- Summary

- Table Of Content

- Methodology

Rock Breaker Market Size:

Rock Breaker Market size is estimated to reach over USD 4.35 Billion by 2032 from a value of USD 2.89 Billion in 2024 and is projected to grow by USD 2.99 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

Rock Breaker Market Scope & Overview:

A rock breaker is a hydraulic or pneumatic attachment designed to demolish hard surfaces such as rock, concrete, and asphalt in mining, quarrying, and construction operations. Typically mounted on excavators, backhoes, or skid steers, it delivers controlled impact energy to fracture dense material efficiently.

Key components include a chisel or moil point, hydraulic piston, accumulator, and mounting bracket. Units are available in light, medium, and heavy-duty classifications depending on carrier size and application requirements.

The primary advantages of rock breakers include precision, reduced noise and vibration compared to blasting, and compatibility with multiple machines. They enable safe, efficient removal of obstructions in confined or populated environments, supporting continuous excavation without delay. With minimal setup and high impact force, they streamline material handling, contribute to faster project completion, and are an essential tool for contractors seeking productivity and reliability in tough terrain and demolition tasks.

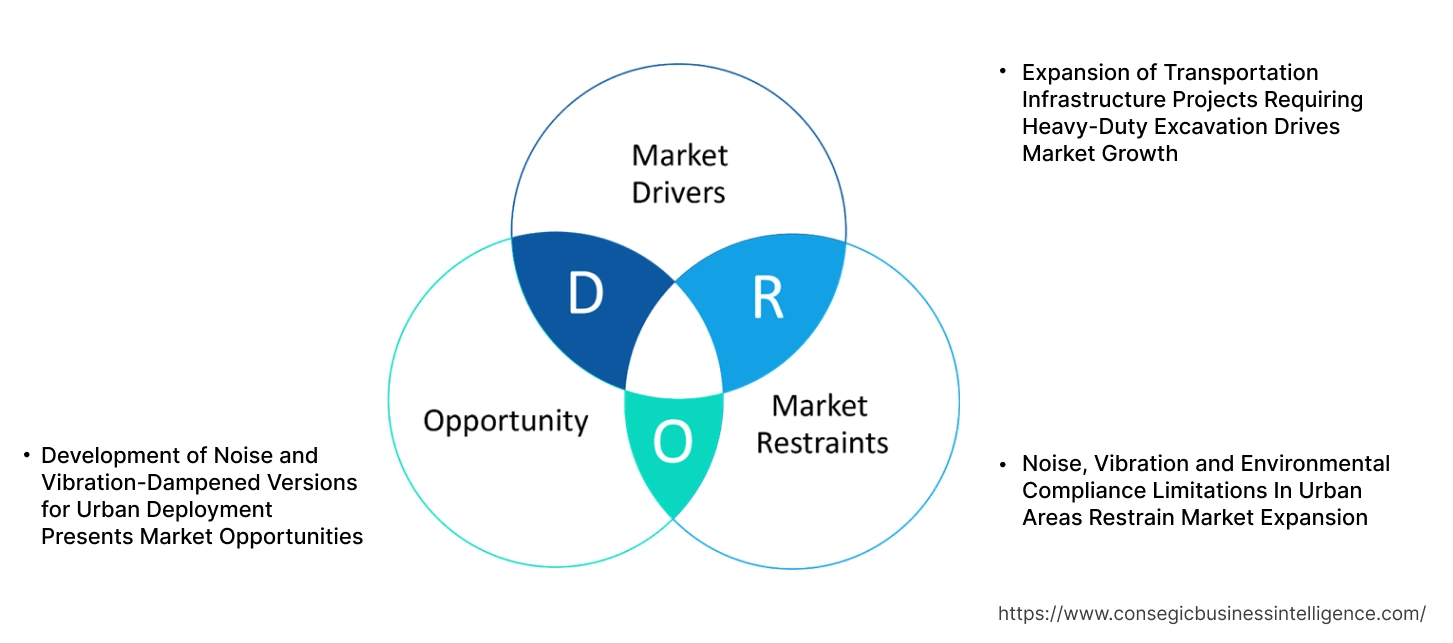

Rock Breaker Market Dynamics - (DRO) :

Key Drivers:

Expansion of Transportation Infrastructure Projects Requiring Heavy-Duty Excavation Drives Market Growth

The rise in road, railway, and metro infrastructure development is generating substantial demand for efficient rock-breaking and excavation equipment. Rock breakers are widely used for demolishing tough substrates such as boulders, concrete foundations, and bedrock layers encountered during tunnel construction, highway grading, and bridge foundation works. These attachments enhance on-site productivity by allowing faster fragmentation of oversized materials and enabling uninterrupted workflow. In large-scale infrastructure projects, their compatibility with excavators and backhoe loaders makes them indispensable across various job phases. Developing regions such as Southeast Asia, Latin America, and Africa are witnessing increased public and private investments in transportation corridors, often involving challenging terrain. These conditions create consistent need for high-impact hydraulic attachments with extended duty cycles and robust performance. As governments continue to scale up infrastructure spending globally, heavy-duty excavation requirements are contributing significantly to the rock breaker market expansion.

Key Restraints:

Noise, Vibration and Environmental Compliance Limitations In Urban Areas Restrain Market Expansion

The operation of rock breakers generates high levels of noise and vibration, posing challenges in urban settings with strict environmental and community safety regulations. Activities near residential zones, hospitals, and schools often face legal restrictions on permissible decibel levels and vibration thresholds. This restricts the use of heavy-duty hydraulic attachments in densely populated areas or sensitive zones. Furthermore, local authorities in many cities enforce work-hour limitations and project-specific noise permits, increasing operational complexity. Environmental compliance also requires dust suppression and emission control strategies, further escalating project costs. In locations where sustainable construction practices are prioritized, contractors tend to opt for less intrusive demolition alternatives. Despite rising demand for efficient excavation tools, these environmental and operational limitations continue to hinder broader rock breaker market growth in urban and regulated construction environments.

Future Opportunities :

Development of Noise and Vibration-Dampened Versions for Urban Deployment Presents Market Opportunities

Manufacturers are increasingly focusing on engineering quieter and more vibration-controlled rock breakers to address the evolving requirements of urban construction projects. Innovations such as internal dampening systems, anti-rebound buffers, and enclosed hammer housings are being integrated to significantly reduce sound emissions and operational impact. These upgrades allow contractors to meet stringent noise regulations while maintaining productivity in noise-sensitive areas. The use of advanced materials and energy-absorbing components also minimizes wear on carrier machines and enhances operator comfort. As demand rises for compact, efficient, and environmentally compliant equipment in city redevelopment, utilities, and tunneling works, these low-impact models are gaining traction. Their adoption is expanding, particularly in Europe, Japan, and urban zones in North America, where sustainable demolition practices are embedded in planning standards.

- For instance, in November 2021, Komatsu launched the new hydraulic breaker series, JMHB-V. The breakers contain rubber/poly components to absorb impact and reduce vibrations in order to minimize noise generation. Additionally, the product enables adjustable piston stroke length and speed to achieve maximum production output.

The evolution of controlled-impact technology is unlocking new rock breaker market opportunities aligned with regulatory compliance and urban infrastructure growth.

Rock Breaker Market Segmental Analysis :

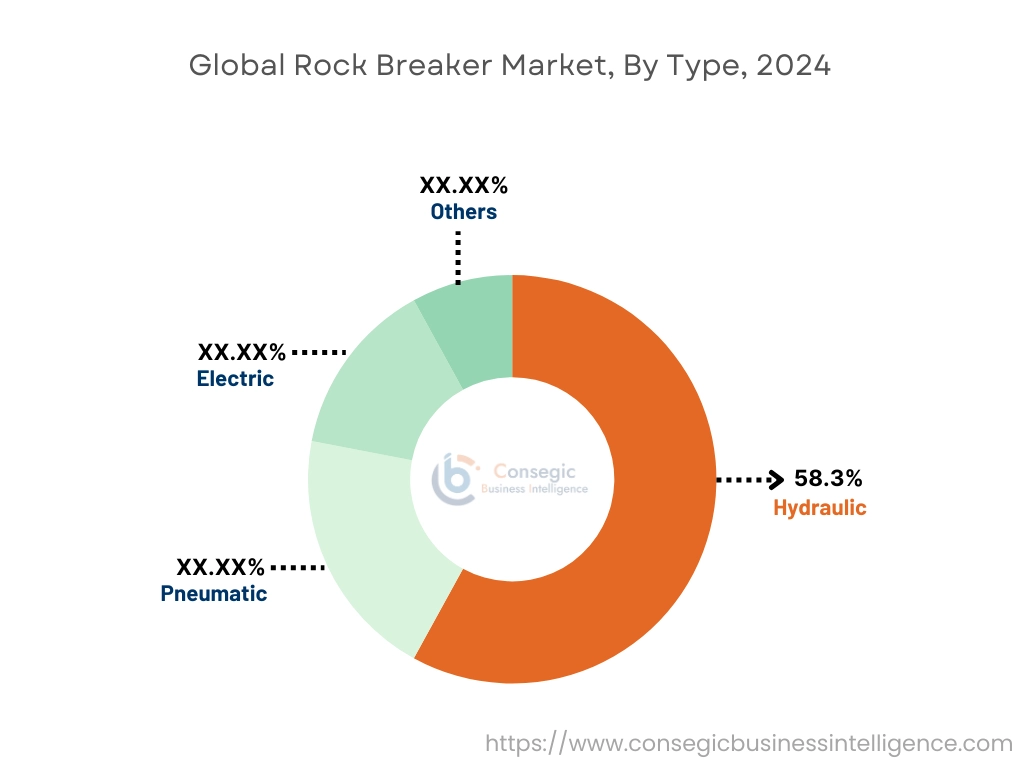

By Type:

Based on type, the market is segmented into hydraulic, pneumatic, electric, and others.

The hydraulic segment accounted for the largest revenue share of 58.3% in 2024.

- Hydraulic breakers are highly favored in construction and mining applications due to their power and efficiency in breaking tough materials.

- These systems are ideal for heavy-duty applications, providing precise control and higher impact forces compared to other types of breakers.

- They are widely used in large-scale demolition, quarrying, and tunneling projects where high-performance equipment is required.

- For instance, in October 2023, Normet entered a new market by unveiling a line of hydraulic breakers, the Normet Xrock. Ranging from 335 kg to 7250 kg, the breakers are designed for a wide variety of tasks in construction, tunneling and infrastructure.

- As per the rock breaker market analysis, the hydraulic segment continues to dominate due to its proven reliability and ability to handle large workloads.

The pneumatic segment is projected to grow at the fastest CAGR during the forecast period.

- Pneumatic rock breakers are powered by compressed air, offering a lower cost solution compared to hydraulic systems while still delivering effective breaking performance.

- These breakers are used in medium-duty applications, especially in mining and demolition projects with lower load requirements.

- Their portability, ease of use, and efficiency in rocky terrains make them popular in both industrial and construction applications.

- According to rock breaker market trends, the increasing need for lightweight and cost-effective tools drives the growth of the pneumatic versions.

By Operating Weight:

Based on operating weight, the market is segmented into below 500 kg, 500–1,000 kg, 1,000–2,000 kg, and above 2,000 kg.

The 500–1,000 kg segment held the largest rock breaker market share in 2024.

- Breakers in the 500–1,000 kg range are widely used in both construction and mining, offering a balance between power and maneuverability.

- These machines are ideal for mid-sized projects where both mobility and efficiency are required, such as medium-scale demolition or road construction projects.

- The versatility of this weight class, which allows for attachment to a variety of machinery, ensures its dominance in various industries.

- As per rock breaker market trends, the 500–1,000 kg segment remains dominant due to its flexibility and ability to meet diverse customer needs.

The above 2,000 kg segment is expected to grow at the fastest CAGR during the forecast period.

- The heavy-duty types above 2,000 kg are used in the most demanding applications, including large-scale quarrying, mining, and infrastructure development.

- These systems offer the highest impact energy and are ideal for breaking extremely hard materials such as granite or reinforced concrete.

- Their adoption is increasing due to the growing requirement for equipment capable of handling tough environments and large-scale operations.

- Thus, the heavy-duty segment is seeing strong growth as industrialization and mining activities intensify in emerging markets, driving the rock breaker market expansion.

By Application:

Based on application, the rock breaker market is segmented into demolition, quarrying, tunneling, scaling, and others.

The demolition segment accounted for the largest revenue share in 2024.

- They are extensively used in demolition for breaking down concrete structures, steel, and asphalt in urban construction projects.

- Their ability to break up large sections of concrete without damaging the surrounding area makes them essential in urban infrastructure renewal and building deconstruction.

- The segment is growing due to increasing construction and redevelopment projects in urban areas, along with a rising focus on sustainable demolition practices.

- As per rock breaker market demand, the demolition segment continues to dominate due to continuous urbanization and infrastructure redevelopment.

The quarrying segment is projected to experience the fastest CAGR during the forecast period.

- In the quarrying industry, rock breakers are used to reduce large rock sizes into manageable pieces for further processing.

- The need for efficient extraction and material processing in aggregate production is driving the adoption of high-power tools in quarrying operations.

- This segment benefits from increasing construction and road-building activities globally, which require vast quantities of stone and aggregate.

- According to the rock breaker market analysis, the quarrying segment is witnessing strong need as the global construction industry expands.

By End-Use Industry:

Based on end-use industry, the market is segmented into construction, mining, oil & gas, and others.

The construction segment held the largest rock breaker market share in 2024.

- Rock breakers are essential for various construction tasks, including site clearing, road construction, and building demolition.

- They are used in both urban and rural settings to break down hard materials quickly, making construction projects more efficient and cost-effective.

- As cities expand and infrastructure projects increase, the requirement for reliable, high-performance tools continues to rise.

- Hence, the construction segment remains dominant due to its widespread application in urbanization and infrastructure development and the significant rock breaker market demand.

The mining segment is expected to register the fastest CAGR.

- Mining operations rely heavily on them to extract minerals and metals from hard rock formations, making them crucial for the industry.

- With the global push toward increased mining productivity and environmental compliance, there is a growing adoption of high-impact machines capable of handling tough mining environments.

- The need for cost-efficient and environmentally friendly mining operations drives the growth of advanced technologies.

- For instance, in October 2022, Astec Industries’ Materials Solutions Group launched its newest mobile rock breaker, the BreakerBOSS 5D for underground mine applications. Consisting of a standard Deutz, 177 hp (132 kW), Tier 3 engine and a 5,000 foot-pound (6,800 J) BTI BXR50 hydraulic attachment, the machine is designed for heavy-duty operations.

- Thus, mining is becoming a key sector for its adoption as the requirement for minerals increases in industrial applications, bolstering the rock breaker market growth.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

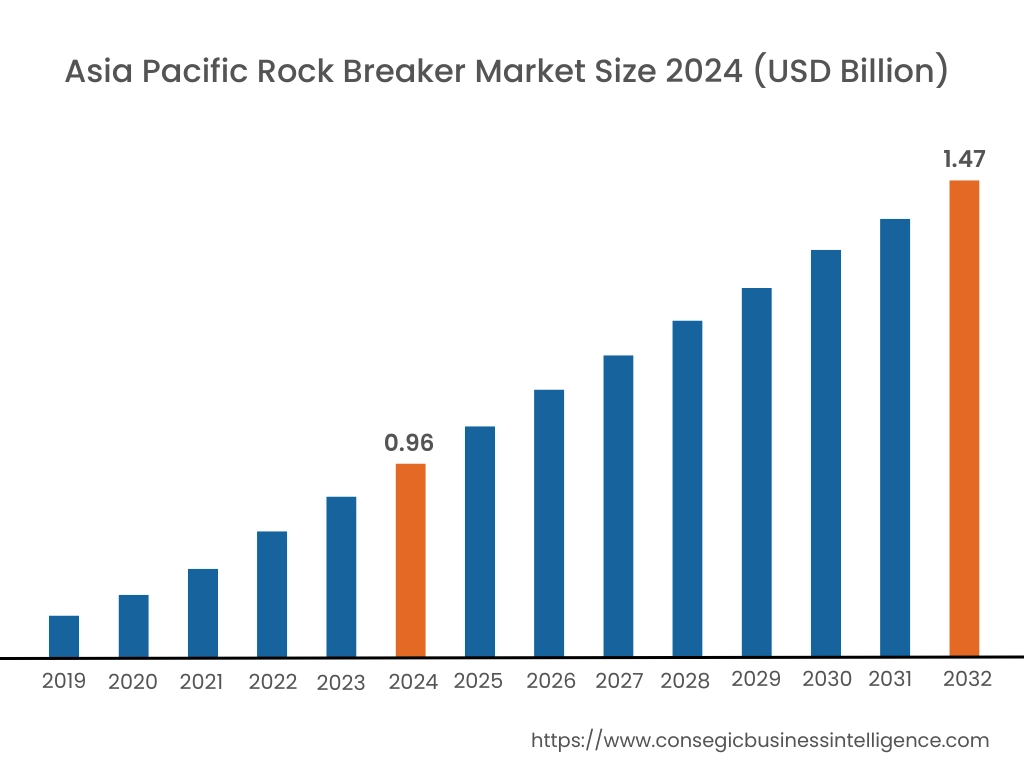

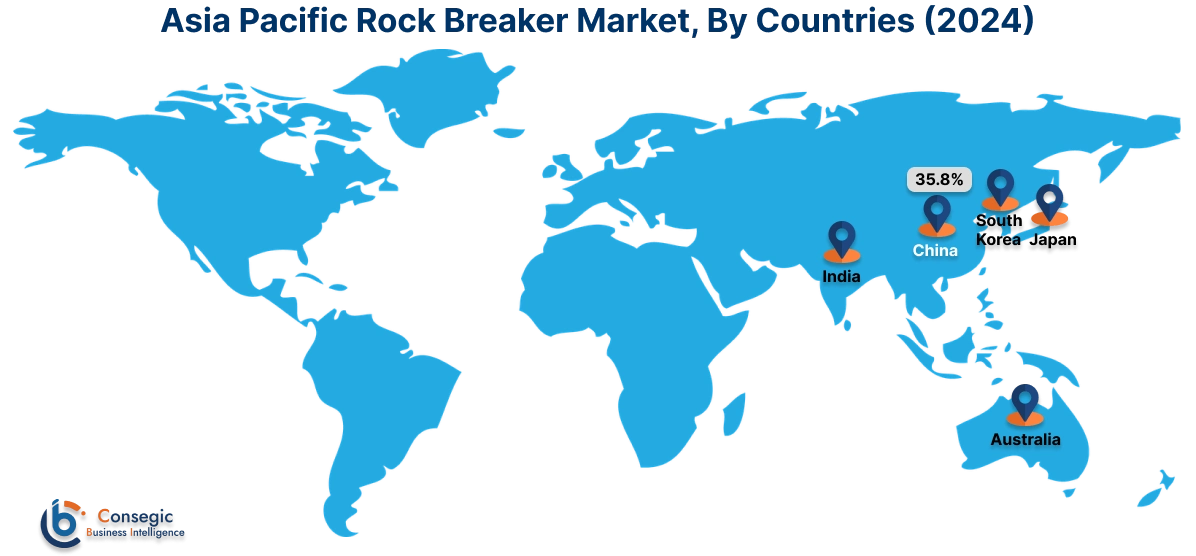

Asia Pacific region was valued at USD 0.96 Billion in 2024. Moreover, it is projected to grow by USD 1.00 Billion in 2025 and reach over USD 1.47 Billion by 2032. Out of this, China accounted for the maximum revenue share of 35.8%. Asia-Pacific is witnessing rapid growth in the rock breaker market, supported by expansive construction activities, mining operations, and public infrastructure programs. China and India lead in market size due to their aggressive investment in roads, bridges, tunnels, and mining exploration. Market analysis shows that there is robust demand for heavy-duty machines capable of withstanding intensive usage in open-pit and underground operations. Japan and South Korea focus on technologically advanced models with sensor-based performance monitoring and auto-lubrication features for extended service life. The region’s construction equipment market is also supported by strong local manufacturing ecosystems and government-led initiatives to improve mechanized excavation efficiency.

North America is estimated to reach over USD 1.28 Billion by 2032 from a value of USD 0.85 Billion in 2024 and is projected to grow by USD 0.88 Billion in 2025. In North America, the need for rock breakers remains consistent across urban infrastructure, utility excavation, and aggregate production. The United States and Canada exhibit mature markets where contractors utilize advanced hydraulic breaker systems integrated with backhoes and excavators. Market analysis highlights a rising preference for equipment with low vibration output and noise control features, especially in urban redevelopment zones. Growth in this region is propelled by large-scale transport and energy projects, alongside stringent safety regulations that favor precision-controlled demolition equipment. The ongoing shift toward electric-powered construction tools is also influencing procurement preferences among fleet operators.

Europe presents a highly standardized and regulation-sensitive market with strong requirements from civil engineering, tunneling, and quarrying activities. Countries such as Germany, France, and Italy are at the forefront of adopting low-emission, high-performance breaker attachments engineered to comply with EU environmental norms. Market analysis reveals that the increasing complexity of inner-city projects is driving the usage of compact and silent demolition systems that minimize structural disruption. The rock breaker market opportunity in Europe is supported by regional infrastructure renewal efforts, investments in underground utility development, and widespread emphasis on sustainable construction practices supported by public-sector initiatives.

Latin America shows growing adoption of rock-breaking tools, particularly in countries like Brazil, Chile, and Peru, where mining and raw material extraction are dominant industries. Market analysis indicates that hydraulic and pneumatic breakers are increasingly used for blasting-free operations in mineral zones, especially where strict environmental compliance is necessary. In the construction sector, road development and commercial site preparation are emerging as key application areas. Growth in this region is linked to the modernization of mining infrastructure, investment in port expansions, and improved accessibility to mid-sized hydraulic equipment suited for rugged terrains.

The Middle East and Africa region holds a strategic position in the rock breaker industry, driven by extensive quarrying, oilfield development, and road construction projects. In the UAE and Saudi Arabia, breakers are commonly deployed in pipeline trenching and rock excavation for mega infrastructure projects. South Africa and Kenya exhibit demand from both mining and urban expansion initiatives. Market analysis reveals that while cost sensitivity remains a challenge, the need for durable, serviceable, and impact-optimized equipment is growing. The ongoing public-private partnerships in infrastructure and increased foreign investment in mining and industrial development offer potential avenues for development and expansion.

Top Key Players and Market Share Insights:

The rock breaker market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global rock breaker market. Key players in the rock breaker industry include –

- Epiroc AB (Sweden)

- Komatsu Ltd. (Japan)

- Rammer (Sandvik Group) (Finland)

- Daemo Engineering Co., Ltd. (South Korea)

- MSB Corporation (South Korea)

- Doosan Corporation (Montabert) (South Korea / France)

- Furukawa Rock Drill Co., Ltd. (Japan)

- Atlas Copco (Sweden)

- Indeco Ind. S.p.A. (Italy)

- Socomec S.p.A. (Italy)

Recent Industry Developments :

Acquisitions:

- In September 2024, Epiroc completed the acquisition of ACB+, a French manufacturer of attachments and related couplers used by the construction industry.

- In August 2021, Epiroc acquired DandA Heavy Industries, a South Korean hydraulic breaker manufacturer, to expand its product portfolio.

Partnerships:

- In January 2025, JCB India and Shriram Automall India Limited (SAMIL) signed a Memorandum of Understanding (MOU) to better manage the sales of pre-owned JCB construction machines. This partnership aims to expand the construction machinery market without compromising on quality as well as maintain cost efficiency.

Rock Breaker Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 4.35 Billion |

| CAGR (2025-2032) | 5.2% |

| By Type |

|

| By Operating Weight |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Rock Breaker Market? +

Rock Breaker Market size is estimated to reach over USD 4.35 Billion by 2032 from a value of USD 2.89 Billion in 2024 and is projected to grow by USD 2.99 Billion in 2025, growing at a CAGR of 5.2% from 2025 to 2032.

What specific segmentation details are covered in the Rock Breaker Market report? +

The Rock Breaker market report includes specific segmentation details for type, operating weight, application and end-use industry.

What are the end-use industries of the Rock Breaker Market? +

The end-use industries of the Rock Breaker Market are construction, mining, oil & gas, and others.

Who are the major players in the Rock Breaker Market? +

The key participants in the Rock Breaker market are Epiroc AB (Sweden), Komatsu Ltd. (Japan), Doosan Corporation (Montabert) (South Korea / France), Furukawa Rock Drill Co., Ltd. (Japan), Atlas Copco (Sweden), Indeco Ind. S.p.A. (Italy), Socomec S.p.A. (Italy), Rammer (Sandvik Group) (Finland), Daemo Engineering Co., Ltd. (South Korea) and MSB Corporation (South Korea).