- Summary

- Table Of Content

- Methodology

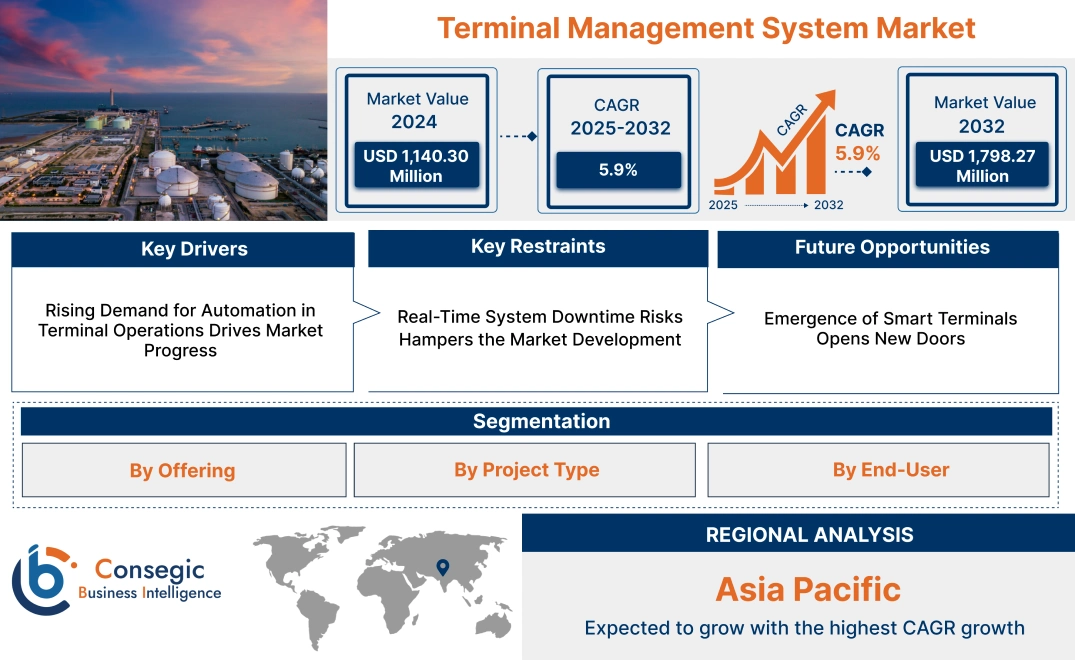

Terminal Management System Market Size:

Terminal Management System Market size is estimated to reach over USD 1,798.27 Million by 2032 from a value of USD 1,140.30 Million in 2024 and is projected to grow by USD 1,186.80 Million in 2025, growing at a CAGR of 5.9% from 2025 to 2032.

Terminal Management System Market Scope & Overview:

A terminal management system refers to a software and hardware-based solution designed to optimize and streamline operations at terminal facilities, such as oil and gas terminals, chemical plants, and transportation hubs. These systems enable effective management of processes like loading, unloading, storage, and distribution, ensuring efficiency and compliance with safety regulations.

Terminal management systems are equipped with features such as real-time monitoring, inventory management, and automated control of equipment, providing enhanced accuracy and operational visibility. These systems integrate seamlessly with enterprise resource planning (ERP) software and other digital platforms, enabling centralized management of terminal operations. They are tailored to meet the specific needs of various industries, ensuring adaptability and scalability.

End-users include terminal operators, logistics companies, and industrial facilities that require efficient and secure management of terminal activities. These systems play a vital role in improving productivity, reducing operational risks, and supporting modern terminal operations.

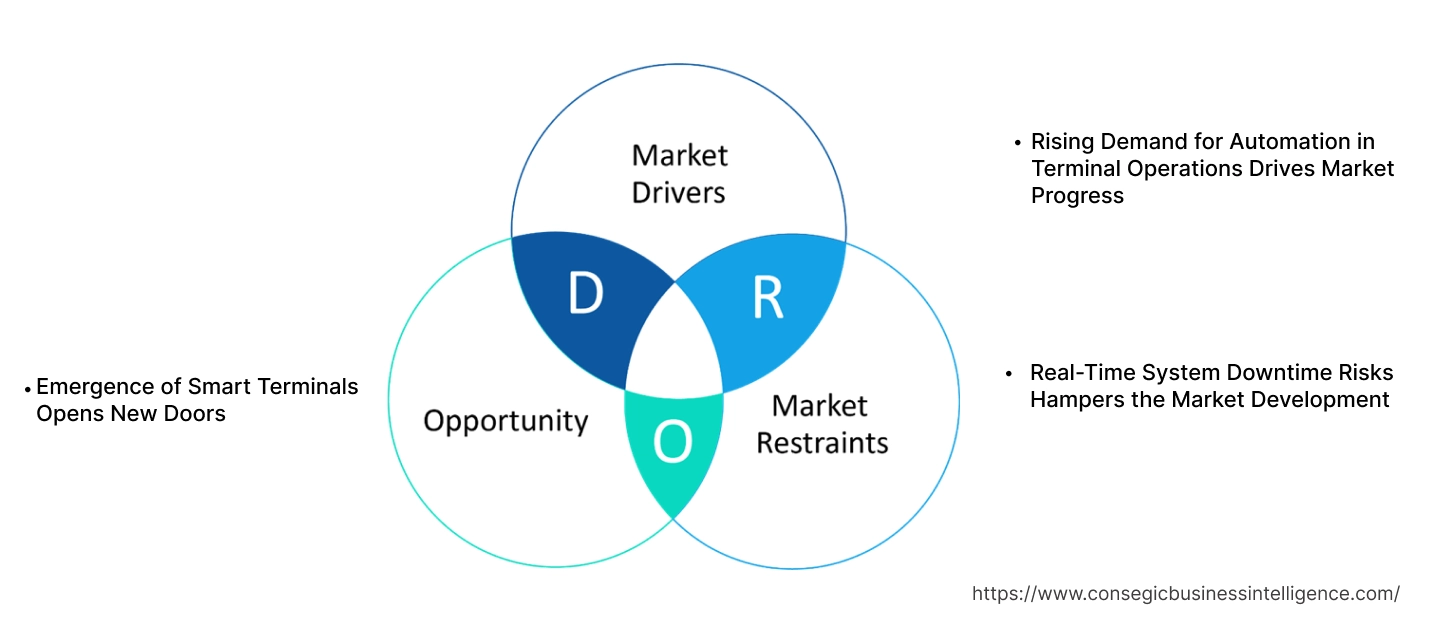

Terminal Management System Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Automation in Terminal Operations Drives Market Progress

Automation is revolutionizing terminal operations by streamlining processes and minimizing the scope for human error. Automated systems are increasingly being adopted for critical tasks such as inventory management, cargo loading, and unloading, enabling terminals to manage larger volumes of goods with greater precision. These solutions enhance operational speed by optimizing workflows and reducing bottlenecks, ensuring that goods are processed efficiently.

Additionally, automation ensures accurate inventory tracking, minimizing discrepancies and improving resource allocation. For industries handling high-value or hazardous materials, automation adds a layer of safety by reducing manual handling and implementing fail-safe procedures. As global trade expands and terminals face higher throughput demands, automated systems are becoming indispensable for maintaining operational efficiency and reducing downtime, positioning automation as a key driver for the terminal management system market growth.

Key Restraints:

Real-Time System Downtime Risks Hampers the Market Development

Terminal management systems depend on continuous real-time data exchange for seamless operations, including inventory tracking, scheduling, and cargo handling. Any disruption, whether caused by network outages, software glitches, or hardware malfunctions, severely impacts operational efficiency. These disruptions lead to delays in loading and unloading processes, resulting in prolonged turnaround times and increased operational costs.

Additionally, critical processes such as inventory updates and billing face inaccuracies, creating further constraints for terminal operators. For high-traffic terminals, even short periods of downtime result in significant financial losses and tarnish reputations with supply chain partners, hindering the terminal management system market demand. As terminal operations become increasingly digitized and interconnected, mitigating downtime risks has become a critical priority for operators to ensure uninterrupted and efficient workflows.

Future Opportunities :

Emergence of Smart Terminals Opens New Doors

The emergence of smart terminals is revolutionizing terminal operations by integrating advanced technologies such as robotics, analytics, and automated workflows. These systems enable real-time monitoring, predictive maintenance, and data-driven decision-making, enhancing productivity and operational efficiency. Robotics streamline repetitive tasks such as cargo handling, while advanced analytics provide actionable insights to optimize resource allocation and reduce downtime.

Additionally, automated workflows minimize human intervention, lowering operational costs and improving accuracy in managing complex logistics networks. Smart terminals also enhance connectivity, enabling seamless integration with supply chain ecosystems, which is crucial for modern logistics operations. As the demand for efficient, cost-effective, and technologically advanced solutions rises, smart terminals are becoming an essential part of the global logistics infrastructure, creating significant terminal management system market opportunities.

Terminal Management System Market Segmental Analysis :

By Offering:

Based on the offering, the terminal management system market is segmented into software and services.

The software segment accounted for the largest revenue of the total terminal management system market share in 2023.

- Comprehensive software platforms facilitate terminal automation, enabling efficient control of processes such as inventory management, loading, and unloading.

- Advanced analytics and reporting tools enhance decision-making capabilities, driving adoption in industrial and commercial sectors.

- Customizable software solutions cater to specific industry needs, ensuring seamless integration with existing infrastructure.

- Thus, as per the segmental trends analysis the dominance of this segment is attributed to its role in enhancing operational efficiency and reducing downtime, further fueling terminal management system market expansion.

The services segment is expected to register the fastest CAGR during the forecast period.

- Consulting services guide organizations in implementing terminal management solutions tailored to unique operational requirements.

- Maintenance and support services ensure the smooth functioning of systems, minimizing disruptions in terminal operations.

- Integration services provide seamless connectivity between software and hardware components, enhancing overall system efficiency.

- As per the terminal management system market analysis, increasing demand for expert assistance in navigating complex terminal environments is driving the rapid growth of this segment.

By Project Type:

Based on project type, the market is categorized into greenfield and brownfield projects.

The greenfield segment held the largest revenue of the total terminal management system market share in 2023.

- Greenfield projects leverage advanced terminal management systems from inception, enabling state-of-the-art automation and process optimization.

- These projects prioritize sustainability, adopting solutions designed to minimize environmental impact and improve energy efficiency.

- The growing number of new industrial and commercial terminals in emerging economies contributes to the segment's prominence.

- As per the terminal management system market trends, the dominance of this segment reflects the preference for modern infrastructure that incorporates cutting-edge terminal management technologies.

The brownfield segment is expected to register the fastest CAGR during the forecast period.

- Brownfield projects focus on upgrading and modernizing existing terminals, integrating advanced software and hardware components.

- Retrofitting operations with terminal management systems improves operational efficiency and extends the lifespan of older facilities.

- The segment’s growth is fueled by increasing investments in modernizing infrastructure to meet evolving industry standards.

- The analysis of segmental trends shows that the rising focus on digital transformation in established terminals is propelling the growth of this segment, further driving the terminal management system market demand.

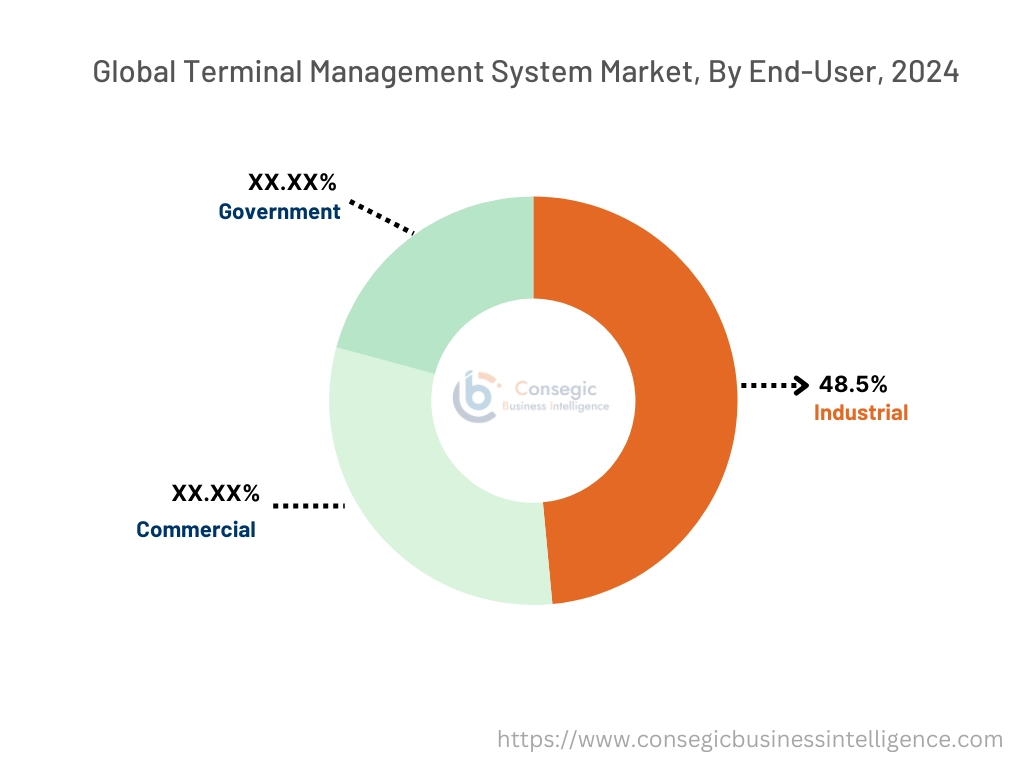

By End-User:

Based on end-user, the terminal management system market is segmented into industrial, commercial, and government.

The industrial segment accounted for the largest revenue of 48.5% share in 2024.

- Industrial facilities adopt terminal management systems to streamline complex processes such as storage, transportation, and distribution.

- Advanced solutions enable real-time monitoring of operations, ensuring compliance with safety and regulatory standards.

- The segment benefits from significant investments in terminal automation across industries such as oil & gas, chemicals, and power generation.

- As per the terminal management system market analysis, the dominance of this segment is attributed to the critical role of terminal management systems in optimizing industrial operations.

The government segment is expected to register the fastest CAGR during the forecast period.

- Government entities utilize terminal management systems for managing public terminals and ensuring efficient cargo handling.

- These systems support strategic initiatives aimed at improving logistics and supply chain efficiency in public infrastructure projects.

- Increasing investments in smart city projects and modernization of public terminals are driving the growth of this segment.

- As per the terminal management system market trends, the rising focus on digital transformation and infrastructure development underpins the rapid expansion of the government segment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

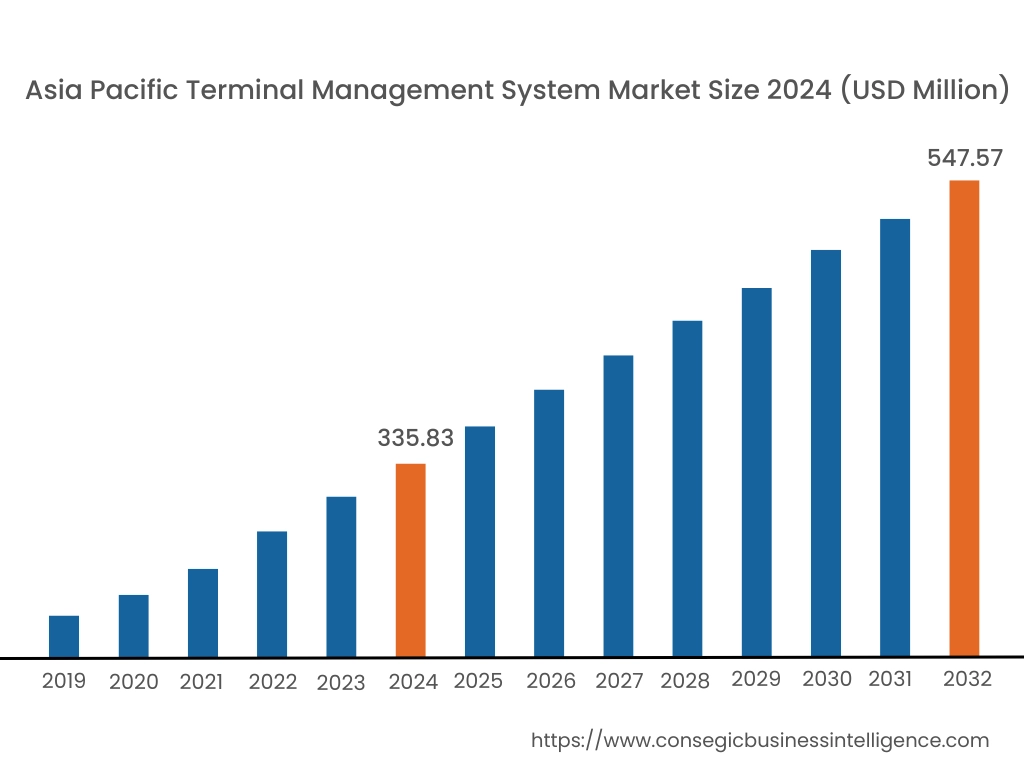

Asia Pacific region was valued at USD 335.83 Million in 2024. Moreover, it is projected to grow by USD 350.51 Million in 2025 and reach over USD 547.57 Million by 2032. Out of this, China accounted for the maximum revenue share of 33.6%. The Asia-Pacific region is witnessing rapid advancements in the TMS market, propelled by industrial growth and increasing investments in automation across countries like China, India, and Japan. The expanding oil and gas sector in these nations necessitates efficient terminal management to handle complex operations. A prominent trend is the deployment of cloud-based TMS solutions to facilitate scalability and flexibility. Analysis suggests that the pursuit of operational excellence and the need to meet international standards are key factors influencing the terminal management system market growth in this area.

North America is estimated to reach over USD 582.82 Million by 2032 from a value of USD 378.25 Million in 2024 and is projected to grow by USD 392.92 Million in 2025. This region commands a significant share of the TMS market, driven by the widespread adoption of advanced automation technologies and a strong emphasis on operational efficiency. The presence of key industry players and substantial investments in infrastructure further bolster the market. A notable trend is the integration of Internet of Things (IoT) solutions to enhance real-time monitoring and control within terminal operations. Analysis indicates that the focus on reducing operational costs and improving safety standards continues to propel market dynamics in this region.

European countries, including Germany, France, and the United Kingdom, are significant contributors to the TMS market. The region's commitment to environmental sustainability and stringent regulatory frameworks has led to the adoption of TMS solutions that ensure compliance and enhance efficiency. A significant trend is the collaboration among European firms to develop innovative TMS technologies tailored to specific sector needs are creating new terminal management system market opportunities in this region.

In the Middle East and Africa, the TMS market is gradually evolving, with a focus on enhancing the efficiency of oil and gas terminal operations. Nations rich in natural resources are investing in TMS solutions to optimize supply chain processes and ensure regulatory compliance. A notable trend is the adoption of integrated TMS platforms that offer end-to-end visibility and control.

Latin America presents emerging opportunities for the TMS market, with countries such as Brazil and Mexico focusing on modernizing their industrial operations. The region's emphasis on improving operational efficiency and adhering to safety standards has spurred interest in advanced TMS solutions. Government policies aimed at enhancing technological capabilities influence terminal management system market expansion.

Top Key Players and Market Share Insights:

The Terminal Management System market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Terminal Management System market. Key players in the Terminal Management System industry include -

- ABB Ltd. (Switzerland)

- Honeywell International Inc. (USA)

- Siemens AG (Germany)

- Emerson Electric Co. (USA)

- Rockwell Automation, Inc. (USA)

- Schneider Electric SE (France)

- Yokogawa Electric Corporation (Japan)

- General Electric Company (USA)

- Endress+Hauser AG (Switzerland)

- Implico Group (Germany)

Terminal Management System Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2032 |

| Market Size in 2032 | USD 1,798.27 Million |

| CAGR (2025-2032) | 5.9% |

| By Offering |

|

| By Project Type |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Terminal Management System Market? +

The Terminal Management System Market size is estimated to reach over USD 1,798.27 Million by 2032 from a value of USD 1,140.30 Million in 2024 and is projected to grow by USD 1,186.80 Million in 2025, growing at a CAGR of 5.9% from 2025 to 2032.

What are the key segments in the Terminal Management System Market? +

The market is segmented by offering (software and services), project type (greenfield and brownfield), and end-user (industrial, commercial, and government).

Which segment is expected to grow the fastest in the Terminal Management System Market? +

The services segment is expected to register the fastest CAGR during the forecast period, driven by growing demand for expert assistance in implementing and maintaining terminal management systems.

Who are the major players in the Terminal Management System Market? +

Key players in the Terminal Management System market include ABB Ltd. (Switzerland), Honeywell International Inc. (USA), Siemens AG (Germany), Emerson Electric Co. (USA), Rockwell Automation, Inc. (USA), Schneider Electric SE (France), Yokogawa Electric Corporation (Japan), General Electric Company (USA), Endress+Hauser AG (Switzerland), and Implico Group (Germany).