- Summary

- Table Of Content

- Methodology

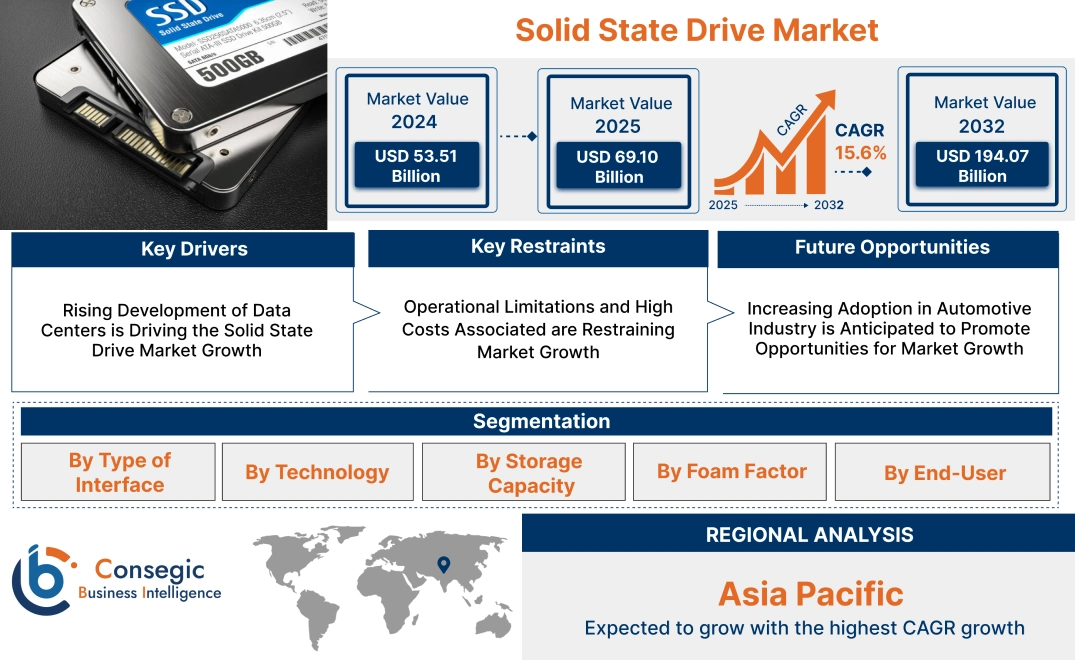

Solid State Drive Market Size:

Solid State Drive Market is estimated to reach over USD 194.07 Billion by 2032 from a value of USD 53.51 Billion in 2024 and is projected to grow by USD 69.10 Billion in 2025, growing at a CAGR of 15.6% from 2025 to 2032.

Solid State Drive Market Scope & Overview:

Solid state drives (SSD) refer to semiconductor-based storage devices that utilize integrated circuit assemblies for storing data persistently and often use flash memory as secondary computer storage. The drive offers a range of benefits including high reliability, durability, improved power efficiency, lower latency, and higher input/output operations among others. The aforementioned benefits of solid-state drives are key determinants for increasing utilization in consumer, enterprise, and industrial storage applications. Further, Factors including the rising development of business enterprises, growing adoption of high-end cloud computing, and increasing demand for enhanced storage solutions among business enterprises are among the key prospects driving the adoption of solid-state drives. Moreover, rising production of consumer electronic devices including laptops and PCs, along with growing demand for high-speed storage solutions for consumer devices are significant factors fostering market demand. Additionally, the market is also driven by advances in technology, which has led to the development of more efficient and reliable drive.

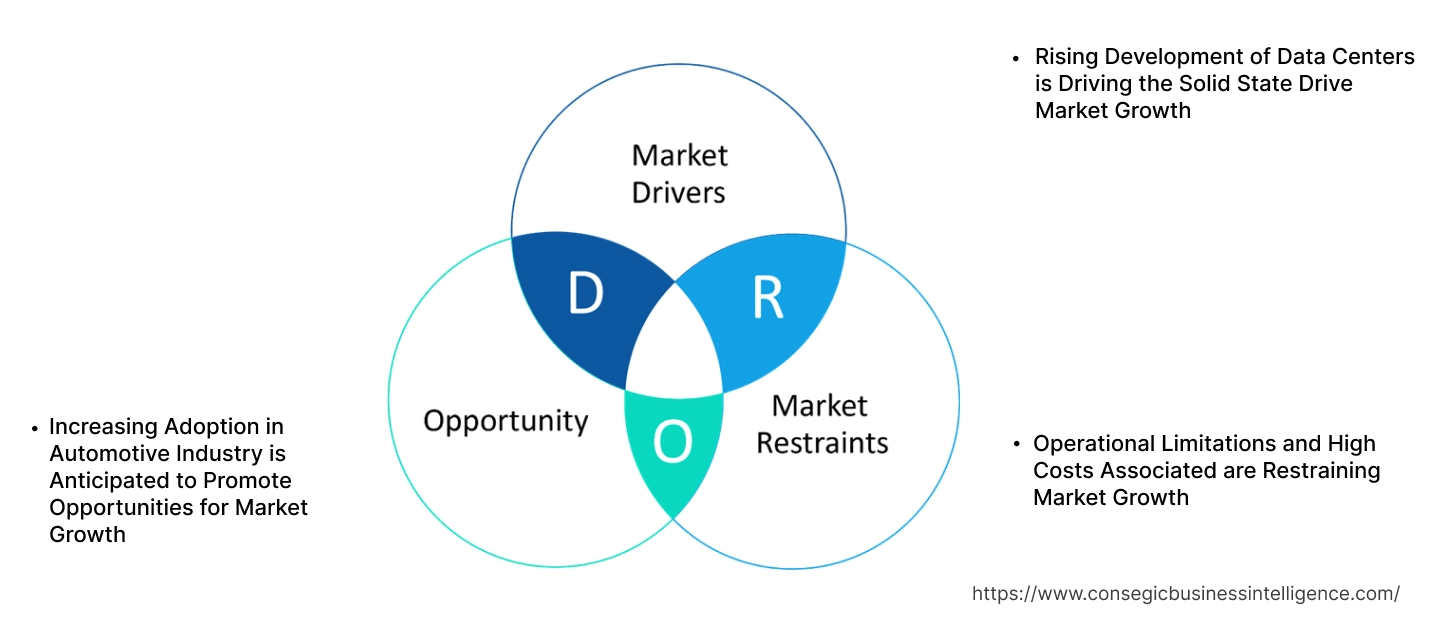

Solid State Drive Market Dynamics - (DRO) :

Key Drivers:

Rising Development of Data Centers is Driving the Solid State Drive Market Growth

Solid state drives are primarily used in data center servers for storing large volumes of data and electronic information. They are also capable of accelerating data center workloads, attaining maximum throughput, and transforming data into actionable insights. Moreover, they offer a wide range of benefits including faster speed, improved system performance, high reliability, lower power consumption, and increased durability. The aforementioned benefits of drives are primary determinants for increasing their application in data centers. Factors including the rapid pace of digital transformation, increasing deployment of cloud services, expansion of data centers, and rising demand for higher capacity server storage solutions are among the key prospects driving the adoption of drives.

- For instance, in February 2024, Azora Group launched its new European Edge data center platform. The company launched Quetta Data Centers, in collaboration with Core Capital. Azora Group further announced plans to invest over USD 538.5 million in the development of six Edge data centers in Portugal and Spain, with total capacity of 60MW.

Hence, the rise in development of data centers is driving the adoption of drives for application in data center servers for storing large volumes of data and electronic information, in turn proliferating the growth of market.

Key Restraints:

Operational Limitations and High Costs Associated are Restraining Market Growth

The implementation of enterprise solid state drives is often associated with certain operational limitations and high cost, which are prime factors limiting the market growth. Enterprise SSDs are designed for dealing with demanding enterprise systems and require higher performance, better reliability, longer lifespan, and higher endurance, which makes it relatively expensive in comparison to conventional HDDs (hard disk drives). For instance, enterprise SSDs typically cost an average of USD 185 per TB while the average cost of HDDs is around USD 19 per TB, demonstrating a significant difference in price by around 9.7 times higher per TB. Further, the drives are associated with certain operational limitations including relatively limited storage capacity, potential data loss in case of drive failure, and limited writing cycles which can affect their life span and result in performance degradation over time after frequent usage. Therefore, the aforementioned limitations and high costs associated with are constraining the growth of the solid state drives market.

Future Opportunities :

Increasing Adoption in Automotive Industry is Anticipated to Promote Opportunities for Market Growth

The integration of AI (artificial intelligence) and sophisticated sensor arrays in automotive is increasing the need for enhanced in-vehicle data storage solutions. Solid state drives are often used in the automotive sector for storage applications involving infotainment system, advanced driver assistance system (ADAS), and autonomous driving system. Moreover, automotive-grade SSDs have extended temperature ranges and low power consumption, which assists in maintaining optimal vehicle performance. Factors including the increasing production of automobiles, advancements in autonomous driving systems, and growing integration of enhanced automobile infotainment, sensor, and safety solutions are key aspects fostering the growth of the automotive sector and in turn offers significant opportunities.

- For instance, according to the European Automobile Manufacturers Association, total production of passenger cars in the EU (European Union) reached 10.9 million in 2022, depicting an incline of 8.3% in comparison to 2021.

Thus, the rising automobile production projected to increase the adoption of SSDs in modern automobiles for in-vehicle data storage applications involving infotainment system, advanced driver assistance system (ADAS), telematics, and autonomous driving system, thereby, promoting opportunities for market growth in the upcoming years.

Solid State Drive Market Segmental Analysis :

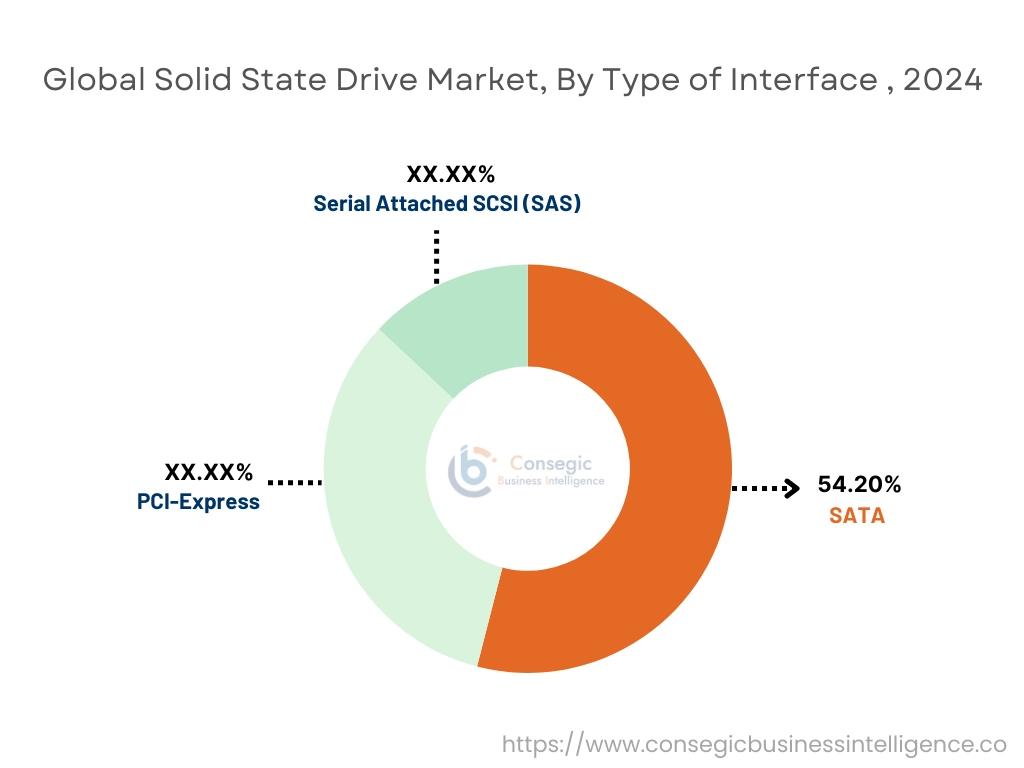

By Type of Interface:

Based on the type of interface, the market is segmented into Serial Attached SCSI (SAS), SATA, and PCI-Express

Trends in the Type of Interface:

- PCIe offers significantly higher bandwidth and lower latency compared to SATA and SAS, crucial for demanding applications which is driving the solid state drive market.

- Increasing trend in the adoption of SATA due to Widespread Compatibility and cost effectiveness.

SATA accounted for the largest revenue share of 54.20% in the year 2024.

- SATA (Serial Advanced Technology Attachment) refers to a bus interface that is designed to connect a computer's host bus adapter to storage devices including SSD and others.

- Further, benefits including higher data transfer rate, increased airflow, lower latency, and higher bandwidth among others are driving the solid state drives market growth.

- For instance, in June 2022, Micron Technology Inc. launched its new Micron 5400 SATA SSD for offering advanced storage for critical infrastructure. The SATA SDD offers optimized performance, increased reliability, along with more usable life per drive and fewer failures to support critical infrastructure.

- Thus, as per analysis, benefits including higher data transfer rate, increased airflow, lower latency, and higher bandwidth are driving the market growth of SATA.

PCI-Express is expected to register the fastest CAGR during the forecast period.

- PCI-express (PCIe) refers to a standardized interface that is designed for motherboard components including storage, memory, and graphics. Drives with PCI-express interface utilize flash memory for storing files and applications.

- Further, factors including rising pace of digitalization, increasing adoption of solid states drives as storage solutions in consumer devices, along with growing need for improved enterprise storage solutions with lower latency is driving solid state drive market.

- For instance, in January 2024, Samsung launched its new 990 EVO model of drive that supports both PCIe 5.0x2 interface and PCIe 4.0x4 interface. The 990 EVO PCIe SSD offers improved performance, sequential read speeds up to 5,000 megabytes-per-second (MB/s) and writing speeds up to 4,200 MB/s.

- Therefore, as per analysis, wide range applications and rising pace of digitalization are anticipated to boost the growth of the market during the forecast period.

By Technology:

Based on Technology, the market is segmented into SLC, MLC, TLC, and others

Trends in Technology:

- Increasing adoption of MLC and TLC due to their lower cost per gigabyte compared to SLC.

- QLC is gaining traction in cost-sensitive applications, such as bulk storage and data centers which in turn drive solid state drive market

TLC accounted for the largest revenue share in the year 2024 and is anticipated to register the fastest CAGR during the forecast period.

- TLC (triple-level cell) refers to a form of NAND flash storage, wherein three bits of data is stored per cell. Triple-level cell SSDs are capable of holding three bits per NAND cell, and have eight different voltage states, which increases storage capacity significantly

- Further, TLC offer faster performance at an economical price, thereby, increasing its application to several digital consumer devices in driving the adoption.

- Furthermore, factors including the growing consumer electronics industry, rising adoption of solid states drive as storage solutions in consumer devices, and increasing usage of economical storage devices driving the adoption of TLC drives

- For instance, in June 2023, ATP Electronics introduced its new high-speed N601 series of drives featuring 176-layer triple level cell (TLC) NAND flash. The TLC SSD provides a maximum bandwidth of 8 GB/s for fulfilling the increasing need for high-speed data transfer in several applications.

- Thus, based on analysis, faster performance and economic prices are driving the need for TLC, which in turn drives the solid state drive market.

By Storage Capacity:

Based on the storage capacity, the market is segmented into up to 500 GB, 500 GB - 1 TB, 1TB - 2 TB, and above 2 TB

Trends in Storage Capacity:

- The trend towards increasing size of files, such as 4K and 8K videos, high-resolution images, and large game files, is driving adoption of higher capacity SSDs.

- Advancements in 3D NAND technology and other innovations are driving down production costs

Up to 500 GB accounted for the largest revenue share in the year 2024.

- Drives with storage capacity up to 500 GB are widely used in consumer electronic devices including laptops, tablets, gaming consoles, and others which in turn drives market growth

- Further, relatively lower costs in comparison to higher storage drives, improved battery life, faster performance, and enhanced user experiences are primary factors for increasing its application in consumer electronics among others which in tune drives the solid state drives market.

- For instance, Seagate Technology offers BarraCuda SSD series in its product portfolio with storage capacity ranging up to 500 GB. The BarraCuda SSDs are available in multiple storage options including 240 GB, 256 GB, and 480GB among others

- Thus, wide range of uses in consumer electronic devices and relatively lower costs are driving the adoption of drives with capacity of up to 500 GB.

Above 2 TB is anticipated to register the fastest CAGR during the forecast period.

- Drives with storage capacity above 2 TB are widely used as external storage solutions for consumer devices or applications involving enterprise data centers, and others.

- Furthermore, features including exceptionally faster speeds, superior energy efficiency, very fast boot-up and load times, along with efficient data transfer and storage play a key role in driving the market growth.

- For instance, in October 2023, Samsung launched its new external storage device, portable SSD T9, which offers storage options up to 4 TB. The SSD can deliver fast data transfer speed and abundant storage capacity while ensuring high reliability and convenience.

- Therefore, faster speeds, superior energy efficiency, and fast boot-up & load time are anticipated to boost the growth of the market during the forecast period.

By Foam Factor:

Based on the foam factor, the market is segmented into 2.5 inch SSD, M.2 SSD, U.2 SSD, E1.S SSD, and Other

Trends in Foam Factor:

- 2 supports both SATA and PCIe interfaces, catering to a wide range of applications in turn driving the solid state drive market.

- 2 and E1.S form factors are gaining traction in enterprise and data center environments due to their high performance, density, and power efficiency.

M.2 SSD accounted for the largest revenue share in the year 2024.

- 2 SSD refers to a small form factor that is widely utilized in portable and lightweight computers such as laptops and notebooks, which in turn boost market growth

- Further, M.2 SSD is designed to enable high-performance storage in thin power-constrained devices and consumes less space as compared to 2.5-inch SSDs.

- For instance, Kingston Technology offers DC1000B model of high-performance SSD with M.2 (2280) form factor. The M.2 SSD utilizes PCIe interface with TLC NAND. The M.2 SSD provides an economical boot drive solution for data centres.

- Thus, small form factors and high-performance drive the need for 2 SSD form factor in turn drives the solid state drive market.

E1.S SSD is anticipated to register the fastest CAGR during the forecast period.

- S is available in four form factors including 5.9 mm 9.5 mm, 15 mm, and 25 mm, which signifies the thickness and is designed for flash memory chips and leverages PCIe interface and NVMe protocol technologies.

- Further, E1.S SSD offers a range of design benefits in terms of storage density, power, thermal management, performance, and other related parameters which in turn drive the market.

- For instance, in October 2022, KIOXIA Europe GmbH launched its new XD7P series with E1.S form factor that is specifically designed for application in hyperscale data centers.

- Therefore, good storage density and high performance are anticipated to boost the growth of the market during the forecast period.

By End User:

Based on the end user, the market is segmented into consumer, enterprises, and industrial

Trends in the End user:

- The increasing demand for data storage and processing in data centers is driving significant growth in the enterprise SSD market.

- The rise of gaming and content creation is fueling the need for high-performance SSDs in the consumer market.

Consumer accounted for the largest revenue share in the year 2024

- SSDs are often used as internal or external storage solutions in a range of consumer devices including laptops, tablets, notebooks, desktops, and gaming consoles among others.

- Further, drives offer a range of benefits including improved battery life, faster speed and performance, enhanced user experiences, and others, which are key determinants for increasing its utilization in consumer storage applications.

- For instance, in July 2023, KIOXIA Europe GmbH launched its new consumer SSD for mainstream users. The EXCERIA PLUS G3 series consumer SSD leverages PCIe 4.0 technology and provides up to 2 terabytes (TB) of storage capacity.

- Thus, according to analysis, benefits including improved battery life, faster speed & performance, and enhanced user experiences are driving the solid state drive market.

Industrial is expected to register the fastest CAGR during the forecast period.

- SSDs are often used for industrial data storage applications involving automotive storage, industrial automation, and others.

- Further, drives that are designed for industrial applications offer a range of benefits including robust design, wider operating temperature, stable writing performance, increased resistance to shock and vibrations, power loss protection, and others.

- Furthermore, factors including the growth in industrial automation fueled by Industry 4.0, increasing adoption of digital technologies in industrial manufacturing, and growing requirement for robust and reliable industrial data storage solutions are driving the solid state drive market.

- Therefore, based on analysis, robust design, wider operating temperature, stable writing performance, increased resistance to shock and vibrations, is anticipated to boost the market size during the forecast period.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

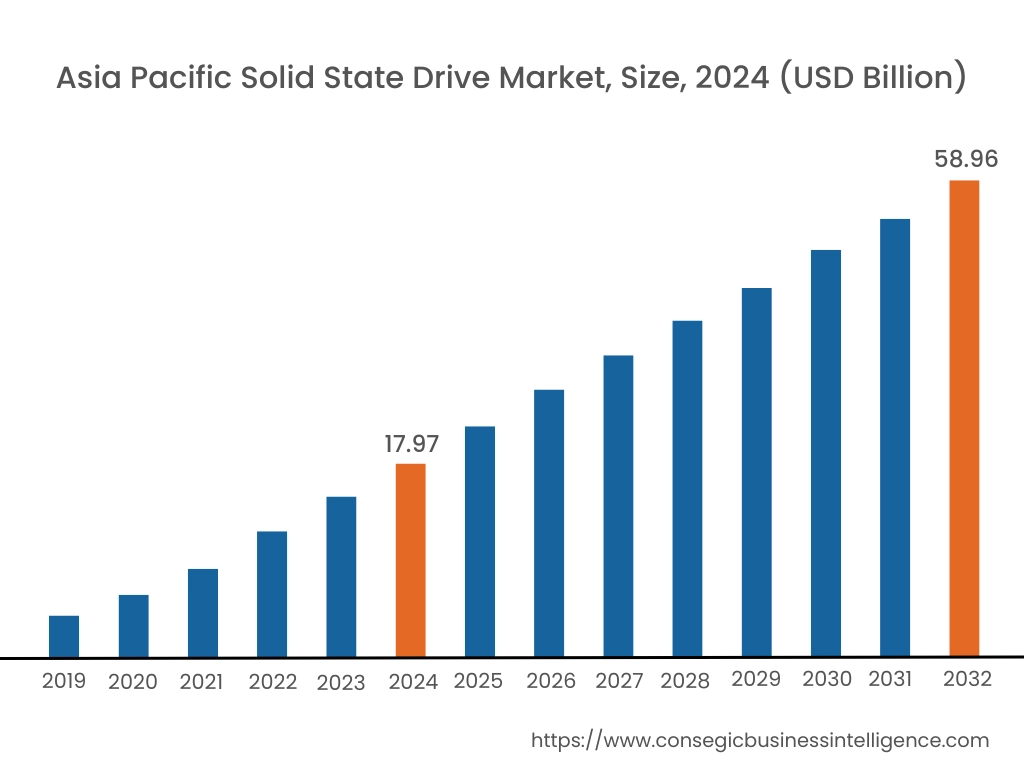

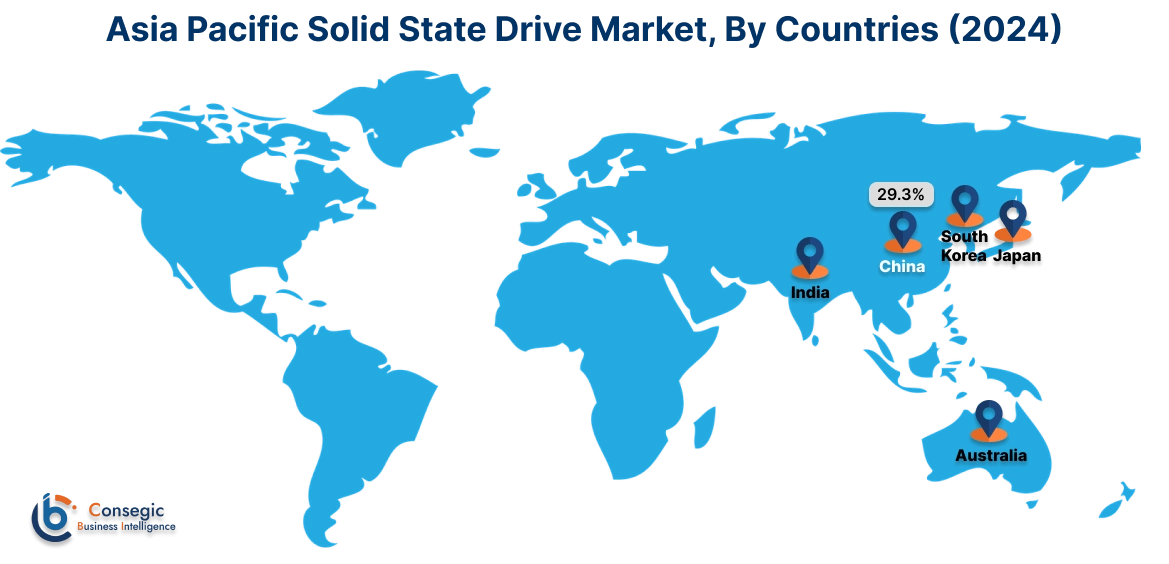

Asia Pacific region was valued at USD 17.97 Billion in 2024. Moreover, it is projected to grow by USD 20.51 Billion in 2025 and reach over USD 58.96 Billion by 2032. Out of this, China accounted for the maximum revenue share of 29.3%. The solid state drives market is mainly driven by the rapid economic rise and technological advancements in the region, coupled with the increasing need for high-performance computing and data storage solutions across various sectors, including data centers, enterprises, and consumers. Additionally, the rapid expansion of data centers across the region is creating a significant market for high-capacity and high-performance SSDs.

- For instance, May 2023, Kioxia Corporation headquartered in Japan announced new consumer SSDs released in the third quarter of 2023. The EXCERIA PLUS G3 Series will leverage PCIe 4.0 technology and offer up to 2 terabytes (TB) of capacity. The new series is well-suited to mainstream users of high performance gaming PCs, desktops and notebooks, bringing the speed and affordability that they require.

North America is estimated to reach over USD 62.65 Billion by 2032 from a value of USD 19.68 Billion in 2024 and is projected to grow by USD 22.41 Billion in 2025. The solid state drive market in North America is mainly driven by the strong presence of major technology companies and cloud service providers, coupled with the region's robust IT infrastructure and early adoption of advanced technologies. Further, North America is home to many leading technology companies and cloud service providers, driving the high-performance storage solutions like SSDs.

- For instance, in June 2023 Seagate Technology headquartered in U.S. introduced the next generation of SSD technology to its lineup, the FireCuda 540. The PCIe Gen5 NVMe SSD delivers unparalleled performance to gamers, creators, and tech enthusiasts, adding the fastest speeds and endurance to the company’s line of PC storage products.

The regional analysis depicts that the solid state drive market in Europe is primarily driven by multiple factors including rising trend of cloud deployment by business enterprises, increasing development of data centers, and growing requirement for high-capacity storage solutions in data centers in the region. The primary factor driving the market in the Middle East and African region is the rapid economic growth and infrastructure development across various sectors, coupled with increasing investments in technology and digital transformation initiatives. Further, rapid urbanization and growing digitalization across the region, coupled with increasing investments in infrastructure and technological advancement is paving the way for the progress of market trends in Latin America region.

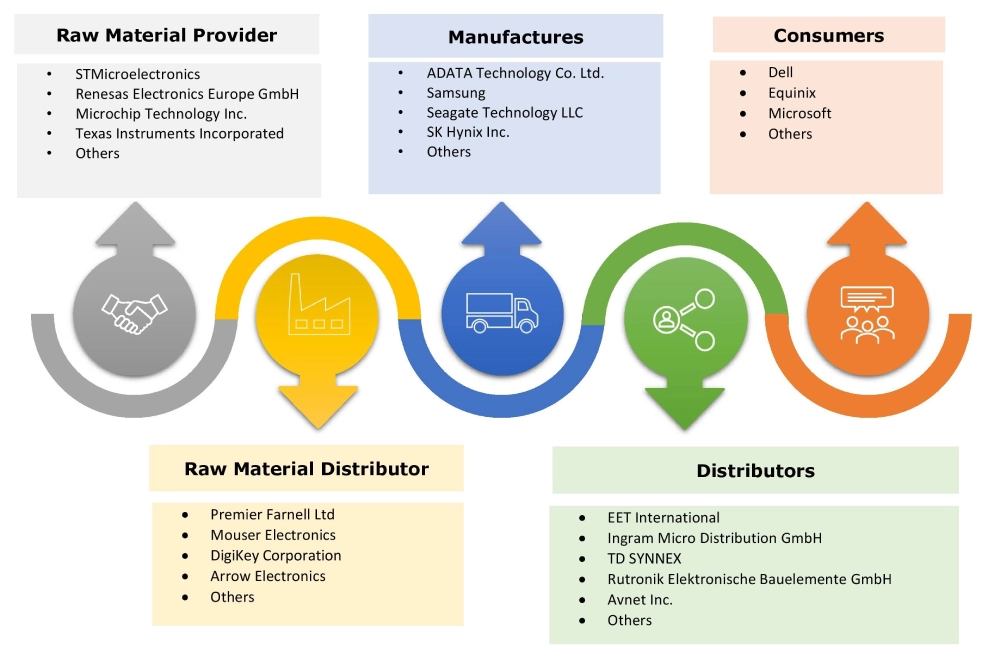

Top Key Players and Market Share Insights:

The global solid state drive market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the solid state drive industry. Key players in the solid state drive market include-

- ADATA Technology Co. Ltd. (Taiwan)

- Micron Technology, Inc. (US)

- Viking Technology (US)

- Western Digital Corporation (US)

- Transcend Information, Inc (Taiwan)

- KIOXIA Corporation (Japan)

- Microsemi Corporation (US)

- SAMSUNG (South Korea)

- Seagate Technology LLC (US)

- SK Hynix Inc (South Korea)

Recent Industry Developments :

Product Launches:

- For instance, in September 2023, Solid State Storage Technology Corporation launched its new CL6 series of industrial-grade solid state drives integrated with BiCS FLASH 3D flash memory. The CL6 series industrial-grade SSD employs the PCIe 4.0 interface and adheres to the NVMe 1.4c standard while providing more reliable and efficient storage solutions for industrial applications.

- For instance, in August 2023, Kioxia Corporation announced the addition of the KIOXIA CD8P Series to its lineup of data center-class SSDs. The KIOXIA CD8P Series is well-suited to general purpose server and cloud environments. These data center applications can generate complex mixed workloads spread across large scale virtualized systems in 24x7 operational data centers.

Solid State Drive Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 194.07 Billion |

| CAGR (2025-2032) | 15.6 % |

| By Type of Interface |

|

| By Technology |

|

| By Storage Capacity |

|

| By Foam Factor |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Solid State Drive Market? +

The Solid State Drive Market is estimated to reach over USD 194.07 Billion by 2032 from a value of USD 60.66 Billion in 2024 and is projected to grow by USD 69.10 Billion in 2025, growing at a CAGR of 15.6% from 2025 to 2032.

What specific segmentation details are covered in the solid state drive report? +

The solid state drive report includes specific segmentation details for type of interface, technology, storage capacity, foam factor, end user, and regions.

Which is the fastest segment anticipated to impact the market growth? +

In the solid state drive market, E1.S SSD form factor is the fastest-growing segment during the forecast period due to its high density, improved thermal performance, and enhanced power efficiency, making it ideal for high-density server deployments in data centers.

Who are the major players in the Solid State Drive Market? +

The key participants in the Solid State Drive Market are ADATA Technology Co. Ltd. (Taiwan), Micron Technology, Inc. (US), KIOXIA Corporation (Japan), Microsemi Corporation (US), SAMSUNG (South Korea), Seagate Technology LLC (US), SK Hynix Inc (South Korea), Viking Technology (US), Western Digital Corporation (US), Transcend Information, Inc (Taiwan)and others.

What are the key trends in the Solid State Drive Market? +

The Solid State Drive Market is being shaped by several key trends including the increasing demand for high-performance storage solutions across various applications like gaming, enterprise, and data centers, the introduction of advanced algorithms for enhancing SSD performance, reliability, and lifespan, and the persistent need for enhanced storage performance and reliability across diverse computing applications.