- Summary

- Table Of Content

- Methodology

Reversible Heat Pump Market Size:

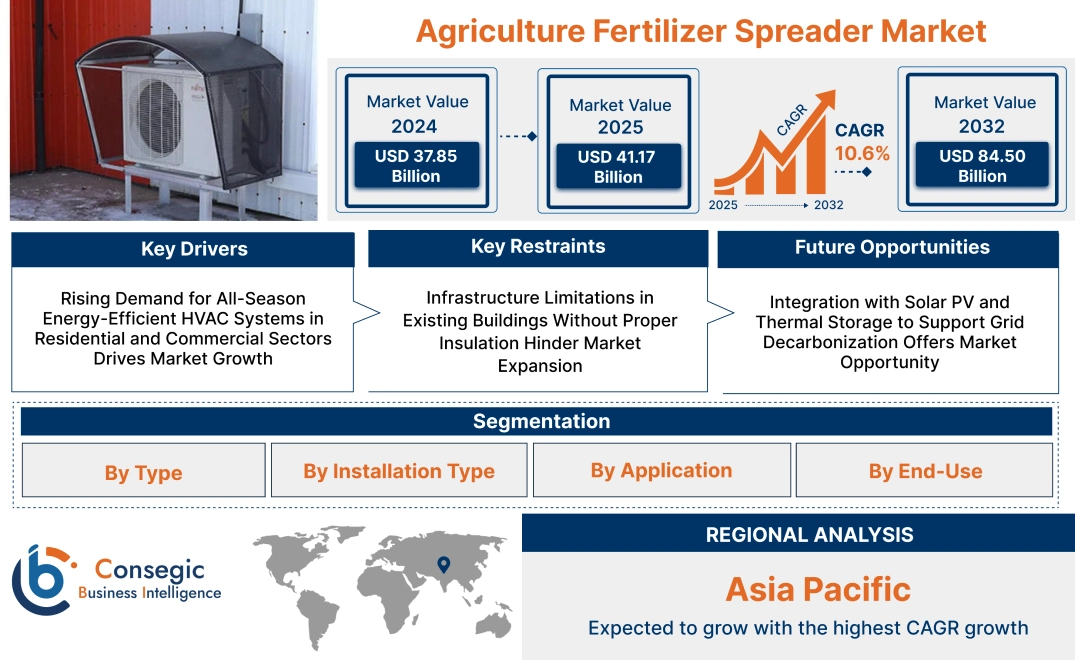

Reversible Heat Pump Market size is estimated to reach over USD 84.50 Billion by 2032 from a value of USD 37.85 Billion in 2024 and is projected to grow by USD 41.17 Billion in 2025, growing at a CAGR of 10.6% from 2025 to 2032.

Reversible Heat Pump Market Scope & Overview:

Reversible heat pump is a two-mode climate control unit that is engineered to offer heating and cooling functions by reversing refrigerant flow. Applicable in residential, commercial, and light industrial settings, it offers round-the-year temperature control through one single integrated device.

Its major elements are a compressor, expansion valve, evaporator, and condenser, designed to reverse functions based on seasonal needs. Programmable thermostats, variable-speed operation, and zoning capabilities add to energy optimization and indoor comfort.

They provide significant benefits such as compactness, quiet operation, and effective space integration. They minimize the requirement for multiple heating and cooling systems, reducing installation and servicing costs. The technology enables underfloor system, radiator, and air handler compatibility with easy integration into new buildings and retrofits. Its flexibility and dual-mode capability make it an effective solution for balanced indoor climate control in different types of buildings.

Reversible Heat Pump Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for All-Season Energy-Efficient HVAC Systems in Residential and Commercial Sectors Drives Market Growth

The dual-use capability of reversible heat pumps provides effortless mode switching between heating and cooling, providing year-round climate control through one system. They provide high energy efficiency by leveraging ambient heat transfer, resulting in a marked decrease in energy usage relative to traditional HVAC configurations. Their application in a variety of building types, such as apartments, offices, and schools, makes them ideal for new building construction and energy retrofits as well. As the world's energy standards become more stringent and consumers move towards electrified heating solutions, the need for combined, low-emission HVAC systems is growing. They fit into building electrification policies and minimize reliance on gas-based systems. The capability to provide heating and cooling from one unit streamlines design and minimizes long-term maintenance.

- For instance, in February 2025, Carrier launched AquaSnap® 61AQ, the first high-temperature air source reversible heat pump for commercial applications using R-290. This product delivers high temperatures with increased energy efficiency, noise reduction, and enhanced operational performance. The use of R-290 with a GWP of 0.02 minimizes environmental impact.

As homeowners and developers focus on energy efficiency and comfort, the uptake of these systems is increasing, fueling the reversible heat pump market expansion.

Key Restraints:

Infrastructure Limitations in Existing Buildings Without Proper Insulation Hinder Market Expansion

Effective operation of reversible heat pumps relies on well-insulated building envelopes to store thermal energy and minimize heat loss. Poorly insulated older buildings with unsealed windows and old glazing have considerably lower system efficiency and higher electric consumption. In these conditions, heat pumps will find it challenging to provide a consistent indoor temperature, particularly in extreme weather conditions. Retrofitting them usually involves wide-scale structural changes, like improving wall insulation or window replacement, which increases the overall installation cost. Where widespread energy retrofit funds are scarce and prevalent in areas of aging housing stock, these limitations lessen the attractiveness of converting to electric HVAC systems. This incompatibility between new system needs and existing infrastructure retards the rate of technology deployment. While demand for effective heating and cooling is rising, infrastructure incompatibility is still a dominant restraint to the reversible heat pump market growth.

Future Opportunities :

Integration with Solar PV and Thermal Storage to Support Grid Decarbonization Offers Market Opportunity

Reversible heat pump systems coupled with rooftop solar arrays and thermal storage technologies can provide self-sustaining, low-carbon HVAC operation in residential and commercial buildings. During the day, excess solar electricity drives the heat pump for space heating or cooling, and excess energy is stored in thermal tanks for release during peak demand times. This arrangement minimizes grid dependence, maximizes solar use, and facilitates building-level energy independence. While governments encourage net-zero energy goals and utilities reward demand-side management, the attractiveness of solar-integrated systems is on the rise. Such solutions become especially pertinent in off-grid residential applications, zero-energy building ventures, and territories embracing dynamic tariffs for electricity. The world has an increasing need for clean, resilient, and grid-responsive technology, generating significant reversible heat pump market opportunities founded on energy efficiency, renewable integration, and sustainable growth.

Reversible Heat Pump Market Segmental Analysis :

By Type:

Based on type, the market is segmented into air-to-air heat pumps and air-to-water heat pumps.

The air-to-air heat pumps segment accounted for the largest revenue share in 2024.

- Air-to-air systems are widely used in residential and light commercial applications for their ability to provide both heating and cooling efficiently through ducted or ductless systems.

- Their lower installation costs and minimal space requirements support strong adoption across new and retrofit installations.

- These units are particularly popular in moderate climate zones where extreme heating or cooling is not required.

- According to the reversible heat pump market analysis, simplicity, affordability, and improved seasonal energy efficiency ratios (SEER) contribute to their widespread use.

The air-to-water heat pumps segment is projected to witness the fastest CAGR during the forecast period.

- Air-to-water systems are ideal for integration with underfloor heating, radiators, and domestic hot water systems, making them well-suited for whole-home solutions.

- These systems are gaining traction in colder regions due to improved performance at low ambient temperatures.

- Their compatibility with solar thermal panels and thermal storage systems enhances long-term energy savings.

- As per reversible heat pump market trends, growing emphasis on decarbonization and electrification of heating drives this segment’s rapid acceleration.

By Installation Type:

Based on installation type, the market is segmented into new installation and retrofit installation.

The new installation segment accounted for the largest reversible heat pump market share in 2024.

- In newly built residential and commercial properties, builders increasingly install these pumps as part of zero-energy building compliance.

- Regulatory incentives, energy efficiency mandates, and green certifications drive the inclusion of these systems in initial construction.

- The ability to size and design HVAC systems from the ground up leads to optimal performance and customer satisfaction.

- As per reversible heat pump market analysis, integration during construction contributes significantly to the segment's dominance.

The retrofit installation segment is expected to register the fastest CAGR during the forecast period.

- Retrofitting heat pumps into existing structures is driven by rising electricity prices and the desire to replace fossil-fuel-based heating systems.

- Technological advancements allow easier upgrades with minimal modifications to the existing HVAC or hydronic systems.

- Government rebates and renovation-focused green energy subsidies promote market penetration in older housing stock.

- According to the reversible heat pump market trends, improving indoor comfort and energy savings in established buildings supports retrofit adoption.

By Application:

Based on application, the reversible heat pump market is segmented into space heating & cooling, water heating, and industrial process heating.

The space heating & cooling segment accounted for the largest revenue share in 2024.

- They provide year-round indoor climate control, offering both heating in winter and cooling in summer through a single system.

- These systems are popular in regions with seasonal temperature swings and are supported by inverter technology for precise comfort regulation.

- Homeowners favor them for their quiet operation, consistent air distribution, and low environmental impact.

- Reversible heat pump market demand in this segment is driven by consumer preference for energy-efficient alternatives to conventional furnaces and air conditioners.

The industrial process heating segment is expected to grow at the fastest CAGR during the forecast period.

- Industrial sectors are increasingly adopting reversible heat pumps to recover waste heat and improve process efficiency while lowering emissions.

- These systems are especially valuable in food processing, pharmaceuticals, and chemical industries for pre-heating, drying, and fluid heating.

- Integration with smart control systems allows predictive energy management and peak load reduction.

- Hence, decarbonizing industrial heat is a key strategic goal that bolsters the reversible heat pump market growth.

By End-Use:

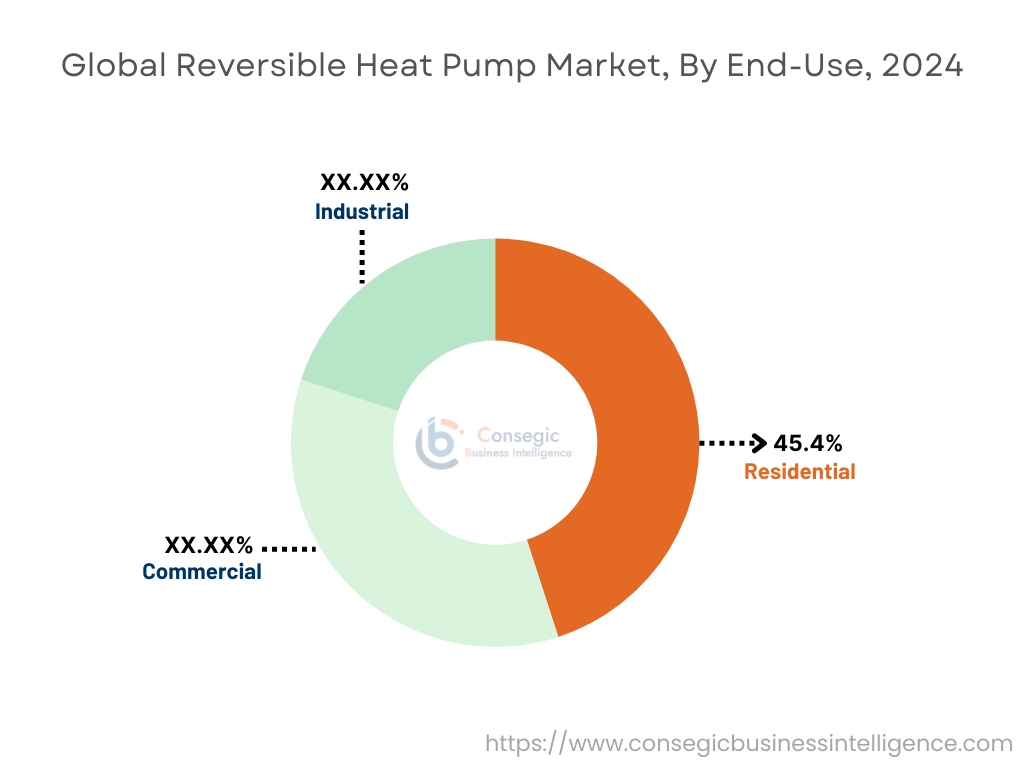

Based on end-use, the market is segmented into residential, commercial, and industrial.

The residential segment held the largest reversible heat pump market share of 45.4% in 2024.

- Homeowners are increasingly adopting them due to rising awareness of energy efficiency, comfort, and sustainability.

- These systems reduce carbon emissions and are compatible with renewable energy setups such as photovoltaic panels.

- Smart thermostats and home automation compatibility enhance consumer appeal.

- Thus, electrification of home heating systems continues to drive the reversible heat pump market demand.

The commercial segment is projected to experience the fastest CAGR during the forecast period.

- Commercial buildings, including schools, office complexes, and retail centers, are adopting centralized or zoned heat pump systems to optimize energy usage.

- The segment benefits from building decarbonization mandates, LEED certifications, and ESG-focused investments.

- Advanced control systems and modular installation make reversible systems viable for both small and large commercial facilities.

- Reversible heat pump market expansion in this segment is supported by the shift toward clean energy and operating cost reduction.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

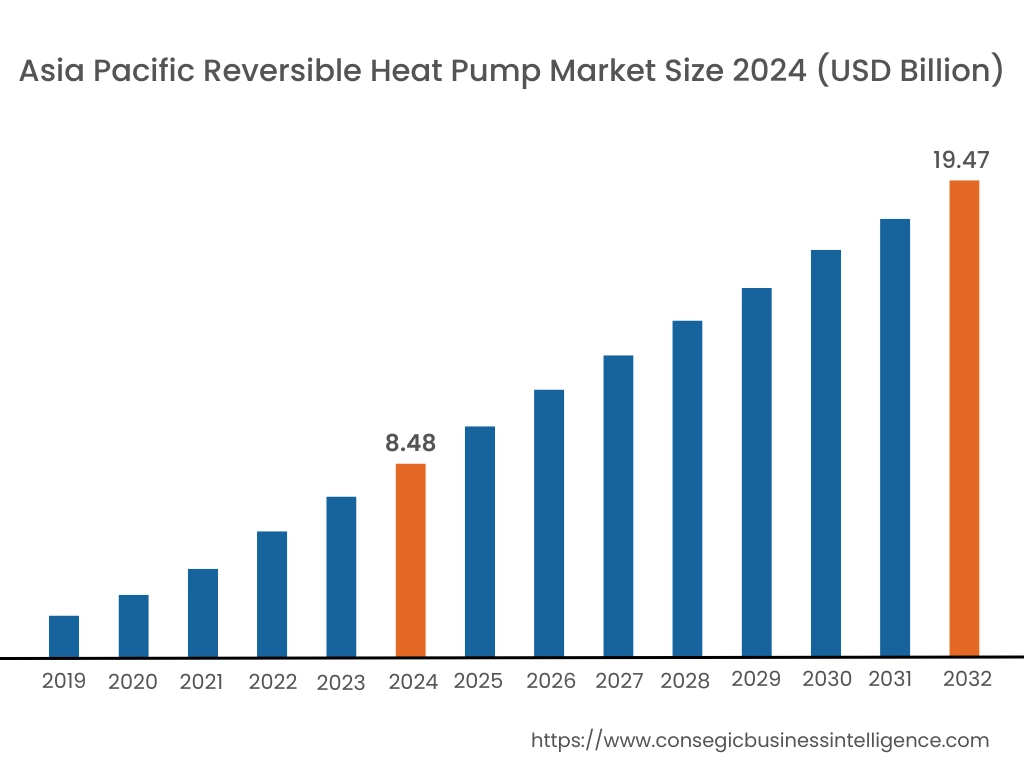

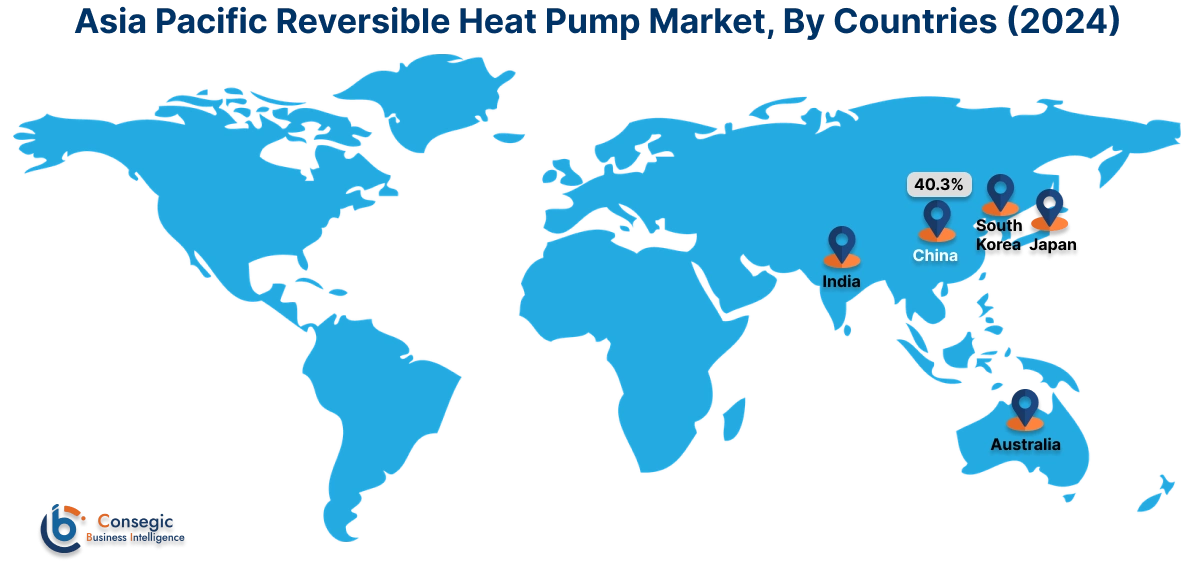

Asia Pacific region was valued at USD 8.48 Billion in 2024. Moreover, it is projected to grow by USD 9.25 Billion in 2025 and reach over USD 19.47 Billion by 2032. Out of this, China accounted for the maximum revenue share of 40.3%. Asia-Pacific is experiencing rapid growth in the reversible heat pump industry, with demand driven by increasing urbanization, energy-saving policy enforcement, and rising middle-class expectations. In Japan and South Korea, advanced inverter technologies are being adopted at scale, with compact, high-efficiency reversible units preferred in residential high-rises. China is accelerating installation across public buildings and residential housing as part of nationwide initiatives to decrease dependency on coal-fueled heating. Market research suggests that seasonal climatic changes across zones from northern cold climates to southern tropical climates place them as optimum multi-climate solutions. Australia is also adopting the technology because of its two-season use and compatibility with net-zero home schemes.

North America is estimated to reach over USD 29.08 Billion by 2032 from a value of USD 12.97 Billion in 2024 and is projected to grow by USD 14.11 Billion in 2025. North America represents a mature market with adoption growing, especially in areas with clear seasonal temperature variations. The United States and Canada are adopting reversible heat pumps in new buildings and retrofits, with increasing requirement in residential, multifamily, and light commercial structures. Market analysis points to the role of decarbonization incentives and energy efficiency rebate programs as driving the shift from traditional HVAC systems to dual-purpose, inverter-driven systems. The ubiquitous adoption of smart thermostats and zoning controls is further increasing the accessibility of reversible systems. As sustainability legislation grows more aggressive, particularly at state and provincial levels, long-term development will continue.

Europe is still leading the world in the adoption of heat pump technologies with the support of ambitious climate targets, energy efficiency requirements, and the phase-out of fossil-fuel heating. France, Germany, Italy, and the Nordic countries are making large-scale use of reversible heat pumps to satisfy both heating and cooling requirements in the residential and tertiary sectors. Market research indicates that government-sponsored incentives under green renovation schemes, in addition to stringent energy labeling requirements, are compelling steady installations. Furthermore, the shift toward almost zero-energy buildings is transforming reversible systems into a central element of compliant mechanical systems. With the electrification of heat gaining momentum, the reversible heat pump market opportunity in Europe remains robust.

Latin America is witnessing nascent interest, particularly in Chile, Brazil, and Argentina, where seasonal climates and rising energy prices underscore the necessity for effective thermal control. Although conventional air conditioning systems are still prevalent, market research indicates a slow move towards consumer appreciation of the advantages of reversible systems, particularly in new residential projects and mid-scale commercial buildings. The region's take-up is driven by increasing environmental concern and initiatives to diversify energy consumption away from carbon-emitting sources. Nevertheless, economic uncertainty and limited availability of qualified installation experts can present short-term limitations to widespread take-up.

Reversible heat pump systems are receiving increasing interest in the Middle East and Africa, where there are strong daily and seasonal temperature fluctuations. In the Gulf, nations such as the UAE and Saudi Arabia are integrating the systems into energy-efficient building regulations, specifically on green-certified commercial developments and high-end residential skyscrapers. In Africa, South Africa is experiencing early uptake in eco-housing and hospitality complexes in temperate climates. Purchasing drivers in the market, according to analysis, include energy reliability, climate adaptability on the ground, and long-term cost savings. Although there are some markets where infrastructure constraints apply, the long-term market opportunity is good, especially as urbanization and electrification continue to advance.

Top Key Players and Market Share Insights:

The reversible heat pump market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global reversible heat pump market. Key players in the reversible heat pump industry include -

- Daikin Industries Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- SAMSUNG (South Korea)

- Vaillant Group (Germany)

- LG Electronics Inc. (South Korea)

- Midea Group (China)

- Carrier Corporation (USA)

- Trane Technologies plc (Ireland)

- Bosch Thermotechnology (Germany)

Recent Industry Developments :

Product Launches:

- In September 2024, Clivet launched a water-cooled, multipurpose, polyvalent reversible heat pump. The SCREWLINE-i (WiDHN-KSL1 PL) operates on hydrofluoroolefins-based, azeotropic refrigerant known as R513a and inverter screw compressors. The use of this refrigerant enables a lower environmental impact and simpler installation.

Reversible Heat Pump Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 84.50 Billion |

| CAGR (2025-2032) | 10.6% |

| By Type |

|

| By Installation Type |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Reversible Heat Pump Market? +

Reversible Heat Pump Market size is estimated to reach over USD 84.50 Billion by 2032 from a value of USD 37.85 Billion in 2024 and is projected to grow by USD 41.17 Billion in 2025, growing at a CAGR of 10.6% from 2025 to 2032.

What specific segmentation details are covered in the Reversible Heat Pump Market report? +

The Reversible Heat Pump market report includes specific segmentation details for type, installation, application and end-use.

What are the end-use segments of the Reversible Heat Pump Market? +

The end-use of the Reversible Heat Pump Market are residential, commercial, and industrial.

Who are the major players in the Reversible Heat Pump Market? +

The key participants in the Reversible Heat Pump market are Daikin Industries, Ltd. (Japan), Mitsubishi Electric Corporation (Japan), Panasonic Holdings Corporation (Japan), SAMSUNG (South Korea), LG Electronics (South Korea), Midea Group (China), Carrier Corporation (USA), Trane Technologies plc (Ireland), Bosch Thermotechnology (Germany) and Vaillant Group (Germany).