- Summary

- Table Of Content

- Methodology

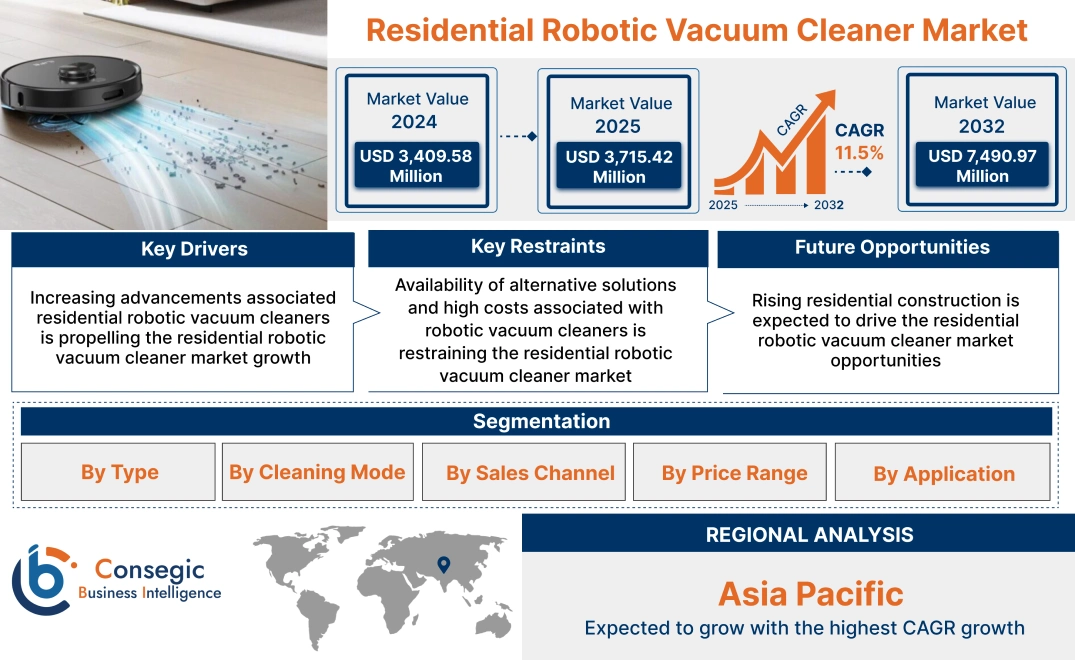

Residential Robotic Vacuum Cleaner Market Size:

Residential Robotic Vacuum Cleaner Market size is estimated to reach over USD 7,490.97 Million by 2032 from a value of USD 3,409.58 Million in 2024 and is projected to grow by USD 3,715.42 Million in 2025, growing at a CAGR of 11.5% from 2025 to 2032.

Residential Robotic Vacuum Cleaner Market Scope & Overview:

Residential robotic vacuum cleaner refer to autonomous cleaning devices that are designed for household cleaning applications. These vacuum cleaners utilize various technologies such as sensors, mapping, and machine learning to efficiently move and navigate around a home, avoid obstacles, and clean multiple surfaces, such as hardwood floors, carpets, tiles, and others. Moreover, the utilization of robotic vacuum cleaner offers a range of benefits such as ease of cleaning, increased convenience, efficient cleaning, automatic charging, and others. The aforementioned benefits of robotic vacuum cleaners are key determinants for increasing its utilization in residential cleaning applications.

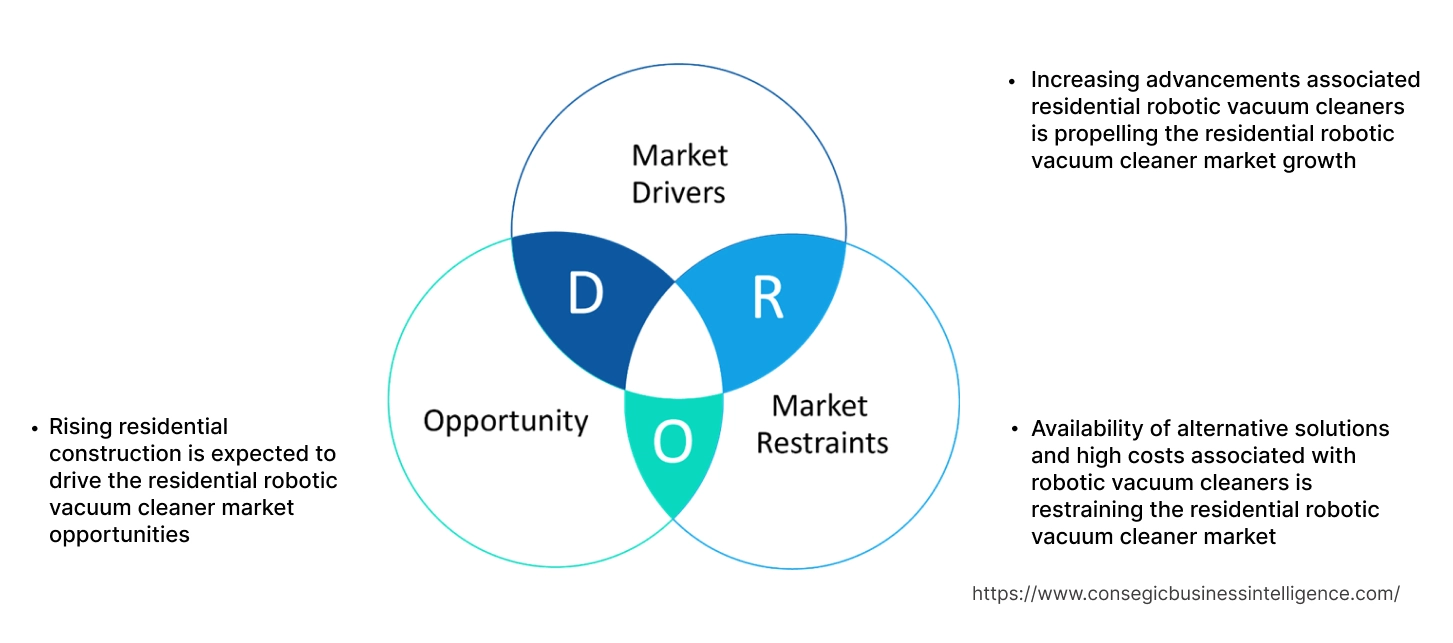

Residential Robotic Vacuum Cleaner Market Dynamics - (DRO) :

Key Drivers:

Increasing advancements associated residential robotic vacuum cleaners is propelling the residential robotic vacuum cleaner market growth

Robotic vacuum cleaner manufacturers are frequently investing in the development of new technologies associated with robotic vacuum cleaners to ensure its safe and effective utilization in residential cleaning applications. As a result, robotic vacuum cleaner manufacturers are launching new products with updated feature, which in turn is driving the market.

- For instance, in April 2024, iRobot Corporation launched its new Roomba Combo Essential robot, which is an easy-to use 2-in-1 robot vacuum and mop. The robotic vacuum cleaner is capable of delivering cleaning essentials with improved performance and wide range of features.

- Additionally, in September 2024, SharkNinja Inc. launched its new Shark PowerDetect NeverTouch Pro model of 2-in-1 robot vacuum and mop, which integrates performance, power, and intelligence to offer enhanced cleaning. The robotic vacuum cleaner features PowerDetect technology that is capable of detecting dirt, floor types, edges, and corners to elevate cleaning capabilities while reducing human involvement.

Hence, as per the analysis, the rising advancements associated with robotic vacuum cleaners for utilization in residential cleaning applications are proliferating the residential robotic vacuum cleaner market size.

Key Restraints:

Availability of alternative solutions and high costs associated with robotic vacuum cleaners is restraining the residential robotic vacuum cleaner market

There are several alternative solutions for robotic vacuum cleaners for residential cleaning applications including electric or handheld vacuum cleaners and conventional cleaning tools such as broom and mops, which is a primary factor restricting the market. In addition, robotic vacuum cleaners are also associated with relatively higher costs in comparison to manual/electric vacuum cleaners, which may further limit its adoption.

Handheld vacuum cleaners refer to small, portable devices that are ideal for quick clean-ups, particularly in small or tight spaces. Electric vacuum cleaners operate manually and offers numerous benefits including ease of utilization, portability, convenient storage, quick cleaning, maneuverability, and lower cost among others. Meanwhile, conventional cleaning tools such as broom and mops offer thorough cleaning and are capable of removing sticky residues, stains, and spills that robotic vacuum cleaners may struggle with.

Further, robotic vacuum cleaners are usually available at a higher costs as compared to manual/electric vacuum cleaners with average price ranging from USD 160 to USD 1,000 per unit or more, depending on the type, features, and specification of the vacuum cleaners. Hence, the availability of alternative solutions and high costs associated with robotic vacuum cleaners are hindering the residential robotic vacuum cleaner market expansion.

Future Opportunities :

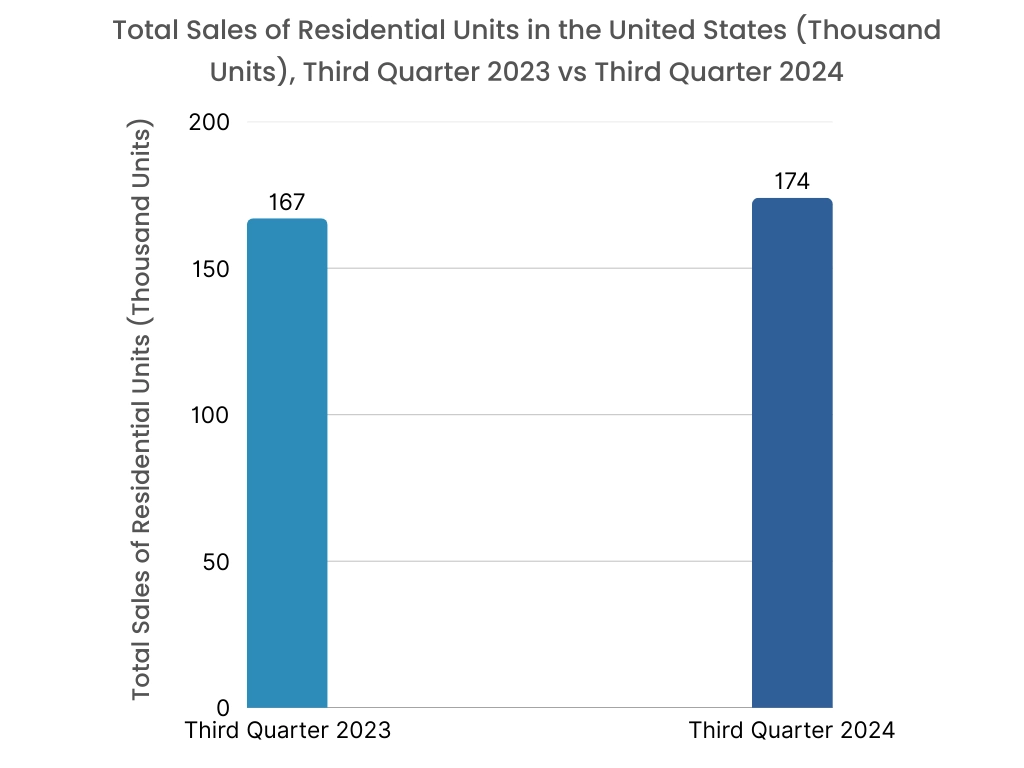

Rising residential construction is expected to drive the residential robotic vacuum cleaner market opportunities

The rise in residential construction is expected to provide lucrative aspect for market growth. Robotic vacuum cleaners are primarily used in residential sector for automated cleaning of indoor and outdoor residential spaces. Moreover, the ability of robotic vacuum cleaners to efficiently move and navigate around a home, avoid obstacles, and clean multiple surfaces, such as hardwood floors, carpets, tiles, and others, makes it ideal for utilization in residential cleaning applications.

- For instance, according to the United States Census Bureau, the total number of new residential units sold in the United States reached up to 174 thousand units during the third quarter of 2024, witnessing an increase of 4.2% in comparison to 167 thousand units in third quarter of 2023.

Hence, as per the analysis, the rising residential construction is anticipated to increase the adoption of robotic vacuum cleaners for automated cleaning of indoor and outdoor residential spaces, in turn driving the residential robotic vacuum cleaner market opportunities during the forecast period.

Residential Robotic Vacuum Cleaner Market Segmental Analysis :

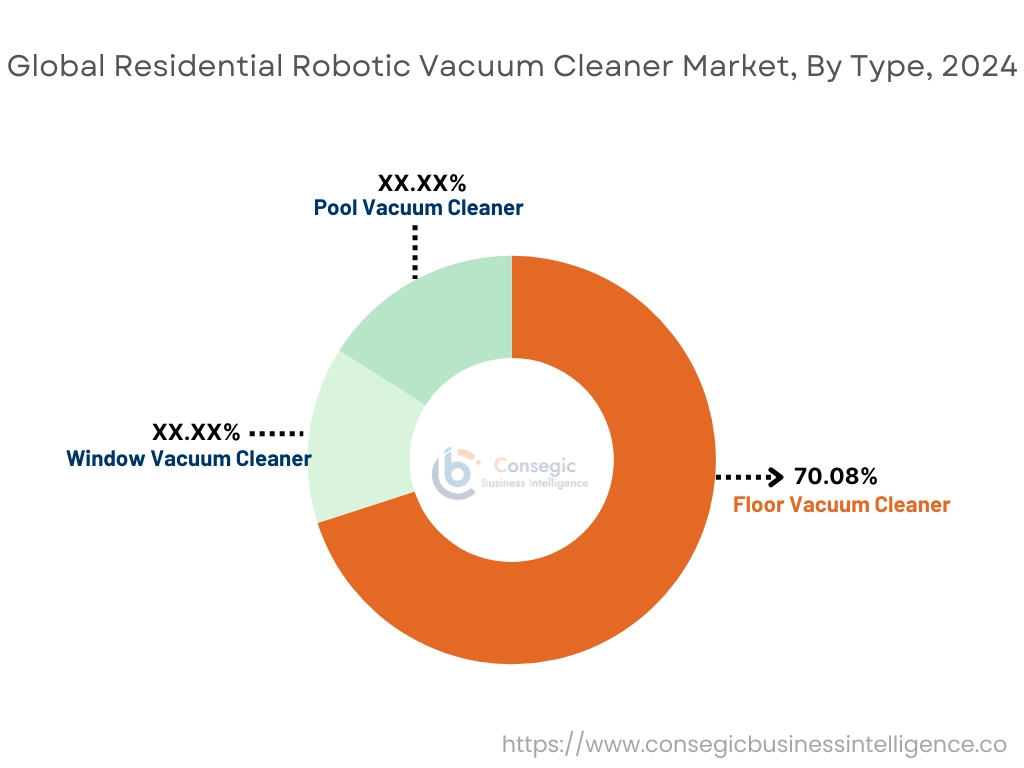

By Type:

Based on type, the market is segmented into floor vacuum cleaner, window vacuum cleaner, and pool vacuum cleaner.

Trends in the type:

- Increasing adoption of floor vacuum cleaners in residential spaces, attributing to its ability to clean multiple surfaces, such as hardwood floors, tiles, carpets, and others.

- Increasing technological advancements associated with window vacuum cleaners for facilitating automated and efficient cleaning of windows in residential spaces.

The floor vacuum cleaner segment accounted for the largest revenue share of 70.08% in the total residential robotic vacuum cleaner market share in 2024, and it is anticipated to register a significant CAGR growth during the forecast period.

- Robotic floor vacuum cleaners refer to autonomous cleaning devices that are integrated with advanced sensors, mapping technology, and artificial intelligence for navigating and cleaning residential spaces with minimal human intervention.

- Robotic floor vacuum cleaners are capable of detecting different types of flooring surfaces, avoiding obstacles, and efficiently cleaning areas that are typically hard to reach, such as under furniture floor area and edges among others.

- For instance, iRobot Corporation offers Roomba s9+ model of self-emptying robot vacuum in its product offerings that are designed for floor cleaning application. The robotic floor vacuum cleaner offers sophisticated design and powerful suction for capturing dust and particles in corners and edges. The vacuum cleaner can adjust to different floor types and offer comprehensive cleaning without any requirement of human effort.

- According to the residential robotic vacuum cleaner market analysis, the rising advancements associated with robotic floor vacuum cleaners are driving the market.

By Cleaning Mode:

Based on cleaning mode, the market is segmented into auto cleaning, spot cleaning, edge cleaning, turbo cleaning, and others.

Trends in the cleaning mode:

- Rising trend towards adoption of auto cleaning mode in robotic vacuum cleaners due to its several benefits including automated scheduling, optimized cleaning, consistency in cleaning operations, and others.

- Increasing adoption of spot cleaning mode, attributing to its ability to facilitate targeted cleaning in a quicker and efficient manner.

The auto cleaning segment accounted for a significant revenue in the overall market in 2024.

- In auto cleaning mode, robotic vacuum cleaners are optimized for comprehensively cleaning of the complete area at once while covering all reachable places until the cleaning task is completed or the battery needs to be recharged.

- Auto cleaning mode is designed for cleaning the entire area as efficiently as possible in one cleaning cycle in order to avoid repeated cleaning of the same area, which further saves battery power and improves cleaning efficiency.

- Moreover, auto cleaning mode offers a range of benefits including whole home coverage, automated scheduling, optimized cleaning, consistency in cleaning operations, and others.

- For instance, Neato Robotics Inc. is a robotic vacuum cleaner manufacturer that offers a broad range of residential robotic vacuum cleaners integrated with auto cleaning mode in its product portfolio. The auto cleaning mode enables the robotic vacuum to detect diverse flooring types automatically and switch between cleaning modes on hard floors and carpeted surfaces for optimizing brush and motor speed for that specific surface type.

- Therefore, increasing advancements related to robotic vacuum cleaners integrated with auto cleaning mode are driving the residential robotic vacuum cleaner market growth.

The spot cleaning segment is anticipated to register a substantial CAGR growth during the forecast period.

- In spot cleaning mode, robotic vacuum cleaners are optimized to focus on a small, specific area that requires extra attention during cleaning. The user typically activates spot cleaning mode manually, which directs the vacuum to a particular spot for extensive cleaning purpose.

- Moreover, spot cleaning mode is ideal for addressing localized stains, spills, or heavy dirt accumulation in a specific area of the floor.

- Additionally, spot cleaning mode is capable of quickly and effectively cleaning small spaces without the necessity to run a full cleaning cycle for an entire room, thereby, saving time and energy.

- For instance, Ecovacs Robotics offers a range of robotic vacuum cleaners with spot cleaning mode in its product offerings. The spot cleaning mode enables the robot to clean a localized area intensely.

- Hence, the increasing development of robotic vacuum cleaners integrated with spot cleaning mode for residential cleaning application is anticipated to boost the residential robotic vacuum cleaner market size during the forecast period.

By Sales Channel:

Based on sales channel, the market is segmented into online and offline.

Trends in the sales channel:

- Factors including the availability of targeted advertising, ease of utilization, competitive pricing, along with reliable shipping and return policies are key prospects driving the online sales channel segment.

- Factors such as higher credibility, strong customer base, and ease of customization as per the target market are major determinants for driving the offline sales channel segment.

Online sales channel segment accounted for a significant revenue in the overall residential robotic vacuum cleaner market share in 2024.

- Online sales channel deploys a mode of distribution in which the manufacturers sell the products through the company websites or any other third-party e-commerce websites that are available on the internet.

- Online sales channels offer various benefits including a quicker buying process, easy access to the products, and higher flexibility.

- Moreover, the availability of robotic vacuum cleaners in online sales channels allows quicker comparison of multiple products and prices and reduces overhead as compared to offline sales channels.

- For instance, iRobot Corporation and Samsung are few of the robotic vacuum cleaner manufacturers that offers a broad range of robotic vacuum cleaners for direct online purchase through the company’s website. Additionally, iRobot Corporation and Samsung also offers its robotic vacuum cleaners for online purchase through e-commerce platforms such as Amazon, eBay, and others.

- Therefore, increasing availability of robotic vacuum cleaners in online sales channels are driving the residential robotic vacuum cleaner market trends.

Offline sales segment is anticipated to register a substantial CAGR growth during the forecast period.

- Offline sales channel involves the distribution of robotic vacuum cleaners from manufacturers to the end-users directly or indirectly through offline distributors such as hypermarkets/supermarkets, specialty stores, and others.

- In addition, offline sales channels play a significant role in enhancing the product supply and fulfilling customer demands in the local markets, which is a prime factor in increasing its utilization for the distribution of robotic vacuum cleaners.

- For instance, Chroma and Reliance Digital are Indian retail chains of consumer electronics and goods that offers a wide range of robotic vacuum cleaners for offline purchase through its several retail outlets that are prevalent in multiple cities across India.

- Thus, the rising availability of robotic vacuum cleaners in offline sales channel is projected to boost the market during the forecast period.

By Price Range:

Based on price range, the market is segmented into below USD 250, USD 250-500, and above USD 500.

Trends in the price range:

- Factors including increasing advancements in vacuum cleaners and growing consumer preference for economical, efficient, and compact robotic vacuum cleaners for residential cleaning applications are among the key prospects driving the USD 250-500 price range segment.

- Factors including growing need for compact vacuum cleaners, integrated with advanced features, enhanced aesthetics, and increased durability are propelling the adoption of robotic vacuum cleaners with price range above USD 500.

The USD 250-500 segment accounted for a significant revenue share in the overall market in 2024, and it is anticipated to register a substantial CAGR during the forecast period.

- Robotic vacuum cleaners with price range from USD 250-500 primarily offer improved performance and features as compared to entry-level lower cost models.

- Moreover, robotic vacuum cleaners with the price range between USD 250-500 are often equipped with advanced navigation systems, improved suction power, and additional features such as mapping, scheduling, app connectivity, improved battery life, and multiple cleaning mode options among others.

- For instance, Neato Robotics Inc. offers Neato D8 and Neato D9 models of robotic vacuum cleaner for residential application in its product offerings. The robotic vacuum cleaners offer several features including deep cleaning, large coverage area, and LaserSmart SLAM technology with LIDAR for completely mapping, navigating, and cleaning the residential space.

- Hence, increasing advancements associated with robotic vacuum cleaners with price range from USD 250-500 are driving the market.

By Application:

Based on the application, the market is segmented into indoor cleaning and outdoor cleaning.

Trends in the application:

- Rising trend towards adoption of robotic vacuum cleaners for indoor cleaning applications due to its increased convenience, automated operations, consistency, and improved cleaning efficiency.

- Increasing adoption of robotic vacuum cleaners for outdoor residential cleaning applications such as patios or deck cleaning and pool cleaning among others.

Indoor cleaning segment accounted for the largest revenue share in the total market in 2024, and it is anticipated to register substantial CAGR growth during the forecast period.

- Robotic vacuum cleaners are primarily used in residential households for cleaning indoor surfaces including hardwood floors, tiles, carpets, and others.

- Many robotic vacuum cleaners feature edge cleaning mode, which enables them to effectively clean edges and corners of indoor residential spaces.

- Moreover, robotic vacuum cleaners are capable of navigating through different room layouts, cleaning under furniture, and tight spaces, which makes it ideal for indoor cleaning applications.

- For instance, in 2024, Ecovacs Robotics launched its DEEBOT Y1 PRO model of robotic vacuum cleaner, which is designed for residential cleaning applications including indoor cleaning. The robotic vacuum cleaner is specifically designed to clean hard floors and can sustainably clean for 320 minutes on a full charge.

- According to the analysis, the rising development of robotic vacuum cleaners for indoor cleaning applications is turn propelling the market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

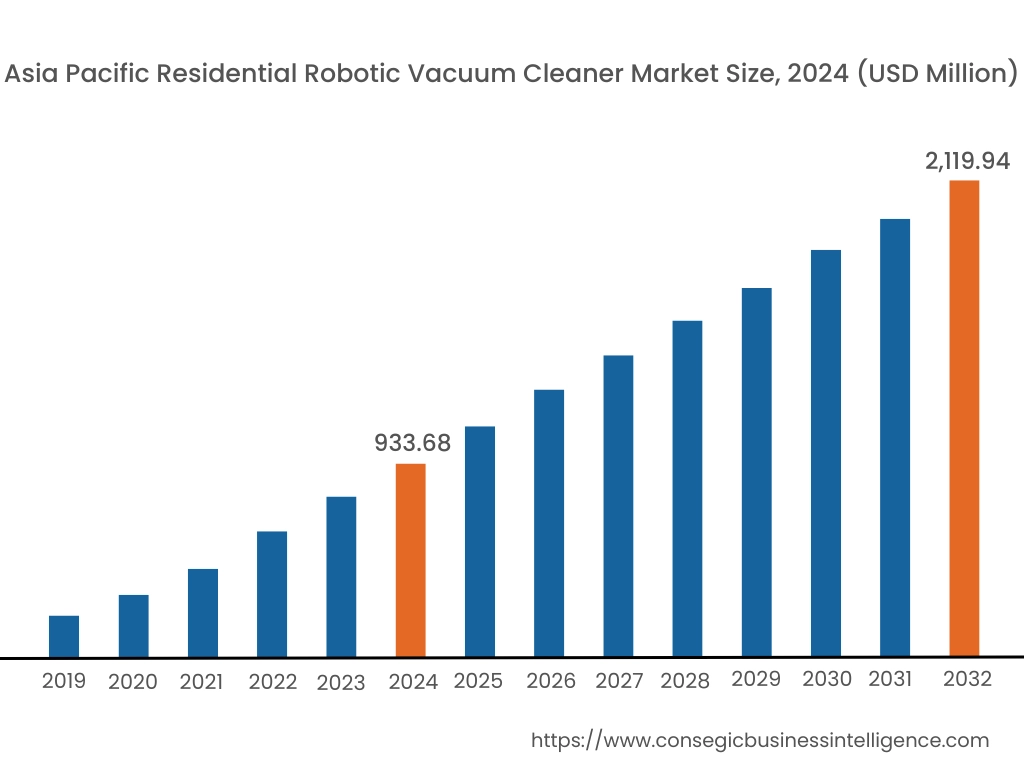

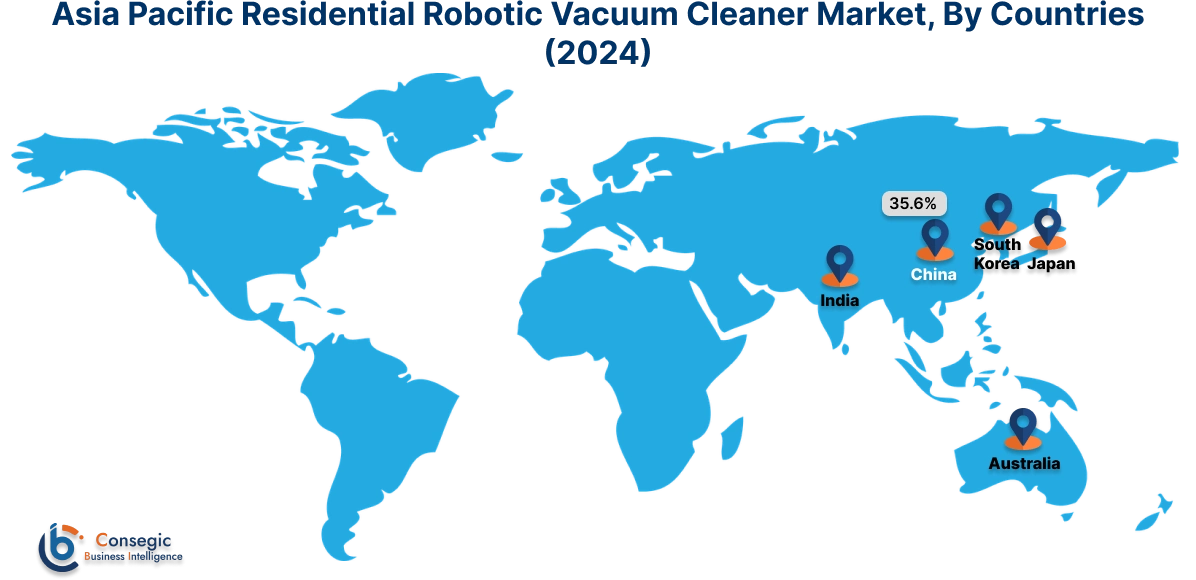

Asia Pacific region was valued at USD 933.68 Million in 2024. Moreover, it is projected to grow by USD 1,020.27 Million in 2025 and reach over USD 2,119.94 Million by 2032. Out of this, China accounted for the maximum revenue share of 35.6%. As per the residential robotic vacuum cleaner market analysis, the adoption of robotic vacuum cleaners in the Asia-Pacific region is primarily driven by rising disposable income and increasing development of residential spaces among others. Additionally, the rising adoption of robotic vacuum cleaners in residential spaces due to its increased convenience, automated operations, and improved energy efficiency is further accelerating the residential robotic vacuum cleaner market expansion in the Asia-Pacific region.

- For instance, according to the Building and Construction Authority of Singapore, the total construction demand including residential construction in Singapore reached between USD 24 billion to USD 29 billion by the end of 2024. The above factors are further driving the adoption of robotic vacuum cleaners in residential spaces for automated and efficient cleaning operations, in turn propelling the robotic vacuum cleaner industry in the Asia-Pacific region.

North America is estimated to reach over USD 2,473.52 Million by 2032 from a value of USD 1,125.56 Million in 2024 and is projected to grow by USD 1,226.54 Million in 2025.

In North America, the growth of residential robotic vacuum cleaner industry is driven by rising investments in residential construction projects along with increasing sales of residential units among others. Similarly, the rising penetration of smart and connected devices in residential spaces is further contributing to the residential robotic vacuum cleaner market demand.

- For instance, according to the United States Census Bureau, the total number of new residential units sold in the United States reached up to 666 thousand units in 2023, witnessing an increase of nearly 4% in comparison to 641 thousand units in 2022. The above factors are projected to drive the residential robotic vacuum cleaner market trends in North America during the forecast period.

The regional analysis depicts that the prevalence of favorable government measures for smart homes and rising adoption of robotic vacuum cleaners in residential spaces are driving the residential robotic vacuum cleaner market demand in Europe. Furthermore, as per the market analysis, the market demand in Latin America, Middle East, and African regions is expected to grow at a considerable rate due to factors such as rising pace of urbanization, increasing development of residential spaces, and growing demand for automated cleaning devices among others.

Top Key Players and Market Share Insights:

The global residential robotic vacuum cleaner market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the residential robotic vacuum cleaner market. Key players in the residential robotic vacuum cleaner industry include-

- iRobot Corporation (United States)

- Ecovacs Robotics (China)

- Miele & Cie. KG (Germany)

- Robert Bosch GmbH (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Haier Group (China)

- Dyson Ltd (Singapore)

- SharkNinja Operating LLC (United States)

- Samsung (South Korea)

- Neato Robotics Inc. (United States)

- Roborock Technology Co., Ltd. (China)

- Panasonic Corporation (Japan)

Recent Industry Developments :

Product Launch:

- In January 2025, Roborock introduced its new Saros series of robotic vacuum cleaners, which includes the first mass-produced robotic vacuum integrated with a five-axis mechanical arm. The Saros Z70 features ultimate floor coverage while ensuring thorough cleaning with minimal effort.

- In September 2024, SharkNinja Inc. introduced its new Shark PowerDetect NeverTouch Pro model of 2-in-1 robot vacuum and mop. The 2-in-1 robotic vacuum and mop integrates performance, power, and intelligence to offer enhanced cleaning.

- In April 2024, iRobot Corporation launched its new Roomba Combo Essential robot, which is a 2-in-1 robotic vacuum and mop that is integrated with numerous features to deliver improved cleaning performance.

Residential Robotic Vacuum Cleaner Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 7,490.97 Million |

| CAGR (2025-2032) | 11.5% |

| By Type |

|

| By Cleaning Mode |

|

| By Sales Channel |

|

| By Price Range |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the residential robotic vacuum cleaner market? +

The residential robotic vacuum cleaner market was valued at USD 3,409.58 Million in 2024 and is projected to grow to USD 7,490.97 Million by 2032.

Which is the fastest-growing region in the residential robotic vacuum cleaner market? +

Asia-Pacific is the region experiencing the most rapid growth in the residential robotic vacuum cleaner market.

What specific segmentation details are covered in the residential robotic vacuum cleaners report? +

The residential robotic vacuum cleaner report includes specific segmentation details for type, cleaning mode, sales channel, price range, application, and region.

Who are the major players in the residential robotic vacuum cleaner market? +

The key participants in the residential robotic vacuum cleaner market are iRobot Corporation (United States), Ecovacs Robotics (China), Dyson Ltd (Singapore), SharkNinja Operating LLC (United States), Samsung (South Korea), Neato Robotics Inc. (United States), Roborock Technology Co., Ltd. (China), Panasonic Corporation (Japan), Miele & Cie. KG (Germany), Robert Bosch GmbH (Germany), Koninklijke Philips N.V. (Netherlands), and Haier Group (China).