- Summary

- Table Of Content

- Methodology

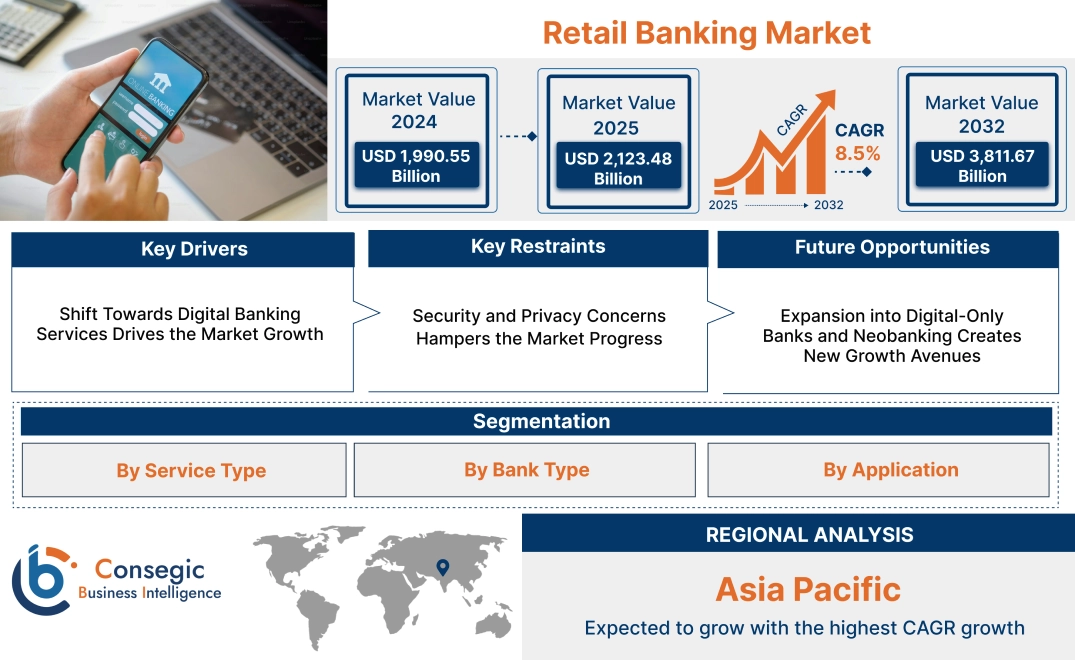

Retail Banking Market Size:

Retail Banking Market size is estimated to reach over USD 3,811.67 Billion by 2032 from a value of USD 1,990.55 Billion in 2024 and is projected to grow by USD 2,123.48 Billion in 2025, growing at a CAGR of 8.5% from 2025 to 2032.

Retail Banking Market Scope & Overview:

Retail banking refers to financial services offered by banks to individual consumers, including savings accounts, personal loans, mortgages, credit cards, and payment solutions. These services enable secure transactions, fund management, and access to credit, catering to the daily financial needs of individuals and households. They are accessible through physical branches, online platforms, and mobile applications, ensuring convenience for customers.

Financial institutions providing these services focus on customer-centric solutions such as digital banking, advisory support, and automated transaction processing. The sector includes traditional banks, credit unions, and digital-only institutions, each offering tailored financial products. Secure payment processing, intuitive banking interfaces, and multi-channel accessibility enhance the overall customer experience.

End-users include individuals, small business owners, and professionals seeking banking solutions to manage personal finances and business transactions. These services form a fundamental part of the financial ecosystem, supporting everyday financial activities.

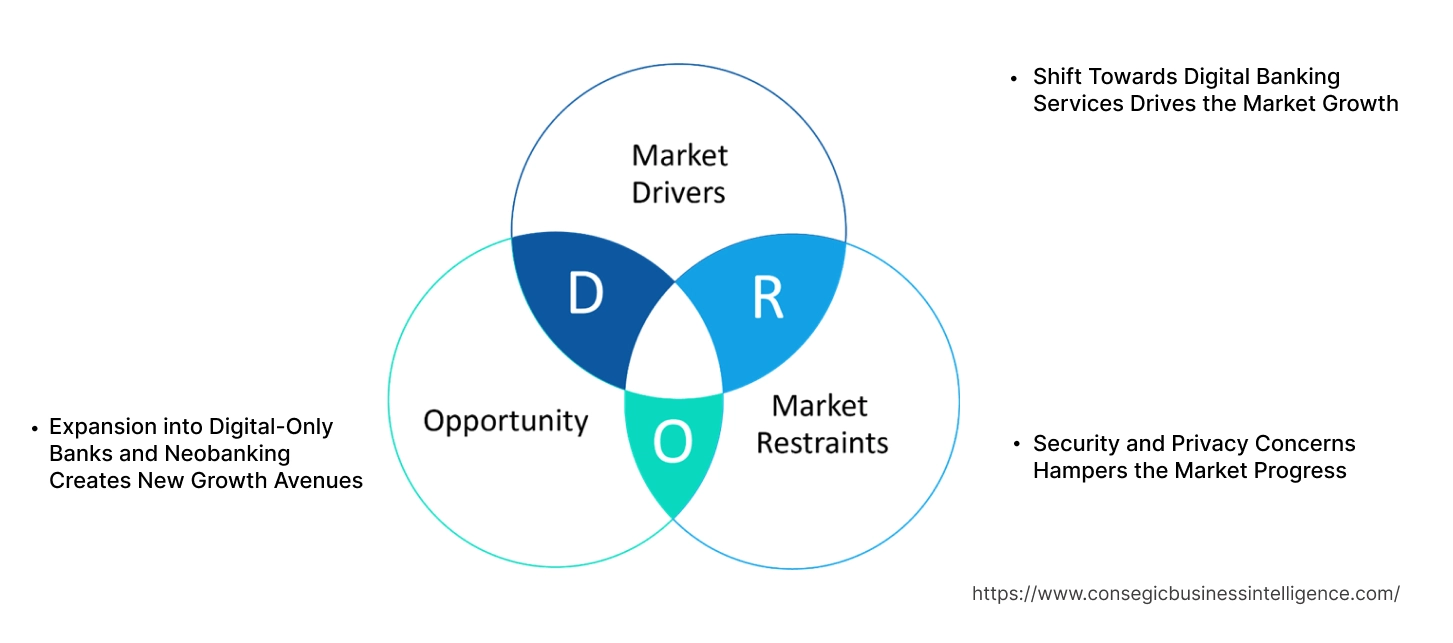

Retail Banking Market Dynamics - (DRO) :

Key Drivers:

Shift Towards Digital Banking Services Drives the Market Growth

Consumers increasingly seek convenient, accessible, and secure banking solutions that allow them to manage their finances on-the-go. Mobile banking, online payments, and digital wallets provide consumers with the ability to conduct transactions, check balances, and make payments anytime, anywhere, without the need to visit a physical bank. As a result, banks are heavily investing in advanced digital platforms and mobile applications to meet the growing demand for seamless digital experiences. This trend is especially appealing to younger, tech-savvy customers who prefer using smartphones and computers for their banking needs. Additionally, the COVID-19 pandemic accelerated the adoption of digital banking as consumers sought contactless solutions for their financial transactions. This shift is not only driving the retail banking market expansion but also transforming the way banks interact with their customers, making banking more efficient and user-friendly.

Key Restraints:

Security and Privacy Concerns Hampers the Market Progress

As digital banking services expand, the risk of cybersecurity threats and data privacy issues becomes a critical restraint. Banks are increasingly vulnerable to cyberattacks, fraud, and data breaches that compromise sensitive customer information, including account details and financial transactions. These security threats erodes consumer trust, especially as more customers move their banking activities online, making it essential for banks to implement robust security measures such as encryption, multi-factor authentication, and real-time fraud detection systems. Failure to address these risks results in severe financial and reputational damage, hindering customer retention and slowing retail banking market demand. With the rising number of cybercrimes targeting financial institutions, ensuring data privacy and maintaining secure digital platforms is paramount for banks to build and sustain consumer confidence in their services. As the market grows, maintaining a strong cybersecurity framework will be crucial to supporting the ongoing adoption of digital banking solutions.

Future Opportunities :

Expansion into Digital-Only Banks and Neobanking Creates New Growth Avenues

The growth of digital-only banks and neobanks presents a major opportunity for traditional banking players to tap into the growing demand for mobile-first, branchless banking solutions. These digital-native platforms offer cost-effective services such as instant loans, savings accounts, mobile wallets, and other financial products that cater to tech-savvy consumers seeking convenience and accessibility. The shift toward digital-only banking models has gained traction, particularly among younger generations and underserved populations who prefer online banking over traditional brick-and-mortar branches. For traditional banks, entering the neobanking space through partnerships, acquisitions, or digital transformation initiatives allows them to reach a wider customer base, reduce operational costs, and innovate their product offerings. By embracing the mobile-first, user-friendly approach of neobanks, established banks will stay competitive, capture new market segments, and offer a seamless banking experience that meets the evolving expectations of today’s digital consumers. Thus, the above factors are creating new retail banking market opportunities.

Retail Banking Market Segmental Analysis :

By Service Type:

Based on service type, the market is segmented into savings accounts, loans, mortgages, credit cards, wealth management, and others.

The savings accounts segment accounted for the largest revenue of the total retail banking market share in 2024.

- Savings accounts remain the fundamental service in retail banking, providing customers with a secure way to deposit funds while earning interest.

- Financial institutions offer customized savings accounts with tiered interest rates, digital access, and personalized financial planning tools to attract a diverse customer base.

- The integration of mobile and online banking services has enhanced the accessibility and convenience of managing savings, supporting the expansion of digital banking ecosystems.

- As per retail banking market analysis, savings accounts continue to be a primary service offering, aligning with trends in financial inclusion and secure cash management solutions.

The wealth management segment is projected to see steady adoption during the forecast period.

- Wealth management services cater to high-net-worth individuals (HNWIs) and professionals seeking investment advisory, portfolio management, and tax planning solutions.

- Banks are increasingly integrating AI-driven analytics and robo-advisors into wealth management platforms to enhance investment decision-making and risk assessment.

- Personalized wealth management solutions, including estate planning and retirement funds, are becoming essential offerings within private banking divisions.

- As per retail banking market trends, the rising emphasis on financial planning and diversified investment portfolios has driven the adoption of digital wealth management services.

By Bank Type:

Based on bank type, the market is segmented into public sector banks, private sector banks, community banks, and credit unions.

The private sector banks segment accounted for the largest revenue of the total retail banking market share in 2024.

- Private sector banks leverage advanced digital banking services, superior customer support, and competitive financial products to attract and retain clients.

- These banks prioritize innovation by integrating AI-powered chatbots, biometric authentication, and personalized banking solutions to enhance user experience.

- Private institutions play a key role in offering flexible financial products, including high-yield savings accounts, investment advisory, and premium credit cards.

- As per retail banking market analysis, private sector banks dominate due to their ability to adopt evolving banking trends and expand their customer base through targeted marketing strategies.

The credit unions segment is expected to gain steady adoption during the forecast period.

- Credit unions provide community-focused banking services with lower fees and personalized financial assistance, making them a preferred choice for small businesses and individuals.

- These institutions emphasize financial literacy programs and offer favorable loan terms, strengthening their presence among cost-conscious banking customers.

- The increasing adoption of digital transformation strategies among credit unions has improved their competitive positioning against larger banking entities.

- Thus, the rising consumer preference for member-owned financial institutions has contributed to the sustained relevance of credit unions, driving the retail banking market growth.

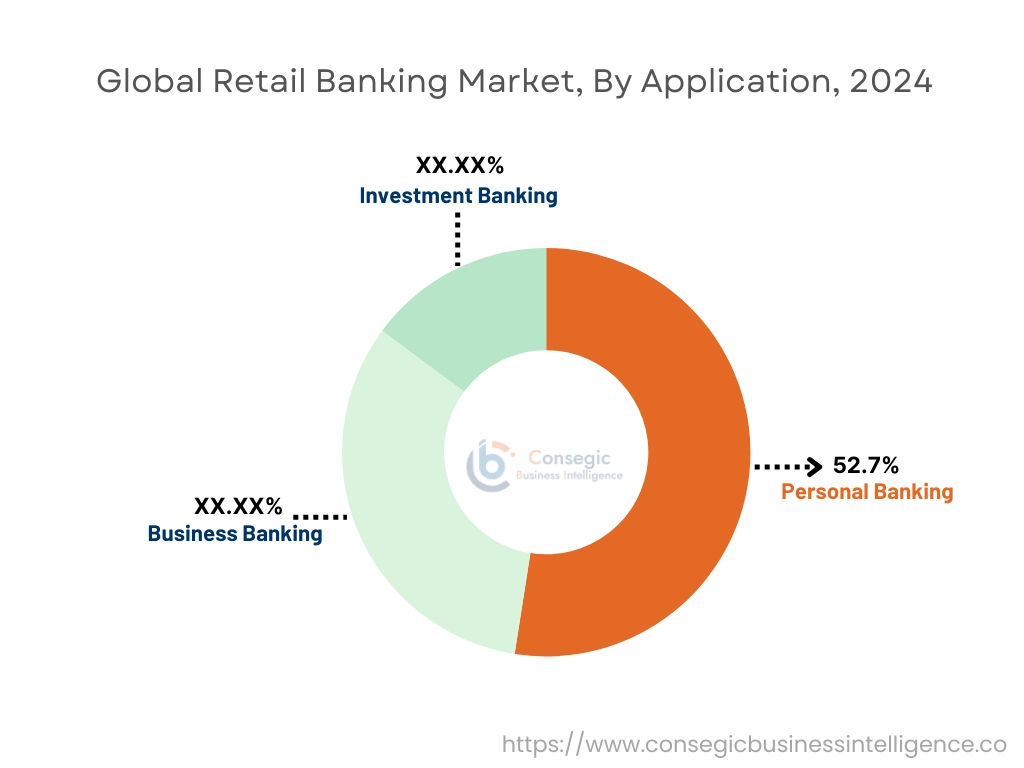

By Application:

Based on application, the market is segmented into personal banking, business banking, and investment banking.

The personal banking segment accounted for the largest revenue of 52.7% share in 2024.

- Personal banking services encompass a wide range of financial products, including checking and savings accounts, credit cards, and personal loans, making them essential in retail banking.

- Digital banking solutions, such as mobile apps and online portals, have enhanced customer engagement by offering seamless transactions, fund transfers, and real-time financial tracking.

- Personalized banking services, including tailored credit offerings and mortgage solutions, play a critical role in improving customer retention.

- As per market analysis, the enlargement of digital-first banking models aligns with customer expectations for convenience and self-service financial management, fueling the retail banking market demand.

The business banking segment is projected to expand steadily during the forecast period.

- Business banking solutions support small and medium-sized enterprises (SMEs) with financial products such as working capital loans, commercial credit, and treasury management services.

- The adoption of automated financial solutions, including AI-powered risk assessment and blockchain-enabled transaction security, has enhanced business banking services.

- Financial institutions are increasingly offering specialized accounts and credit facilities tailored to startups and entrepreneurs, strengthening their engagement with business clients.

- As per retail banking market trends, the emphasis on digital business banking platforms has led to improved financial efficiency and operational agility for enterprises.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

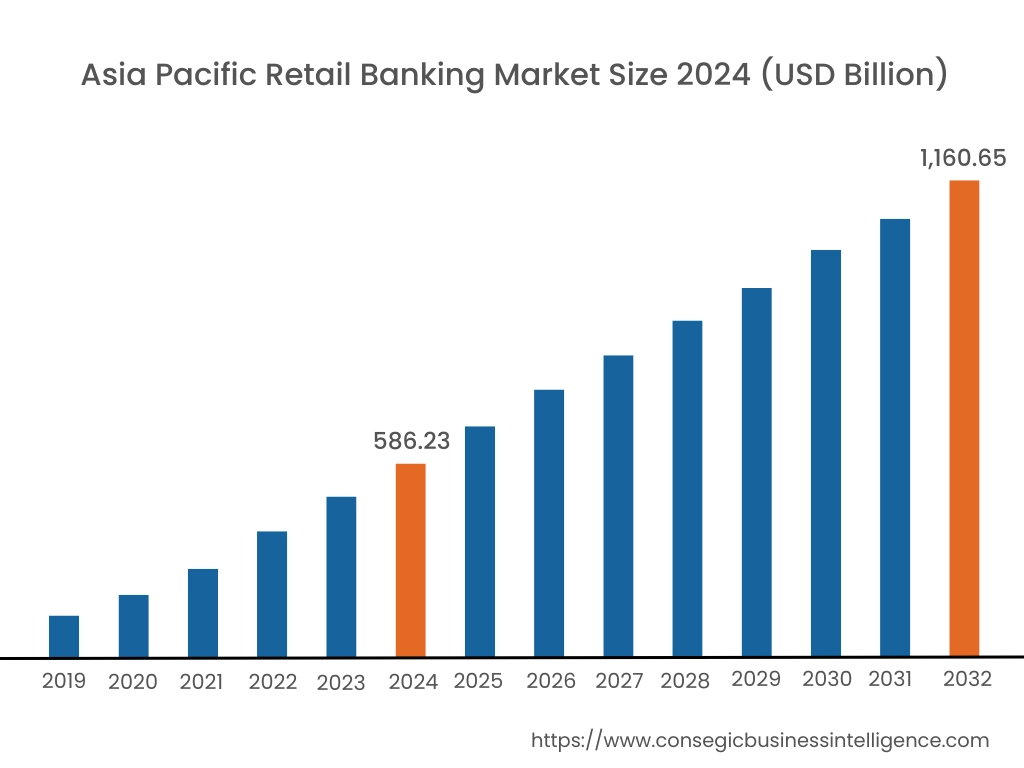

Asia Pacific region was valued at USD 586.23 Billion in 2024. Moreover, it is projected to grow by USD 627.15 Billion in 2025 and reach over USD 1,160.65 Billion by 2032. Out of this, China accounted for the maximum revenue share of 33.1%. The Asia-Pacific region is witnessing a dynamic shift in retail banking, propelled by rapid technological adoption and a vibrant, diverse consumer base. A key trend here is the rising popularity of mobile banking and fintech collaborations, which are redefining traditional banking operations by delivering services through cutting-edge digital platforms. Analysis reveals that these changes are driven by a cultural inclination toward technological convenience and the need for financial inclusion across both urban and rural areas. The region’s retail banks are therefore focusing on creating seamless, integrated experiences that merge digital innovation, boosting the retail banking market growth.

North America is estimated to reach over USD 1,235.36 Billion by 2032 from a value of USD 660.28 Billion in 2024 and is projected to grow by USD 703.03 Billion in 2025. In North America, retail banking is undergoing a significant transformation as traditional institutions integrate digital channels with personalized customer service. A notable trend is the accelerated move toward digital banking solutions, where mobile applications and online platforms are becoming central to customer interactions. Concurrently, analysis reveals that banks are reconfiguring their service models to balance efficiency with human touch, ensuring that both digital and branch-based experiences meet evolving consumer demands. This region’s approach reflects a strategic focus on harnessing technology while maintaining regulatory compliance and customer trust.

European retail banking continues to redefine its operating model amid robust regulatory frameworks and a strong emphasis on sustainability. One prominent trend is the adoption of innovative digital tools designed to streamline account management and enhance user experiences, even as traditional banking channels remain integral. In parallel, analysis indicates that European banks are investing in secure digital infrastructures and personalized financial products, driven by an environment that encourages technological experimentation alongside strict adherence to consumer protection standards. This blend of innovation and regulation creates a unique market dynamic where both customer-centric solutions and compliance are equally prioritized, thereby creating significant retail banking market opportunities.

In the Middle East and Africa, retail banking is adapting to a landscape marked by both robust infrastructure development and emerging market challenges. A significant trend is the growth in integration of digital payment systems and mobile banking services aimed at reaching previously underserved populations. Analysis shows that banks in this region are embracing technology to improve financial accessibility and operational efficiency while navigating a complex regulatory environment. These efforts are complemented by initiatives to strengthen cybersecurity measures and enhance consumer trust in digital platforms, fueling the retail banking market expansion.

Latin America is experiencing a gradual transformation in retail banking as financial institutions work to modernize their operations and improve customer engagement. One prominent trend is the increasing use of digital channels, which is reshaping how traditional banking services are delivered in an environment where mobile connectivity plays a crucial role. Analysis suggests that regional banks are investing in technology to offer innovative financial solutions while overcoming infrastructural and regulatory challenges. This strategic shift is fostering a more agile banking industry that aims to better serve a diverse and evolving customer base.

Top Key Players and Market Share Insights:

The Retail Banking market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Retail Banking market. Key players in the Retail Banking industry include -

- Industrial and Commercial Bank of China (ICBC) (China)

- Agricultural Bank of China (China)

- BNP Paribas (France)

- Mitsubishi UFJ Financial Group (Japan)

- Crédit Agricole Group (France)

- China Construction Bank (China)

- Bank of China (China)

- JPMorgan Chase & Co. (USA)

- Bank of America (USA)

- HSBC Holdings plc (UK)

Recent Industry Developments :

Product Launches:

- In October 2024, Santander launched Openbank in the U.S., expanding its consumer banking business nationwide. Openbank offers a high-yield savings product with a fast onboarding process, leveraging Santander’s proprietary technology for a seamless customer experience. The platform integrates core banking infrastructure with a customer data layer, enabling account openings in just five minutes via the Openbank app or website. This launch supports Santander's U.S. growth strategy by generating deposits to fund its auto finance division, marking a significant step in the bank’s global digital transformation.

Acquisitions & Mergers:

- In February 2024, Barclays completed the acquisition of Tesco Bank’s retail banking business, including credit cards, personal loans, and deposits. The deal also establishes a 10-year strategic partnership with Tesco Stores Ltd., allowing Barclays UK to market and distribute financial products under the Tesco brand. The collaboration aims to enhance financial services for Tesco customers through its distribution channels and the open market. This acquisition aligns with Barclays UK’s strategy of partnering with major retail and consumer brands, with Tesco Bank continuing to operate under its existing brand but under Barclays UK’s management.

Service Launch:

- In January 2025, NAB and Amazon introduced PayTo as a payment option for Amazon.com.au customers, enabling secure, cardless transactions directly from bank accounts. This integration enhances payment visibility and control, allowing users to authorize PayTo arrangements via online banking for seamless one-click payments. NAB’s Pay by Bank (PayTo) simplifies digital payments, offering Amazon shoppers a secure and efficient alternative while providing businesses with an instant, cost-effective solution.

Retail Banking Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 3,811.67 Billion |

| CAGR (2025-2032) | 8.5% |

| By Service Type |

|

| By Bank Type |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Retail Banking Market? +

The Retail Banking Market size is estimated to reach over USD 3,811.67 Billion by 2032 from a value of USD 1,990.55 Billion in 2024 and is projected to grow by USD 2,123.48 Billion in 2025, growing at a CAGR of 8.5% from 2025 to 2032.

What are the key segments in the Retail Banking Market? +

The market is segmented by service type (savings accounts, loans, mortgages, credit cards, wealth management, others), bank type (public sector banks, private sector banks, community banks, credit unions), and application (personal banking, business banking, investment banking).

Which segment is expected to grow the fastest in the Retail Banking Market? +

The wealth management segment is projected to see steady adoption and growth during the forecast period, driven by the increasing emphasis on personalized financial planning, portfolio management, and investment advisory services for high-net-worth individuals (HNWIs) and professionals.

Who are the major players in the Retail Banking Market? +

Key players in the Retail Banking Market include Industrial and Commercial Bank of China (ICBC) (China), Agricultural Bank of China (China), China Construction Bank (China), Bank of China (China), JPMorgan Chase & Co. (USA), Bank of America (USA), HSBC Holdings plc (UK), BNP Paribas (France), Mitsubishi UFJ Financial Group (Japan), Crédit Agricole Group (France).