- Summary

- Table Of Content

- Methodology

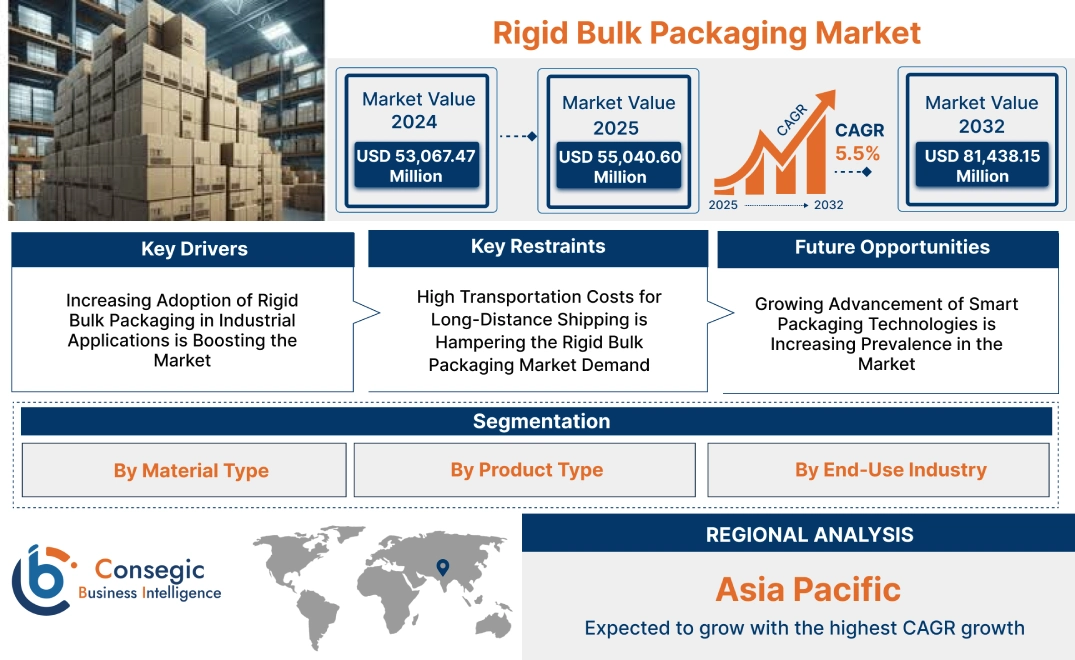

Rigid Bulk Packaging Market Size:

Rigid Bulk Packaging Market size is estimated to reach over USD 81,438.15 Million by 2032 from a value of USD 53,067.47 Million in 2024 and is projected to grow by USD 55,040.60 Million in 2025, growing at a CAGR of 5.5% from 2025 to 2032.

Rigid Bulk Packaging Market Scope & Overview:

The rigid bulk packaging are durable and reusable packaging solution designed for the safe transport and storage of bulk materials. This market includes products such as drums, intermediate bulk containers (IBCs), bulk crates, and rigid totes, which are widely used in industrial, agricultural, and chemical sectors. Key characteristics of this packaging include high strength, resistance to impact, and compatibility with a variety of materials, including liquids, powders, and granules. The benefits include improved material handling efficiency, enhanced protection against contamination, and reduced product wastage during transportation. Applications span chemicals, food and beverages, pharmaceuticals, and construction materials, where bulk handling and durability are critical. End-users include manufacturers, logistics companies, and agriculture sectors, driven by increasing industrialization, rising application for efficient logistics solutions, and advancements in packaging technologies ensuring sustainability and cost efficiency.

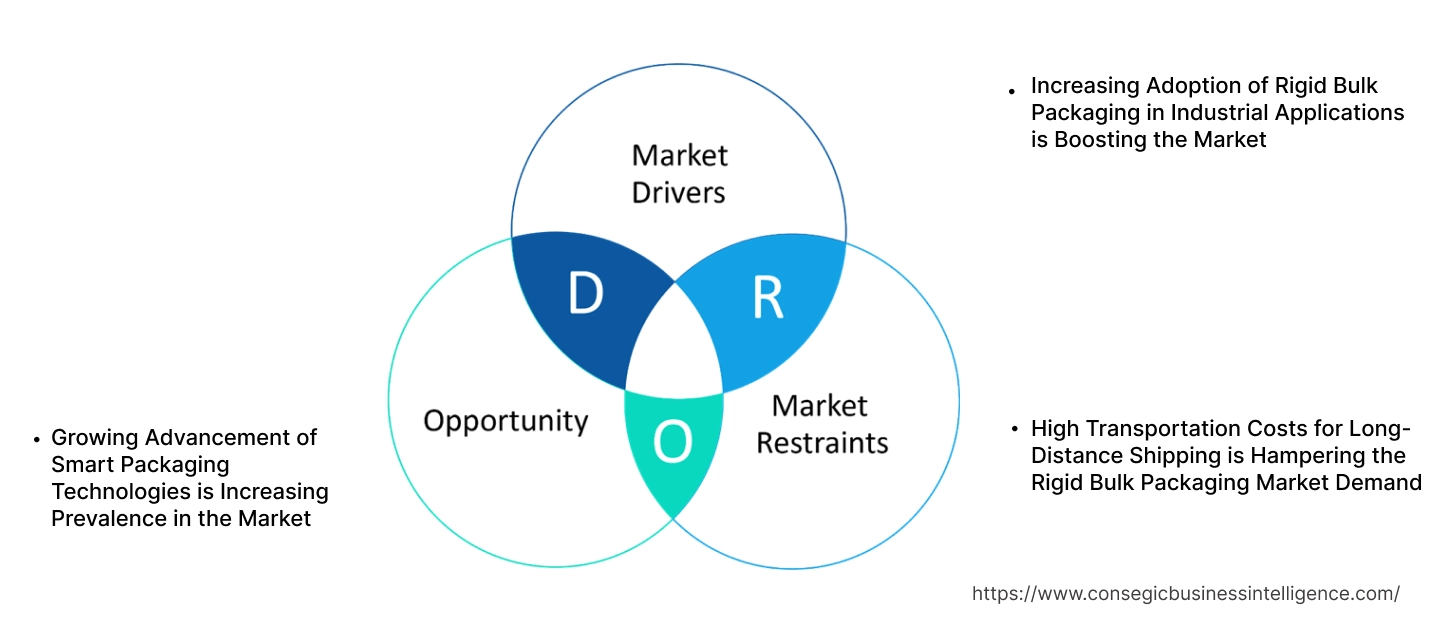

Rigid Bulk Packaging Market Dynamics - (DRO) :

Key Drivers:

Increasing Adoption of Rigid Bulk Packaging in Industrial Applications is Boosting the Market

The growing reliance on rigid bulk packaging in industries such as chemicals, food and beverage, pharmaceuticals, and manufacturing is shaping key trends in the market expansion. Products like intermediate bulk containers (IBCs), drums, and bulk bins are widely adopted for their ability to securely store and transport large volumes of liquids, powders, and granules. Their durability and resistance to extreme environmental conditions make them ideal for safeguarding goods during handling and transit.

In the chemical and pharmaceutical industries, rigid bulk packaging ensures compliance with stringent safety and hygiene standards by preventing contamination and leakage. Similarly, the food and beverage sector benefits from these solutions for storing syrups, oils, and other perishable products under controlled conditions. With businesses focusing on operational efficiency and reduced product wastage, rigid bulk packaging continues to emerge as a reliable and preferred solution across various industrial applications.

Key Restraints:

High Transportation Costs for Long-Distance Shipping is Hampering the Rigid Bulk Packaging Market Demand

While rigid bulk packaging offers exceptional durability and reliability, its size and weight contribute to high transportation costs, particularly for long-distance shipments. Containers such as metal drums and IBCs are heavier and bulkier compared to flexible alternatives, resulting in increased fuel consumption and logistical expenses. Additionally, their inability to compact during return trips adds to the overall cost, making them less efficient for industries with high shipping volumes.

These cost implications pose a significant challenge for manufacturers and distributors operating in regions with complex supply chains or distant export markets. Companies must also invest in specialized handling equipment and protocols to manage the transport of rigid bulk packaging, further increasing operational expenses. As businesses strive to optimize logistics and reduce shipping costs, addressing these challenges will be crucial for the sustained adoption of rigid bulk packaging solutions.

Future Opportunities :

Growing Advancement of Smart Packaging Technologies is Increasing Prevalence in the Market

The integration of smart technologies into rigid bulk packaging solutions is revolutionizing supply chain operations and creating new opportunities for the market. Advanced features such as RFID tags, GPS tracking, and IoT-enabled sensors are being incorporated into IBCs and bulk bins to enhance real-time monitoring of shipments. These technologies allow businesses to track the location, temperature, and humidity of goods during transportation, ensuring product safety and regulatory compliance.

Smart packaging also supports predictive maintenance by identifying potential issues with containers, such as structural weaknesses or exposure to adverse conditions. This reduces downtime and enhances operational efficiency. The adoption of these innovative solutions aligns with the increasing focus on digital transformation and automation in logistics. As industries prioritize data-driven decision-making and supply chain transparency, smart packaging technologies are expected to play a pivotal role in the evolution of rigid bulk packaging.

Rigid Bulk Packaging Market Segmental Analysis :

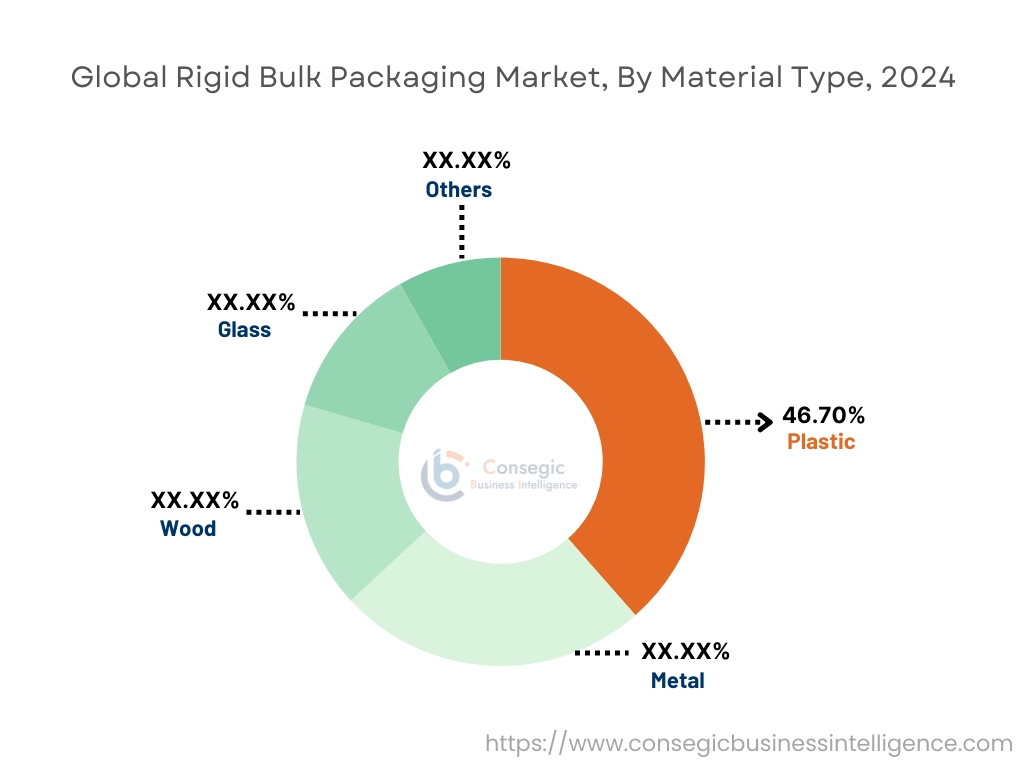

By Material Type:

Based on material type, the rigid bulk packaging market is segmented into plastic, metal, wood, glass, and others.

The plastic segment accounted for the largest revenue in rigid bulk packaging market share of 46.70% in 2024.

- Plastic dominates the market due to its lightweight nature, durability, and cost-effectiveness.

- It is extensively used in various industries, including food & beverage and e-commerce, for its adaptability in designing boxes, containers, and trays.

- The rigid bulk packaging market trends of adopting recyclable and reusable plastics is driving innovations in this segment, meeting both economic and environmental rigid bulk packaging market demands.

- Additionally, plastic’s resilience to impact and moisture makes it a preferred choice for bulk packaging solutions.

- Plastic analysis leads the market due to its versatility, cost efficiency, and alignment with the trends of adopting sustainable packaging solutions.

The glass segment is anticipated to register the fastest CAGR during the forecast period.

- Glass is increasingly being used in rigid bulk packaging, particularly in the food & beverage and pharmaceuticals industries, due to its inert nature and ability to preserve product integrity.

- The trends of using eco-friendly and recyclable materials has significantly boosted the development for glass packaging.

- Furthermore, its superior barrier properties against moisture, oxygen, and other contaminants ensure the long-term storage of sensitive products.

- Thus, according to market analysis, glass is expected to grow rapidly, driven by its eco-friendly attributes and increasing adoption in industries emphasizing product quality and sustainability, boosting the rigid bulk packaging market expansion.

By Product Type:

Based on product type, the market is segmented into boxes, trays, containers & cans, bottles & jars, pallets, and others.

The containers & cans segment accounted for the largest revenue in rigid bulk packaging market share in 2024.

- Containers & cans are widely used across industries such as chemicals, pharmaceuticals, and food & beverage for bulk storage and transportation.

- Their durability, stackability, and resistance to external damage make them ideal for high-volume packaging.

- The trends of using specialized containers with enhanced sealing capabilities to meet regulatory standards in the chemical and pharmaceutical sectors has further driven demand in this segment.

- As per the market analysis, containers & cans dominate the market growth due to their robust design and suitability for various bulk packaging applications, particularly in regulated industries.

The pallets segment is anticipated to register the fastest CAGR during the forecast period.

- Pallets are essential for logistics and supply chain operations, offering ease of handling and efficient space utilization during transportation.

- The rising trends of automating warehouses and logistics facilities has increased the demand for standardized pallets compatible with automated systems.

- Furthermore, the adoption of lightweight and reusable pallet designs in e-commerce and agriculture supports their rapid rigid bulk packaging market growth.

- As per the market analysis, pallets are expected to grow rapidly, fueled by the trends of warehouse automation and the demand for reusable, lightweight packaging solutions, fueling the rigid bulk packaging market opportunities.

By End-User Industry:

Based on end-user industry, the market is segmented into food & beverage, chemicals, electronics, e-commerce, pharmaceuticals, agriculture, and others.

The food & beverage segment accounted for the largest revenue share in 2024.

- The food & beverage companies are heavily relies on packaging to ensure the safety and freshness of perishable items during storage and transportation.

- The rigid bulk packaging market trends of adopting hygienic and tamper-proof packaging solutions has driven innovations in rigid bulk packaging for this sector.

- Additionally, the increasing oportunities focus on reducing food waste through advanced packaging technologies further boosts the demand for rigid bulk packaging in this segment.

- Food & beverage leads the market due to its critical need for preserving product quality and the rise of adopting advanced packaging solutions to ensure safety and freshness.

The e-commerce segment is anticipated to register the fastest CAGR during the forecast period.

- The e-commerce sector’s exponential growth has driven the demand for durable and protective bulk packaging solutions to handle high shipping volumes.

- The trends of adopting custom and lightweight packaging solutions to enhance operational efficiency and customer satisfaction has significantly boosted demand in this segment.

- Additionally, the increasing opportunities focus on eco-friendly and recyclable packaging in e-commerce aligns with global sustainability initiatives.

- As per the rigid bulk packaging market analysis, E-commerce is expected to grow rapidly, driven by its rising shipping volumes and the trends of adopting sustainable, protective packaging solutions.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

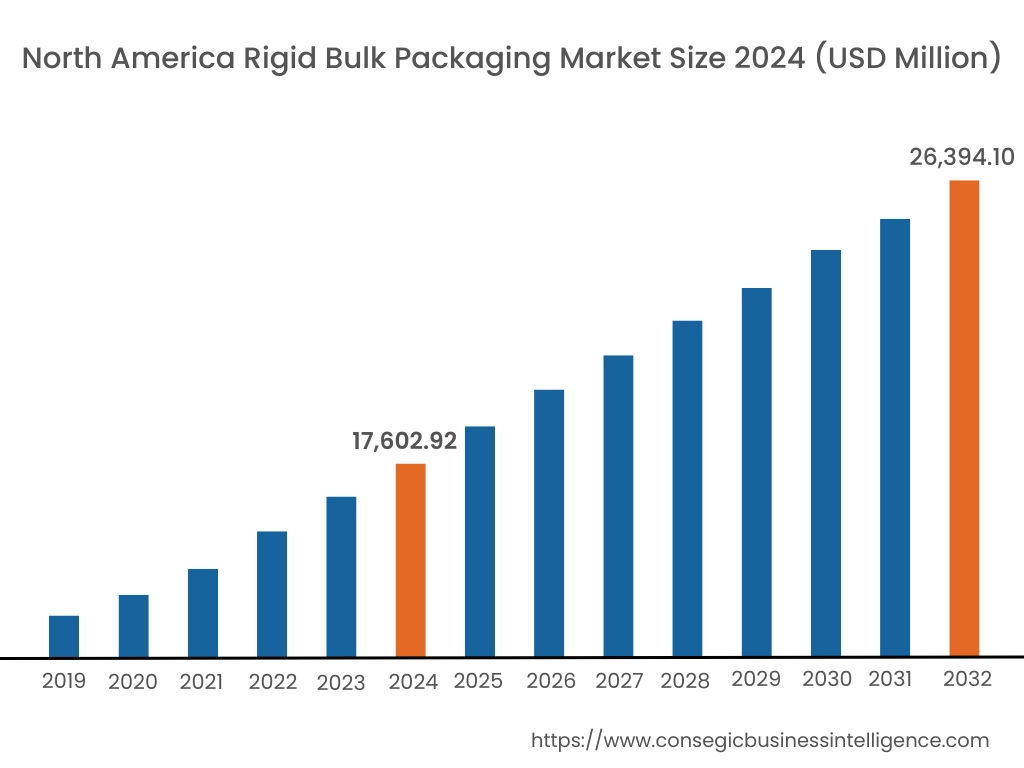

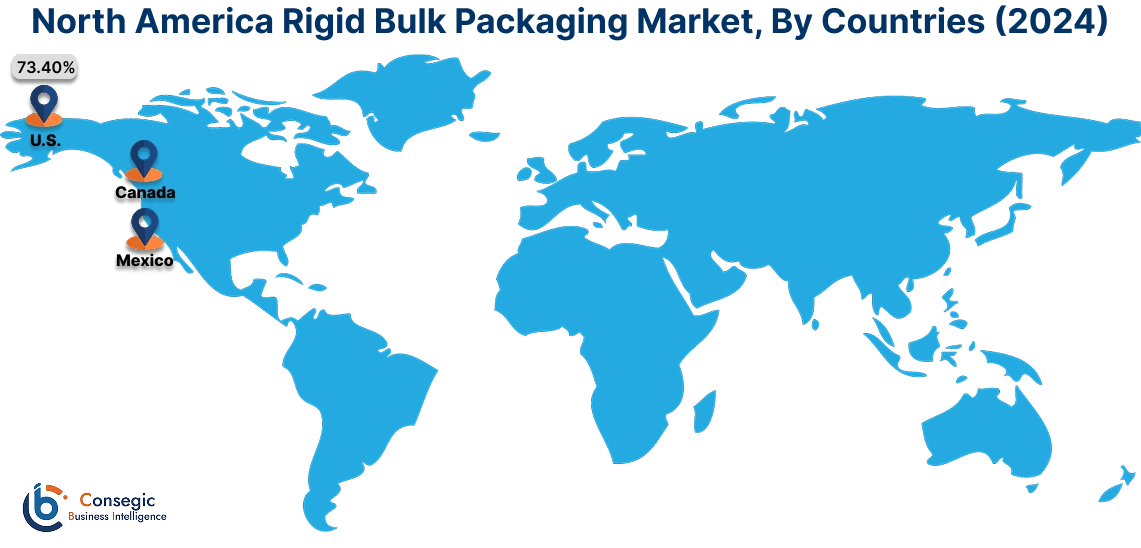

In 2024, North America was valued at USD 17,602.92 Million and is expected to reach USD 26,394.10 Million in 2032. In North America, the U.S. accounted for the highest share of 73.40% during the base year of 2024. North America is a major region for the rigid bulk packaging market analysis, driven by the strong presence of food and beverage, chemical, and pharmaceutical industries. The U.S. leads the region, leveraging rigid bulk containers for efficient storage and transportation of liquids, chemicals, and bulk food products. Increasing adoption of sustainable packaging solutions and the use of reusable intermediate bulk containers (IBCs) are enhancing the market's value. Canada contributes with rising industrial activities and the adoption of robust packaging solutions for bulk material handling. However, fluctuating raw material prices and environmental regulations surrounding plastic usage pose challenges.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.9% over the forecast period. Asia-Pacific is the largest and fastest-growing region in the rigid bulk packaging market growth, fueled by rapid industrialization, urbanization, and expanding agricultural and chemical industries in China, India, and Japan. China leads the market with its large-scale manufacturing sector and significant growth for packaging solutions in chemicals, food, and construction materials. India is experiencing increasing rigid bulk packaging market opportunities of rigid bulk containers in agriculture and pharmaceuticals, supported by its growing export activities. Japan’s advanced logistics systems and focus on high-quality packaging materials drive the adoption of IBCs and drums. However, limited recycling infrastructure in some areas and environmental concerns about plastic packaging materials pose challenges.

Europe analysis depicts it holds a significant share of the packaging market, supported by advanced manufacturing industries and stringent environmental regulations. Countries like Germany, France, and the UK dominate the market with extensive use of rigid bulk containers in chemicals, agriculture, and food applications. Germany’s strong industrial base drives high usage of IBCs and drums for chemical storage. France is witnessing growth in eco-friendly bulk packaging solutions, aligning with the EU’s sustainability goals. The UK’s logistics and distribution sectors rely heavily on rigid packaging for safe and efficient transport. However, rising raw material costs and strict compliance requirements for sustainable materials remain challenges.

As per the analysis The Middle East & Africa region is steadily advancing in the rigid bulk packaging market expansion, driven by the growing oil and gas, chemical, and food industries. Countries like Saudi Arabia and the UAE rely on rigid bulk containers for transporting and storing crude oil, petrochemicals, and industrial chemicals. In Africa, South Africa’s agricultural sector utilizes rigid packaging for safe storage and transport of grains and fertilizers. However, the region faces challenges such as limited local manufacturing capabilities and reliance on imports for advanced packaging solutions.

Latin America is an emerging market for rigid bulk packaging, with Brazil and Mexico being the key contributors. Brazil’s agricultural sector uses bulk packaging extensively for grains, sugar, and fertilizers, while its chemical industry relies on IBCs and drums for material handling. Mexico’s expanding automotive and chemical industries utilize packaging for transporting liquids and industrial chemicals. The region is also witnessing increased adoption of reusable and sustainable packaging solutions. However, economic instability and inconsistent regulations on material usage may hinder broader adoption across the region.

Top Key Players & Market Share Insights:

The Rigid Bulk Packaging market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Rigid Bulk Packaging market. Key players in the Rigid Bulk Packaging industry include -

- Core Plastech International Inc. (Canada)

- PlastiPak (United States)

- Schoeller Allibert (Netherlands)

- Greif, Inc. (United States)

- Mauser Packaging Solutions (United States)

- SCHÜTZ GmbH & Co. KGaA (Germany)

- Berry Global Inc. (United States)

- Packaging Corporation of America (United States)

- Hoover Ferguson Group, Inc. (United States)

- Amcor (Australia)

Recent Industry Developments :

Innovatioms:

- In February 2024, HP introduced its innovative HP Thermal Inkjet (TIJ) 108mm Bulk Printing Solution, a development designed to enhance the efficiency of high-volume packaging processes. This new solution allows for high-speed, high-resolution printing of extensive 1D and 2D barcodes and characters on rigid bulk packaging, without the need for traditional labeling systems. Technology enables automatic switching between bulk supply systems, reducing downtime and labor costs, while ensuring consistent, high-quality prints even after extended periods of inactivity. HP’s TIJ solution also supports sustainability by eliminating the need for label inventories, enhancing recyclability, and lowering production costs. This development represents a significant shift toward more cost-effective and eco-friendly packaging solutions in the rigid packaging market.

Rigid Bulk Packaging Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 81,438.15 Million |

| CAGR (2025-2032) | 5.5% |

| By Material Type |

|

| By Product Type |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected size of the Rigid Bulk Packaging Market by 2032? +

The market is expected to reach over USD 81,438.15 Million by 2032.

What is rigid bulk packaging? +

Rigid bulk packaging includes durable and reusable solutions like drums, intermediate bulk containers (IBCs), bulk crates, and rigid totes designed for transporting and storing bulk materials securely.

Which industries primarily use rigid bulk packaging? +

Key industries include food & beverage, chemicals, pharmaceuticals, agriculture, construction, and logistics.

What materials are commonly used in rigid bulk packaging? +

The primary materials are plastic, metal, wood, glass, and composites.

Why is plastic the dominant material type? +

Plastic is lightweight, durable, cost-effective, and versatile, making it suitable for a wide range of applications in bulk packaging.