- Summary

- Table Of Content

- Methodology

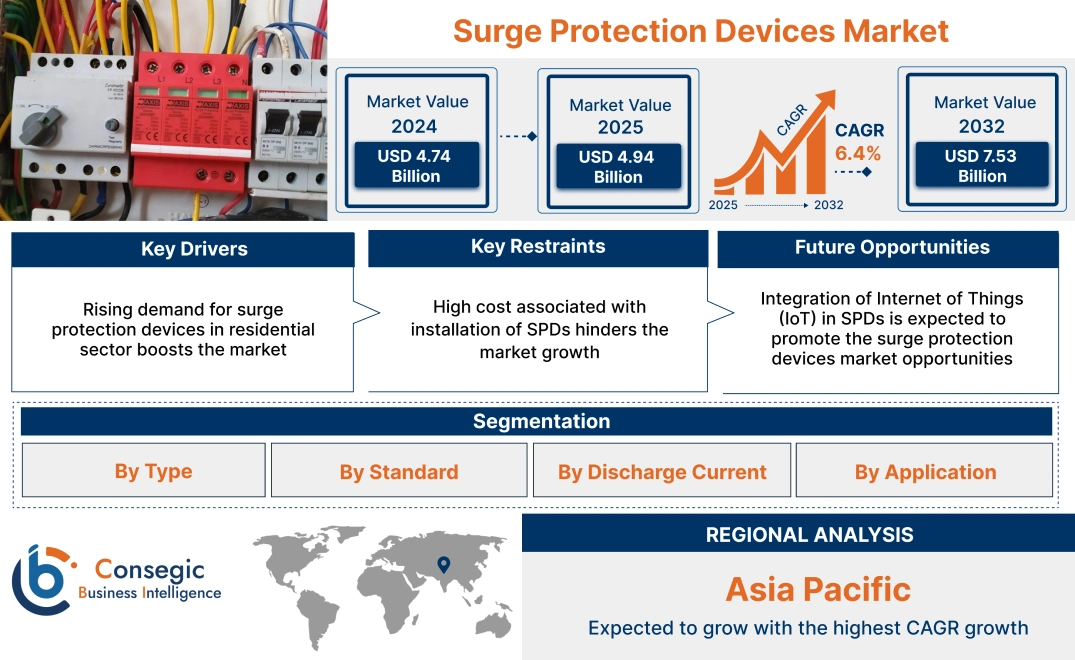

Surge Protection Devices Market Size:

Surge Protection Devices Market size is estimated to reach over USD 7.53 Billion by 2032 from a value of USD 4.74 Billion in 2024 and is projected to grow by USD 4.94 Billion in 2025, growing at a CAGR of 6.4% from 2025 to 2032.

Surge Protection Devices Market Scope & Overview:

Surge protection devices (SPDs) protect the electrical equipment from damage caused by voltage spikes and surges. The sudden voltage spikes are caused due to lightning strikes, power switching, damaged wiring, or other electrical disturbances. The SPDs absorb excess voltage from power surges and redirect it to ground before it damages the electronics systems.The devices prevent potential fires, extend the lifespan of devices, and protect against power fluctuations. The devices are used in residential, industrial, and commercial sectors.

Surge Protection Devices Market Dynamics - (DRO) :

Key Drivers:

Rising demand for surge protection devices in residential sector boosts the market

In residential buildings, SPDs are used to protect sensitive electronic equipment including computers, televisions, gaming consoles, appliances, and other electronics. The SPDs protect against voltage spikes caused by lightning strikes, which tend to travel through power lines and damage electronics.Moreover, SPDs are plugged directly into wall outlets and then used to power multiple electronic devices, or are installed at the electrical panel for complete-house protection.

- For instance, the S. Census Bureau and the Department of Housing and Urban Development announced that 657,000 new houses were sold in January 2025.

Hence, the rising sales of residential units is increasing the adoption of surge protection devices for protecting sensitive electronic equipment installed in residential spaces, in turn driving the surge protection devices market growth.

Key Restraints:

High cost associated with installation of SPDs hinders the market growth

The high cost of installation of SPDs is attributed due to complex wiring configurations, labor costs, system complexity, and requirement of additional components including grounding systems, which are primary factors restraining the adoption of SPDs in the market. The cost barrier discourages individuals and small businesses from implementing surge protection measures, leading to damage of sensitive electronics from sudden power surges.

Thus, the market analysis shows that the aforementioned factors are restraining the surge protection devices market demand.

Future Opportunities :

Integration of Internet of Things (IoT) in SPDs is expected to promote the surge protection devices market opportunities

SPDs integrated with IoT are equipped with sensors and connectivity capabilities. This allows the devices to monitor and report real-time data about power surges through an IoT network. It enables features including remote monitoring, alerts on potential damage, and maintenance of connected devices.Sensors within the SPDs detect voltage fluctuations and surges, recording data such as surge magnitude, duration, and frequency.This collected data is then transmitted wirelessly to a cloud platform via an internet connection.When a significant surge is detected, the system sends alerts to users using notifications on smartphones or other devices.By analyzing historical surge data, users identify potential issues, and take preventive measures to protect connected equipment.

- For instance, Weidmüller launched VARITECTOR PU AC IoT surge protection devices. The device enables real-time status monitoring function that allows for live monitoring of the arrester.

Thus, the ongoing advancements in IoT and its integration with SPDs are projected to drive surge protection devices market opportunities during the forecast period.

Surge Protection Devices Market Segmental Analysis :

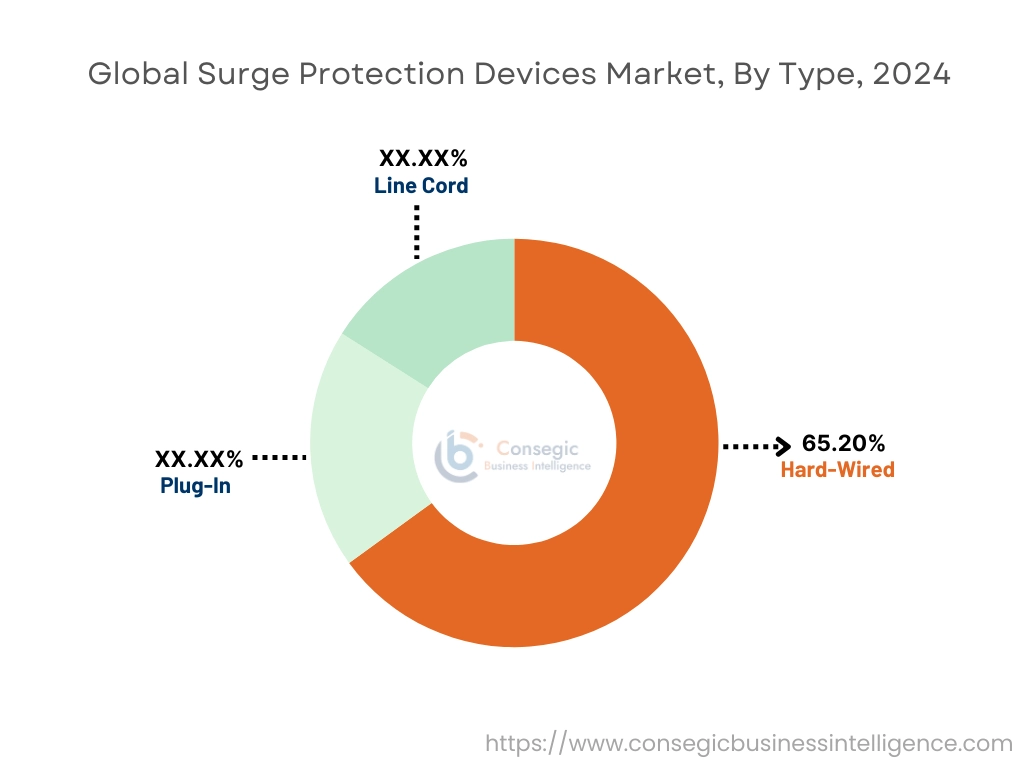

By Type:

Based on the type, the market is segmented into hard-wired, plug-in, and line cord.

Trends in the Type:

- Rising adoption of plug-in SPDs to protect valuable electronic equipment including TVs, computers, gaming consoles, and other devices.

- Increasing trend in adoption of hard-wired SPDs to protect home automation systems from damage caused by power surges, in turn, boosting the surge protection devices market size.

The hard-wired segment accounted for the largest revenue share of 65.20% in the surge protection devices market share in 2024.

- Hard-wired SPDs are installed within the electrical system of a building, mostly at the service panel. The devices protect all connected appliances and electronics from power surges by diverting the excess voltage to the ground before it reaches sensitive equipment.

- Hard-wired SPDs are designed to handle larger voltage surges compared to standard plug-in units, providing better protection against severe electrical events.

- For instance, CITEL offers hard-wired AC surge protector in its product offerings. The products are designed for single and three phase AC networks connected to sensitive equipment.

- Therefore, the wide applications of hard-wired SPDs are propelling the surge protection devices market

The plug-in segment is expected to register the fastest CAGR during the forecast period.

- The plug-in SPD is used by plugging it into a wall outlet and then plugging electronic devices into the surge protector outlets.

- They provide protection against voltage spikes caused by factors like power grid fluctuations, lightning strikes, or powering on of large appliances.

- For instance, SolarEdge offers SPD plug-in in its product portfolio. The device is suitable for both new and existing installations.

- Thus, according to surge protection devices market analysis, the aforementioned factors are driving the market growth during the forecast period.

By Standard:

Based on the standard, the market is segmented into type 1, type 2, type 3, and others.

Trends in the Standard:

- Rising trend in adoption of type 1 SPDs to protect electrical installations from direct lightning strikes and to handle high voltage surges, in turn, drives the surge protection devices market size.

- Increasing adoption of type 3 SPDs to provide direct protection to sensitive electronic equipment, including computers, TVs, and audio systems.

The type 2 segment accounted for the largest revenue in the surge protection devices market share in 2024 and it is also expected to register the fastest CAGR growth during the forecast period.

- The type 2 SPDs are used to protect electrical equipment within a building's sub-distribution panels. The devices offer protection against residual surges from lightning strikes and internal switching in systems.

- These SPDs are the second stage of surge protection after a Type 1 SPD at the service entrance panel. Type 2 devices are installed on the load side of the main distribution panel to protect connected appliances and sensitive electronics.

- For instance, Phoenix Contact offers Type 2 SPDs in its product portfolio. These devices are available in various elements including arresters, protection plugs, and others.

- Therefore, the wide applications of type 2 SPDs are driving the surge protection devices market

By Discharge Current:

Based on the discharge current, the market is segmented into less than 50 KA, 51 KA to 200 KA, and above 200 KA.

Trends in the Discharge Current:

- Rising demand in adoption of SPDs with discharge current less than 50 KA for use in home electrical panels and smaller office buildings.

- Increasing trend in adoption of SPDs with discharge current above 200 KA in main electrical panel at the service entrance to handle the initial surge from a lightning strike in large commercial or industrial buildings.

The 51 KA to 200 KA segment accounted for the largest revenue share in the market in 2024 and it is also expected to register fastest CAGR growth during the forecast period.

- The 51 KA to 200 KA discharge capacity SPDs are used in commercial and industrial places.

- These devices are used in applications where large surges of electrical current are expected, including the main power entrance of a building, industrial facilities, or locations prone to frequent lightning strikes.

- These devices handle a very high discharge capacity of 51 to 200 KA without damage and provide protection against large voltage surges.

- For instance, ABB provides ABB 4 phase industrial surge protector in its product offerings. The device is able to tackle 100 KA of surge current.

- Therefore, the market analysis depicts that the aforementioned factors are driving the surge protection devices market

By Application:

Based on the application, the market is segmented into industrial, commercial, and residential.

Trends in the Application:

- Rising adoption of SPDs in residential sector due to the need to protect sensitive electronics equipment from sudden power surges and spikes.

- Increasing demand of SPDs in industries including oil and gas, manufacturing, and others to protect equipments against over-voltages.

The industrial segment accounted for the largest revenue share in the market in 2024.

- In industrial segment, the SPDs are used to protect sensitive electrical equipment including machinery, control systems, safety interlock circuits, and communication systems from damage caused by sudden voltage spikes. The devices minimize downtime by diverting excess voltage to the ground.

- Industrial SPDs are suitable for high-power industrial applications as they are designed to handle large surge voltages compared to standard household surge protectors.

- For instance, DEHN SE offers various surge protection equipment for industrial buildings in its product portfolio. These devices can be energy-coordinated to ensure interaction of the distinct protection levels.

- Therefore, the market analysis shows that the wide applications of SPDs in industrial sector are boosting the surge protection devices market

The commercial segment is expected to register the fastest CAGR growth during the forecast period.

- In commercial segment, the SPDs are used to protect equipment such as computers, telecommunications systems, servers, and building management systems from sudden spikes caused due to lightning strikes, power fluctuations, or equipment malfunctions.

- Moreover, surge protectors provide multi-tier protection, including voltage spike protection on power lines, data lines, and other telecommunications lines.

- For instance, Siemens offers commercial SPDs in its product offerings. These products are available in BSPD, TPS4, and FSPD product ranges.

- Thus, the market analysis depicts that the rising utilization of SPDs in commercial sector is expected to drive the surge protection devices market demand during the forecast period.

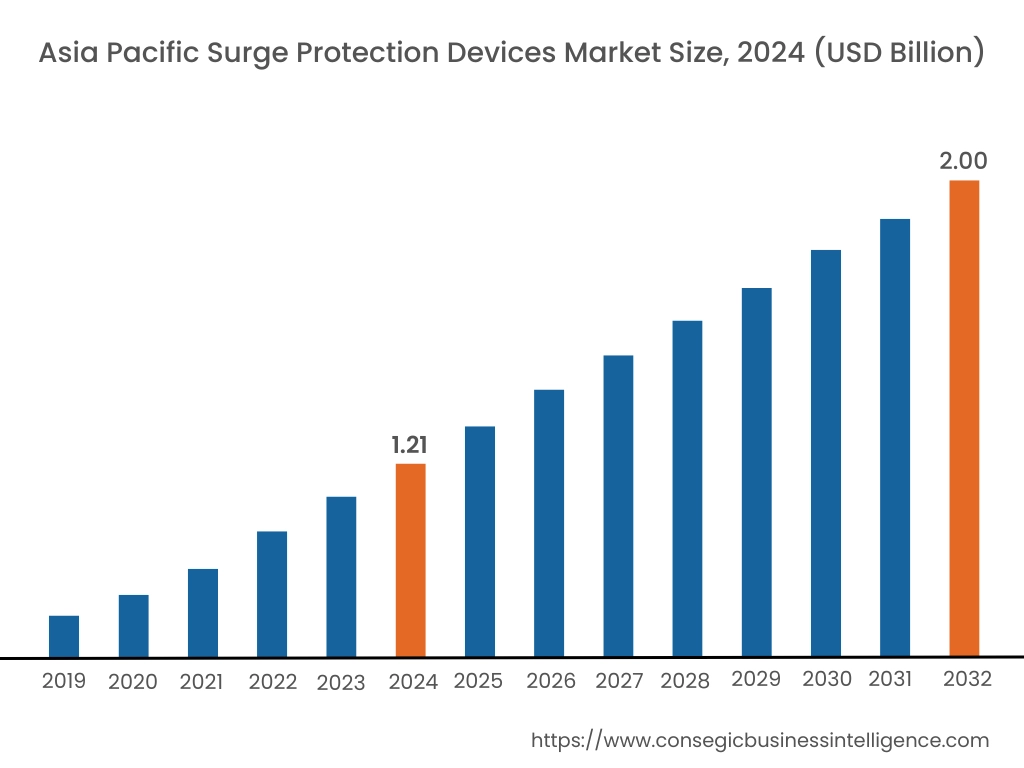

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

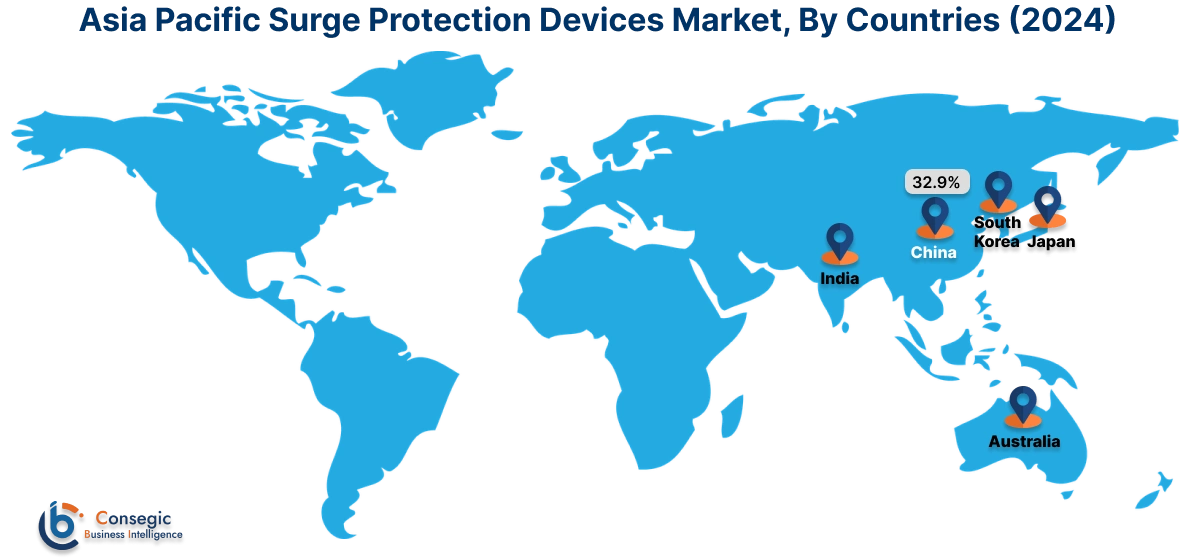

Asia Pacific region is estimated to reach over USD 2.00 Billion by 2032 from a value of USD 1.21 Billion in 2024 and is projected to grow by USD 1.26 Billion in 2025. Out of this, China accounted for the maximum revenue share of 32.9%. The market in the Asia-Pacific region is driven due to factors including rising investments in power infrastructure, rapid urbanization, increasing industrialization, and rising adoption of sensitive electronics.

- For instance, in October 2024, Secure Connection launched Honeywell licensed surge protectors. The products include 1 Outlet Surge Cube, 3 Outlet Surge Protector, 4 Outlet Surge Protector, 6 Outlet Surge Protector, and 8 Outlet Surge Protector.

North America was valued at USD 1.67 Billion in 2024. Moreover, it is projected to grow by USD 1.74 Billion in 2025 and reach over USD 2.63 Billion by 2032. The surge protection devices market expansion in the North American region is proliferating due to well-developed infrastructure, strict regulatory standards that mandate surge protection, and high reliance on advanced electrical systems in the region.

- For instance, in December 2024, Tessan launched surge protector power strip. The strip provides effective surge protection solution for household and office usage.

Additionally, the surge protection devices market analysis depicts that the European market is growing due to wide usage of SPDs in industries including manufacturing, power, and oil and gas to protect sensitive equipment. In Latin America, the market is driven by expanding commercial and industrial development. In Middle East and Africa, the market is driven by rapid urbanization, increasing pace of industrialization, and growing need for reliable power distribution solutions among others.

Top Key Players and Market Share Insights:

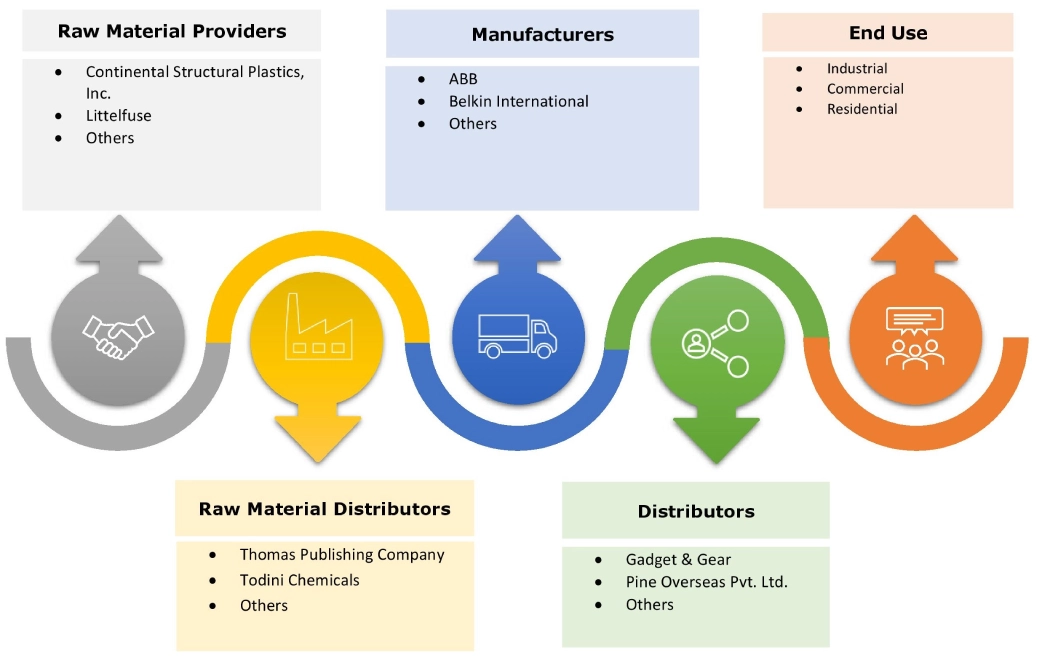

The surge protection devices industry is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global surge protection devices market. Key players in the surge protection devices industry include -

- ABB (Switzerland)

- Alltec LLC (US)

- Belkin International (US)

- CITEL-2CP SA (France)

- DEHN SE (Germany)

- Eaton Corporation plc (Ireland)

- Emerson Electric Co. (US)

- Honeywell International Inc. (US)

- Hubbell Incorporated (US)

- Littelfuse, Inc. (US)

Recent Industry Developments :

Product Launches:

- In June 2024, Belkin launched surge protection products lineup in Australia. The products offer protection to home and office electronics along with Connected Equipment Warranty (CEW).

Collaborations and Partnerships:

- In August 2024, Dallas’ CSW Industrials acquired PSP Products. This brings higher range of surge protection and load management products to CSWI.

Surge Protection Devices Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 7.53 Billion |

| CAGR (2025-2032) | 6.4% |

| By Type |

|

| By Standard |

|

| By Discharge Current |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the surge protection devices market? +

Surge Protection Devices Market size is estimated to reach over USD 7.53 Billion by 2032 from a value of USD 4.74 Billion in 2024 and is projected to grow by USD 4.94 Billion in 2025, growing at a CAGR of 6.4% from 2025 to 2032.

What are the major segments covered in the surge protection devices market report? +

The segments covered in the report are type, standard, discharge current, application, and region.

Which region holds the largest revenue share in 2024 in the surge protection devices market? +

North America holds the largest revenue share in the surge protection devices market in 2024.

Who are the major key players in the surge protection devices market? +

The major key players in the market are ABB (Switzerland), Alltec LLC (US), Belkin International (US), CITEL-2CP SA (France), DEHN SE (Germany), Eaton Corporation plc (Ireland), Emerson Electric Co. (US), Honeywell International Inc. (US), Hubbell Incorporated (US), and Littelfuse, Inc. (US).