- Summary

- Table Of Content

- Methodology

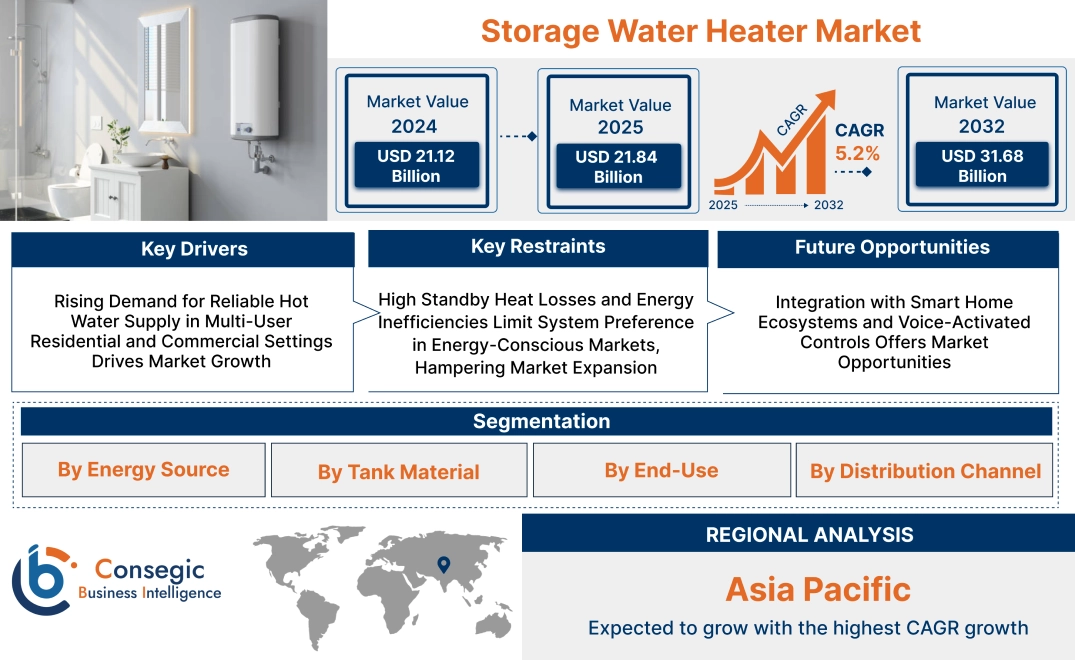

Storage Water Heater Market Size:

Storage Water Heater Market size is estimated to reach over USD 31.68 Billion by 2032 from a value of USD 21.12 Billion in 2024 and is projected to grow by USD 21.84 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

Storage Water Heater Market Scope & Overview:

The storage water heater is a conventional hot water solution which operates by heating and storing water in an insulated tank for later use. It is widely applied in residential, commercial, and hospitality settings where consistent and on-demand hot water is necessary.

The system includes a heating element or burner, thermostat, pressure-relief valve, and corrosion-resistant tank lining. These heaters are available in a range of capacities and fuel types, including electric, gas, and solar-assisted models, allowing users to match system size with consumption needs.

Key advantages include predictable hot water supply, ease of installation, and compatibility with existing plumbing infrastructure. Some models also incorporate digital controls, energy-efficient insulation, and anti-scale technologies. Storage water heater units are valued for their reliability, steady performance, and ability to serve multiple fixtures simultaneously, making them a dependable choice for environments requiring simple yet effective hot water delivery.

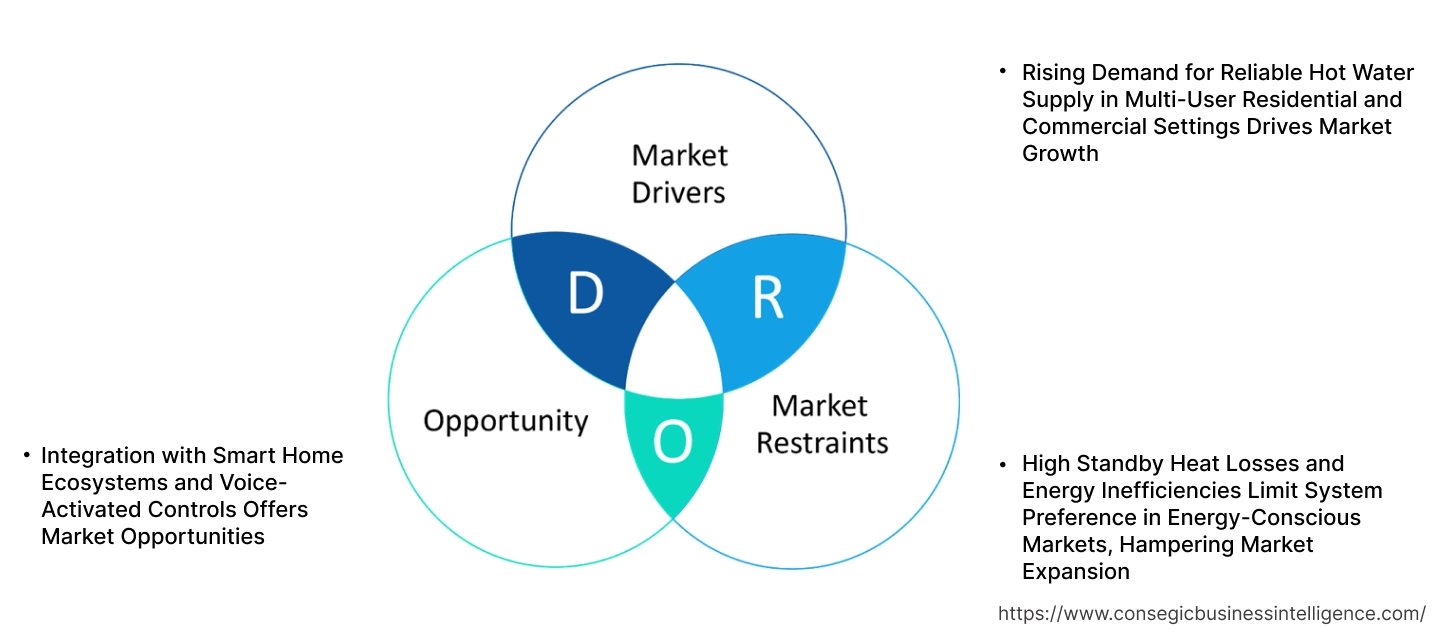

Storage Water Heater Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Reliable Hot Water Supply in Multi-User Residential and Commercial Settings Drives Market Growth

In multi-occupancy residential complexes, hospitals, and hotels, uninterrupted access to hot water is essential for hygiene, comfort, and operational continuity. Storage water heaters provide a dependable solution by maintaining a reserve of pre-heated water ready for use, even during high-demand periods. These systems are particularly valuable in regions with fluctuating water pressure or where simultaneous usage across several fixtures is common. Builders and facility managers prefer storage-based units in environments where performance consistency and volume delivery matter more than compactness or instant heating. Additionally, their straightforward maintenance and relatively low initial cost make them suitable for institutional installations. As urban development expands and the requirement for multi-point hot water systems grows, adoption of bulk-capacity water heaters continues to rise, supporting long-term storage water heater market expansion.

Key Restraints:

High Standby Heat Losses and Energy Inefficiencies Limit System Preference in Energy-Conscious Markets, Hampering Market Expansion

Storage-based systems continuously maintain water temperature, which results in thermal losses over time, especially when insulation is inadequate or tank materials degrade. This leads to higher standby energy consumption and reduced system efficiency, particularly when usage patterns are irregular. In energy-conscious markets where consumers actively track monthly consumption or where government regulations incentivize low-energy appliances, this inefficiency becomes a deterrent. Modern buyers increasingly seek alternatives that align with energy-saving goals, shifting interest toward tankless or hybrid systems. While demand for reliable hot water remains strong, performance-related concerns continue to restrain broader product preference, ultimately limiting storage water heater market growth in high-efficiency-focused regions.

Future Opportunities :

Integration with Smart Home Ecosystems and Voice-Activated Controls Offers Market Opportunities

As smart homes become mainstream, consumers are looking for appliances that offer more than just functionality—they expect connectivity, personalization, and seamless integration. Modern storage water heaters are now being developed with features like voice control compatibility, app-based scheduling, and cloud-based diagnostics. These smart features allow users to adjust temperature settings, monitor energy usage, and receive maintenance alerts from their smartphones or smart speakers. The convenience of aligning hot water supply with daily routines—without manual intervention—is increasing appeal in tech-savvy markets. As the requirement for intelligent home solutions grows, manufacturers offering connected water heating systems are gaining a clear competitive edge.

- For instance, in September 2023, Midea introduced the Smart Wi-Fi Storage Water Heaters, which ensure convenience, safety, energy efficiency, and durability. The product line provides remote control via the SmartHome app, intelligent scheduling to customize heating and save energy, voice control through Alexa and Google Home and a 5-star BEE energy rating for an elevated user experience.

This intersection of traditional utility and modern user experience is unlocking fresh storage water heater market opportunities driven by digital lifestyle growth and the necessity for real-time control.

Storage Water Heater Market Segmental Analysis :

By Energy Source:

Based on energy source, the storage water heater market is segmented into electric, gas, solar, hybrid, and others.

The electric segment accounted for the largest revenue share in 2024.

- Electric storage water heaters are popular due to their ease of installation, low initial costs, and compatibility with standard electrical grids.

- These units are suitable for residential and small commercial applications, providing a consistent supply of hot water.

- The segment benefits from advancements in energy-efficient heating elements, which enhance operational efficiency and reduce electricity consumption.

- As per storage water heater market analysis, the widespread adoption of electric models in areas with stable and affordable power supply sustains the segment's dominance.

The solar segment is projected to grow at the fastest CAGR during the forecast period.

- Solar water heaters offer sustainable solutions by harnessing renewable energy from the sun, reducing reliance on grid electricity or gas.

- They are highly popular in regions with abundant sunlight, supported by government incentives for clean energy adoption.

- Technological innovations in solar collectors and storage tank insulation are improving their efficiency and making them more accessible for residential use.

- For instance, in December 2023, Vaysunic unveiled a hybrid photovoltaic water heater that operates using either PV or AC grid power. Available in 100 liters, 150 liters, 200 liters, and 300 liters capacities, the heater is powered by the solar panel on sunny days and AC on rainy days, automatically.

- According to storage water heater market trends, the increasing emphasis on sustainability and carbon reduction drives the need for solar water heating solutions.

By Tank Material:

Based on tank material, the market is segmented into copper, stainless steel, thermoplastic, and others.

The stainless steel segment held the largest storage water heater market share in 2024.

- Stainless steel tanks are preferred for their durability, resistance to corrosion, and longevity, making them ideal for both residential and commercial applications.

- These tanks can withstand high temperatures and pressures, ensuring consistent performance and reducing the need for maintenance.

- The segment's growth is driven by increasing requirement for long-lasting, high-quality water heating systems that offer superior safety.

- As per storage water heater market trends, stainless steel’s versatility and high-performance capabilities keep it as the go-to material for a wide variety of end users.

The thermoplastic segment is expected to register the fastest CAGR during the forecast period.

- Thermoplastic tanks are lightweight, resistant to corrosion, and offer a cost-effective alternative to metal tanks.

- These tanks are becoming increasingly popular in residential applications due to their affordability and ease of manufacturing.

- Their ability to retain heat longer than some metal tanks contributes to their growing need in energy-conscious markets.

- Thus, thermoplastic tanks are gaining traction in both budget-friendly residential installations and high-volume commercial applications, driving storage water heater market growth.

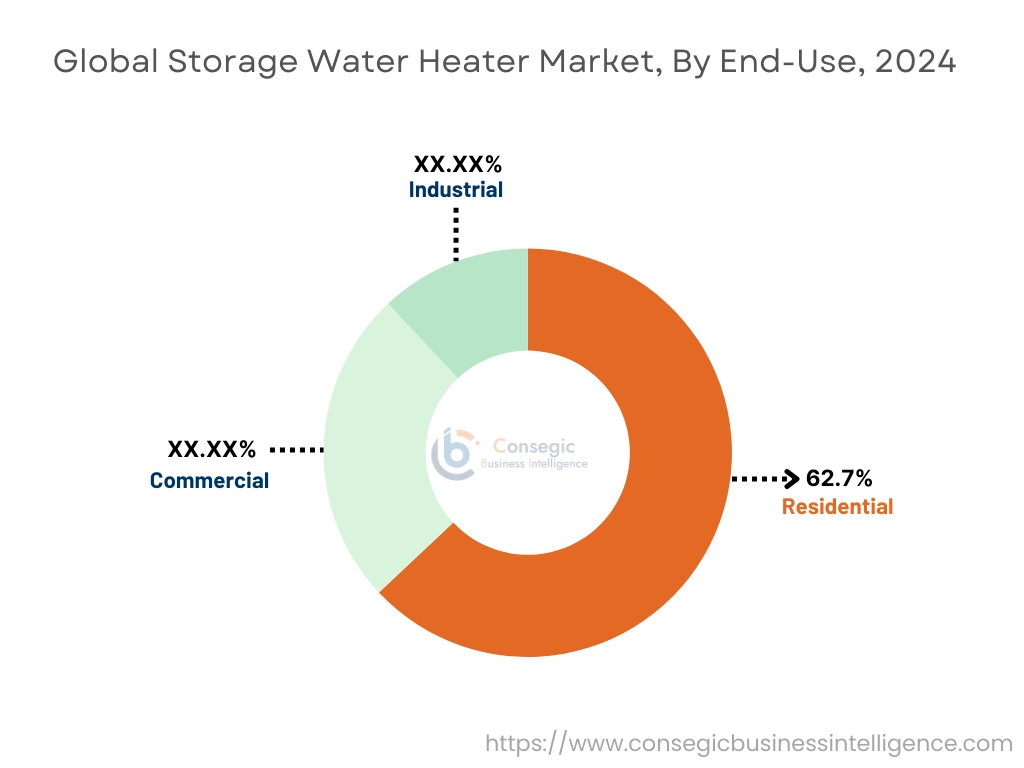

By End-Use:

Based on end-use, the market is segmented into residential, commercial, and industrial.

The residential segment accounted for the largest storage water heater market share of 62.7% in 2024.

- Storage water heaters are essential in homes for providing hot water for daily activities such as bathing, cooking, and cleaning.

- The growing trend of smart homes, where water heating systems are integrated with IoT and energy management systems, drives further adoption.

- Consumer awareness regarding energy-efficient models and the availability of space-saving designs make residential storage water heaters a popular choice.

- As per storage water heater market demand, the continued expansion of residential construction and renovation projects propels this segment's dominance.

The commercial segment is expected to grow at the fastest CAGR during the forecast period.

- Commercial establishments like hotels, hospitals, and restaurants require high-capacity, reliable water heating systems to accommodate high volumes of hot water usage.

- Increasing need for energy-efficient water heating solutions in commercial buildings is driving the segment’s growth.

- Hybrid and solar water heaters are gaining popularity in the commercial sector due to their ability to reduce operational costs while contributing to sustainability goals.

- Hence, commercial building regulations requiring energy-efficient systems and green certifications are boosting the storage water heater market expansion.

By Distribution Channel:

Based on distribution channel, the storage water heater market is segmented into online retail and offline retail (distributors, dealers, OEMs).

The offline retail segment accounted for the largest revenue share in 2024.

- Offline retail channels, including distributors, dealers, and original equipment manufacturers (OEMs), provide essential value-added services such as installation, maintenance, and warranty management.

- Retailers and distributors serve as key touchpoints for customer education, product demonstrations, and after-sales support.

- The physical presence of showrooms and service centers offers a competitive advantage in markets where consumers prefer face-to-face interaction before making significant purchases.

- As per storage water heater market analysis, offline retail continues to dominate due to the importance of installation support and consumer trust.

The online retail segment is projected to witness the fastest CAGR during the forecast period.

- E-commerce platforms offer greater convenience, allowing customers to compare models, prices, and read user reviews before purchasing.

- The growing trend of online home appliance shopping, along with better logistics networks, is making online retail more appealing to consumers.

- Online retailers are increasingly offering direct-to-consumer models, along with installation services bundled with the product.

- For instance, in December 2023, the electronics company GM Modular introduced its first storage water heater R1X in India, which is available for purchase not only in outlets but also on e-commerce platforms like Amazon and Flipkart. With unique hydrodynamic technology, the water heater ensures minimum hot and cold water mixing, providing immense comfort and convenience to users.

- Thus, the rapid adoption of online shopping platforms is reshaping the sales channels, contributing to the storage water heater market demand.

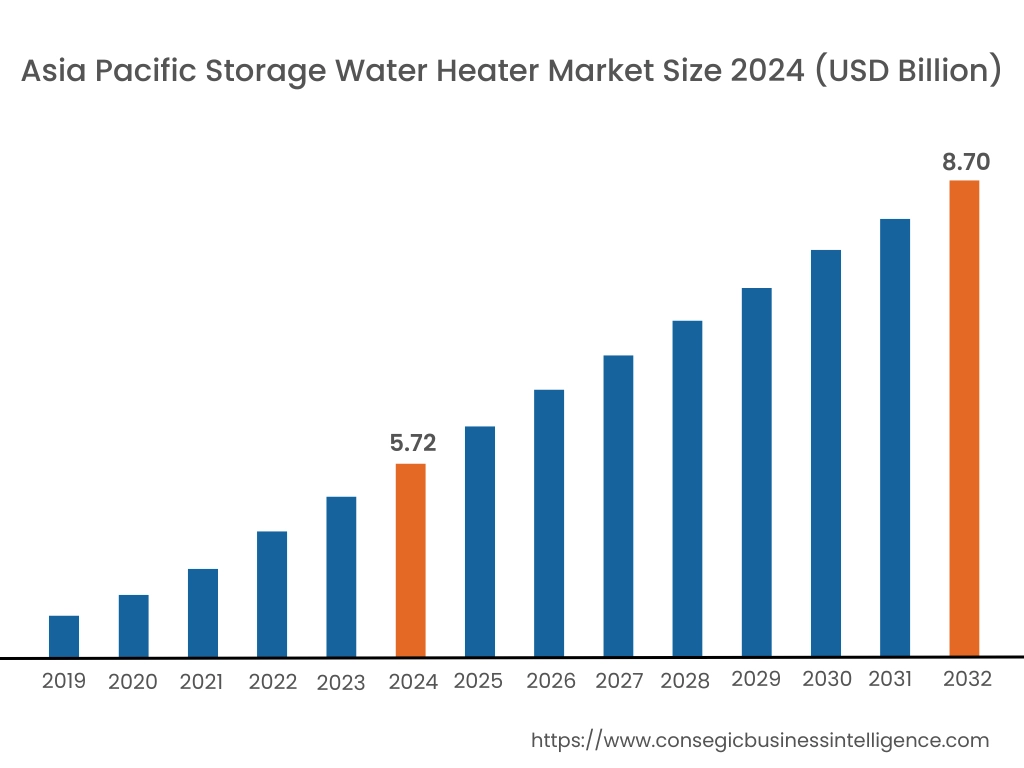

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

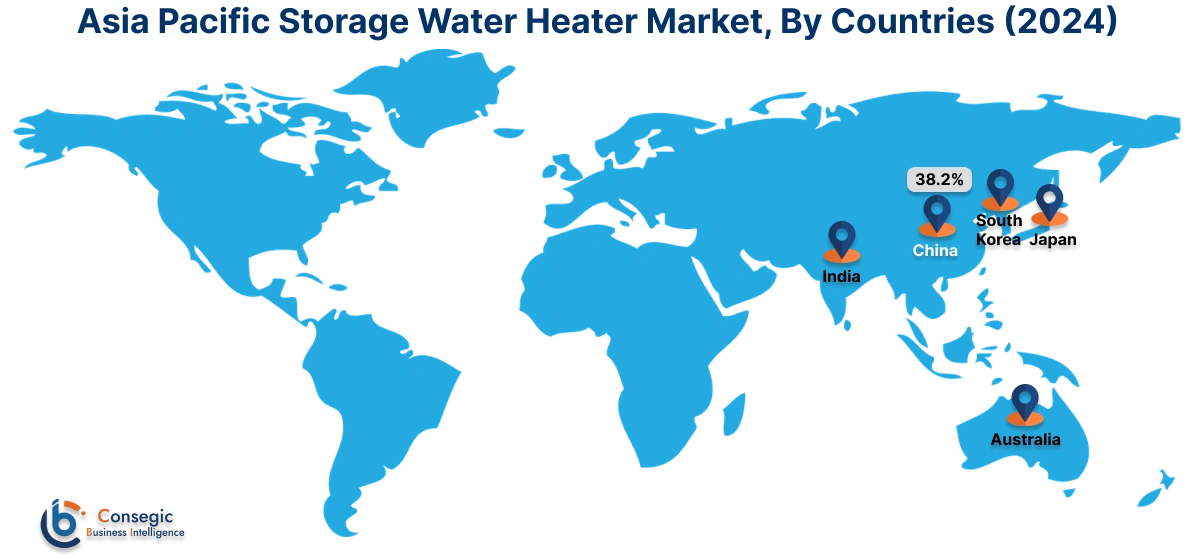

Asia Pacific region was valued at USD 5.72 Billion in 2024. Moreover, it is projected to grow by USD 5.92 Billion in 2025 and reach over USD 8.70 Billion by 2032. Out of this, China accounted for the maximum revenue share of 38.2%. Asia-Pacific is experiencing the fastest growth in the storage water heater industry, fueled by rapid urban development, increasing disposable income, and the electrification of residential infrastructure. In China and India, rising middle-class populations are driving demand for reliable and low-maintenance water heating in apartments and independent homes.

- For instance, in March 2025, Xiaomi launched the Mijia Smart Crystal Dual-Tank Electric Water Heater P10 in China. The heater has a compact and lightweight design for easy installation in different setups. Moreover, the inner polymer tank eliminates the need for magnesium rods, preventing scale buildup and enhancing durability. Furthermore, it can also be operated using the Mijia app remotely.

Market analysis highlights the growing use of vertically mounted tank systems, supported by national programs for energy access and appliance efficiency. In mature markets such as Japan and South Korea, technological innovation is leading to advanced models with multi-mode operation and enhanced safety features. Expansion of smart cities and the rising popularity of green buildings continue to accelerate adoption across the region.

North America is estimated to reach over USD 10.55 Billion by 2032 from a value of USD 7.02 Billion in 2024 and is projected to grow by USD 7.26 Billion in 2025. In North America, particularly in the United States and Canada, the market remains well-established with widespread residential and light commercial installations. Market analysis reveals that growing awareness of energy consumption and utility costs is prompting a transition toward high-efficiency, insulated tank models equipped with smart controls and demand response capabilities. In colder regions, the preference for large-capacity units with hybrid heat pump functionality is increasing. Growth in this region is largely driven by housing renovation trends, the push for decarbonized domestic heating, and rebates offered for ENERGY STAR-rated systems.

Europe represents a highly regulated and innovation-focused market where energy performance directives and carbon reduction targets are reshaping product choices. Countries such as Germany, France, and Italy are increasingly deploying electric and solar-assisted storage systems in multi-dwelling buildings and off-grid homes. Market analysis shows a strong preference for compact, wall-mounted units with rapid reheat functions, especially in densely populated urban areas with limited space. The storage water heater market opportunity in Europe is being strengthened by policy-backed incentives, smart grid integration, and need for systems compatible with low-carbon energy sources such as photovoltaics and district energy.

Latin America presents a steadily growing market, especially in countries such as Brazil, Mexico, and Chile where urban housing construction is gaining momentum. Market analysis indicates that electric tank-type water heaters dominate due to their ease of installation and affordability, particularly in mid-income residential segments. Regional variations in energy cost and availability are influencing a gradual shift toward solar-compatible or time-of-use programmable units. Growth is supported by building code revisions and sustainability efforts, with opportunities emerging in retrofitting older homes and supplying equipment to expanding hospitality and healthcare sectors.

In the Middle East and Africa, adoption is increasing at a gradual pace, primarily driven by infrastructure development and rising need for domestic comfort systems. In the Gulf countries, high-rise residential and hospitality developments are installing centralized storage heating units, often integrated with solar thermal systems. Market analysis also points to growing deployment in South Africa and Egypt, where the reliability of hot water access and energy resilience are critical. The region benefits from growing construction activity, donor-backed electrification programs, and rising consumer preference for durable, long-lasting products in both urban and rural settings.

Top Key Players and Market Share Insights:

The storage water heater market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global storage water heater market. Key players in the storage water heater industry include -

- Ariston Thermo Group (Italy)

- Bosch Thermotechnology (Germany)

- Bajaj Electricals Ltd. (India)

- Havells India Limited (India)

- Groupe Atlantic (France)

- Rinnai Corporation (Japan)

- Haier Group Corporation (China)

- Viessmann Group (Germany)

- Vaillant Group (Germany)

- Ferroli S.p.A. (Italy)

Recent Industry Developments :

Acquisitions:

- In April 2025, Bradford White Corporation, a leading provider of water heating solutions, acquired Bock Water Heaters. The companies have had a longstanding relationship extending back to three decades, with Bock serving as both an important supplier and a valued customer, enabling a natural evolution through this acquisition.

Storage Water Heater Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 31.68 Billion |

| CAGR (2025-2032) | 5.2% |

| By Energy Source |

|

| By Tank Material |

|

| By End-Use |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Storage Water Heater Market? +

Storage Water Heater Market size is estimated to reach over USD 31.68 Billion by 2032 from a value of USD 21.12 Billion in 2024 and is projected to grow by USD 21.84 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

What specific segmentation details are covered in the Storage Water Heater Market report? +

The Storage Water Heater market report includes specific segmentation details for energy source, tank material, end-use and distribution channel.

What are the end-use of the Storage Water Heater Market? +

The end-use of the Storage Water Heater Market are residential, commercial, and industrial.

Who are the major players in the Storage Water Heater Market? +

The key participants in the Storage Water Heater market are Ariston Thermo Group (Italy), Bosch Thermotechnology (Germany), Rinnai Corporation (Japan), Haier Group Corporation (China), Viessmann Group (Germany), Vaillant Group (Germany), Ferroli S.p.A. (Italy), Bajaj Electricals Ltd. (India), Havells India Limited (India) and Groupe Atlantic (France).