- Summary

- Table Of Content

- Methodology

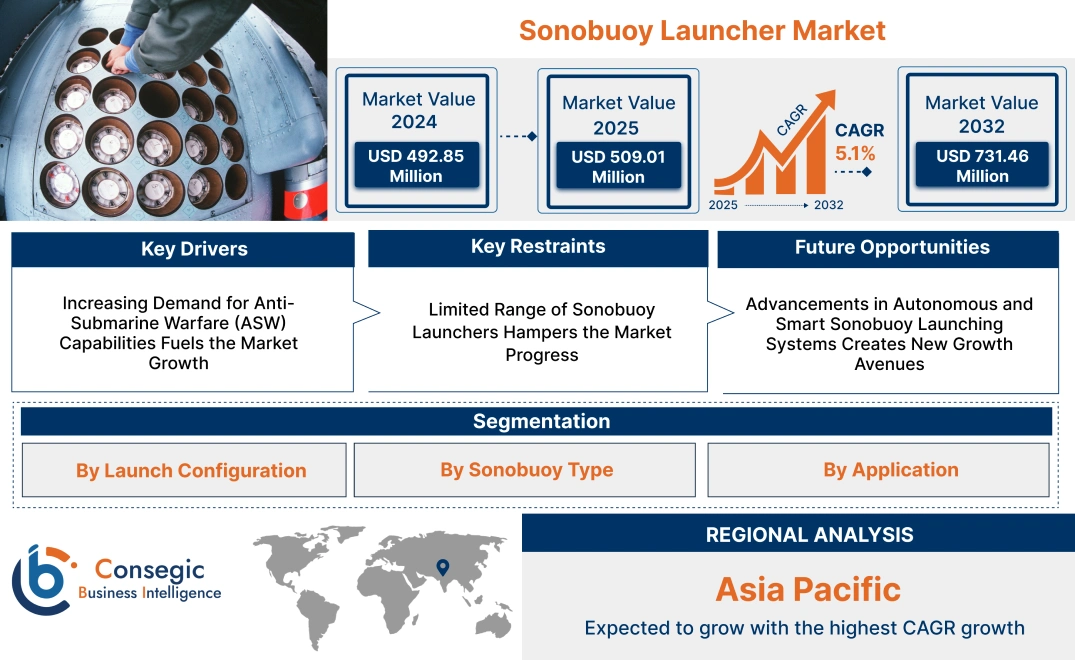

Sonobuoy Launcher Market Size:

Sonobuoy Launcher Market size is estimated to reach over USD 731.46 Million by 2032 from a value of USD 492.85 Million in 2024 and is projected to grow by USD 509.01 Million in 2025, growing at a CAGR of 5.1% from 2025 to 2032.

Sonobuoy Launcher Market Scope & Overview:

A sonobuoy launcher is a specialized system designed to deploy sonobuoys, which are used for detecting and tracking underwater objects such as submarines. These launchers are integral to anti-submarine warfare (ASW) and oceanographic research, enabling precise deployment of sonobuoys from aircraft or naval vessels. They ensure accurate positioning and optimal performance of sonobuoys in various operational conditions.

These launchers are available in both pneumatic and cartridge-actuated designs, catering to different platform requirements. They are engineered for reliability and ease of use, offering automated and manual deployment options. These systems are compatible with multiple types of sonobuoys, including passive, active, and special-purpose variants, ensuring versatility in ASW and research industry applications.

End-users include naval forces, defense organizations, and research institutions that rely on these systems for enhanced underwater monitoring and threat detection capabilities. Sonobuoy launchers play a critical role in supporting maritime security and advancing oceanographic studies.

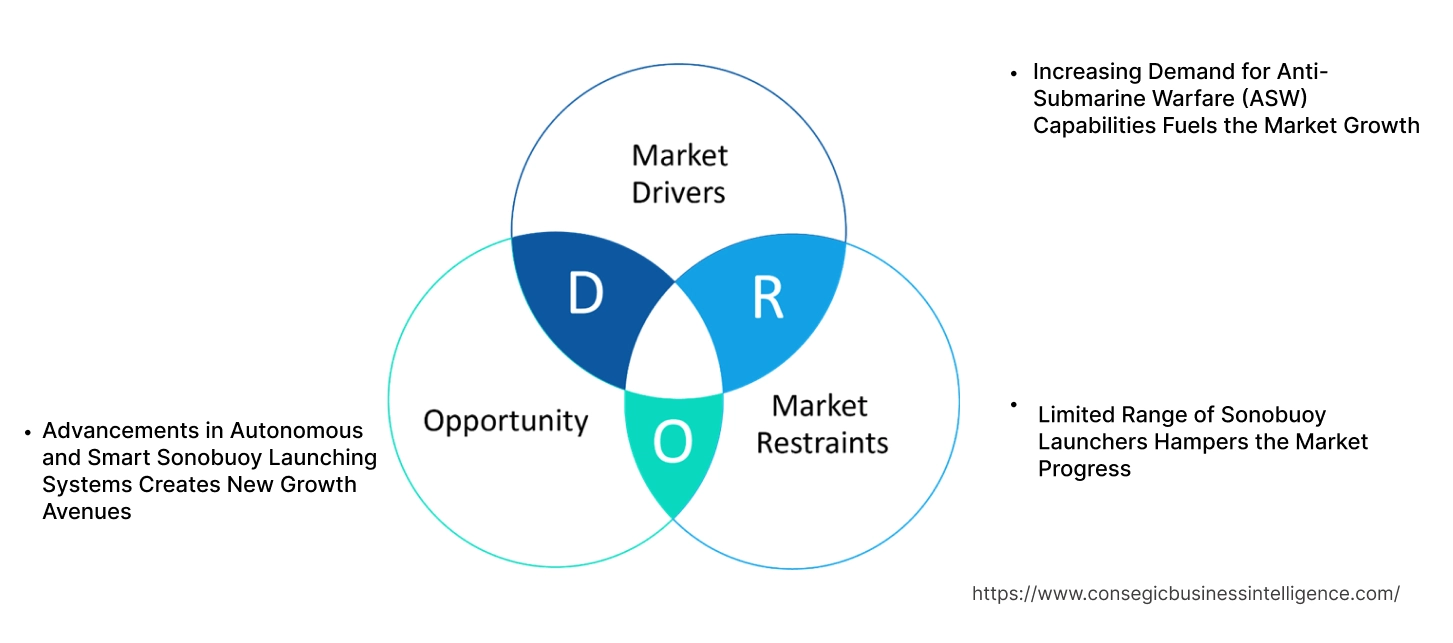

Sonobuoy Launcher Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Anti-Submarine Warfare (ASW) Capabilities Fuels the Market Growth

As submarine threats evolve and become more sophisticated, naval forces worldwide are modernizing their Anti-Submarine Warfare capabilities to detect, track, and neutralize these threats. Sonobuoys play a critical role in this process by providing sonar capabilities to detect submarines across vast oceanic areas. These buoy-based sensors are dropped into the water and relay sonar data back to naval platforms, enabling real-time detection and analysis. As the need for enhanced maritime security intensifies, especially in strategic regions, the demand for efficient and reliable sonobuoy launchers increases. These launchers are essential for deploying sonobuoys quickly and accurately, boosting the effectiveness of ASW operations. The modernization of naval fleets and the integration of more advanced sonar systems further drives the sonobuoy launcher market demand, making them indispensable for ASW missions.

Key Restraints:

Limited Range of Sonobuoy Launchers Hampers the Market Progress

A significant restraint for the launcher is the limited range at which these systems effectively deploy and operate. The range of sonobuoy deployment is often constrained by the size and capacity of the launchers, as well as the effectiveness of sonar signals over long distances. In large oceanic areas, sonobuoys struggle to provide comprehensive coverage, limiting their ability to detect and track submarines in remote or deep-water regions. Additionally, harsh environmental conditions, such as strong currents and underwater topography, reduce the operational range of sonobuoys, affecting the overall efficiency of the system. As a result, navies need to deploy multiple launchers or reposition their platforms frequently, which increases operational costs and complexity. These limitations hinder the ability to monitor vast areas continuously, making the performance of sonobuoy launchers less effective in some strategic operations. Therefore, the aforementioned factors are limiting the sonobuoy launcher market growth.

Future Opportunities :

Advancements in Autonomous and Smart Sonobuoy Launching Systems Creates New Growth Avenues

The development of autonomous and smart sonobuoy launching systems presents a significant opportunity to enhance operational efficiency and reduce human intervention in anti-submarine warfare (ASW) operations. These advanced systems automatically deploy sonobuoys and adjust their placement based on real-time data, such as environmental conditions and mission requirements. By integrating sensors, AI algorithms, and predictive analytics, smart launchers are able to optimize the positioning and performance of sonobuoys, improving the accuracy and reliability of submarine detection. Autonomous launchers also reduce the need for manual deployment, decreasing operational costs and the risk of human error. Furthermore, these systems enable more dynamic and responsive ASW operations, as sonobuoys are deployed in real-time based on the evolving situation. The integration of autonomous capabilities into sonobuoy launching systems makes them highly efficient, flexible, and scalable, addressing the growing demand for advanced, automated solutions in naval defense strategies, thereby creating significant sonobuoy launcher market opportunities.

Sonobuoy Launcher Market Segmental Analysis :

By Launch Configuration:

Based on launch configuration, the market is segmented into single launch systems and multiple rotary launch systems.

The multiple rotary launch system segment accounted for the largest revenue of the total sonobuoy launcher market share in 2024.

- These systems enable rapid deployment of multiple sonobuoys, making them essential for large-scale maritime operations.

- Their compatibility with advanced naval platforms enhances efficiency in anti-submarine warfare and surveillance missions.

- Increasing adoption by military forces worldwide highlights their importance in modern naval strategies.

- As per sonobuoy launcher market analysis, their dominance is attributed to their ability to handle complex maritime challenges effectively.

The single launch system segment is expected to register the fastest CAGR during the forecast period.

- Single launch systems are favored for targeted deployments in specific areas, ensuring precision and cost-effectiveness.

- They are widely used in scientific research and environmental monitoring applications.

- The compact design and operational simplicity make them ideal for smaller naval platforms.

- Thus, as per the market trends, increasing demand for customized and focused maritime operations supports the segment’s growth trajectory, further contributing to the sonobuoy launcher market expansion.

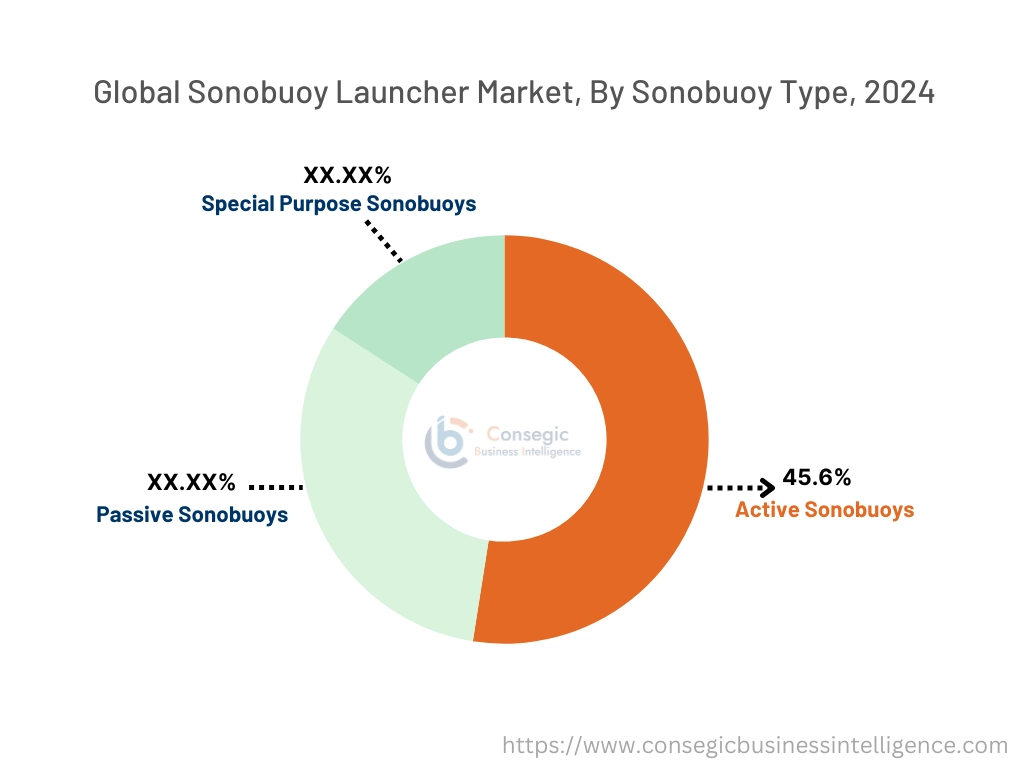

By Sonobuoy Type:

Based on sonobuoy type, the market is categorized into active sonobuoys, passive sonobuoys, and special purpose sonobuoys.

The active sonobuoys segment accounted for the largest revenue of 45.6% of the total sonobuoy launcher market share in 2024.

- These sonobuoys actively emit signals to detect underwater objects, making them crucial for anti-submarine warfare.

- Their ability to cover large detection ranges ensures enhanced operational capabilities for military forces.

- Advanced technological features, such as enhanced signal processing, contribute to their widespread adoption.

- As per the sonobuoy launcher market trends, the segment's dominance reflects the growing emphasis on proactive maritime threat detection and response.

The passive sonobuoys segment is expected to register the fastest CAGR during the forecast period.

- Passive sonobuoys rely on detecting sound waves, making them stealthier and energy-efficient.

- Their deployment in both military and commercial applications, such as underwater acoustic studies, drives demand.

- Increasing investments in environmental monitoring and scientific research contribute to their growing popularity.

- The segment benefits from technological advancements improving signal accuracy and reliability, fueling the sonobuoy launcher market growth.

By Application:

Based on application, the market is divided into anti-submarine warfare, maritime surveillance, search & rescue, scientific research, and others.

The anti-submarine warfare segment held the largest revenue share in 2024.

- The rising focus on underwater threat detection and neutralization drives the need for advanced sonobuoy systems.

- The integration of sonobuoy launchers with naval fleets enhances operational readiness against submarine threats.

- Increased defense budgets and maritime security initiatives bolster the adoption of anti-submarine warfare systems.

- As per the sonobuoy launcher market analysis, the segment's dominance is underpinned by its critical role in maintaining global naval security.

The maritime surveillance segment is expected to register the fastest CAGR during the forecast period.

- Maritime surveillance industry applications emphasize the real-time monitoring of oceanic regions to detect illegal activities.

- The growth in need for monitoring commercial shipping routes supports the deployment of sonobuoy launchers.

- Advanced surveillance technologies integrated with sonobuoy systems ensure precise data collection.

- As per the sonobuoy launcher market trends, increasing investments in coastal and offshore security enhance the growth prospects of this segment.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

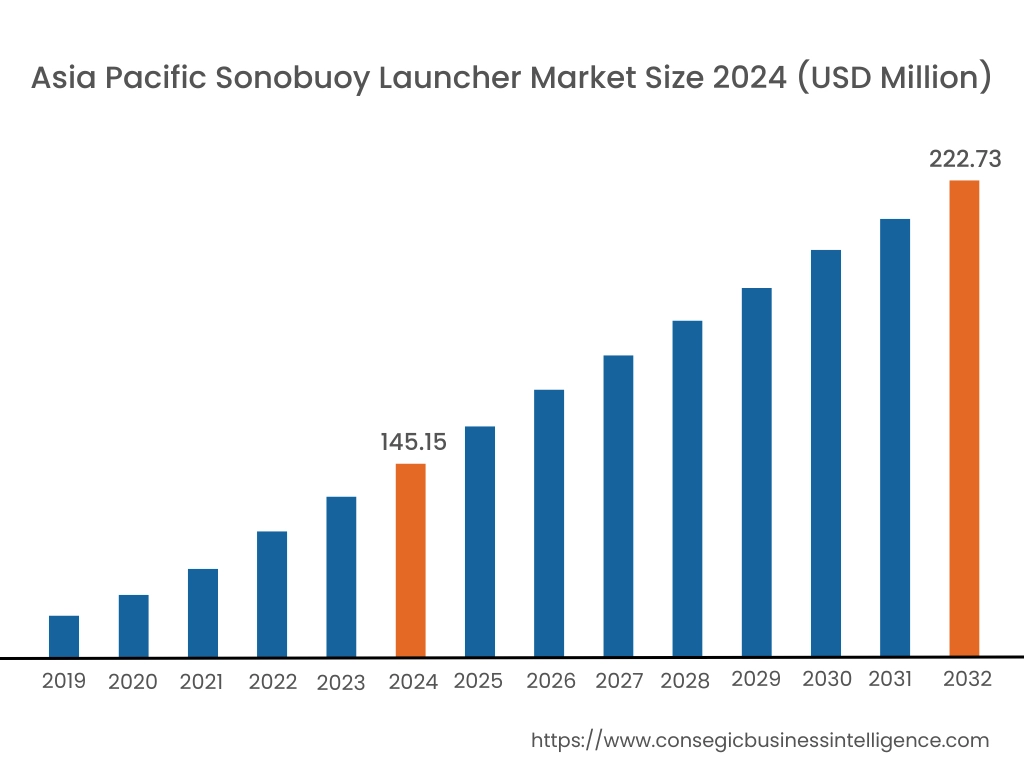

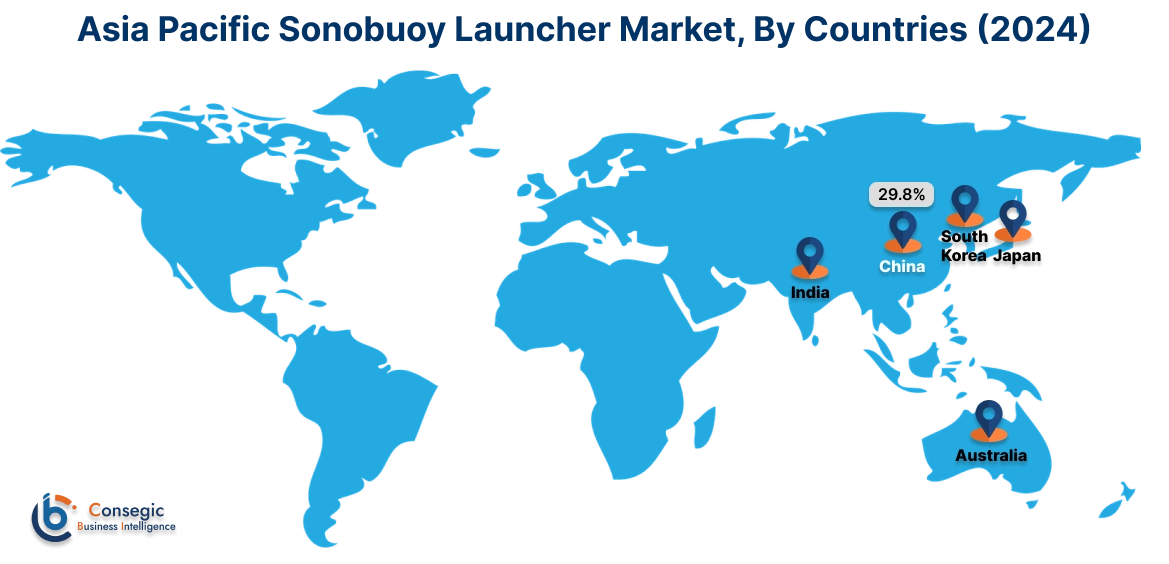

Asia Pacific region was valued at USD 145.15 Million in 2024. Moreover, it is projected to grow by USD 150.33 Million in 2025 and reach over USD 222.73 Million by 2032. Out of this, China accounted for the maximum revenue share of 29.8%. The Asia-Pacific region is witnessing rapid advancements in the sonobuoy launcher market, attributed to rising maritime tensions and the need for robust ASW capabilities. A prominent trend is the development of indigenous sonobuoy launch systems by countries like China and India, aiming to reduce reliance on foreign technology. Analysis indicates that regional naval forces are investing in modern ASW platforms, including aircraft and ships equipped with sophisticated sonobuoy launchers, to counter potential underwater threats.

North America is estimated to reach over USD 237.07 Million by 2032 from a value of USD 163.48 Million in 2024 and is projected to grow by USD 168.52 Million in 2025. This region commands a substantial share of the sonobuoy launcher market, driven by the United States' emphasis on enhancing anti-submarine warfare (ASW) capabilities. A notable trend is the integration of launchers with unmanned aerial vehicles (UAVs), providing greater flexibility to naval forces and broadening their submarine detection capabilities. Analysis indicates that the U.S. Navy's focus on modernizing its ASW assets is propelling the sonobuoy launcher market demand for advanced sonobuoy launch systems.

European nations, particularly the United Kingdom and France, are key players in the market, with a strong emphasis on maritime security and defense modernization. A significant trend is the collaboration among defense contractors and naval forces to develop next-generation launchers compatible with both manned and unmanned platforms. The analysis of market trends suggests that the increasing procurement of maritime patrol aircraft and the integration of advanced sonar technologies are driving the sonobuoy launcher market expansion in this region.

In the Middle East, the sonobuoy launcher market is influenced by the strategic importance of securing vital maritime routes. The focus is on enhancing naval surveillance capabilities through the acquisition of advanced sonobuoy launch systems. In Africa, the market is gradually evolving, with efforts to bolster maritime security against piracy and illegal fishing. Analysis suggests that international partnerships and defense aid are pivotal in facilitating the adoption of sonobuoy launch technologies in these regions.

Latin American countries are increasingly recognizing the importance of maritime domain awareness, driving interest in sonobuoy launcher systems. A notable trend is the modernization of naval fleets with ASW capabilities to protect extensive coastlines and exclusive economic zones. However, economic constraints and budgetary limitations may impact the pace of adoption. Analysis indicates that regional collaborations and investments in defense infrastructure are boosting the sonobuoy launcher market opportunities in this area.

Top Key Players and Market Share Insights:

The Sonobuoy Launcher market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Sonobuoy Launcher market. Key players in the Sonobuoy Launcher industry include -

- L3Harris Technologies (USA)

- Ultra Maritime (UK)

- GeoSpectrum Technologies Inc. (Canada)

- Aresia (France)

- Sparton Corporation (USA)

Sonobuoy Launcher Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 731.46 Million |

| CAGR (2025-2032) | 5.1% |

| By Launch Configuration |

|

| By Sonobuoy Type |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Sonobuoy Launcher Market? +

The Sonobuoy Launcher Market size is estimated to reach over USD 731.46 Million by 2032 from a value of USD 492.85 Million in 2024 and is projected to grow by USD 509.01 Million in 2025, growing at a CAGR of 5.1% from 2025 to 2032.

What are the key segments in the Sonobuoy Launcher Market? +

The market is segmented by launch configuration (single launch system, multiple rotary launch system), sonobuoy type (active sonobuoys, passive sonobuoys, special purpose sonobuoys), and application (anti-submarine warfare, maritime surveillance, search & rescue, scientific research, others).

Which segment is expected to grow the fastest in the Sonobuoy Launcher Market? +

The single launch system segment is expected to register the fastest CAGR during the forecast period, as it is favored for targeted deployments, offering precision and cost-effectiveness, particularly in scientific research and environmental monitoring applications.

Who are the major players in the Sonobuoy Launcher Market? +

Key players in the Sonobuoy Launcher market include L3Harris Technologies (USA), Ultra Maritime (UK), Aresia (France), Sparton Corporation (USA), GeoSpectrum Technologies Inc. (Canada).