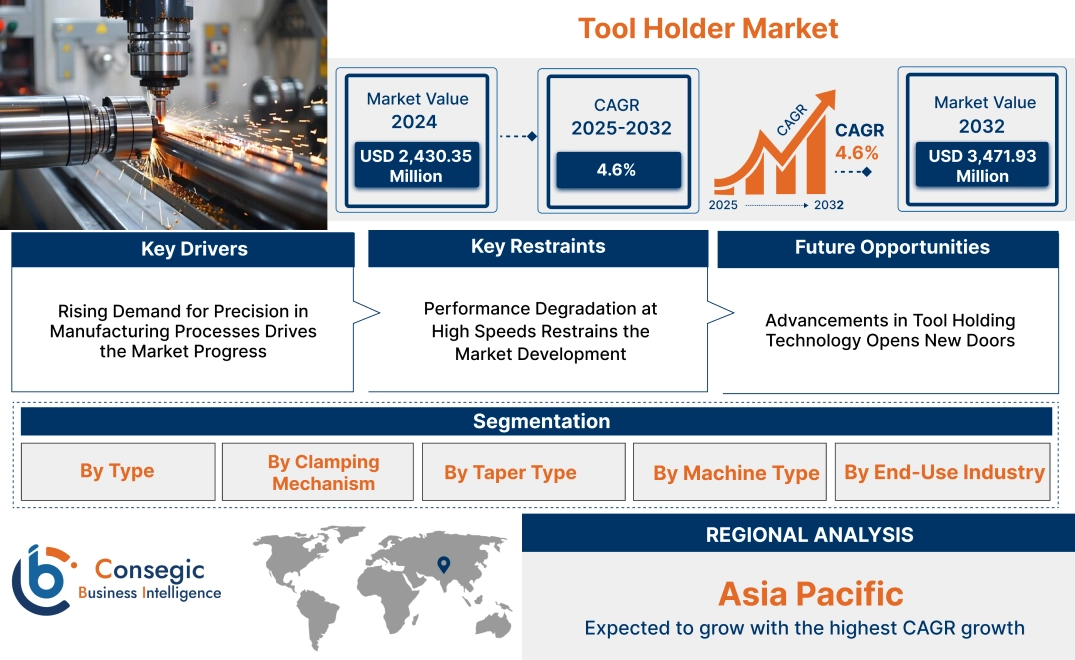

Tool Holder Market Size:

Tool Holder Market size is estimated to reach over USD 3,471.93 Million by 2032 from a value of USD 2,430.35 Million in 2024 and is projected to grow by USD 2,497.87 Million in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

Tool Holder Market Scope & Overview:

A tool holder is a critical component in machining operations, designed to securely hold and position cutting tools during processes such as milling, drilling, and turning. These holders ensure precision, stability, and efficient power transmission between the machine spindle and the cutting tool, making them essential for achieving high-quality machining results. They are used across industries such as automotive, aerospace, manufacturing, and energy for various machining applications.

It is available in various types, including collet chucks, end mill holders, hydraulic tool holders, and shrink-fit holders, catering to specific machining requirements. They are engineered to deliver accuracy and durability, even under high-speed or heavy-duty machining conditions. Advanced holders are designed to minimize vibration, enhance tool life, and improve surface finish, ensuring reliable performance across diverse operations.

End-users of these holders include CNC machine operators, precision engineering companies, and manufacturers requiring robust and adaptable solutions for machining tasks. These components play a vital role in enhancing productivity and maintaining consistency in machining operations.

Tool Holder Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Precision in Manufacturing Processes Drives the Market Progress

The growing emphasis on precision manufacturing across industries like aerospace, automotive, and electronics is significantly boosting the demand for advanced tool holders. Precision machining requires exceptional accuracy, particularly for components with intricate geometries and tight tolerances. Tool holders play a crucial role in ensuring accurate tool alignment, minimizing vibrations, and maintaining dimensional stability during high-speed operations. Industries are increasingly adopting these holders engineered for high-precision applications to enhance productivity and meet stringent quality standards. These advanced solutions are indispensable in achieving consistent performance in demanding machining processes. As manufacturers continue to prioritize efficiency and precision, these holders capable of supporting high-speed machining while ensuring reliability and durability are gaining widespread adoption. This trend is further amplified by the need for superior surface finishes and the machining of complex materials, making precision-focused tool holders a critical component in modern manufacturing workflows. Therefore, the aforementioned factors are driving the tool holder market growth.

Key Restraints:

Performance Degradation at High Speeds Restrains the Market Development

High-speed machining presents unique constraints for tool holders, including increased vibrations and thermal expansion. These factors compromise tool stability, reduce machining accuracy, and lead to uneven wear on cutting tools. Vibrations at high speeds result in surface finish issues and dimensional inaccuracies, particularly in precision-intensive industries like aerospace and automotive manufacturing. Additionally, thermal expansion caused by prolonged high-speed operations distort tool holder geometry, further impacting performance. To counter these issues, manufacturers often turn to advanced materials, such as titanium or specialized alloys, and integrate cooling systems, which significantly increase production costs. However, even with such enhancements, maintaining precision at extreme speeds requires ongoing maintenance and monitoring, adding to operational complexity. These limitations make it difficult for industries focused on high-speed machining to adopt standard tool holding solutions without incurring higher costs or performance trade-offs, hindering the tool holder market demand.

Future Opportunities :

Advancements in Tool Holding Technology Opens New Doors

Advancements in tool holding technology, including shrink-fit holders, hydrostatic clamping, and magnetic tool holders, are revolutionizing machining processes by offering superior performance and efficiency. Shrink-fit holders provide exceptional grip strength and high precision, ensuring minimal runout during high-speed operations. Hydrostatic clamping enhances tool stability by evenly distributing clamping pressure, reducing vibrations and extending tool life. Magnetic tool holders enable rapid tool changes and offer versatility for applications requiring frequent adjustments. These innovations significantly reduce setup times, improve machining accuracy, and minimize tool wear, making them highly attractive to industries with demanding machining requirements, such as aerospace, automotive, and medical device manufacturing. As manufacturing processes evolve to accommodate advanced materials and tighter tolerances, the adoption of these cutting-edge tool holding technologies is creating tool holder market opportunities for increased productivity and cost savings, driving progress in high-performance machining environments.

Tool Holder Market Segmental Analysis :

By Type:

Based on type, the market is segmented into collet chuck, hydraulic tool holder, milling chuck, and others.

The collet chuck segment held the largest revenue of the total tool holder market share in 2023.

- Collet chucks are widely used due to their precision in gripping cylindrical tools, making them indispensable for machining operations.

- They enhance operational accuracy and tool life, driving their adoption in industries requiring high-speed machining processes.

- The versatility of collet chucks across various machining centers contributes to their dominance in the market.

- As per tool holder market analysis, the increasing focus on precision engineering in aerospace and electronics sectors bolsters the prominence of collet chucks.

The hydraulic tool holder segment is expected to register the fastest CAGR during the forecast period.

- Hydraulic tool holders are gaining traction for their ability to dampen vibrations and improve machining performance.

- The segment's growth is attributed to the rising adoption of advanced CNC machining centers in automotive and industrial manufacturing.

- Their ability to provide superior grip force and tool stability makes hydraulic holders a preferred choice for high-precision applications.

- Thus, increasing investments in high-performance manufacturing technologies across emerging markets further accelerate the segment's growth, contributing to the tool holder market expansion.

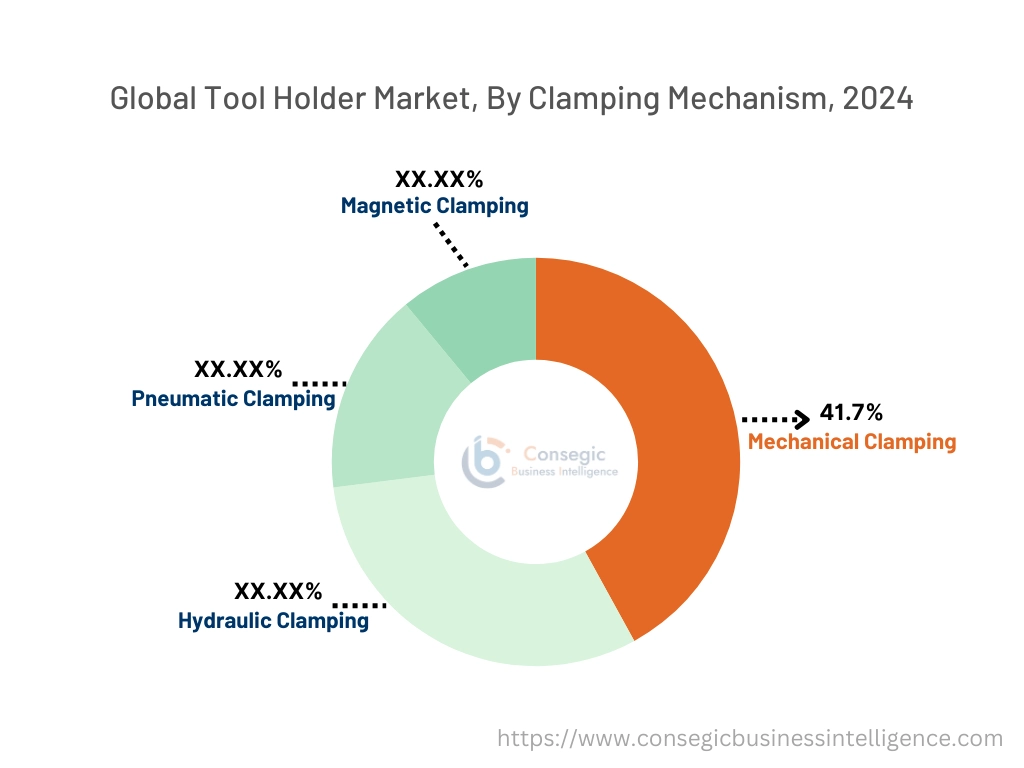

By Clamping Mechanism:

Based on clamping mechanism, the market is segmented into mechanical clamping, hydraulic clamping, pneumatic clamping, and magnetic clamping.

The mechanical clamping segment held the largest revenue of 41.7% of the total tool holder market share in 2023.

- Mechanical clamping systems are cost-effective and provide reliable tool stability, making them a preferred choice in industrial manufacturing.

- The simplicity and durability of mechanical clamping systems contribute to their widespread usage in conventional and CNC machines.

- Their compatibility with a variety of holders ensures their dominance across different machining applications.

- As per tool holder market trends, industries with budget constraints, such as small-scale manufacturing, continue to favor mechanical clamping systems.

The hydraulic clamping segment is projected to grow at the fastest CAGR during the forecast period.

- Hydraulic clamping systems offer precise and uniform clamping pressure, enhancing machining accuracy and reducing tool wear.

- The growing adoption of automation in manufacturing processes drives the need for hydraulic clamping solutions.

- Their application in high-speed machining operations, particularly in aerospace and automotive industries, fuels the segment's growth.

- Thus, advancements in hydraulic systems, such as quick-change capabilities, further enhance their appeal in high-performance applications, fueling the tool holder market growth.

By Taper Type:

Based on taper type, the market is segmented into R8, Morse taper, V-flange taper, and BT flange taper.

The V-flange taper segment accounted for the largest revenue share in 2023.

- V-flange tapers are widely used for their compatibility with high-speed machining and heavy-duty cutting operations.

- Their ability to provide superior tool rigidity and minimal runout makes them a preferred choice in precision engineering applications.

- The dominance of V-flange tapers is supported by their widespread use in CNC machining centers across automotive and aerospace sectors.

- As per analysis, the continuous focus on high-performance machining technologies underpins the growth of this segment, further encouraging the tool holder market demand.

The BT flange taper segment is expected to grow at the fastest CAGR during the forecast period.

- BT flange tapers are gaining popularity due to their symmetrical design, which ensures better balance during high-speed machining.

- Their application in advanced CNC turning centers and machining centers drives their adoption in industrial and automotive sectors.

- The development of this segment is supported by the increasing preference for tool holders that enhance machining efficiency and accuracy.

- As per the tool holder market analysis, innovations in taper technology to improve tool stability further accelerate the adoption of BT flange tapers.

By Machine Type:

Based on machine type, the market is segmented into CNC machining center and CNC turning center.

The CNC machining center segment held the largest revenue share in 2023.

- CNC machining centers are extensively used for their capability to perform multiple operations with high precision and efficiency.

- Their dominance is attributed to their versatility in handling complex machining tasks across various industries.

- The integration of advanced features, such as multi-axis control and real-time monitoring, enhances their adoption in industrial manufacturing.

- As per tool holder market trends, the increasing focus on automation in machining processes continues to support the prominence of CNC machining centers.

The CNC turning center segment is expected to grow at the fastest CAGR during the forecast period.

- CNC turning centers are increasingly adopted for their efficiency in producing cylindrical components with high accuracy.

- Their application in the production of automotive and aerospace components drives the segment's growth.

- The demand for high-speed turning operations and reduced production times further supports the adoption of CNC turning centers.

- Thus, advancements in turning center technologies, such as live tooling capabilities, enhance their appeal across various end-user industries, driving the tool holder market expansion.

By End-Use Industry:

Based on end-use industry, the market is segmented into automotive, aerospace & defense, electronics & semiconductors, industrial manufacturing, and others.

The automotive segment accounted for the largest revenue share in 2023.

- The automotive sector relies heavily on advanced machining tools for the production of precision components, supporting the dominance of this segment.

- Increasing investments in electric vehicle manufacturing further drive the requirement for tool holders in automotive applications.

- The emphasis on enhancing production efficiency and reducing machining costs strengthens the adoption of tool holders in this sector.

- As per analysis, the growing focus on lightweight and high-performance automotive components underpins the segment's growth.

The aerospace & defense segment is projected to grow at the fastest CAGR during the forecast period.

- The aerospace sector requires high-precision machining solutions for the production of critical components, driving the adoption of tool holders.

- The segment's progress is attributed to advancements in machining technologies to meet the stringent requirements of aerospace manufacturing.

- Increasing defense investments and aircraft production in emerging economies further accelerate the segment's enlargement.

- Thus, innovations in tool holder designs to enhance performance in aerospace applications fuel the development of this segment, creating significant tool holder market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

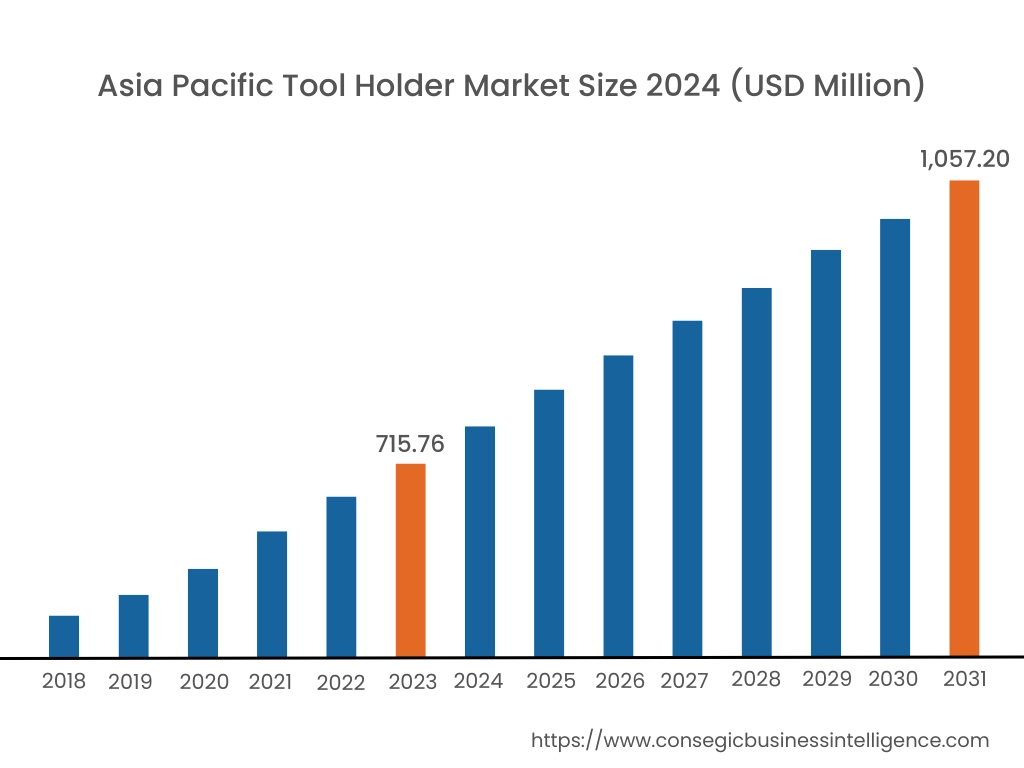

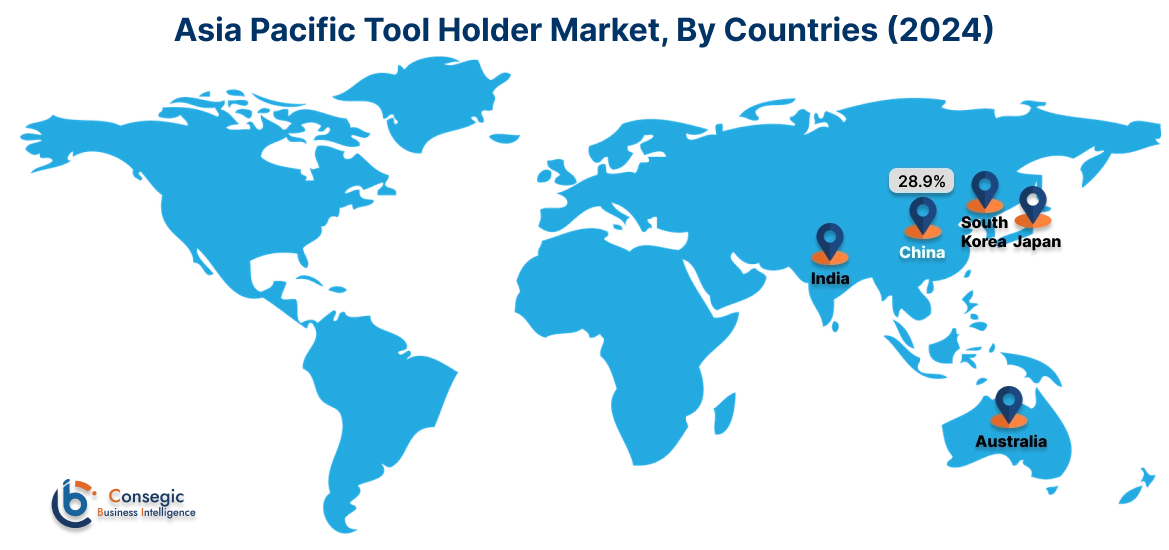

Asia Pacific region was valued at USD 715.76 Million in 2024. Moreover, it is projected to grow by USD 737.72 Million in 2025 and reach over USD 1,057.20 Million by 2032. Out of this, China accounted for the maximum revenue share of 28.9%. The Asia-Pacific region is experiencing rapid development in the tool holder market, driven by industrialization and technological advancements in countries such as China, Japan, and India. The extension of the manufacturing sector and the rising requirement for high-precision machining have intensified the need for advanced tool holding systems. Government initiatives promoting industrial efficiency further influence market trends.

North America is estimated to reach over USD 1,125.25 Million by 2032 from a value of USD 806.17 Million in 2024 and is projected to grow by USD 826.98 Million in 2025. This region holds a significant share of the tool holder market, driven by the expanding manufacturing and automotive industries. The United States, in particular, has seen extensive adoption of advanced tool holding systems across sectors such as aerospace and defense. A notable trend is the increasing need for high-precision machining in manufacturing industries, which is propelling the market.

Europe represents a substantial portion of the global tool holder market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's emphasis on industrial automation and precision engineering has propelled the utilization of advanced tool holding solutions. Analysis indicates a growing trend towards the deployment of intelligent holders equipped with sensors for real-time data analysis, enhancing precision and reducing downtime.

The Middle East & Africa region shows a growing interest in advanced tool holding solutions, particularly in the construction and industrial sectors. Countries like Saudi Arabia and South Africa are investing in modern manufacturing technologies to enhance production efficiency. Analysis suggests an increasing trend towards adopting high-precision holders to meet international quality standards.

Latin America is an emerging market with Brazil and Mexico being key contributors. The region's growing focus on industrial modernization and the automotive sector has spurred the adoption of advanced tool holding solutions. Government policies aimed at enhancing manufacturing capabilities influence market trends.

Top Key Players and Market Share Insights:

The Tool Holder market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Tool Holder market. Key players in the Tool Holder industry include –

- Techniks Inc. (USA)

- Guhring, Inc. (Germany)

- Emuge Corporation (Germany)

- NT Tool (Japan)

- ISCAR Ltd. (Israel)

- SCHUNK (Germany)

- Kennametal Inc. (USA)

- Sandvik Coromant (Sweden)

- Haimer GmbH (Germany)

Recent Industry Developments :

Product Launches:

- In November 2024, MAPAL introduced a new patent-pending bayonet-type connection for milling cutter systems with replaceable heads at AMB 2024. This innovative connection simplifies tool handling by requiring just a 90-degree turn to lock the replaceable head in place, eliminating the need for threaded fastening. The system provides a rigid connection and optimized cooling through a ring of cooling channel bores in the tool holder, improving tool life and machining quality. The system also reduces material usage by 70%, supporting sustainability. It is available in 7 sizes, offering versatility for various applications, including automotive component manufacturing.

Tool Holder Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,471.93 Million |

| CAGR (2025-2032) | 4.6% |

| By Type |

|

| By Clamping Mechanism |

|

| By Taper Type |

|

| By Machine Type |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Tool Holder Market? +

Tool Holder Market size is estimated to reach over USD 3,471.93 Million by 2032 from a value of USD 2,430.35 Million in 2024 and is projected to grow by USD 2,497.87 Million in 2025, growing at a CAGR of 4.6% from 2025 to 2032.

What are the segments and subsegments covered in the Tool Holder Market report? +

The market is segmented into tool holder types (Collet Chuck, Hydraulic Tool Holder, Milling Chuck, Others), clamping mechanisms (Mechanical Clamping, Hydraulic Clamping, Pneumatic Clamping, Magnetic Clamping), taper types (R8, Morse Taper, V-Flange Taper, BT Flange Taper), machine types (CNC Machining Center, CNC Turning Center), and end-use industries (Automotive, Aerospace & Defense, Electronics & Semiconductors, Industrial Manufacturing, Others).

Which segment is expected to grow the fastest in the Tool Holder Market? +

The hydraulic clamping segment is projected to grow at the fastest CAGR during the forecast period, driven by its ability to provide precise and uniform clamping pressure, enhancing machining accuracy and reducing tool wear.

Who are the key players in the Tool Holder Market? +

Key players in the Tool Holder Market include SCHUNK (Germany), Kennametal Inc. (USA), Sandvik Coromant (Sweden), Haimer GmbH (Germany), Techniks Inc. (USA), Guhring, Inc. (Germany), Emuge Corporation (Germany), NT Tool (Japan), and ISCAR Ltd. (Israel).