- Summary

- Table Of Content

- Methodology

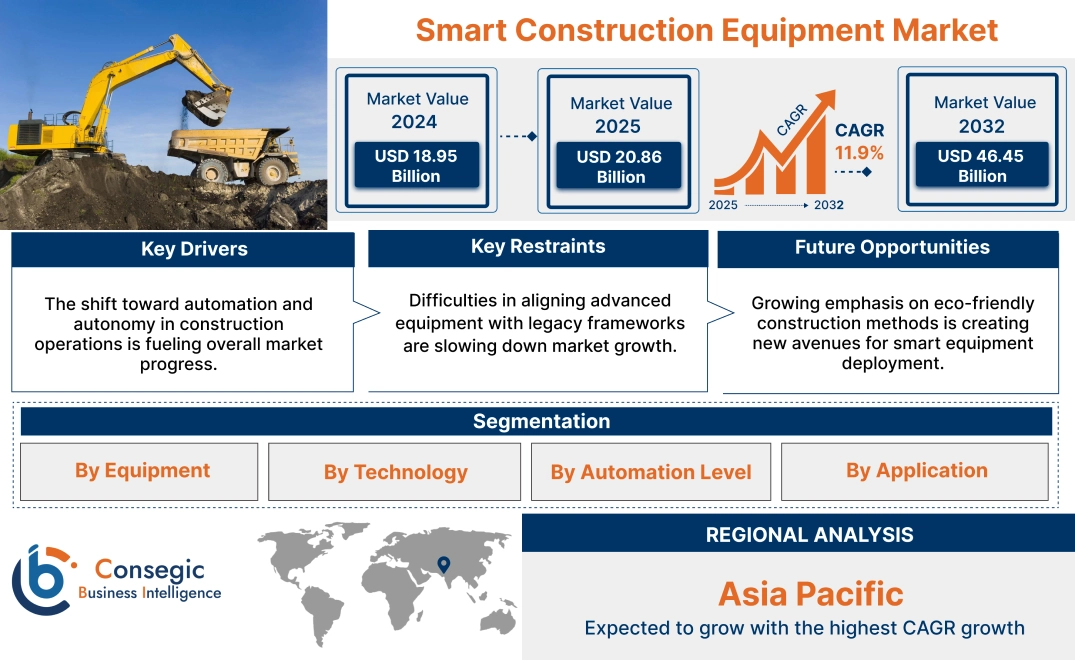

Smart Construction Equipment Market Size:

Smart Construction Equipment Market size is estimated to reach over USD 46.45 Billion by 2032 from a value of USD 18.95 Billion in 2024 and is projected to grow by USD 20.86 Billion in 2025, growing at a CAGR of 11.9% from 2025 to 2032.

Smart Construction Equipment Market Scope & Overview:

Smart construction equipment refers to advanced machinery integrated with digital control systems, connectivity modules, and data sensors that support automated and precision-based operations on construction sites. These machines are equipped with embedded systems that collect and transmit operational data, allowing real-time monitoring, remote diagnostics, and adaptive performance control across excavation, material handling, paving, and structural assembly tasks.

These systems often include GPS tracking, telematics, weight sensors, and smart controls that help improve precision and reduce manual effort. Common equipment like excavators, graders, cranes, and bulldozers can be equipped with these technologies. The machines can also connect with construction management software to stay in sync with overall project plans. Depending on the site, they may use wireless connections through cellular, satellite, or local network systems.

Smart construction equipment supports the execution of complex, multi-phase construction activities while enhancing field-level equipment management. End-users include construction contractors, equipment rental providers, and infrastructure development firms requiring automated solutions for improving operational oversight and machine coordination.

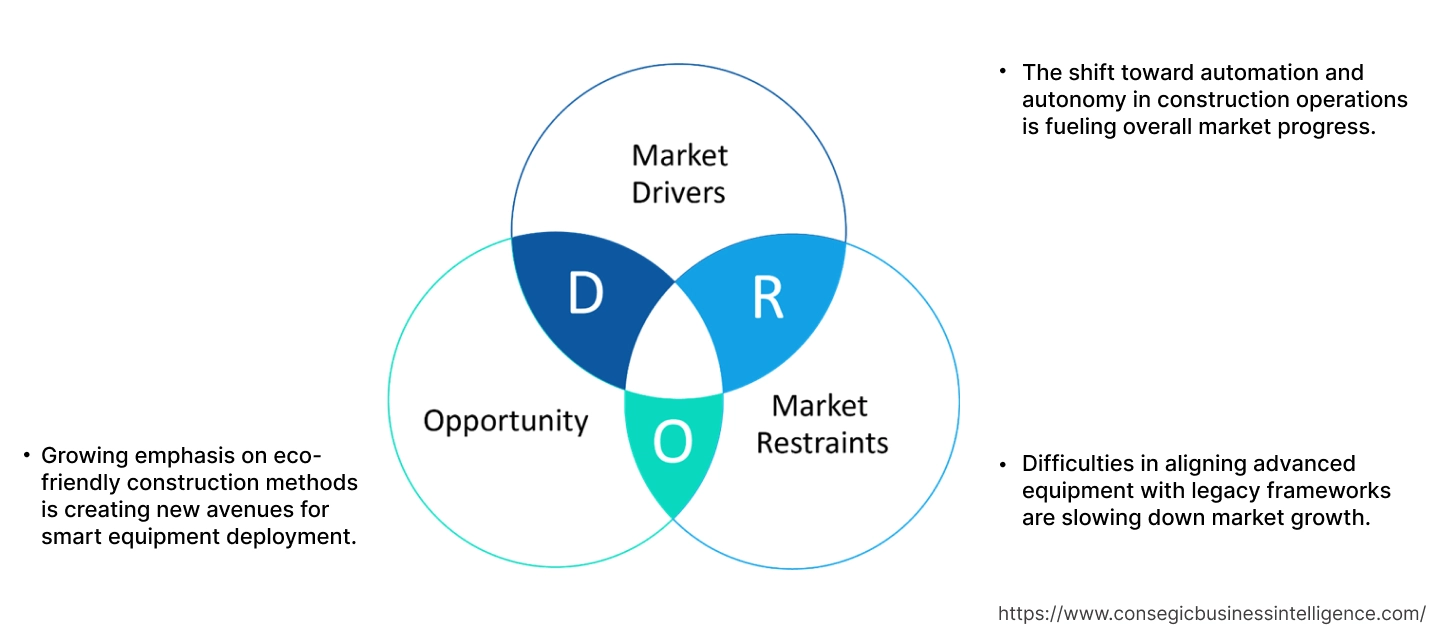

Smart Construction Equipment Market Dynamics - (DRO) :

Key Drivers:

The shift toward automation and autonomy in construction operations is fueling overall market progress.

Autonomous bulldozers, excavators, and cranes, equipped with AI and real-time monitoring systems, enhance efficiency, safety, and productivity, while significantly reducing the reliance on human labor. This technology improves precision in tasks such as digging, lifting, and hauling, which is crucial in high-risk environments like mining, demolition, and heavy-duty construction. In hazardous areas where human presence is unsafe, autonomous machines ensure the work is completed with minimal risk. These machines also reduce errors, streamline project timelines, and lower operational costs by working continuously without breaks.

- For instance, in May 2024, Volvo Construction Equipment (Volvo CE) introduced a new generation of innovative excavators—EC500, EC400, EC230, EC210, and ECR145—featuring an advanced electro-hydraulic system and enhanced human-machine interface (HMI). These machines include advancements in electrification, autonomous solutions, electric and low-emission machines, new compact models, and smart technology features that enhance efficiency, safety, and connectivity, aligning with the company’s technology-driven approach to meet diverse customer needs.

As the technology matures, construction companies are becoming more inclined to integrate autonomous systems into their operations. The ability to operate with higher efficiency and accuracy is driving demand, pushing the market towards further growth and wider adoption of autonomous construction machinery in the sector, significantly propelling market progress.

Key Restraints:

Difficulties in aligning advanced equipment with legacy frameworks are slowing down market growth.

The transition from traditional machinery to advanced, smart construction equipment presents a significant barrier due to the integration issues with existing infrastructure. Many construction companies still operate older machinery that were not designed to be compatible with modern technologies such as IoT, AI, and GPS. Retrofitting legacy systems to work seamlessly with these new technologies requires substantial investment in both time and money. Additionally, these upgrades often disrupt ongoing construction projects, affecting timelines and productivity. Construction companies are also faced with the obstacle of maintaining a balance between the cost of upgrading their equipment and the potential returns from adopting these advanced systems. As a result, companies that heavily rely on their traditional systems may hesitate to invest in new technologies. This incompatibility between old and new systems presents a barrier to faster adoption hindering the market's growth potential.

Future Opportunities :

Growing emphasis on eco-friendly construction methods is creating new avenues for smart equipment deployment.

Sustainability is becoming a top priority in the construction industry, driving demand for equipment that minimizes energy use, reduces waste, and supports environmentally friendly practices. With growing concerns over climate change and environmental impact, the focus has shifted toward reducing the carbon footprint of construction projects. Smart construction equipment, such as those powered by renewable energy or optimized for energy efficiency, plays a critical role in this shift. These machines help meet the increasing regulations aimed at lowering emissions in construction. They also assist in reducing waste by improving precision and efficiency in construction tasks.

- For instance, in April 2025, SANY Global announced that it is set to unveil a comprehensive lineup of intelligent, eco-friendly, and high-efficiency construction machinery, emphasizing its commitment to sustainable innovation. The showcase will feature cutting-edge equipment, including electric excavators, hydrogen-powered trucks, and smart construction solutions designed to enhance productivity while reducing environmental impact.

As governments and industries prioritize green building practices and sustainable development, the demand for equipment that aligns with these goals has increased. This transition toward eco-friendly construction practices is accelerating the adoption of smart, sustainable construction equipment, creating significant avenues, driving the global Smart Construction Equipment market opportunities.

Smart Construction Equipment Market Segmental Analysis :

By Equipment:

Based on Equipment, the market is categorized into Earthmoving & Road Building Equipment (Backhoe, Excavator, Loader, Compaction Equipment, and Others), Material Handling & Cranes (Storage and Handling Equipment, Engineered Systems, Industrial Trucks, and Bulk Material Handling Equipment), Concrete Equipment (Concrete Pumps, Crusher, Transit Mixers, Asphalt Pavers, and Batching Plants), and Crushing & Screening Equipment (Crushers, Screens, and Others).

The Earthmoving & Road Building Equipment segment holds the largest revenue of the overall Smart Construction Equipment Market share in the year 2024.

- Earthmoving and road building machinery dominates due to its core role in excavation, grading, and site preparation across infrastructure, commercial, and industrial construction.

- Smart-enabled Excavators and Loaders lead this segment with GPS-controlled depth tracking, real-time load monitoring, and automated grading functions.

- Backhoes and Compaction Equipment are increasingly being upgraded with telematics for diagnostics, productivity reporting, and location tracking.

- For instance, in December 2024, SANY Global unveiled a wide range of intelligent, electric, and low-carbon construction machinery, reinforcing its vision for the future of the industry at the bauma CHINA 2024. The exhibition featured over 40 advanced equipment models, including electric excavators, electric mixers, hydrogen-powered machinery, and intelligent road construction solutions.

- According to the Smart Construction Equipment market analysis, its indispensability across construction phases, Earthmoving & Road Building Equipment holds the largest share, fueling the Smart Construction Equipment market expansion.

The Material Handling & Cranes segment is expected to grow at the fastest CAGR during the forecast period.

- Material handling systems are experiencing rapid digitization to improve logistics, inventory tracking, and jobsite safety.

- Storage and Handling Equipment are being embedded with RFID scanners and smart load sensors for warehouse construction and prefab yards.

- Engineered Systems are increasingly integrating AI and automation for automated guided vehicle (AGV) operations and vertical storage solutions.

- As per the market analysis, the rising demand for high-speed, labor-efficient logistics within construction environments fuel the global Smart Construction Equipment market development.

By Technology:

Based on Technology, the market is categorized into GPS, telematics, IoT, AI-based systems, and others.

The Telematics segment holds the largest revenue of the overall Smart Construction Equipment Market share in the year 2024.

- Telematics systems allow contractors and fleet managers to monitor equipment health, fuel consumption, location, and idle time remotely.

- This technology is widely embedded in new equipment and retrofitted on legacy fleets to improve maintenance scheduling and operational efficiency.

- Telematics data is often integrated with centralized fleet management dashboards, enabling real-time productivity and cost tracking.

- According to the Smart Construction Equipment market analysis, its maturity and integration across most equipment classes, telematics is the most widely adopted smart construction technology, significantly fuels the market growth.

The AI-Based Systems segment is expected to grow at the fastest CAGR during the forecast period.

- AI-based platforms use machine learning algorithms to optimize construction processes, automate grading, detect jobsite anomalies, and predict mechanical failures.

- OEMs and tech startups are offering AI-powered payload monitoring, autonomous navigation, and camera vision for obstacle recognition and safety.

- AI enhances decision-making in fleet allocation, job sequencing, and material handling, improving overall site efficiency.

- For instance, in April 2025, Liebherr, in collaboration with Reycom and Qualcomm Technologies, announced a strategic partnership to develop AI-powered solutions that enhance machine intelligence and operational efficiency. The collaboration aims to integrate Qualcomm’s advanced processors and Reycom’s software expertise into Liebherr's construction and mining equipment, enabling improved predictive maintenance, real-time data processing, and autonomous capabilities.

- With the continuous advancements in data modeling and cloud processing, AI-based systems are expected to grow, substantially driving the Smart Construction Equipment market demand.

By Automation Level:

Based on Automation Level, the market is categorized into Semi-Automated and Fully Automated Equipment.

The Semi-Automated segment holds the largest revenue share of the overall Smart Construction Equipment Market in the year 2024.

- Most smart construction equipment currently on the market includes features like grade assist, lift assist, or collision alerts while retaining human control.

- These machines are more cost-effective than fully automated alternatives and require less adaptation of operator workflows.

- Adoption is strong across mid-scaled contractors who seek to improve output while maintaining workforce flexibility.

- Thus, its affordability and easier integration, semi-automated equipment holds the largest market segment, significantly driving the Smart Construction Equipment market trends.

The Fully Automated segment is expected to grow at the fastest CAGR during the forecast period.

- Fully automated systems operate with minimal human intervention, guided by AI algorithms, GPS data, and real-time site feedback.

- Applications include autonomous grading, trenching, and site scanning—particularly valuable in repetitive or hazardous environments.

- Firms deploying these systems benefit from reduced labor dependency, improved accuracy, and predictable timelines.

- According to the market analysis, as technology costs decrease and autonomous safety protocols improve, fully automated equipment is expected to expand significantly fueling the global Smart Construction Equipment market expansion.

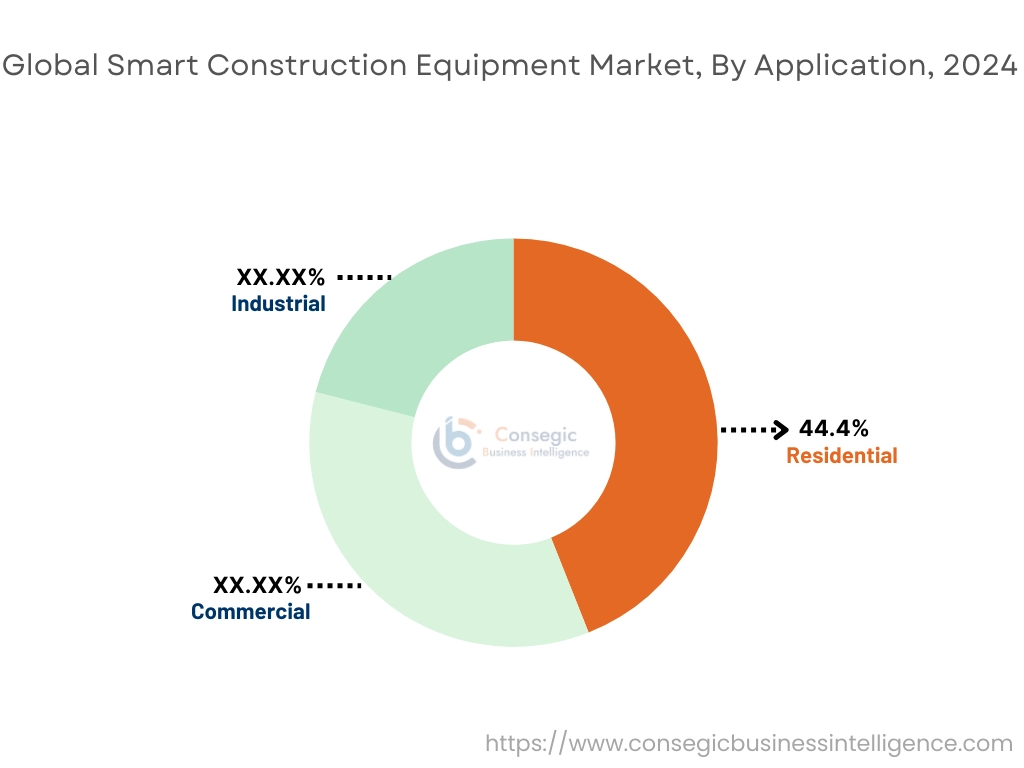

By Application:

Based on Application, the market is categorized residential, commercial, and industrial construction.

The Residential segment holds the largest revenue share of 44.4% in the overall Smart Construction Equipment Market in the year 2024.

- Growing urbanization and increasing demand for residential construction projects, driven by the need for housing, are the key factors fueling this segment's dominance.

- Smart construction equipment used in the residential sector includes automated machinery, drones for surveying, and robotic construction tools for efficient and accurate work.

- The adoption of smart technologies, such as IoT-enabled equipment and AI-based construction solutions, is driving operational efficiency and reducing construction timelines.

- As per Smart Construction Equipment market trends, residential projects benefit from the introduction of automation and advanced technology, leading to better precision, reduced labor costs, and faster construction timelines.

The Industrial segment is expected to grow at the fastest CAGR during the forecast period.

- Industrial construction including factories, logistics parks, refineries, and energy facilities demands high-precision work and 24/7 equipment uptime.

- Smart equipment helps optimize scheduling, reduce idle time, and perform heavy-duty tasks with increased operational visibility.

- High-value EPC (Engineering, Procurement, and Construction) contractors are using smart solutions to meet contract KPIs and sustainability benchmarks.

- The rising industrial investment across emerging markets is significantly fueling the global Smart Construction Equipment market opportunities.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, Middle East and Africa, and Latin America.

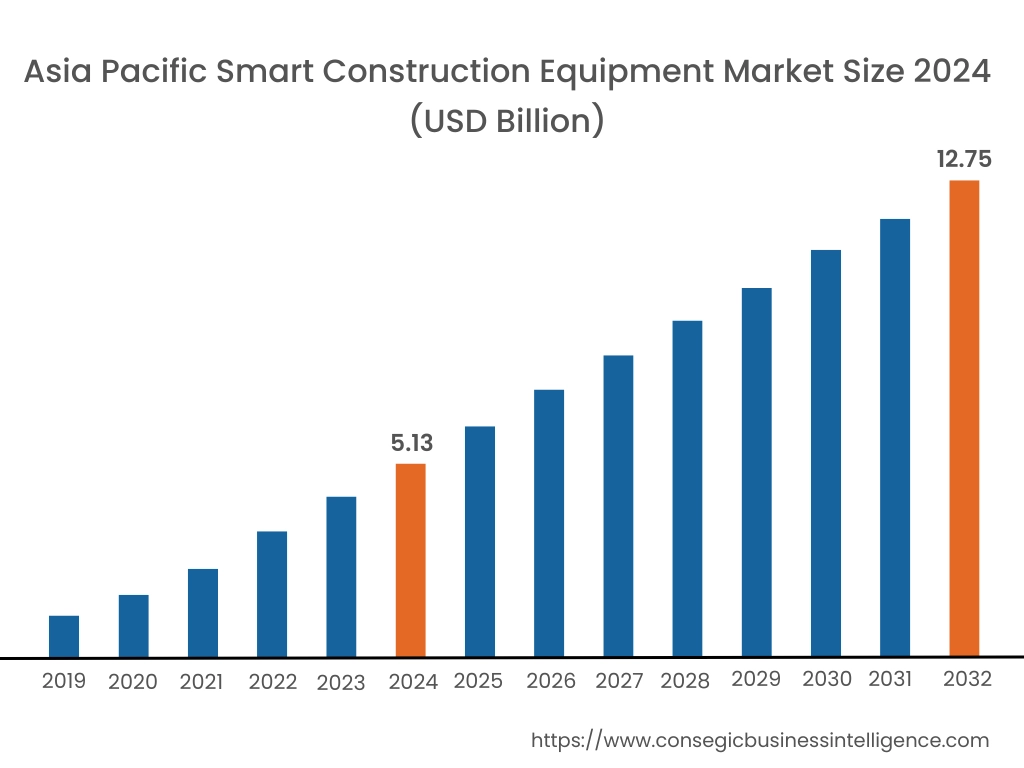

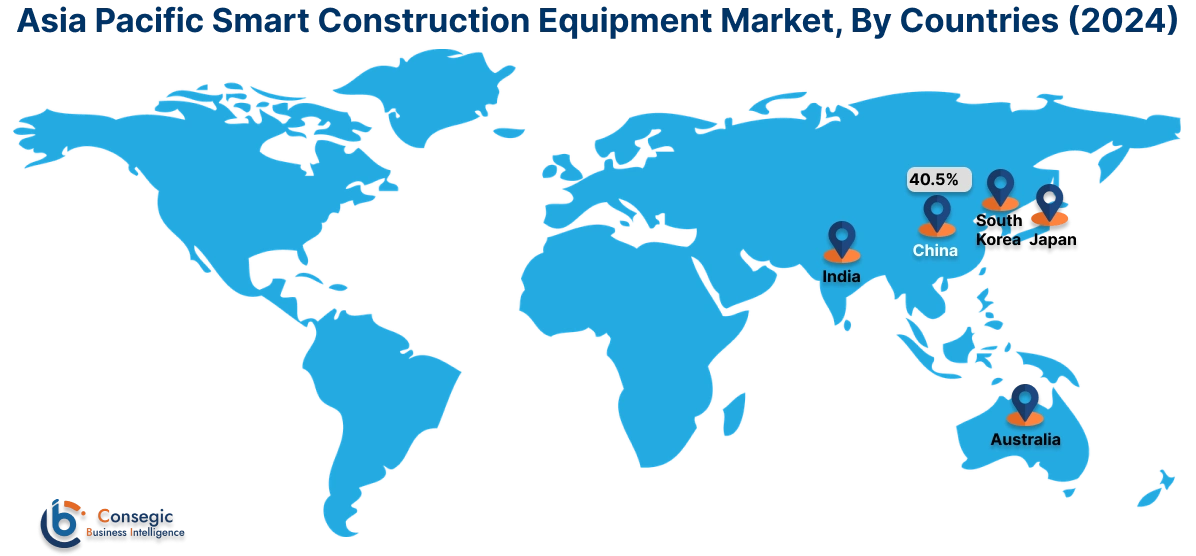

Asia Pacific region was valued at USD 5.13 Billion in 2024. Moreover, it is projected to grow by USD 5.65 Billion in 2025 and reach over USD 12.75 Billion by 2032. Out of this, China accounted for the maximum revenue share of 40.5%.

Across the Asia‑Pacific region, large‑scale infrastructure schemes and automation drives are fueling equipment innovation. Notable trends in the deployment of IoT‑connected hydraulic actuators in excavators along China’s major transport corridors and AI‑assisted grading machines in India’s rural road networks present significant market development.

- For instance, in September 2024, Hitachi Construction Machinery partnered with Dimaag-AI Inc. to develop a 1.7-ton zero-emission compact hydraulic excavator tailored for urban construction and indoor demolition. In this collaboration, Hitachi will provide the base machine specifications, while Dimaag will integrate its Electric No Compromise Off-Road Ecosystem (ENCORE)—featuring high-power, swappable battery modules, advanced thermal management, and EV components. This initiative underscores both companies' commitment to sustainable and innovative construction solutions.

Furthermore, growth in Japan’s precision manufacturing and Australia’s mining modernization efforts and the rising digital tender platforms and public‑private partnerships have significantly driven the Smart Construction Equipment market demand.

North America is estimated to reach over USD 15.47 Billion by 2032 from a value of USD 6.30 Billion in 2024 and is projected to grow by USD 6.94 Billion in 2025.

Across North America, smart construction equipment is being redefined by digitalization and connectivity. One notable trend is the integration of GPS-enabled fleet management systems in excavators and loaders, while another trend centers on the use of AI-based predictive maintenance modules in compact equipment. Additionally, Canada’s stringent emissions regulations and Mexico’s rural road programs encourage widespread technology adoption.

- For instance, in March 2025, Trimble announced that Kirby-Smith Machinery has become the first Trimble Technology Outlet (TTO) in the United States. This new designation allows Kirby-Smith to offer Trimble’s full suite of construction technology solutions, including machine control, site positioning systems, and software services, under one roof. As a TTO, Kirby-Smith will provide sales, service, training, and support, helping contractors integrate advanced digital tools to improve productivity and efficiency. This move strengthens Trimble’s U.S. distribution network and reflects its commitment to making cutting-edge construction technology more accessible and serviceable across the country.

Furthermore, the U.S. federal infrastructure investment and private-sector pilot deployments are key catalysts for the Smart Construction Equipment industry growth in this region.

Throughout Europe, the push for low‑carbon construction and digital transformation is reshaping heavy machinery. Germany’s stringent emission standards and France’s building retrofit incentives are propelling uptake for the equipment. Additionally, trends like the widespread adoption of telematics-enabled loaders and compactors to improve site efficiency and integration of battery‑electric drivetrains in mobile equipment are propelling market progress. Analysis of the market showed that growing smart city lab projects and tourism infrastructure expansions in various countries are significantly boosting the Smart Construction Equipment market in this region.

Within the Middle East & Africa, ambitious urban developments and resource management challenges shape machinery requirements. One prominent trend is the integration of telematics in heavy‑duty cranes for UAE’s skyline projects, while another trend highlights energy‑efficient pump systems tailored to Saudi Arabia’s NEOM initiative. Analysis of the market showed that South Africa’s urban renewal schemes and Kenya’s affordable housing programs are supporting technology uptake, and collaborations with global OEMs accelerate customization for harsh climates have fueled the Smart Construction Equipment market in this region.

In Latin America, the shifting trend for modern infrastructure and industrial diversification are driving equipment digitalization. A significant trend in this region involves cloud‑based fleet telematics in Brazil’s metropolitan projects, while another centers on remote diagnostics for mining rigs in Chile’s copper belt. Additionally, Mexico’s public works modernization and Argentina’s agricultural infrastructure upgrades are key drivers and the increasing partnerships between local fabricators and technology startups drives Smart Construction Equipment market growth in this region.

Top Key Players and Market Share Insights:

The Smart Construction Equipment Market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Smart Construction Equipment Market. Key players in the Smart Construction Equipment industry include -

- Caterpillar Inc. (USA)

- Komatsu Ltd. (Japan)

- Doosan Infracore (South Korea)

- Hyundai Construction Equipment (South Korea)

- Terex Corporation (USA)

- Deere & Company (USA)

- Volvo Construction Equipment (Sweden)

- Liebherr Group (Switzerland)

- XCMG Group (China)

- JCB Ltd. (UK)

Recent Industry Developments :

Product Launches:

- In April 2025, Putzmeister introduced the world’s first bidirectionally connected truck-mounted concrete pump at bauma 2025, marking a major step forward in digital construction technology. This innovative pump allows for real-time two-way communication between the machine and digital platforms, enhancing fleet management, diagnostics, and job site coordination. With this system, operators and project managers can access live data, send updates to the machine, and remotely monitor performance and maintenance needs.

Partnerships:

- In November 2024, Doosan Bobcat signed a tripartite Memorandum of Understanding (MOU) with Gwangyang City and Korea Logis Pool (KLP) to support the "Gwangyang Hydrogen City Project" by expanding the deployment of hydrogen-powered forklifts. This collaboration marks a strategic effort to grow hydrogen mobility and align with national carbon neutrality goals. Following the delivery of its first hydrogen forklift to Korea Zinc earlier this year, Doosan Bobcat continues to push for regulatory advancements.

Smart Construction Equipment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 46.45 Billion |

| CAGR (2025-2032) | 11.9% |

| By Equipment |

|

| By Technology |

|

| By Automation Level |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Smart Construction Equipment Market? +

The Smart Construction Equipment Market is estimated to reach over USD 46.45 Billion by 2032 from a value of USD 18.95 Billion in 2024, growing at a CAGR of 11.9%.

What specific segments are covered in the Smart Construction Equipment Market? +

The Smart Construction Equipment Market specific segments for Equipment, Technology, Automation Level, Application, and Region.

Which is the fastest-growing region in the Smart Construction Equipment Market? +

Asia pacific is the fastest growing region in the Smart Construction Equipment Market.

What are the major players in the Smart Construction Equipment Market? +

The key players in the Smart Construction Equipment Market are Caterpillar Inc. (USA), Komatsu Ltd. (Japan), Deere & Company (USA), Volvo Construction Equipment (Sweden), Liebherr Group (Switzerland), XCMG Group (China), JCB Ltd. (UK), Doosan Infracore (South Korea), Hyundai Construction Equipment (South Korea), Terex Corporation (USA), and others.