- Summary

- Table Of Content

- Methodology

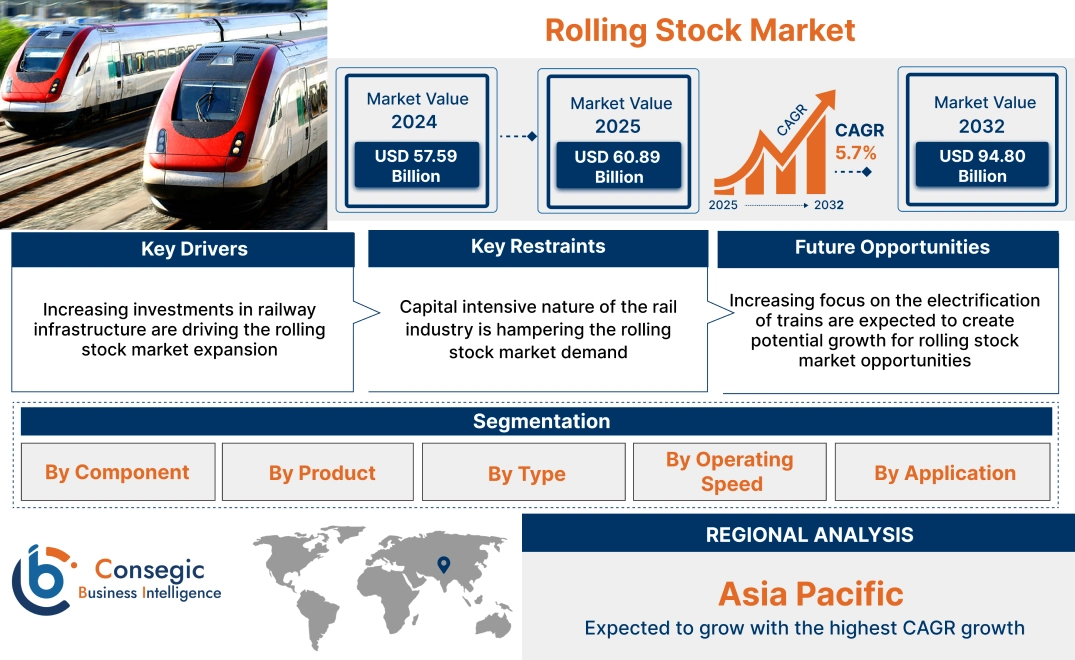

Rolling Stock Market Size:

Rolling Stock Market Size is estimated to reach over USD 94.80 Billion by 2032 from a value of USD 57.59 Billion in 2024 and is projected to grow by USD 60.89 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Rolling Stock Market Scope & Overview:

The term rolling stock is utilized in the railway transportation industry to denote any vehicle capable of moving on railroads. This encompasses both powered vehicles, such as locomotives, and unpowered vehicles, including freight wagons and passenger coaches, among others. Further, technological advancements have enabled the design and production of energy-efficient rolling stock. For instance, contemporary electric locomotives utilize regenerative braking, which recovers energy lost during braking and stores it in onboard batteries. This stored energy can subsequently power the train, thereby decreasing overall energy consumption and costs. Additionally, innovations like computer vision and artificial intelligence are enhancing the safety of rail transportation. For instance, automated or driverless trains operate without a driver, functioning autonomously while being monitored or controlled from a central control station.

Rolling Stock Market Dynamics - (DRO) :

Key Drivers:

Increasing investments in railway infrastructure are driving the rolling stock market expansion

The rising investments in railway infrastructure are having a significant impact on the growth of the rolling stock market. As these investments increase, there is a heightened emphasis on transforming rolling equipment. This modernization includes upgrading locomotives with improving passenger comfort in coaches, more powerful engines, and enhancing braking systems. Additionally, it encompasses the adoption of environmentally friendly solutions, such as alternative fuels rolling equipment solutions or electric trains. The increased investments in railway infrastructure also facilitate the development of railway networks, subsequently driving demand for rolling equipment. This expansion necessitates the procurement of new locomotives, coaches, and wagons to accommodate the need for a larger network. Furthermore, infrastructure upgrades, such as track improvements that reduce curvature or the installation of upgraded signaling systems, are also contributing to the market.

- For instance, in March 2023, Siemens Mobility revealed the investment of USD 220 billion into North Carolina rail manufacturing facility. The facility will generate over 500 new jobs and become one of the largest employers in the city. With enhanced production capacity, the company will meet the rising need for passenger rail in America by manufacturing most sustainable and innovative passenger trains in the North American market.

Thus, according to the rolling stock market analysis and trends, the increase in investments in rail infrastructure is driving the rolling stock market size.

Key Restraints:

Capital intensive nature of the rail industry is hampering the rolling stock market demand

High capital investments associated with rolling equipment manufacturing and railway infrastructure development may impede market growth in the future. Additionally, rising costs related to technology integration could adversely impact market progression. The competitive landscape within the market will further exert pressure on cost optimization. The buying behavior of rail customers is frequently characterized by various factors, including mode of transport, choice of carrier, and, most notably, price. These elements contribute to significant cost control, influencing rolling stock manufacturing activities.

Further, stringent regulatory environment may impact the growth of the rolling stock market during the forecast period. Such regulations require rail companies to compete fairly and effectively, presenting additional challenges. Decarbonization trends, driven by increased awareness of reducing carbon emissions, will promote the electrification of trains in the future. However, this shift will necessitate further capital investment, thereby affecting the rolling stock market growth.

Future Opportunities :

Increasing focus on the electrification of trains are expected to create potential growth for rolling stock market opportunities

The popularity of electric trains is increasing rapidly due to their numerous advantages. These trains do not require high-grade coal and do not produce coal dust. Unlike diesel locomotives, which often require time to warm up due to the internal combustion engine, electric trains are not affected by such delays and have shorter repair and maintenance times compared to other locomotives. The operational and maintenance costs of electric trains are notably lower than those of diesel locomotives. Their large capacity and ease of scheduling make electric trains particularly well-suited for alleviating traffic congestion in urban and suburban areas. Additionally, electric trains are less complex, more reliable, and environmentally friendly. They are generally not prone to sudden and temporary overloading, as the system can draw additional energy from the supply network. Moreover, electric trains can utilize a regenerative braking system, promoting energy efficiency. With a lower center of gravity relative to steam locomotives, electric trains can navigate curves at higher speeds more effectively.

- For instance, in November 2024, Indian Railways has electrified nearly 97% of its Broad-Gauge network. This marks a substantial improvement from the period of 2004 to 2014, during which the electrification rate averaged approximately 1.42 kilometres per day. In the fiscal year 2023–2024, this rate rose to approximately 19. 7 kilometres per day.

Thus, based on the above analysis and trends, the increasing electrification in rolling stocks is driving the rolling stock market opportunities.

Rolling Stock Market Segmental Analysis :

By Component:

Based on the component, the market is segmented into pantograph, axle, wheelset, traction motor, auxiliary power system, air conditioning system, passenger information system, position train control, brakes, gearboxes, train control systems, couplers, and others.

Trends in the component:

- The increasing focus on reducing energy consumption through lightweight materials, braking systems, and aerodynamics design.

- The increasing competition among rolling stock manufacturers is resulting in innovations and cost reductions.

Pantograph segment accounted for the largest revenue share in the year 2024 and is expected to register the highest CAGR during the forecast period.

- Pantographs are being designed with aerodynamics to reduce wind resistance and enhance energy efficiency.

- The increased speeds necessitate more robust and reliable pantographs that can maintain contact with the overhead wire at higher velocities.

- The global shift towards railway electrification is fuelling the demand for more efficient and dependable pantographs.

- The incorporation of sensors and electronics facilitates the monitoring of pantograph performance, prediction of maintenance requirements, and optimization of energy consumption.

- For instance, in November 2024, Wabtech announced the acquisition of Kompozitum and Fanox, a relay and pantograph companies. With the acquisition of Fanox, Wabtec's positioned as a market participant in the manufacture of relays for train operations and several industrial applications. Additionally, the incorporation of Kompozitum enables Wabtec to enhance the quality, manufacturing efficiency, and competitiveness of its market-leading pantograph portfolio, while also unlocking new markets for its graphite and carbon solutions.

- These trends, factors, analysis, and developments in the pantograph segment would further drive the rolling stock market size during the forecast period.

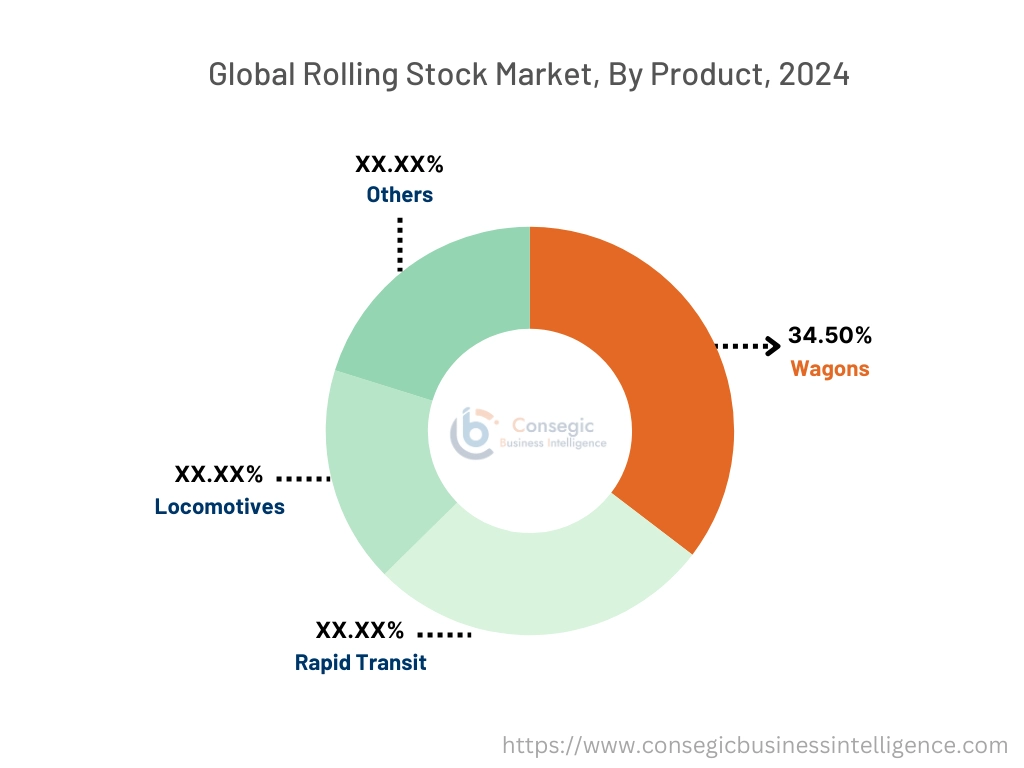

By Product:

Based on the product, the market is segmented into locomotives, wagons, rapid transit, and others.

Trends in the product:

- The rapid urbanization and population growth are escalating the demand for efficient and sustainable transportation systems in numerous countries. Railways are viewed as a feasible solution for reducing congestion and carbon emissions. Consequently, there is a rising demand for rolling stock to serve expanding metropolitan areas and cater to a growing number of passengers.

- The implementation of remote assistance and predictive maintenance solutions allows OEMs to offer enhanced service models, improving the reliability of the committed provision of the available rolling stock fleet and facilitating this progress.

The wagons segment accounted for the largest revenue share of 34.50% in the year 2024.

- The factors such as the growing need for high speed, affordability, and comfortable travel make it preferred choice of public transport option by the increasing urban population.

- Additionally, rising investments by key market players in the automation and digitalization of wagon components are further contributing to the segment progress.

- Both government and private entities favour the use of wagons for domestic and international goods movement, owing to their capacity to transport large volumes. Wagons are both cost-effective and dependable for short and long-distance transit. Worldwide, governments and private sectors are either investing in new wagon fleets or refurbishing their current ones.

- For instance, in January 2025, Titagarh Rail Systems, a rolling equipment manufacturer, targeted a production of 1,000 wagons per month in the freight segment. Further, the company has established long-term contracts with BHEL for the provision of 1,280 Vande Bharat train coaches. The initial delivery of the Vande Bharat train is expected by December 2025 or January 2026.

- Thus, focus on comfortable travel position and rising investments in rail facilities further supplement the global market during the forecast period.

The rapid transit segment is anticipated to register the fastest CAGR during the forecast period.

- The ongoing urbanization resulting in the development of cities and towns is expected to generate opportunities for rail manufacturers.

- Furthermore, the rise in urbanization is prompting government authorities to initiate public transport projects for rapid transit vehicles, such as passenger rails and metros, which is driving increased investment in rapid transit rolling equipment and its infrastructure.

- Thus, increasing investments by government authorities is driving the global market during the forecast period.

By Type:

Based on the type, the market is segmented into electric and diesel.

Trends in the type:

- The advancement of hybrid systems that integrate diesel and electric power, providing the versatility of diesel while lowering emissions.

- The progress of high-capacity batteries for electric and hybrid locomotives, enhancing their range and performance.

The diesel segment accounted for the largest revenue share in the year 2024.

- The factors such as cost-effectiveness, easy accessibility, and reduced volatility of diesel engines are driving the segment.

- Further, the rising need for improved freight transport and the low rate of diesel-to-electric conversions have enabled this segment to propel the rolling stock market.

- Additionally, the rising requirements for improved freight transport and the low rate of diesel-to-electric conversions have enabled this segment to drive the global market.

- Several leading manufacturers are creating turbocharged diesel vehicles to meet the growing need for efficient diesel-powered options. Their capability to haul freight trains laden with heavy goods makes them highly utilized for industrial purposes due to their high-torque engines.

- For instance, in June 2024, Nexrail introduced diesel and battery hybrid locomotives for shunting operations in Europe. These hybrid locomotives are engineered to facilitate the shift toward sustainable rail transport in France, Belgium, Luxembourg, and Germany. The hybrid locomotive integrates a Stage V diesel engine with a 74kWh traction battery, delivering a peak power output of 560kW. This hybrid technology enables operators to decrease fuel consumption and CO2 emissions by 20 to 30 percent.

- Thus, rise in technological innovations in diesel locomotives would further supplement the global market during the forecast period.

The electric segment is anticipated to register the fastest CAGR during the forecast period.

- The growing awareness of environmental pollution is further promoting the adoption of electric vehicles for transportation. In response, countries are increasing the production of electric rolling equipment and establishing service centers through collaboration between governments and manufacturers.

- Electric trains are considerably more energy-efficient than diesel locomotives, resulting in lower operating costs and decreased energy consumption.

- Thus, continued development in technology, coupled with growing environmental concerns and the need for more sustainable transportation solutions are contributing the continuous development in the rolling stock market share.

By Operating Speed:

Based on the operating speed, the market is segmented into less than 80 km, 80 km to 200 Km, and above 200 Km.

Trends in the operating speed:

- The growing focus on ensuring consistent and reliable operating speeds to enhance passenger satisfaction and operational efficiency.

- The advancement of rolling equipment and infrastructure which are capable of seamless operation across various rail networks, enabling quicker and more efficient intercity and international travel.

80 km to 200 km segment accounted for the largest revenue share in the year 2024 and is expected to register the highest CAGR during the forecast period.

- The growing need for faster and more efficient freight transport, particularly for time-sensitive goods is boosting the segment during the forecast period.

- The upgradation of existing rail lines to allow for higher operating speeds while ensuring safety and reliability is also propelling the segment.

- These trends, factors, and developments in the 80 km to 200 km segment would further drive the global market during the forecast period.

By Application:

Based on the application, the market is segmented into passenger and freight.

Trends in the application:

- The advancement of interoperable rolling equipment and infrastructure to enable seamless travel across various rail networks is creating a need for rolling equipment.

- The continual investment in modernization of rail infrastructure, encompassing high-speed rail lines, and urban rail systems is contributing the segment progression during the forecast period.

Freight segment accounted for the largest revenue share in the year 2024.

- The freight segment plays a crucial role in the global supply chain, as its capacity to transport high-volume goods both internationally and domestically makes it a preferred alternative to road transport.

- The digitalization of freight presents rail operators with substantial opportunities for enhancing operating safety and productivity, thereby improving their professional appeal and working conditions.

- For instance, in February 2023, members of the French Rail Freight of the Future (4F) coalition initiated the MONITOR project. This project includes equipping rail cars with sensors designed to detect derailments and improper brake applications, thereby decreasing the time required for train preparations.

- Thus, the global requirement for supply chain across the globe would further supplement the global market during the forecast period.

Passenger segment is anticipated to register the fastest CAGR during the forecast period.

- The growing emphasis on delivering comfortable, efficient, and sustainable transportation solutions is driving the need for passenger coach sector.

- Rapid urbanization is resulting in increased passenger volumes on urban transit systems, prompting the acquisition of modern and technologically advanced passenger coaches, thereby stimulating the segment development.

- The development of high-speed rail networks and the rising need for intercity travel are enhancing the need for innovative and high-performance passenger rolling equipment.

- Thus, continued development in high-speed rail networks are contributing the continuous development in the rolling stock market share.

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

Asia Pacific rolling stock market expansion is estimated to reach over USD 34.13 billion by 2032 from a value of USD 20.03 billion in 2024 and is projected to grow by USD 21.24 billion in 2025. Out of this, the Chinese market accounted for the maximum revenue split of 30.89%. Emerging economies like China and Taiwan are consistently investing in advanced trains to enhance their transportation services. Additionally, manufacturers in the region are backing government initiatives aimed at upgrading transportation systems. The increasing need has led governments to implement trams and widely adopt electric locomotives. These initiatives also allow the countries to achieve economies of scale with their existing railway manufacturing infrastructure. These factors and analysis would further drive the regional market during the forecast period.

- For instance, in January 2023, Siemens Mobility announced the partnership with Indian Railways, to provide 1,200 locomotives with a horse power of 9,000. Siemens Mobility will design, develop, assemble, and conduct testing for the trains. The contract includes 35 years of comprehensive maintenance, with deliveries planned over an 11-year timeframe. The trains will be assembled at the Gujarat, India.

North America market is estimated to reach over USD 24.86 billion by 2032 from a value of USD 15.26 billion in 2024 and is projected to grow by USD 16.13 billion in 2025. The integration of advanced technologies into rolling equipment significantly drives the regional market. Digitalization, automation, and predictive maintenance systems are transforming the railway sector. For instance, predictive maintenance allows operators to proactively manage maintenance needs, leading to reduced downtime and enhanced efficiency in rolling equipment operations. Additionally, the adoption of digital signaling and communication systems improves safety and operational efficiency. High-speed trains, an expanding segment in the region, are advancing technology adoption, while necessitating sophisticated systems for passenger comfort, speed, and safety. These technological innovations not only appeal to buyers seeking modern solutions but also foster innovation within the sector. These factors would further drive the regional market during the forecast period.

- For instance, in February 2023, Stadler Rail AG announced the collaboration with Utah State University and ASPIRE Engineering Research Center, for the construction of trains powered by batteries on the FLIRT Akku idea. The partnership encompasses the enhancement and evaluation of a FLIRT Akku battery-operated train. The subsequent test runs will concentrate on providing insights for the decarbonization of American passenger transit with battery-powered trains.

According to the rolling stock industry analysis, the European market progress can be attributed to the increasing interest in alternative propulsion technologies, such as hydrogen fuel cells and battery-electric trains.. Further, the growing industrial mining activities and urban population globally are significant factors contributing to the need for rapid trams, local passenger trains, and fast metro trains. There is a growing preference for public transportation among individuals due to its ability to alleviate road congestion while providing a time-efficient, comfortable, and economical means of transit. Additionally, economic development in several

Latin American countries has resulted in heightened freight traffic, especially for commodities such as minerals, agricultural products, and manufactured goods. This situation has generated a requirement for freight locomotives, wagons, and other rolling equipment. Furthermore, the energy sector is the largest consumer of rolling equipment in the Middle East region. Wagons are the primary rail vehicles utilized for transporting oil within this industry. Additionally, advantages such as reliability, safety, and cost-effectiveness are likely to drive the region's adoption of rolling equipment for goods transportation. The need for electric locomotives and locomotives equipped with turbochargers is anticipated to rise significantly due to the increasing need for energy-efficient rail vehicles in the region. Thus, according to the above rolling stock market analysis and trends, these factors would further drive the regional market during the forecast period.

Top Key Players and Market Share Insights:

The global rolling stock market is highly competitive with major players providing solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the rolling stock industry includes-

- Alstom Transport (France)

- CRRC Corporation Limited (China)

- The Greenbrier Co. (U.S.)

- Trinity Rail (U.S.)

- Stadler Rail AG (Switzerland)

- ABB Ltd. (Switzerland)

- Hitachi Rail System (U.K.)

- GE Transportation (U.S.)

- Hyundai Rotem (South Korea)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Siemens Mobility (Germany)

Recent Industry Developments :

Expansion:

- In October 2024, Alstom announced that it would provide 12 train sets to Proxima, the French high speed rail operator. Alstom would provide double-decker high-speed trains, which are projected to be delivered by 2028 for operation on the Atlantic lines.

Rolling Stock Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 94.80 Billion |

| CAGR (2025-2032) | 5.7% |

| By Component |

|

| By Product |

|

| By Type |

|

| By Operating Speed |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Rolling Stock market? +

Rolling Stock Market Size is estimated to reach over USD 94.80 Billion by 2032 from a value of USD 57.59 Billion in 2024 and is projected to grow by USD 60.89 Billion in 2025, growing at a CAGR of 5.7%from 2025 to 2032.

Which is the fastest-growing region in the Rolling Stock market? +

Asia-Pacific is the region experiencing the most rapid growth in the market. The regional growth can be attributed to the increase in allocation of the budget for development of railways, rise in demand for secure, safe, & efficient transport, and increase in use of public transportation.

What specific segmentation details are covered in the Rolling Stock report? +

The rolling stock report includes specific segmentation details for material, vehicle type, sales channel, and region.

Who are the major players in the Rolling Stock market? +

The key participants in the market are Alstom Transport (France), CRRC Corporation Limited (China), Hitachi Rail System (U.K.), GE Transportation (U.S.), Hyundai Rotem (South Korea), Kawasaki Heavy Industries, Ltd. (Japan), Siemens Mobility (Germany), Stadler Rail AG (Switzerland), The Greenbrier Co. (U.S.), Trinity Rail (U.S.), ABB Ltd. (Switzerland), and others.