- Summary

- Table Of Content

- Methodology

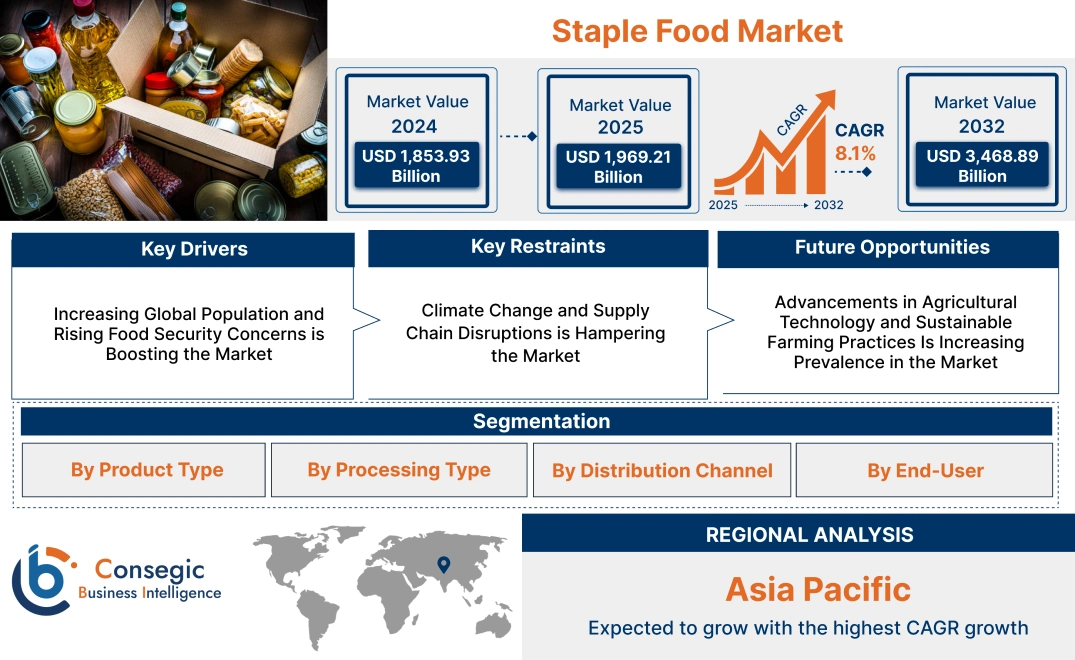

Staple Food Market Size:

Staple Food Market size is estimated to reach over USD 3,468.89 Billion by 2032 from a value of USD 1,853.93 Billion in 2024 and is projected to grow by USD 1,969.21 Billion in 2025, growing at a CAGR of 8.1% from 2025 to 2032.

Staple Food Market Scope & Overview:

The staple food industry focuses on essential food products that serve as primary sources of nutrition and energy in daily diets worldwide. These foods, which include grains (wheat, rice, maize), tubers (potatoes, cassava), legumes (beans, lentils), and staple proteins (dairy, fish, meat), are fundamental to food security and economic stability. The industry encompasses production, processing, packaging, and distribution to ensure a steady supply for both developed and developing regions.

Key characteristics of these foods include high caloric value, long shelf life, and widespread availability, making them critical for meeting global dietary needs. The benefits include affordability, nutritional sustenance, and their role in supporting agricultural economies.

Applications span household consumption, food manufacturing, institutional food programs, and humanitarian aid efforts. End-users include consumers, food processors, retailers, and government agencies, driven by population, evolving dietary patterns, advancements in food preservation technologies, and increasing government initiatives to ensure food security.

Staple Food Market Dynamics - (DRO) :

Key Drivers:

Increasing Global Population and Rising Food Security Concerns is Boosting the Market

The demand for staple foods continues to rise due to the growing global population and increasing focus on food security. Foods including rice, wheat, maize, and potatoes, serve as the primary source of nutrition for billions of people worldwide. Rapid urbanization and economic growth in developing nations have further driven surge, as changing dietary patterns and income levels influence food consumption trends. Additionally, government initiatives promoting agricultural productivity and food distribution programs have strengthened the staple food supply chain, ensuring greater accessibility to essential food products in both rural and urban areas.

Key Restraints:

Climate Change and Supply Chain Disruptions is Hampering the Market

A significant challenge facing the market is the impact of climate change on agricultural production. Extreme weather conditions, including droughts, floods, and temperature fluctuations, directly affect crop yields, leading to price volatility and potential shortages. Additionally, supply chain disruptions, such as transportation bottlenecks and geopolitical conflicts, further strain global food availability. Rising input costs, including fertilizers, seeds, and irrigation expenses, also contribute to higher staple food prices, posing affordability challenges in low-income regions and affecting overall market stability.

Future Opportunities:

Advancements in Agricultural Technology and Sustainable Farming Practices Is Increasing Prevalence in the Market

Innovations in agricultural technology and the adoption of sustainable farming practices present significant opportunities for the market. Trends such as precision farming, genetically modified (GM) crops, and vertical farming are improving crop resilience, optimizing yield, and reducing environmental impact. Additionally, investments in climate-smart agriculture and regenerative farming techniques are helping to combat soil degradation and water scarcity, ensuring long-term sustainability in staple food production. Governments and agribusinesses focusing on food fortification and nutrient-rich staple varieties are also creating new opportunities for enhancing global food security.

These market dynamics highlight the growing staple food market demand amid rising population needs and food security concerns. While challenges such as climate change and supply chain issues pose risks, trends in agricultural innovation and sustainable farming offer promising pathways for ensuring stable and efficient food production worldwide.

Staple Food Market Segmental Analysis :

By Product Type:

Based on product type, the market is segmented into grains & cereals, pulses & legumes, vegetables & tubers, meat & seafood, dairy products, and oils & fats.

The grains & cereals segment accounted for the largest revenue of staple food market share in 2024.

- Grains and cereals, including rice, wheat, and maize, form the foundation of global diets and are consumed in large quantities.

- Increasing staple food market opportunities for whole grains and fortified cereals due to rising health awareness supports expansion.

- Government initiatives promoting food security and sustainable grain production further enhance growth.

- Advancements in packaging and storage technologies improve shelf life and global distribution efficiency.

The meat & seafood segment is anticipated to register the fastest CAGR during the forecast period.

- Growing consumer preference for protein-rich diets and increasing urbanization drive demand for meat and seafood.

- Rising adoption of frozen and processed meat products in fast-paced urban lifestyles supports staple food market expansion.

- Technological advancements in cold chain logistics improve the availability and quality of meat and seafood.

- Expanding international trade and exports of seafood contribute to increased consumption across regions.

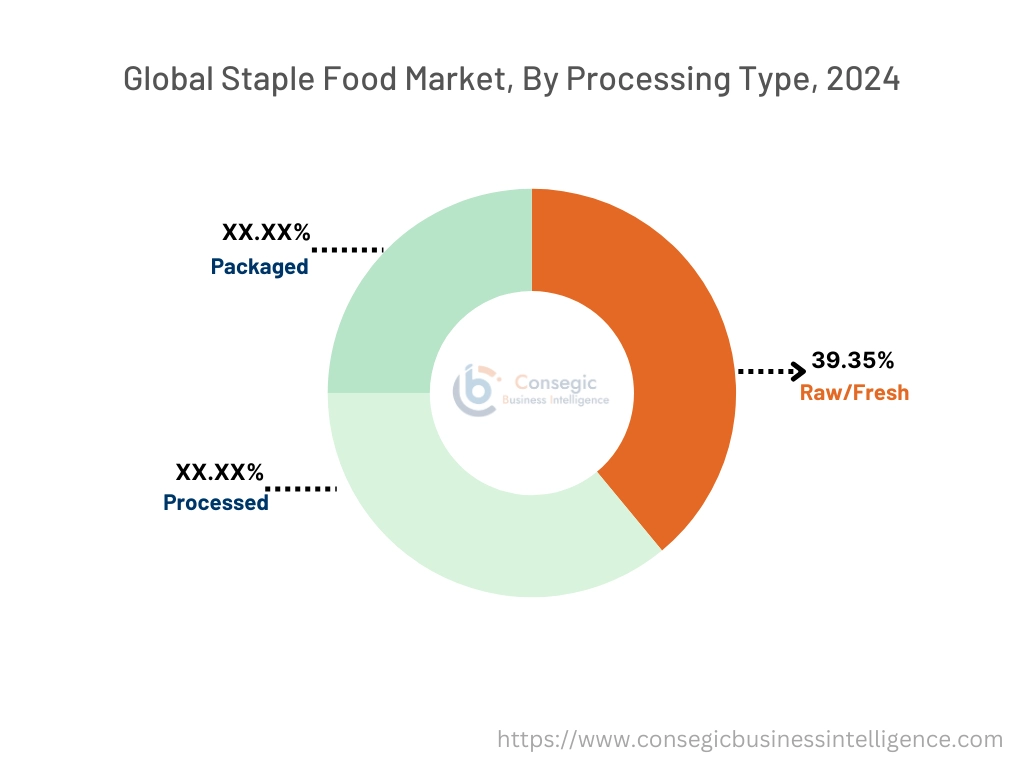

By Processing Type:

Based on processing type, the market is segmented into raw/fresh, processed, and packaged.

The raw/fresh segment accounted for the largest revenue share of 39.35% in 2024.

- Raw and fresh staple foods, including grains, vegetables, and dairy, remain a primary choice for consumers due to their nutritional value.

- Rising consumer awareness regarding organic and farm-fresh products supports staple food market trends in this segment.

- Government efforts promoting local farming and fresh food markets enhance accessibility.

- Increasing preference for fresh, minimally processed foods among health-conscious consumers strengthens staple food market growth.

The packaged segment is anticipated to register the fastest CAGR during the forecast period.

- Growing urbanization and changing consumer lifestyles favor the convenience of packaged staple foods.

- Advancements in food preservation techniques, including vacuum-sealing and modified atmosphere packaging, extend product shelf life.

- The staple food market expansion of e-commerce and online grocery platforms boosts accessibility to packaged staple foods.

- Rising trends for ready-to-cook and pre-packaged food products among working professionals drive market progress.

By Distribution Channel:

Based on distribution channel, the market is segmented into supermarkets & hypermarkets, convenience stores, online retail, specialty stores, and wholesale & bulk suppliers.

The supermarkets & hypermarkets segment accounted for the largest revenue of staple food market share in 2024.

- Supermarkets and hypermarkets offer a wide range of staple food products with bulk purchasing options, driving consumer preference.

- Increasing investments in retail infrastructure and enlargement of supermarket chains in emerging economies support the rise.

- Availability of multiple brands, discounts, and promotional offers enhances customer engagement.

- Rising adoption of in-store digital technologies, such as smart checkout systems and digital labeling, improves shopping experiences.

The online retail segment is anticipated to register the fastest CAGR during the forecast period.

- The rise of e-commerce and home delivery services fuels staple food market demand through online platforms.

- Increasing consumer preference for digital grocery shopping, driven by convenience and price competitiveness, supports advancement.

- Extension of online grocery delivery services, including subscription-based models, enhances accessibility.

- Integration of AI-driven recommendations and contactless payment solutions further boosts online sales.

By End-User:

Based on end-user, the market is segmented into households, food service industry, and food processing industry.

The households segment accounted for the largest revenue share in 2024.

- Households form the primary consumer base for staple foods, driven by daily consumption of grains, dairy, and vegetables.

- Increasing disposable incomes and rising focus on healthy eating habits contribute to demand.

- Growing awareness about food security and sustainable sourcing influences household purchasing decisions.

- The spreading of home meal preparation trends, including organic and farm-to-table cooking, supports segment analysis.

The food service industry segment is anticipated to register the fastest CAGR during the forecast period.

- Growing staple food market trends for quick-service restaurants (QSRs), fine dining, and cloud kitchens accelerate staple food consumption.

- Enlargement in global fast-food chains and international cuisine trends increases reliance on staple food ingredients.

- Increasing adoption of bulk purchasing models and direct supplier partnerships optimizes costs for food service providers.

- Rising consumer preference for healthy menu options, including plant-based and whole-food offerings, supports market surge.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

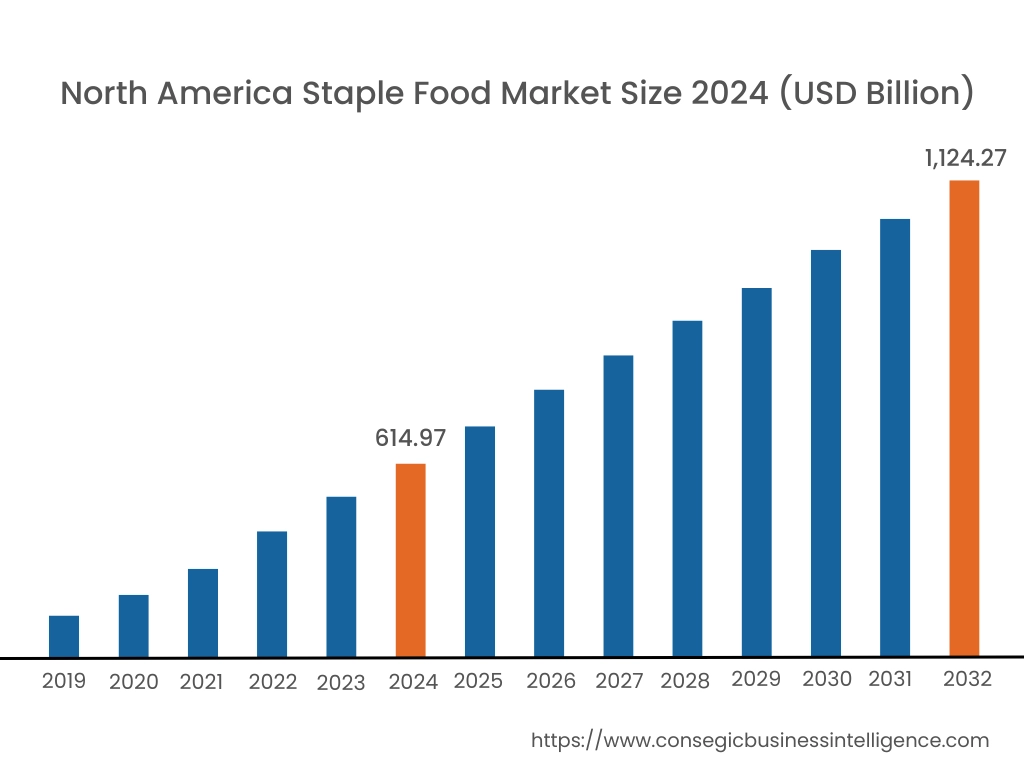

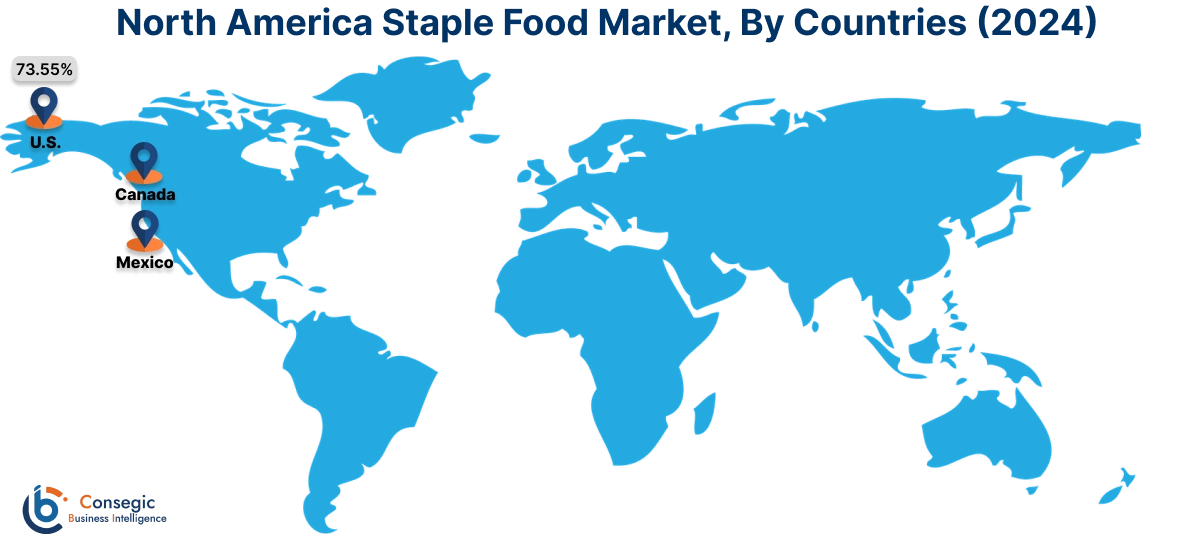

In 2024, North America was valued at USD 614.97 Billion and is expected to reach USD 1,124.27 Billion in 2032. In North America, the U.S. accounted for the highest share of 73.55% during the base year of 2024. North America holds a significant share in the global staple food market, driven by the large consumption of grains, dairy, and processed staple products. The U.S. leads the region with high rise for wheat, corn, and rice-based products, supported by advanced food processing industries and a strong retail distribution network. Canada contributes to market expansion with increasing consumption of these foods like potatoes, dairy, and pulses, alongside a growing preference for organic and minimally processed staples. Analysis highlights that the region's evolving dietary habits and the rising trends for gluten-free and plant-based staple alternatives are influencing market growth.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 8.6% over the forecast period. The staple food market is fueled by rapid population rise, increasing urbanization, and rising appeals for rice, wheat, and pulses in China, India, and Japan. China dominates the region with large-scale production and consumption of rice and wheat-based staple products, alongside increasing advancement for fortified foods. India’s market enlargement is driven by the high consumption of grains, lentils, and dairy, with a growing emphasis on improving food security and nutritional programs. Japan prioritizes rice-based foods and fortified food products, leveraging advanced food processing techniques. Analysis indicates that government efforts to enhance food supply chains and ensure affordability are major factors influencing regional staple food market growth.

Europe is a key market, supported by a strong agricultural sector, well-established food supply chains, and increasing consumer preference for organic and locally sourced staples. Countries like Germany, the UK, and France are major contributors. Germany drives surge with its high consumption of bread, dairy, and cereal products, while the UK emphasizes whole grains and fortified staple foods due to rising health consciousness. France focuses on traditional foods such as bread, rice, and dairy, supported by government initiatives promoting food security. Analysis suggests that sustainability concerns and regulatory measures on food production are shaping the staple food industry across the region.

The Middle East & Africa region is witnessing steady growth in the staple market, driven by increasing food imports, population rise, and government-led food security initiatives. Countries like Saudi Arabia and the UAE rely on staple food imports such as wheat, rice, and dairy, with a focus on improving local agricultural production. In Africa, South Africa is emerging as a key market, with rising demand for maize, sorghum, and dairy as staple food products. The regional staple food market analysis highlights challenges such as price fluctuations, climate impact on food production, and limited access to high-quality food sources in certain areas.

Latin America is an emerging market with Brazil and Mexico leading the region. Brazil’s staple food market is driven by high consumption of rice, beans, and cassava, supported by a strong agricultural base. Mexico focuses on maize-based foods, such as tortillas, alongside increasing demand for wheat and dairy products. The staple food market analysis reveals that economic shifts and changing dietary preferences toward protein-rich and fortified staple foods are influencing market expansion. However, economic instability and supply chain disruptions in some countries may impact accessibility and affordability.

Top Key Players and Market Share Insights:

The staple food market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global staple food market. Key players in the staple food industry include-

- Nestlé S.A. (Switzerland)

- Cargill, Incorporated (USA)

- Archer Daniels Midland Company (ADM) (USA)

- General Mills, Inc. (USA)

- Kraft Heinz Company (USA)

- Unilever PLC (UK/Netherlands)

- Associated British Foods PLC (UK)

- PepsiCo, Inc. (USA)

- Tyson Foods, Inc. (USA)

- Bunge Limited (USA)

Staple Food Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,468.89 Billion |

| CAGR (2025-2032) | 8.1% |

| By Product Type |

|

| By Processing Type |

|

| By Distribution Channel |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the expected size of the Staple Food Market by 2032? +

Staple Food Market size is estimated to reach over USD 3,468.89 Billion by 2032 from a value of USD 1,853.93 Billion in 2024 and is projected to grow by USD 1,969.21 Billion in 2025, growing at a CAGR of 8.1% from 2025 to 2032.

What factors are driving the growth of the staple food market? +

The market is driven by rising global population, increasing food security concerns, government initiatives to enhance agricultural productivity, and changing dietary patterns in urbanizing economies.

Which segment holds the largest share in the market? +

The grains & cereals segment dominates the market, as rice, wheat, and maize are widely consumed staple foods worldwide.

Which region is expected to grow the fastest? +

The Asia Pacific region is anticipated to grow at the highest CAGR due to rapid urbanization, high demand for staple grains, and government initiatives supporting food security.

Who are the major players in the staple food industry? +

Key players include Nestlé S.A. (Switzerland), Cargill, Incorporated (USA), Archer Daniels Midland Company (USA), General Mills, Inc. (USA), Kraft Heinz Company (USA), Unilever PLC (UK/Netherlands), and PepsiCo, Inc. (USA).