- Summary

- Table Of Content

- Methodology

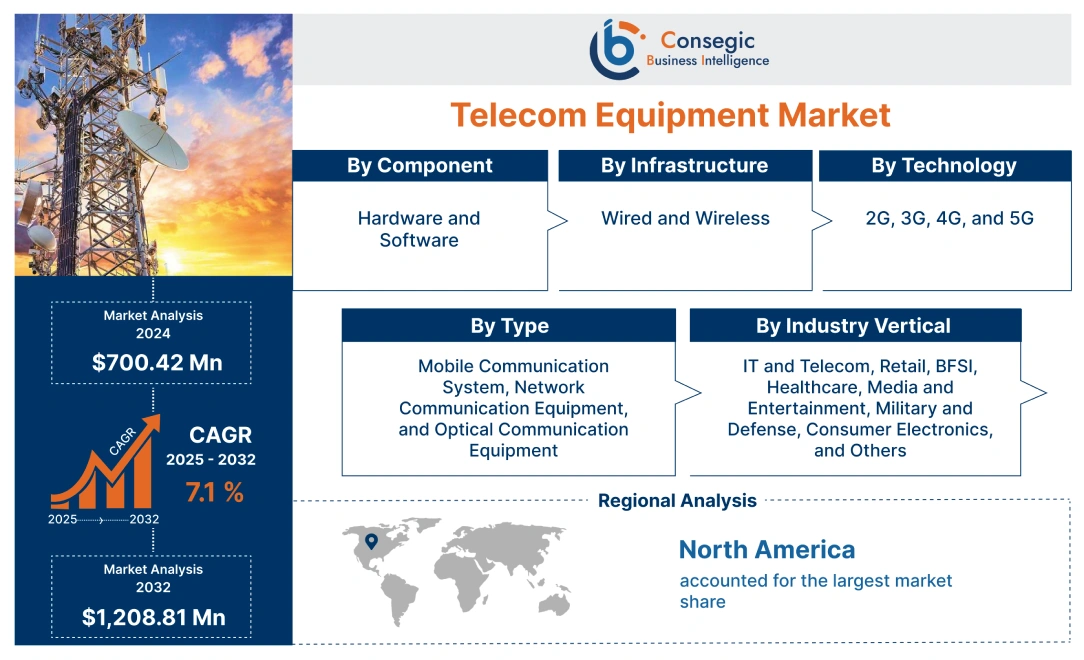

Telecom Equipment Market Size :

Telecom Equipment Market size is estimated to reach over USD 1,208.81 Million by 2032 from a value of USD 700.42 Million in 2024 and is projected to grow by USD 737.38 Million in 2025, growing at a CAGR of 7.10% from 2025 to 2032.

Telecom Equipment Industry Definition & Overview:

Telecom equipment refers to the hardware and infrastructure components essential for the functioning of telecommunications networks. The equipment encompasses a diverse range of devices, including switches, routers, modems, transmitters, receivers, base stations, multiplexers, network management systems, and optical fiber equipment. The devices enable the transmission, reception, and processing of voice, data, and multimedia communications. Additionally, the equipment plays a crucial role in facilitating connectivity, routing signals, managing network performance, and ensuring efficient communication across various networks and mediums.

Telecom Equipment Market Insights :

Telecom Equipment Market Dynamics - (DRO) :

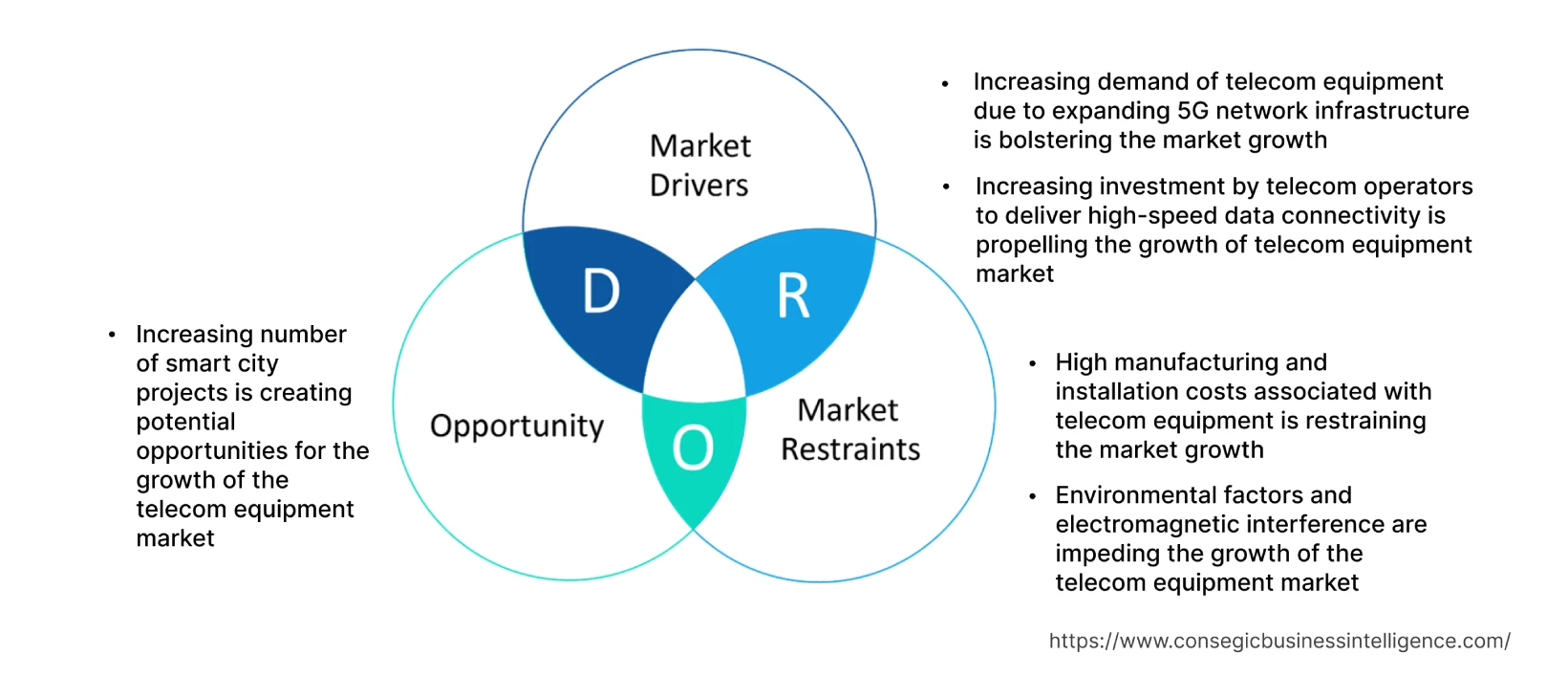

Key Drivers :

Increasing demand for telecom equipment due to expanding 5G network infrastructure is bolstering the market progress

5G networks require a higher number of base stations, antennas, and small-cell power amplifiers to ensure extensive coverage and support for high-speed connectivity. In addition, 5G networks rely on advanced telecom equipment to handle the higher bandwidth, low latency, and massive connectivity requirements. Manufacturers are developing and supplying specialized equipment namely 5G base stations, Massive MIMO (Multiple-Input Multiple-Output) antennas, and millimeter-wave (mmWave) radios to support the unique characteristics of 5G networks. Moreover, 5G networks require robust backhaul and fronthaul solutions to connect the base stations and enable the efficient transfer of data between the network core and access points. The equipment providers play a crucial role in supplying the necessary equipment, including high-capacity fiber optics, microwave links, and network switches, to establish reliable and high-performance backhaul and fronthaul networks. Consequently, the expanding 5G network infrastructure is driving the market to provide higher bandwidth and low latency. For instance, in October 2022, the Indian Prime Minister launched 5G technology in India to improve the digital infrastructure of the country. 5G technology is essential to enhance the functioning of various sectors namely education, agriculture, and healthcare, thus contributing significantly to driving the telecom equipment market growth.

Increasing investment by telecom operators to deliver high-speed data connectivity propels the market

Telecom operators are investing in upgrading the networks including deployment of additional base stations and increasing network capacity to meet the growing demand for high-speed data connectivity. Telecom equipment manufacturers benefit from the increasing demand for equipment including base stations, antennas, routers, and switches, thus promoting the market. Additionally, telecom operators are also investing heavily in fiber optic and 5G networks to deliver high-speed data connectivity. Fiber optics and 5G networks provide high bandwidth and low latency, enabling the transmission of large volumes of data at faster speeds. The installation of advanced network infrastructure drives the need for fiber optic cables, connectors, and transceivers, further accelerating the market. For instance, in December 2022, Bharti Airtel and Meta Platforms, Inc. collaborated to invest to upgrade the network connectivity infrastructure and also to support the emerging data requirement of users in India. The collaboration aims to support the rising trend of high-speed data and expansion of 5G network infrastructure, hence contributing notably to fueling the telecom equipment market demand.

Key Restraints :

High manufacturing and installation costs associated with telecom equipment are restraining the market.

The manufacturing of telecom equipment involves significant capital investments in research and development, production facilities, and advanced technologies that hinder the market. In addition, high initial costs restrain new entrants, causing a lack of competition among existing and new players which creates a monopoly and raises the equipment prices. Moreover, the high upfront costs including equipment installation, network integration, and ongoing maintenance expenses deter telecom operators from expanding the networks, thus hampering the telecom equipment market demand.

Environmental factors and electromagnetic interference are impeding the market.

Environmental factors including rain and fog affect signal propagation and quality. In urban areas with dense infrastructure or in remote regions with challenging terrains, achieving reliable and consistent signal coverage is a technical challenge. Telecom operators need to invest in specialized equipment, namely signal boosters, repeaters, and antenna systems, to overcome environmental restraints and ensure adequate signal coverage. Additionally, Electromagnetic Interference (EMI) inhibits the proper functioning of the equipment, leading to signal degradation, dropped calls, or data transmission errors. Therefore the market trends analysis shows that manufacturers need to design the products to minimize susceptibility to EMI, resulting in additional manufacturing costs, thus impeding telecom equipment market growth.

Future Opportunities :

Increasing number of smart city projects is creating potential opportunities.

Smart cities require robust connectivity infrastructure to support various applications and services. Telecom equipment, including fiber optic networks, base stations, antennas, and wireless connectivity solutions, are essential components for providing reliable and high-speed communication networks in smart cities. In addition, smart city projects leverage Internet of Things (IoT) devices and sensors to monitor and manage urban systems namely transportation, energy, waste management, and public safety. Telecom equipment, including IoT gateways, modules, and network infrastructure, is needed to connect and communicate with the IoT devices. As per the analysis of market trends, the growing adoption of IoT in smart city initiatives is projected to create potential opportunities for the market.

Telecom Equipment Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,208.81 Million |

| CAGR (2025-2032) | 7.10% |

| By Component | Hardware and Software |

| By Type | Mobile Communication System, Network Communication Equipment, and Optical Communication Equipment |

| By Infrastructure | Wired and Wireless |

| By Technology | 2G, 3G, 4G, and 5G |

| By Industry Vertical | IT and Telecom, Retail, BFSI, Healthcare, Media and Entertainment, Military and Defense, Consumer Electronics, and Others |

| By Region | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

| Key Players | Carritech Limited, Extreme Networks, Inc., FiberHome Technologies, Fujitsu Limited, Huawei Technologies Co. Ltd, Juniper Networks, Inc., Rakuten Mobile, Inc., NEC Corporation, Nokia Corporation, Qualcomm TechCompany, Inc., Ribbon Communications Operating Company, Inc., Telefonaktiebolaget LM Ericsson, ZTE Corporation |

Telecom Equipment Market Segmental Analysis :

Based on the Component :

The component segment is bifurcated into hardware and software.

Hardware accounted for the largest market revenue in 2024 and includes hardware network, IP intercom hardware, servers, and storage hardware, among others. Hardware network holds the maximum share as the hardware components form the backbone of the networks, facilitating the transmission of voice-over-data and multimedia communications. Additionally, hardware networks are designed to provide high performance and are optimized for handling large volumes of data, ensuring low latency, and delivering consistent connectivity. For instance, in June 2023, ventureLAB launched Hardware Angel Network, an advanced telecom equipment for delivering high-quality data connectivity to users. The advanced equipment is designed to provide low latency to users, improving the telecom infrastructure, hence contributing remarkably to accelerating telecom equipment market expansion.

Software is projected to witness the fastest CAGR in the market during the forecast period. The growth is attributed to the shift from traditional hardware-based solutions to software-based virtualized networks. In addition, the software-defined network allows for centralized network control and management through software, providing flexibility, scalability, and cost-efficiency. Moreover, the emergence of network function virtualization decouples network functions from dedicated hardware appliances and virtualizes in software, allowing telecom operators to deploy network functions on standard servers and infrastructure, reducing costs and increasing agility. Consequently, the aforementioned factors are collectively responsible for accelerating the telecom equipment market trends in the upcoming years.

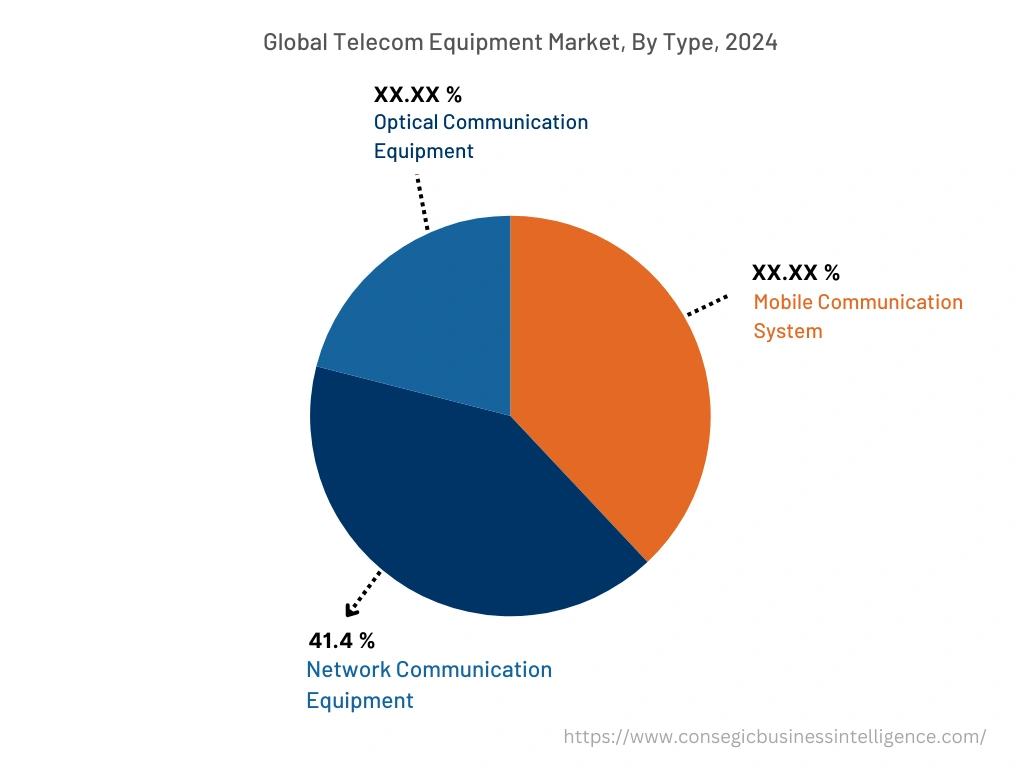

Based on the Type :

The type segment is divided into mobile communication systems, network communication equipment, and optical communication equipment.

Network communication equipment accounted for the largest market revenue of 41.4% in 2024 as network communication equipment forms the fundamental infrastructure of telecom networks. Network communication equipment includes switches, routers, gateways, access points, and other devices that enable the routing, switching, and transmission of data within and between networks. The components are essential for establishing and managing communication pathways, ensuring connectivity, and enabling data transfer across various network nodes. In addition, network communication equipment supports voice communication, data transmission, video streaming, internet access, and cloud services, among others, further driving the adoption of communication equipment.

Mobile communication system is anticipated to witness the fastest CAGR during the forecast period. The progress of the market is endorsed by the rising number of mobile subscribers worldwide, along with the expanding mobile networks, and rising internet penetration. In addition, the exponential surge of mobile data traffic, fueled by video streaming, social media usage, app downloads, and other data-intensive activities, is also contributing to the mobile communication system segment. Moreover, the increasing adoption of mobile communication systems in various sectors including railway, retail, and healthcare is further promoting the market. For instance, in September 2022, Huawei introduced the Future Railway Mobile Communication System (FRMCS) for the development of a secure, efficient, and smarter railway communications network. The system is launched to reshape the digital platform of the railway and improve the digital infrastructure. Thus, the segmental trends analysis concludes that the aforementioned factors are contributing significantly to boosting the telecom equipment market trends.

Based on the Infrastructure :

The infrastructure segment is bifurcated into wired and wireless.

Wireless infrastructure accounted for the largest market revenue in 2024 and is also projected to witness the fastest CAGR in the upcoming years. Wireless infrastructure enables ubiquitous connectivity, allowing users to access communication services without the need for physical cables. In addition, wireless networks provide coverage over large areas, including urban, suburban, and rural regions, ensuring widespread connectivity and accessibility. Moreover, wireless infrastructure allows users to move freely while staying connected and is increasingly adopted in various industries and applications, including transportation, logistics, healthcare, and smart cities. Furthermore, wireless technologies enable the deployment of mobile communication solutions, namely cellular networks, Wi-Fi hotspots, and wireless sensor networks, facilitating seamless connectivity. Consequently, the aforementioned factors are collectively responsible for driving the telecom equipment market opportunities during the forecast period.

Based on the Technology :

The technology segment is classified into 2G, 3G, 4G, and 5G.

4G accounted for the largest market share of the total telecom equipment market share in 2024 as 4G technology is based on globally recognized standards including Long-Term Evolution (LTE) and Worldwide Interoperability for Microwave Access (WiMAX). The standardization ensures compatibility and interoperability between different network equipment manufacturers and network operators and also simplifies the deployment process and reduces costs. In addition, 4G networks provide significantly faster data speeds compared to previous generations. The increased speed enables a wide range of bandwidth-intensive applications, including video streaming, online gaming, and cloud-based services. Moreover, 4G technology offers improved network capacity, allowing more simultaneous connections and better handling of high data traffic. Thus, analysis of segmental trends shows that the aforementioned factors are contributing significantly to driving the segment.

The 5G segment is anticipated to witness the fastest CAGR in the market during the forecast period. The growth of the market is attributed to the ability of 5G networks to offer significantly higher network capacity compared to previous generations. Additionally, 5G networks utilize advanced techniques namely massive MIMO (Multiple-Input Multiple-Output) and beamforming to support a larger number of devices simultaneously. Moreover, 5G promises substantially faster data speeds and delivers peak download speeds of up to 10 gigabits per second. The high speed enables users to download and stream high-definition content, participate in real-time applications, and experience seamless virtual reality and augmented reality experiences. Furthermore, the increasing investments by the government to initiate 5G services to enhance the digital infrastructure are also contributing remarkably to bolstering the market. For instance, in April 2023, the United Kingdom government invested approximately USD 44.02 million to boost the 5G infrastructure. Thus, the telecom equipment market analysis shows that the investment is made with the aim to enhance the digital infrastructure by 2030, hence contributing notably to promoting the market.

Based on the Industry Vertical :

The industry vertical segment is categorized into IT and telecom, retail, BFSI, healthcare, media and entertainment, military and defense, consumer electronics, and others.

Consumer electronics accounted for the largest market share of the overall telecom equipment market share in 2024 as telecom equipment forms the backbone of mobile communication infrastructure, enabling voice calls, text messaging, and internet connectivity on smartphones and other mobile devices. Additionally, the equipment includes components namely cellular base stations, antennas, signal amplifiers, and network switches that facilitate wireless communication between devices and cellular networks. Consequently, the expanding consumer electronics sector is driving the market to enable seamless communication. For instance, in November 2022, according to the India Brand Equity Foundation (IBEF), the consumer electronics sector accounted for USD 9.84 billion in 2021 and is expected to reach USD 21.18 billion in 2025. The rise in the consumer electronics sector thus contributes remarkably to bolstering the telecom equipment market expansion.

The IT and telecom sector is predicted to witness the fastest CAGR during the forecast period. Telecom equipment forms the backbone of telecommunication networks, including landline, mobile, and Internet Service Provider (ISP) networks. The equipment enables voice and data communication, connectivity, and the transmission of information across different communication channels. In addition, the equipment is essential for establishing and maintaining network infrastructure including routers, switches, network cables, wireless access points, and network management systems. The components enable the creation, management, and maintenance of local area networks (LANs), wide area networks (WANs), and other network architectures necessary for IT and telecommunication operations, hence the segmental trends analysis depicts that these are contributing significantly to propelling the telecom equipment market opportunities.

Based on the Region :

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

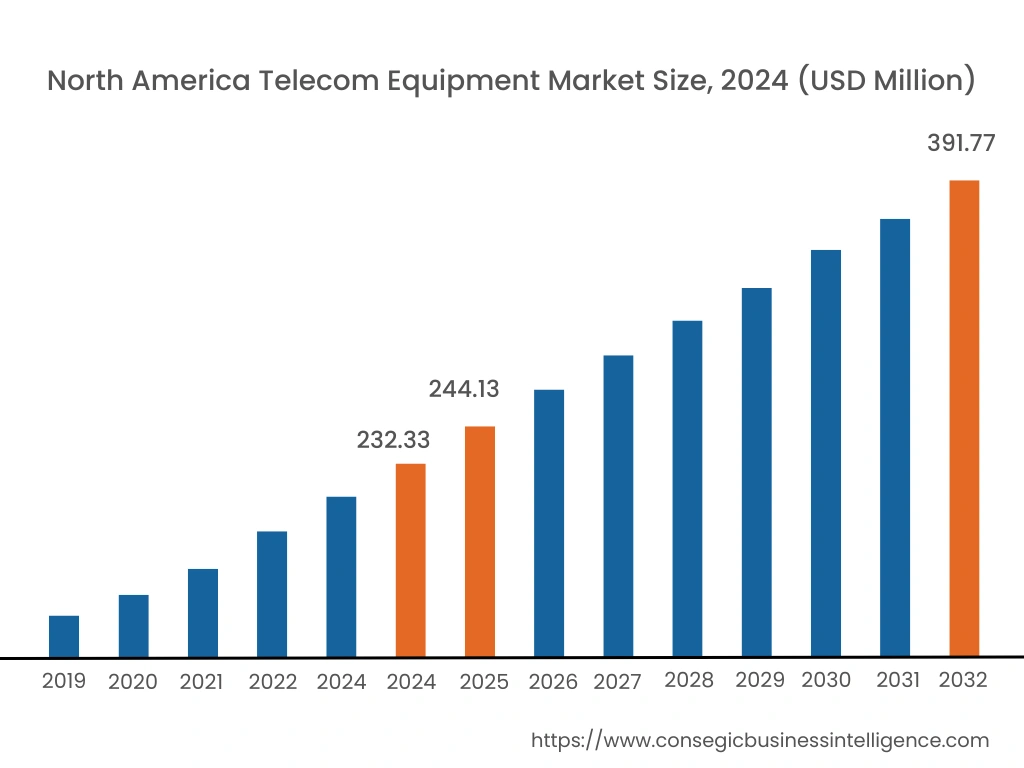

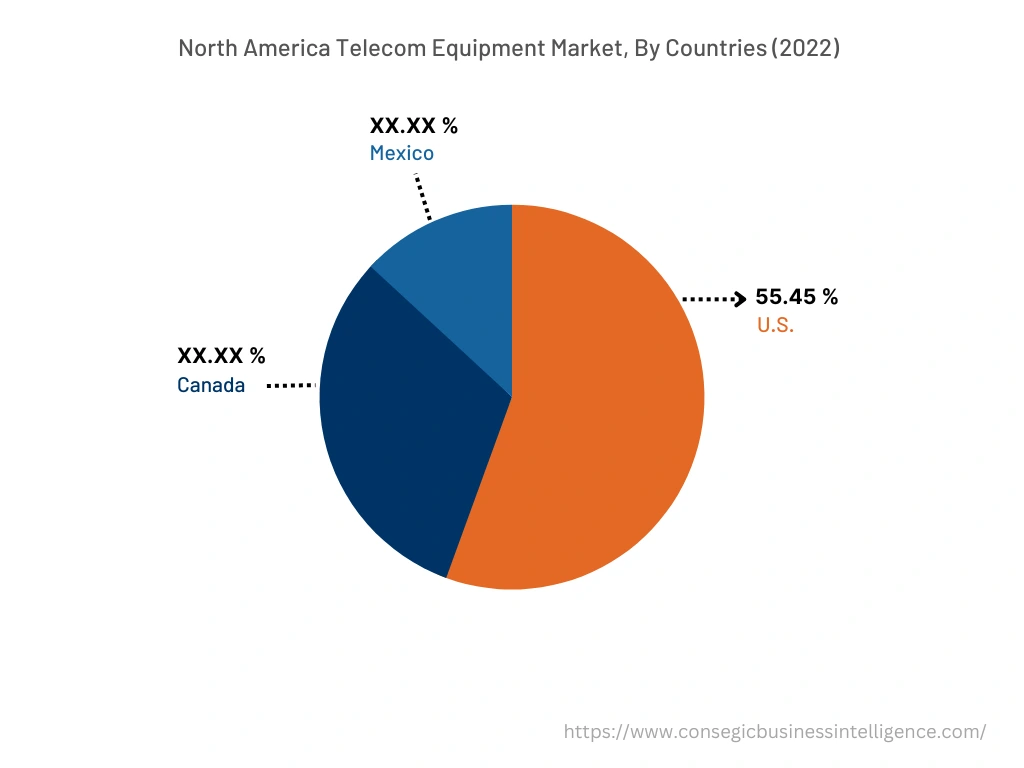

North America is estimated to reach over USD 391.77 Million by 2032 from a value of USD 232.33 Million in 2024 and is projected to grow by USD 244.13 Million in 2025. In addition, in the region, the U.S. accounted for the maximum revenue share of 55.45% in the year 2024. Additionally, as per the telecom equipment market analysis, the region's advanced telecommunications infrastructure, including high-speed broadband networks, extensive fiber-optic connectivity, and 5G cellular networks, provides a solid foundation for the deployment and adoption of the equipment. Moreover, North America boasts robust research and development capabilities in the telecom sector along with the presence of top-tier universities, research institutions, and technology hubs encourages innovation and collaboration among academia, industry, and government organizations. Furthermore, the increasing investments by the government to develop advanced communication technologies are also contributing to driving market growth. For instance, in April 2021, the Department of Defense in partnership with The National Science Foundation invested USD 40 million for the expansion of cellular, Wi-Fi, and satellite networks to connect billions of Americans across the United States.

Asia Pacific is expected to register the fastest CAGR of 7.5% during the forecast period in the telecom equipment market. The regional trends analysis shows that Asia Pacific is at the forefront of mobile connectivity, with high smartphone penetration and data usage. The region has also been actively rolling out 5G networks, with countries including China, South Korea, and Japan leading the way. In addition, the deployment of 5G technology requires significant investments in the equipment, contributing to the growth of the market in the region. Moreover, the growth of e-commerce and digital services in the Asia Pacific is driving the need for robust telecom infrastructure and equipment. The popularity of online shopping, digital payments, and on-demand services is increasing the demand for high-speed connectivity, data centers, and cloud infrastructure, further driving the adoption of telecom equipment. Consequently, the expanding digital infrastructure and rising e-commerce sector are the key factors responsible for accelerating market growth.

Top Key Players & Market Share Insights :

The global telecom equipment market features a competitive landscape with several major players vying for market stakes. The market is dynamic, and the competitive landscape may have evolved with emerging players and evolving partnerships or collaborations. Key players are in the telecom equipment industry:-

- Carritech Limited

- Extreme Networks, Inc.

- Qualcomm TechCompany, Inc.

- Telefonaktiebolaget LM Ericsson

- ZTE Corporation

- Ribbon Communications Operating Company, Inc.

- FiberHome Technologies

- Fujitsu Limited

- Huawei Technologies Co. Ltd

- Juniper Networks, Inc.

- Rakuten Mobile, Inc.

- NEC Corporation

- Nokia Corporation

Recent Industry Developments :

- In July 2023, Rakuten Mobile, Inc. launched a research and development project for the development of advanced Open RAN integration infrastructure for Post-5G Information and Communication Systems.

- In June 2022, Nokia Corporation and Proximus collaborated together to successfully enhance the performance of 5G network slicing using advanced radio software-defined telecom networking equipment.

Key Questions Answered in the Report

What is telecom equipment? +

Telecom equipment refers to the hardware and infrastructure components essential for the functioning of telecommunications networks. The equipment encompasses a diverse range of devices, including switches, routers, modems, transmitters, receivers, base stations, multiplexers, network management systems, and optical fiber equipment.

What specific segmentation details are covered in the telecom equipment market report, and how is the dominating segment impacting the market growth? +

Hardware accounted for the largest market share as hardware networks are designed to provide high performance and are optimized for handling large volumes of data, ensuring low latency, and delivering consistent connectivity.

What specific segmentation details are covered in the telecom equipment market report, and how is the fastest segment anticipated to impact the market growth? +

It and telecommunication are predicted to witness the fastest growth as telecom equipment is essential for establishing and maintaining network infrastructure including routers, switches, network cables, wireless access points, and network management systems.

Which region is anticipated to witness the highest CAGR during the forecast period, 2025-2032? +

Asia Pacific is anticipated to witness the fastest CAGR during the forecast period due to the expanding digital infrastructure and rising e-commerce sector.