- Summary

- Table Of Content

- Methodology

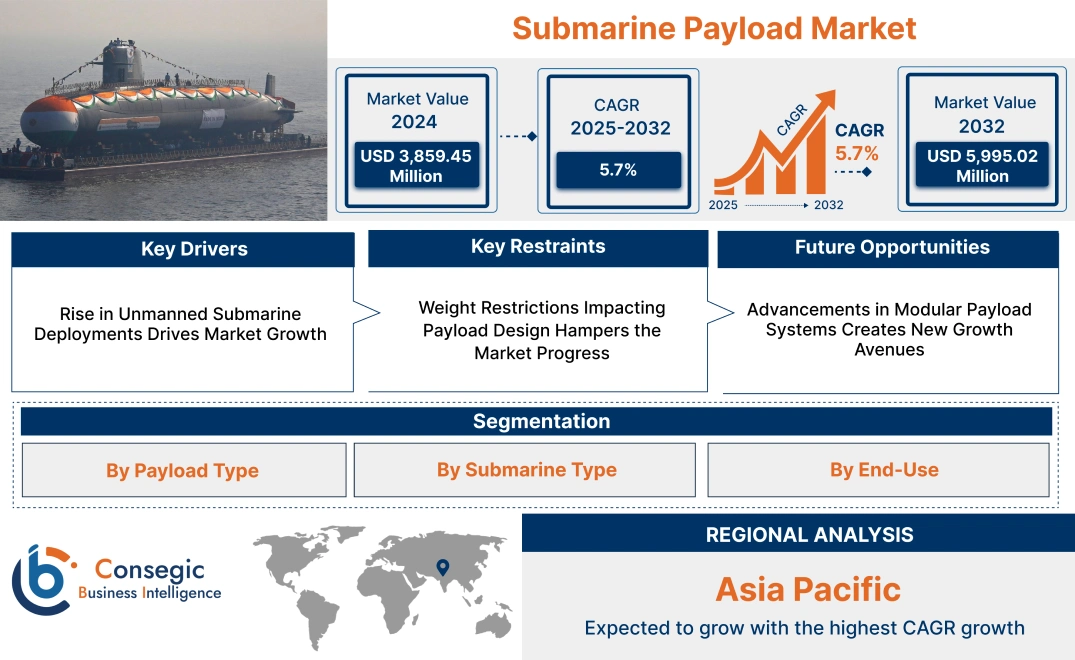

Submarine Payload Market Size:

Submarine Payload Market size is estimated to reach over USD 5,995.02 Million by 2032 from a value of USD 3,859.45 Million in 2024 and is projected to grow by USD 4,009.13 Million in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Submarine Payload Market Scope & Overview:

The submarine payload is equipment and systems carried by submarines to support various operational objectives, including surveillance, reconnaissance, communication, and combat. These payloads include torpedoes, missiles, sensors, unmanned underwater vehicles (UUVs), and communication systems, all designed to enhance the submarine's capabilities and mission efficiency.

Payload systems are tailored to meet specific mission requirements, ranging from offensive weaponry to intelligence-gathering technologies. They are engineered to function reliably in challenging underwater environments, ensuring durability, precision, and operational effectiveness. These payloads are integrated seamlessly into submarine platforms, providing flexibility and adaptability for diverse naval operations.

End-users include naval forces and defense contractors involved in modernizing and expanding submarine capabilities to address evolving security challenges. Submarine payloads play a crucial role in strengthening maritime defense strategies and enabling multi-dimensional operational capabilities.

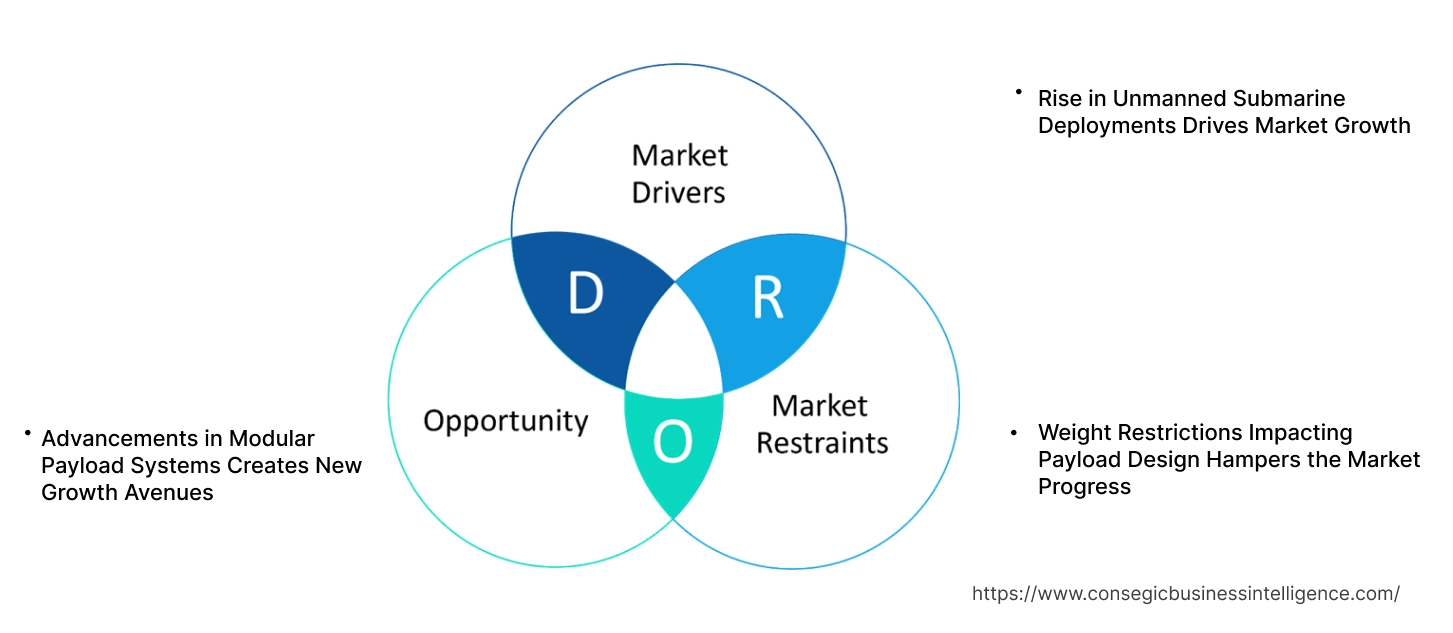

Submarine Payload Market Dynamics - (DRO) :

Key Drivers:

Rise in Unmanned Submarine Deployments Drives Market Growth

The increasing deployment of unmanned submarines is revolutionizing underwater operations, demanding compact and advanced payload systems. Unmanned underwater vehicles (UUVs) are primarily used for surveillance, mine detection, and reconnaissance missions, necessitating lightweight payloads with high functionality.

Autonomous sensors, compact torpedoes, and advanced communication modules are integral to these systems, enabling efficient operation in challenging underwater environments. These payloads must also be energy-efficient to align with the limited power capacities of unmanned platforms. The growth in the use of UUVs in naval and scientific missions is driving innovation in payload designs, focusing on miniaturization without compromising performance. This trend aligns with global naval modernization programs, further expanding opportunities for manufacturers specializing in advanced and compact payload technologies. The demand for unmanned submarines is surging, supported by their cost-effectiveness and ability to perform high-risk missions without endangering human lives. Thus, as per the market analysis, the aforementioned factors are driving the submarine payload market growth.

Key Restraints:

Weight Restrictions Impacting Payload Design Hampers the Market Progress

Submarines operate under strict weight constraints to ensure buoyancy and optimal performance during underwater missions. These limitations significantly influence the design and integration of payload systems, as exceeding weight thresholds compromises maneuverability, fuel efficiency, and mission capabilities. Payload developers must prioritize lightweight materials and compact designs, which limit the functionality or capacity of equipment such as torpedoes, sensors, and communication systems.

Additionally, achieving a balance between weight and performance often increases development costs, as advanced engineering and materials are required. These constraints make it difficult to incorporate innovative technologies while adhering to weight restrictions, hindering the submarine payload market demand.

Future Opportunities :

Advancements in Modular Payload Systems Creates New Growth Avenues

The development of modular payload systems is transforming submarine operations by providing unmatched flexibility and adaptability. These systems allow submarines to be quickly reconfigured for diverse missions, including combat operations, surveillance, and mine detection. By utilizing modular designs, navies optimize their fleet's operational efficiency, reducing the need for specialized vessels while maintaining mission readiness. Modular payloads enable the integration of advanced technologies, such as autonomous sensors, precision-guided weapons, and sophisticated communication systems, without extensive retrofitting. This approach also lowers maintenance costs and accelerates deployment timelines, making it an attractive option for both the defense and commercial industries.

Additionally, modular systems cater to the increasing demand for multi-mission capabilities, aligning with global naval modernization efforts. These advancements are driving innovation in payload technology, offering manufacturers lucrative submarine payload market opportunities to develop versatile solutions tailored to the evolving needs of modern underwater operations.

Submarine Payload Market Segmental Analysis :

By Payload Type:

Based on payload type, the market is segmented into torpedoes, missiles, mines, unmanned underwater vehicles (UUVs), and sensors & surveillance systems.

The torpedoes segment held the largest revenue of the total submarine payload market share in 2024.

- Torpedoes are a primary offensive weapon for submarines, offering precision targeting capabilities in naval warfare.

- The widespread adoption of advanced torpedoes with improved propulsion and guidance systems enhances their utility in modern submarines.

- Their versatility in combating both surface ships and submarines drives their demand in military applications.

- The analysis of segmental trends depicts that the dominance of this segment reflects the growth in investment in underwater combat capabilities globally, contributing to the submarine payload market expansion.

The unmanned underwater vehicles (UUVs) segment is expected to register the fastest CAGR during the forecast period.

- UUVs are gaining traction for their ability to perform reconnaissance, surveillance, and underwater mapping without risking human lives.

- Their use in mine detection and removal operations further supports their increasing adoption.

- Advancements in autonomous technologies are enhancing UUV functionalities, improving their efficiency in both military and civilian operations.

- As per the submarine payload market analysis, the rapid proliferation of UUVs is driven by their cost-effectiveness and ability to operate in challenging underwater environments.

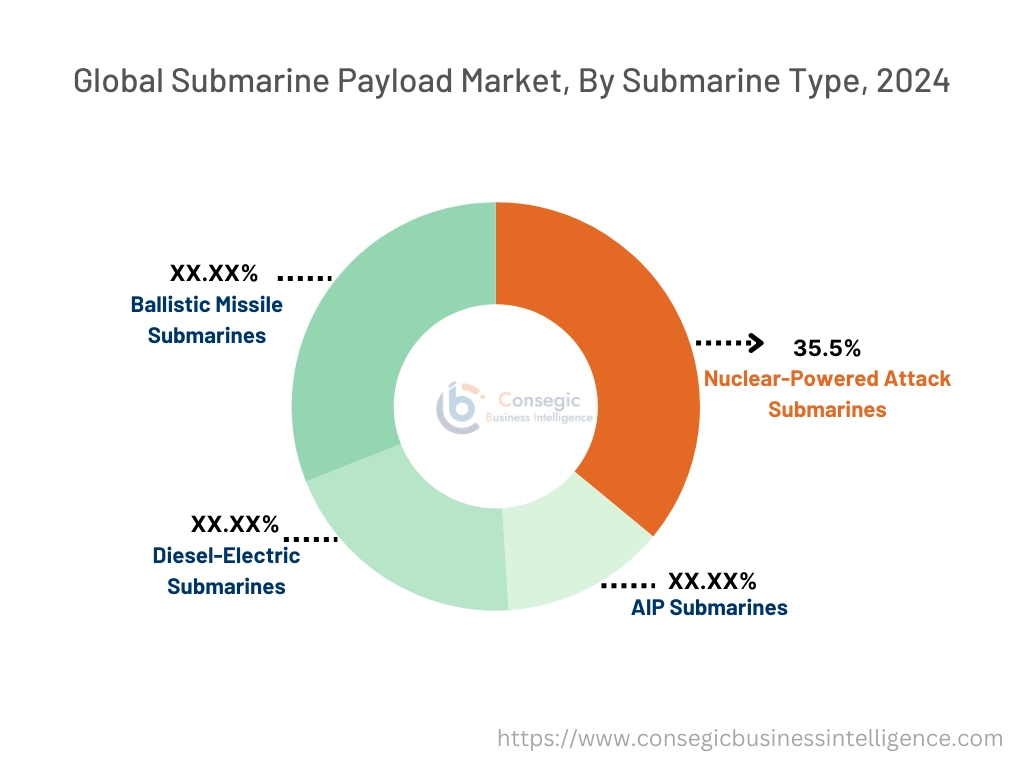

By Submarine Type:

Based on submarine type, the market is segmented into nuclear-powered attack submarines, AIP submarines, diesel-electric submarines, and ballistic missile submarines.

The nuclear-powered attack submarines segment accounted for the largest revenue of 35.5% of the total submarine payload market share in 2024.

- These submarines offer unparalleled endurance and stealth capabilities, making them indispensable for extended underwater missions.

- The ability to operate without surfacing for long durations enhances their strategic value in modern naval operations.

- They are increasingly adopted for their ability to carry advanced payloads, including missiles and UUVs, ensuring tactical superiority.

- As per the submarine payload market trends, the dominance of this segment highlights the ongoing investments in next-generation nuclear-powered submarines by global naval forces.

The air-independent propulsion (AIP) submarines segment is anticipated to grow at the fastest CAGR during the forecast period.

- AIP technology enhances the underwater endurance of non-nuclear submarines, bridging the gap between diesel-electric and nuclear-powered variants.

- Their relatively lower costs compared to nuclear submarines make them attractive for nations with budget constraints.

- AIP submarines are increasingly favored for coastal defense and tactical operations in restricted waters.

- The adoption of AIP technology is driven by the growing focus on achieving operational efficiency while maintaining stealth capabilities, fueling the submarine payload market demand.

By End-Use:

Based on end-use, the market is segmented into military and civilian applications.

The military segment held the largest revenue share in 2024.

- Submarines equipped with advanced payloads are critical assets for naval forces, ensuring dominance in underwater combat and surveillance.

- Increasing geopolitical tensions and the need for maritime security fuel investments in military submarine capabilities.

- Modernization programs by major naval powers are driving the adoption of submarines with enhanced payload integration.

- As per the submarine payload market analysis, the reliance on submarines for deterrence and strategic operations underscores their importance in the military segment.

The civilian segment is expected to grow at the fastest CAGR during the forecast period.

- Civilian applications such as underwater exploration, oil and gas pipeline inspections, and scientific research are driving the adoption of submarine payloads.

- The use of UUVs for environmental monitoring and marine life studies further supports the segment's expansion.

- Increasing investments in undersea infrastructure development creates opportunities for civilian submarine payload applications.

- Thus, technological advancements in sensors and unmanned systems are enabling cost-effective solutions for non-military purposes, fueling the submarine payload market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

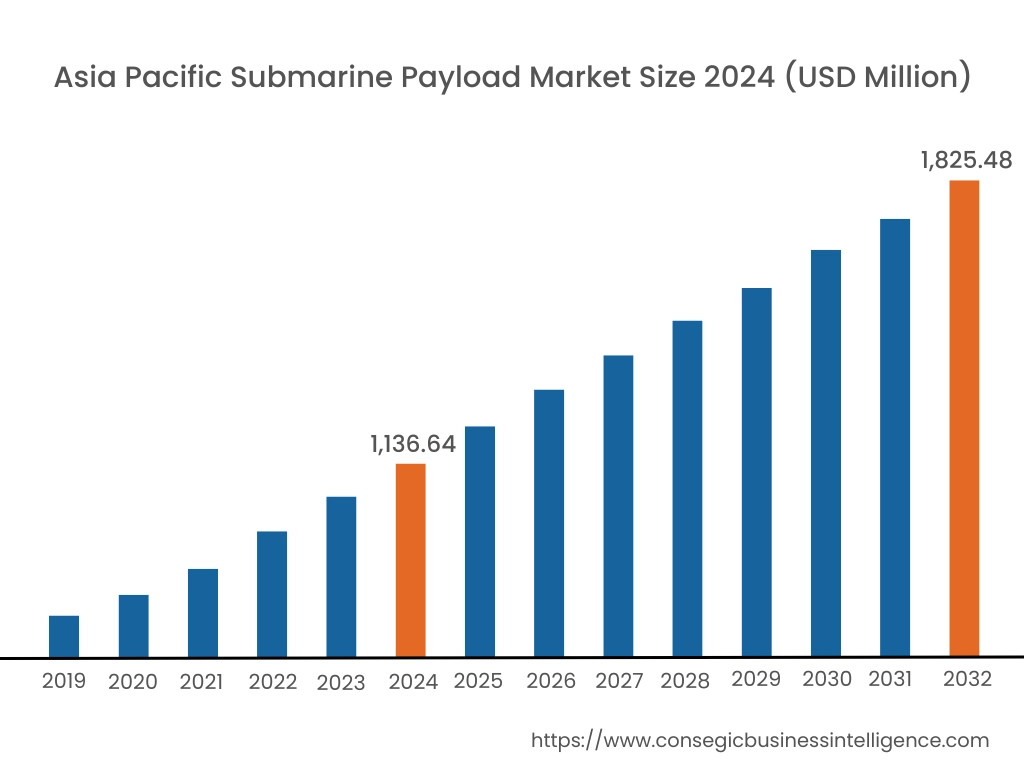

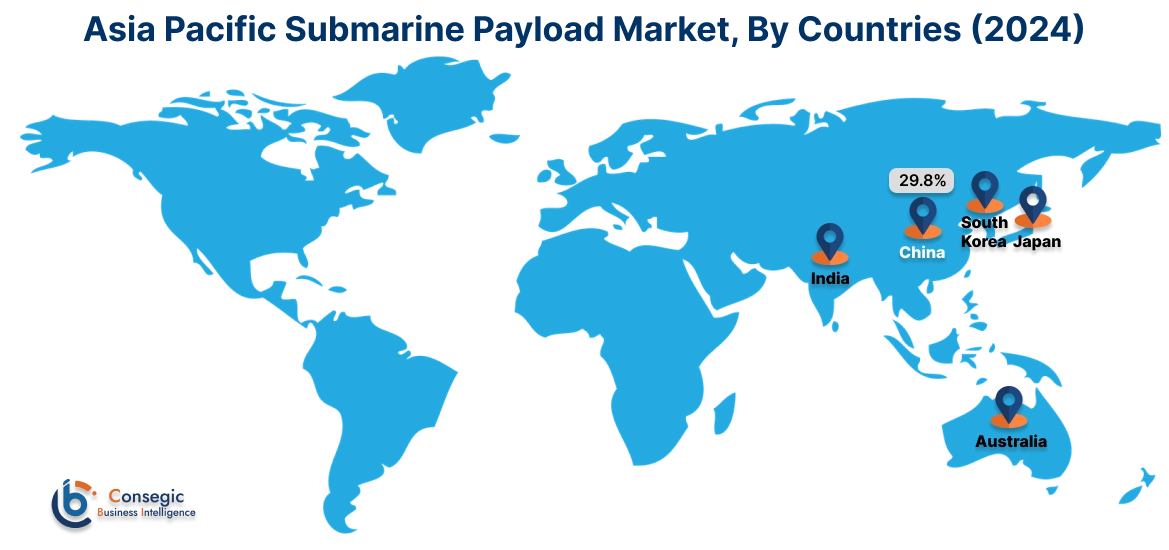

Asia Pacific region was valued at USD 1,136.64 Million in 2024. Moreover, it is projected to grow by USD 1,184.06 Million in 2025 and reach over USD 1,825.48 Million by 2032. Out of this, China accounted for the maximum revenue share of 29.8%. The Asia-Pacific region is witnessing a surge in interest in submarine payload capabilities, driven by regional security concerns and the desire to enhance naval power. Countries such as China, India, and Japan are investing in the development and deployment of indigenous payload systems, including advanced torpedoes, cruise missiles, and intelligence, surveillance, and reconnaissance (ISR) equipment. A prominent trend is the focus on extending operational range and improving payload versatility to address diverse maritime challenges. Analysis suggests that regional tensions and the pursuit of power projection are key factors influencing the submarine payload market opportunities in this area.

North America is estimated to reach over USD 1,942.99 Million by 2032 from a value of USD 1,280.21 Million in 2024 and is projected to grow by USD 1,327.32 Million in 2025. This region commands a significant share of the submarine payload market, primarily due to substantial investments in naval modernization and the presence of leading defense contractors. The United States, in particular, focuses on enhancing its underwater combat capabilities by integrating advanced payloads such as sophisticated sonar systems, unmanned underwater vehicles (UUVs), and advanced communication modules. A notable trend is the emphasis on developing stealth technologies to maintain underwater superiority. Analysis indicates that ongoing research and development efforts, coupled with strategic defense initiatives, continue to drive submarine payload market expansion in this region.

European nations, including the United Kingdom, France, and Germany, are actively investing in submarine payload technologies to bolster their naval capabilities. The region's focus on maintaining a credible deterrent force has led to the adoption of advanced payloads such as missile systems, electronic warfare suites, and enhanced surveillance equipment. A significant trend is the collaboration among European defense contractors to develop next-generation payload technologies, enhancing interoperability and strategic reach.

In the Middle East and Africa, there is a growth in recognition of the strategic importance of submarine payload systems for national defense. Nations are exploring the acquisition of such capabilities to enhance their deterrence posture amidst regional conflicts and security challenges. A notable trend is the interest in procuring advanced payload technologies through international partnerships and defense collaborations.

Latin American countries are gradually exploring the development of submarine payload capabilities to strengthen their naval forces. As per the submarine payload market trends, the focus on modernizing military assets has led to interest in acquiring advanced payload systems, including modern sonar arrays and weaponry. A significant trend is the collaboration with international defense firms to enhance technological expertise and operational readiness.

Top Key Players and Market Share Insights:

The Submarine Payload market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Submarine Payload market. Key players in the Submarine Payload industry include -

- BAE Systems (UK)

- Lockheed Martin Corporation (USA)

- Saab AB (Sweden)

- L3Harris Technologies, Inc. (USA)

- Kongsberg Gruppen (Norway)

- Northrop Grumman Corporation (USA)

- Raytheon Technologies Corporation (USA)

- Thales Group (France)

- General Dynamics Corporation (USA)

- Leonardo S.p.A. (Italy)

Submarine Payload Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5,995.02 Million |

| CAGR (2025-2032) | 5.7% |

| By Payload Type |

|

| By Submarine Type |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Submarine Payload Market? +

The Submarine Payload Market size is estimated to reach over USD 5,995.02 Million by 2032 from a value of USD 3,859.45 Million in 2024 and is projected to grow by USD 4,009.13 Million in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

What are the key segments in the Submarine Payload Market? +

The market is segmented by payload type (torpedoes, missiles, mines, unmanned underwater vehicles (UUVs), and sensors & surveillance systems), submarine type (nuclear-powered attack, AIP, diesel-electric, ballistic missile), and end-use (military, civilian).

Which segment is expected to grow the fastest in the Submarine Payload Market? +

The unmanned underwater vehicles (UUVs) segment is expected to register the fastest CAGR during the forecast period, driven by their increasing adoption in military and civilian applications for reconnaissance, mine detection, and underwater mapping.

Who are the major players in the Submarine Payload Market? +

Major players in the Submarine Payload Market include BAE Systems (UK), Lockheed Martin Corporation (USA), Northrop Grumman Corporation (USA), Raytheon Technologies Corporation (USA), Thales Group (France), General Dynamics Corporation (USA), Leonardo S.p.A. (Italy), Saab AB (Sweden), L3Harris Technologies, Inc. (USA), and Kongsberg Gruppen (Norway).