- Summary

- Table Of Content

- Methodology

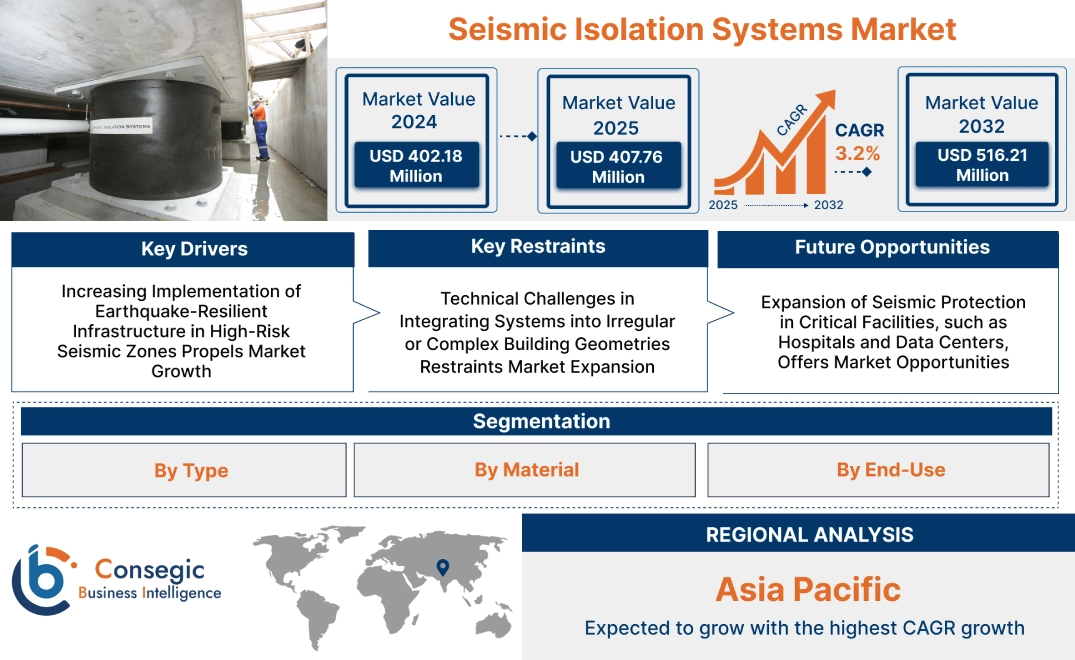

Seismic Isolation Systems Market Size:

Seismic Isolation Systems Market size is estimated to reach over USD 516.21 Million by 2032 from a value of USD 402.18 Million in 2024 and is projected to grow by USD 407.76 Million in 2025, growing at a CAGR of 3.2% from 2025 to 2032.

Seismic Isolation Systems Market Scope & Overview:

Seismic isolation systems are structural technologies designed to decouple buildings and infrastructure from ground motion during an earthquake. By absorbing and dissipating seismic energy, these systems reduce the transfer of vibrations, minimizing structural stress and potential damage.

Key components include elastomeric bearings, sliding bearings, dampers, and base isolators, strategically installed at foundation levels. These elements allow controlled movement, enabling structures to remain stable even under significant seismic displacement.

Seismic isolation systems enhance structural resilience, extend building service life, and reduce repair costs after seismic events. Their implementation is common in hospitals, bridges, high-rise buildings, and critical facilities where operational continuity and safety are priorities. The technology also supports compliance with modern engineering codes and performance-based design standards. Through passive energy absorption and displacement control, these systems offer a proactive approach to earthquake risk reduction in both new constructions and seismic retrofitting projects.

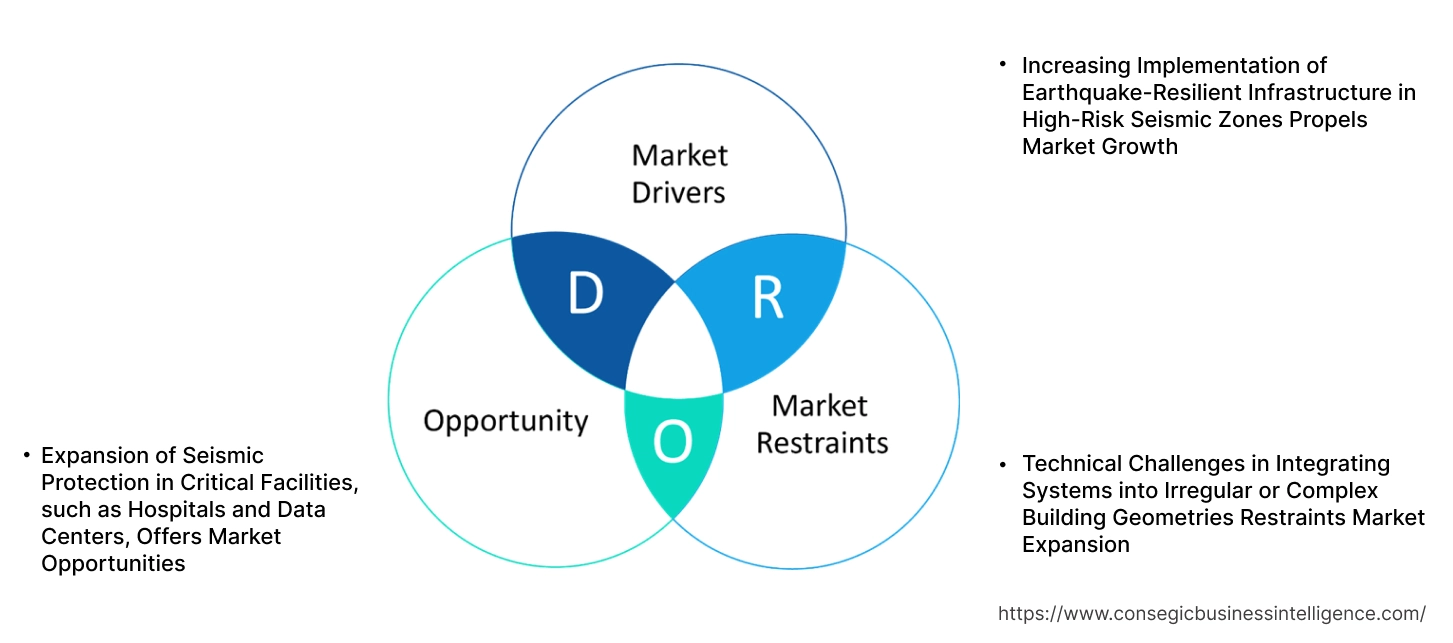

Seismic Isolation Systems Market Dynamics - (DRO) :

Key Drivers:

Increasing Implementation of Earthquake-Resilient Infrastructure in High-Risk Seismic Zones Propels Market Growth

Seismic isolation systems are becoming a core element of modern structural design in earthquake-prone regions such as Japan, California, Turkey, and Chile. As seismic activity continues to pose risks to life and property, public and private sectors are prioritizing infrastructure capable of withstanding ground motion without major structural damage. Urban planners and construction firms are now integrating base isolators, lead rubber bearings, and sliding pendulum isolators in buildings, bridges, and elevated transport systems. These technologies help decouple the superstructure from seismic forces, ensuring operational continuity and protecting occupants. In regions with recurring seismic activity, national building codes increasingly mandate the inclusion of isolation technologies for critical and high-value assets. With growing awareness of earthquake resilience and rising infrastructure investment in vulnerable regions, demand for structural protection is accelerating, leading to consistent seismic isolation systems market expansion.

Key Restraints:

Technical Challenges in Integrating Systems into Irregular or Complex Building Geometries Restraints Market Expansion

Implementing seismic isolation systems in buildings with non-uniform geometries, asymmetric load distribution, or complex architectural features presents notable design and engineering challenges. Structures with irregular footprints or mixed-use layouts require extensive structural analysis and custom isolation strategies to ensure even energy dissipation and proper load transfer. These complexities often extend design timelines and increase project costs, discouraging adoption among developers and contractors. Additionally, limited availability of experienced structural engineers and isolation specialists further complicates execution in many regions. Custom fabrication and adaptive deployment of isolators are also more difficult in retrofitting scenarios where space, foundation type, or access may be restricted. Despite increasing demand for seismic risk mitigation, these engineering constraints continue to hinder widespread adoption—ultimately slowing seismic isolation systems market growth in projects that deviate from standard structural configurations.

Future Opportunities :

Expansion of Seismic Protection in Critical Facilities, such as Hospitals and Data Centers, Offers Market Opportunities

Hospitals, emergency operation centers, data centers, and power plants require uninterrupted function during and after seismic events, making them ideal candidates for seismic isolation systems. These critical facilities house essential services and sensitive equipment that must remain operational to support disaster response and maintain societal continuity. In recent years, governments and private organizations have prioritized investment in seismic protection technologies for these high-value assets. As digital infrastructure and healthcare networks expand globally, the vulnerability of these systems to seismic disruption is gaining attention. Demand for high-performance isolation solutions is growing in both new builds and retrofit projects for mission-critical operations. By reducing downtime, protecting equipment, and ensuring structural integrity, isolation systems deliver measurable benefits.

- For instance, in March 2025, TIS, a global leader in seismic isolation systems, provided proven earthquake resilience technology to data centers located in Chile, one of the most seismically active regions. Having proven their success in Türkiye, the friction pendulum seismic isolators have been installed in three data center projects in the Santiago Metropolitan area.

This trend is opening new seismic isolation systems market opportunities driven by the growth of critical infrastructure and rising expectations for operational resilience.

Seismic Isolation Systems Market Segmental Analysis :

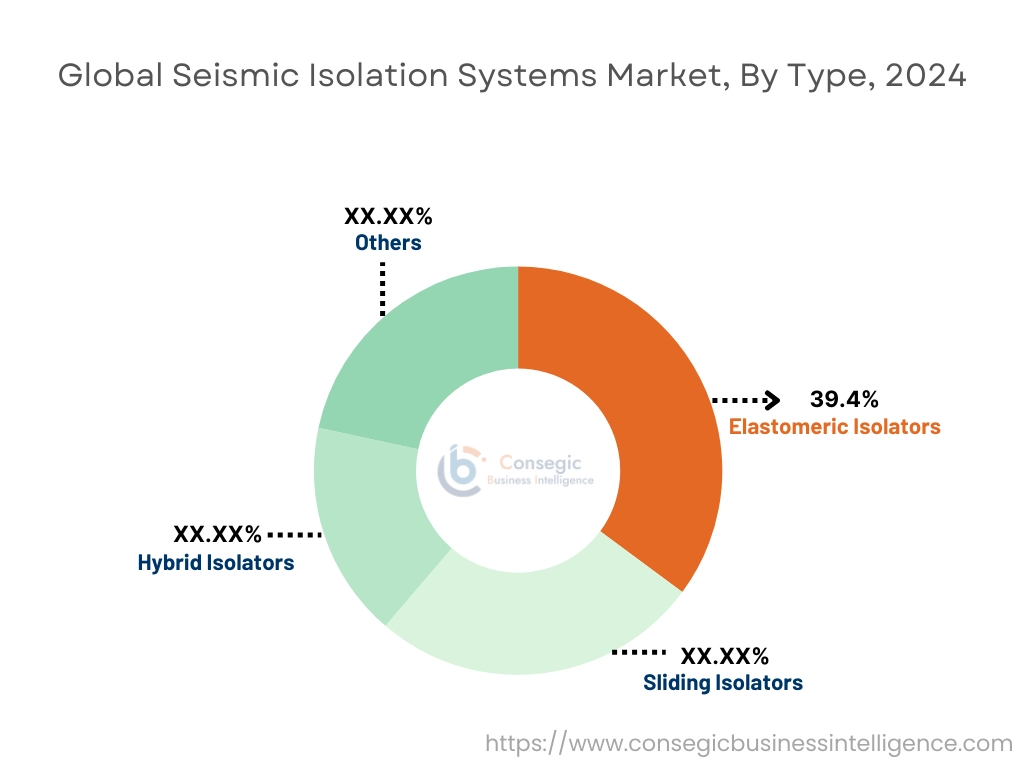

By Type:

Based on type, the market is divided into elastomeric isolators, sliding isolators, hybrid isolators, and others.

The elastomeric isolators segment accounted for the largest seismic isolation systems market share of 39.4% in 2024.

- Elastomeric isolators use rubber as the primary material for absorbing seismic energy, which makes them cost-effective and highly efficient in mitigating earthquake-induced vibrations.

- These isolators are commonly used in both residential and commercial buildings for protection against ground shaking.

- The elastomeric segment dominates due to the widespread use of rubber-based materials, which offer excellent flexibility and long-term performance.

- As per seismic isolation systems market analysis, elastomeric isolators remain the dominant segment due to their proven performance and ease of installation.

The hybrid isolators segment is expected to register the fastest CAGR during the forecast period.

- Hybrid isolators combine the benefits of elastomeric and sliding isolators, offering higher flexibility and better damping capacity for structures located in high-risk seismic zones.

- These isolators are used in more complex structures like high-rise buildings, bridges, and critical infrastructure.

- Hybrid isolators offer enhanced performance under both vertical and horizontal forces, making them ideal for buildings with variable structural designs.

- According to seismic isolation systems market trends, demand for hybrid systems is increasing due to their ability to provide higher protection across diverse construction projects.

By Material:

Based on material, the seismic isolation systems market is segmented into rubber, steel, polymers, composite materials, and others.

The rubber segment held the largest revenue share in 2024.

- Rubber-based systems are preferred for their flexibility, durability, and ability to absorb energy efficiently, especially in residential and commercial applications.

- Rubber materials, such as natural rubber and synthetic elastomers, are used extensively in elastomeric bearings and isolators.

- The segment benefits from the long lifespan, ease of manufacturing, and cost-effectiveness of rubber, which makes it an attractive option for seismic protection in various sectors.

- As per seismic isolation systems market analysis, rubber remains the most widely used material in seismic isolators, particularly in building and infrastructure applications.

The composite materials segment is expected to witness the fastest CAGR during the forecast period.

- Composite materials, such as fiberglass and carbon fiber-reinforced polymers, offer superior strength-to-weight ratios and enhanced performance in dynamic conditions.

- These materials are increasingly being used in hybrid and advanced isolator systems due to their excellent damping properties and high resistance to environmental factors.

- The adoption of composite materials is rising in high-end commercial buildings and critical infrastructure projects, where they provide higher performance and durability.

- Thus, composites are driving the seismic isolation systems market expansion as they offer advanced solutions for complex engineering challenges.

By End-Use:

Based on end-use, the market is categorized into residential, commercial, and industrial.

The commercial segment accounted for the largest seismic isolation systems market share in 2024.

- Commercial buildings, such as offices, shopping malls, and hotels, are adopting seismic isolation systems to protect against earthquake risks, especially in earthquake-prone regions.

- The increasing awareness of seismic risks in urban areas and the need for robust building codes are driving the widespread adoption of seismic isolation in commercial structures.

- Seismic isolators in commercial buildings not only protect the structure but also minimize downtime and operational losses during seismic events.

- Hence, the commercial sector continues to lead the need for advanced seismic protection systems, driven by infrastructure development and regulatory changes, propelling the seismic isolation systems market growth.

The residential segment is projected to grow at a rapid CAGR during the forecast period.

- With rising urbanization and a growing focus on building safety, the residential adoption is increasing, especially in areas with frequent seismic activity.

- Homeowners and residential developers are increasingly incorporating seismic isolation technologies to ensure the protection of life and property during earthquakes.

- The use of cost-effective elastomeric isolators in residential buildings makes them a viable option for residential construction, especially in regions like Japan, California, and Chile.

- According to seismic isolation systems market trends, the residential market is expanding rapidly, particularly in regions with high seismic risks and stricter building regulations.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

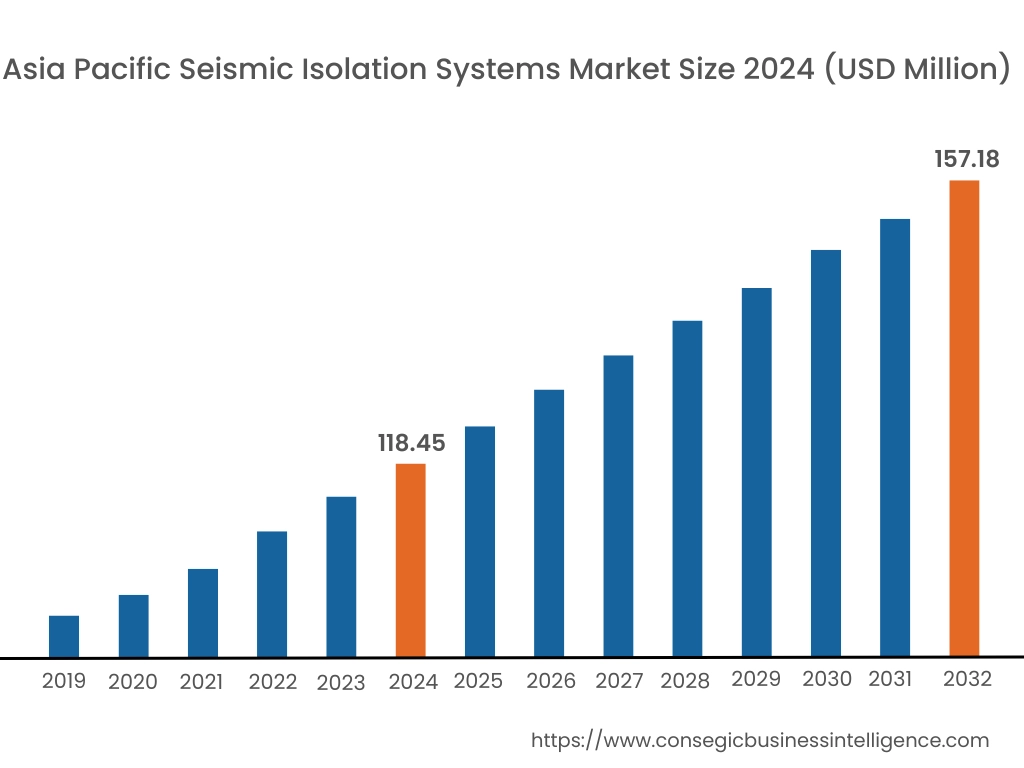

Asia Pacific region was valued at USD 118.45 Million in 2024. Moreover, it is projected to grow by USD 120.43 Million in 2025 and reach over USD 157.18 Million by 2032. Out of this, China accounted for the maximum revenue share of 34.3%. Asia-Pacific leads the global seismic isolation systems industry in scale and innovation, driven by high seismic activity and large-scale urban development. Japan is a global leader in isolation technology, widely applying systems in residential towers, commercial buildings, and transportation infrastructure. Market analysis shows robust need in China, South Korea, and Taiwan, where national policies support seismic safety through mandatory engineering codes and public-private investment. India and Southeast Asia are gradually expanding adoption, particularly in high-rise and industrial projects. The region’s seismic isolation systems market demand is fueled by growing public awareness, dense urbanization, and the proliferation of high-value infrastructure in seismically active zones.

North America is estimated to reach over USD 167.30 Million by 2032 from a value of USD 133.41 Million in 2024 and is projected to grow by USD 135.00 Million in 2025. In North America, the seismic isolation systems market is advancing steadily, particularly in earthquake-prone regions along the western United States and Canada. Adoption is concentrated in critical infrastructure such as hospitals, emergency response centers, and bridges. Market analysis shows that public safety standards and building code updates are key factors driving system implementation. Growth in this region is supported by collaboration between engineering institutions and local governments to promote the use of base isolators and damping devices in both retrofitting and new construction. Seismic isolation systems market demand continues to rise with increased investment in urban resiliency projects and long-term infrastructure modernization efforts.

Europe exhibits consistent adoption of seismic isolation technologies in southern and eastern countries with higher seismic risk, such as Italy, Greece, and Romania. Market analysis indicates that preservation of cultural heritage buildings and infrastructure safety are primary application areas, with base-isolated retrofits being incorporated into historical structures and civic facilities. Northern and western regions also show selective requirement in high-value facilities like data centers and research laboratories. The seismic isolation systems market opportunity in Europe is enhanced by EU-driven funding programs that prioritize risk reduction, along with stringent building performance standards and increasing public-sector interest in lifecycle-based construction solutions.

Latin America is progressively adopting seismic protection technologies in response to historical earthquake events and growing urban populations. Countries like Mexico, Chile, and Peru are enhancing regulatory frameworks and incorporating seismic isolation systems into government buildings, schools, and hospitals. Market analysis indicates that although cost sensitivity remains a factor, demand is increasing in areas where public safety and disaster preparedness are central to infrastructure strategy. The market potential is expanding as regional authorities recognize the long-term savings associated with structural damage mitigation and uninterrupted operational continuity during seismic events.

In the Middle East and Africa, the adoption of seismic isolation systems is emerging, particularly in countries such as Turkey, Iran, and parts of North and East Africa. Market analysis reveals that infrastructure in high-risk seismic zones is beginning to incorporate base-isolated foundations and elastomeric bearings, particularly in bridges, high-rise buildings, and healthcare infrastructure. While broader market penetration is limited due to funding constraints, pilot projects supported by international organizations and disaster resilience programs are helping drive early adoption. Growth in this region is expected to increase as building regulations evolve and construction priorities shift toward long-term risk mitigation and durability.

Top Key Players and Market Share Insights:

The seismic isolation systems market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global seismic isolation systems market. Key players in the seismic isolation systems industry include -

- Bridgestone Corporation (Japan)

- Freyssinet SAS (France)

- Zhenjiang Huayu Seismic Isolation Equipment Co., Ltd. (China)

- Toyo Tire Corporation (Japan)

- OILÉS Corporation (Japan)

- Maurer SE (Germany)

- Kawakin Core-Tech Co., Ltd. (Japan)

- Dynamic Isolation Systems, Inc. (USA)

- Earthquake Protection Systems, Inc. (USA)

- Hirun International Co., Ltd. (China)

Recent Industry Developments :

Partnerships:

- In September 2024, Structural Technologies, in collaboration with Pullman and Tough Leaf, worked on the seismic retrofits to the McGraw St Bridge in Seattle, United States, as part of the Levy to Move Seattle program. This included installation of carbon fiber wrapping, the CSS V-Wrap™ system, by Pullman, to the bridge deck and columns for increased seismic resistance. Additionally, the existing arch was strengthened with concrete infilling and cracks and damaged concrete were replaced at both ends of the bridge.

Seismic Isolation Systems Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 516.21 Million |

| CAGR (2025-2032) | 3.2% |

| By Type |

|

| By Material |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Seismic Isolation Systems Market? +

Seismic Isolation Systems Market size is estimated to reach over USD 516.21 Million by 2032 from a value of USD 402.18 Million in 2024 and is projected to grow by USD 407.76 Million in 2025, growing at a CAGR of 3.2% from 2025 to 2032.

What specific segmentation details are covered in the Seismic Isolation Systems Market report? +

The Seismic Isolation Systems market report includes specific segmentation details for type, material and end-use.

What are the end-use of the Seismic Isolation Systems Market? +

The end-use of the Seismic Isolation Systems Market are residential, commercial, and industrial.

Who are the major players in the Seismic Isolation Systems Market? +

The key participants in the Seismic Isolation Systems market are Bridgestone Corporation (Japan), Freyssinet SAS (France), Maurer SE (Germany), Kawakin Core-Tech Co., Ltd. (Japan), Dynamic Isolation Systems, Inc. (USA), Earthquake Protection Systems, Inc. (USA), Hirun International Co., Ltd. (China), Zhenjiang Huayu Seismic Isolation Equipment Co., Ltd. (China), OILÉS Corporation (Japan) and Toyo Tire Corporation (Japan).