- Summary

- Table Of Content

- Methodology

Residential Furnace Market Size:

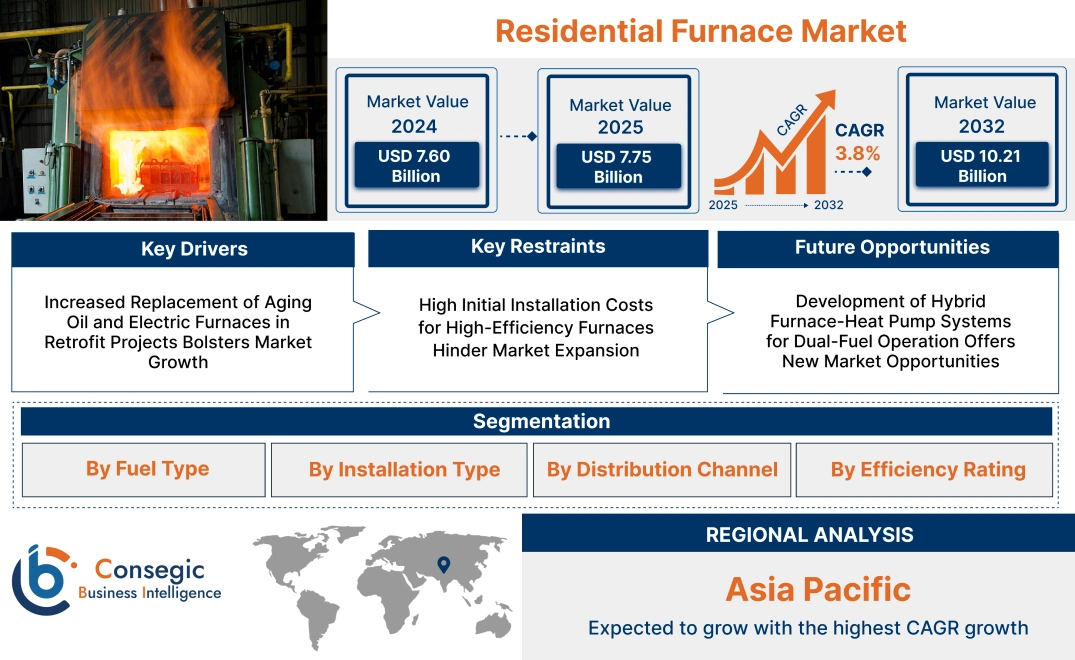

Residential Furnace Market size is estimated to reach over USD 10.21 Billion by 2032 from a value of USD 7.60 Billion in 2024 and is projected to grow by USD 7.75 Billion in 2025, growing at a CAGR of 3.8% from 2025 to 2032.

Residential Furnace Market Scope & Overview:

A residential furnace is a domestic heating equipment intended to produce and spread warm air with the help of ductwork by either combustion or electrical resistance. Natural gas, oil, and electricity are some of the prevalent types of fuels utilized, with system designs adjusted to accommodate diverse climatic conditions and building configurations.

These units feature essential elements like thermostatic controls, heat exchangers, burners or heat sources, and blowers. Sophisticated units provide multi-stage operation, programmable options for indoor comfort and energy optimization, as well as variable-speed blowers.

Advantages of residential furnaces include fast heat transfer, consistent temperature control, and compatibility with both new construction and retrofit applications. Their integration with smart home platforms further increases user experience and efficiency. Engineered for durability and simplicity, residential furnace systems continue to be central to single-family homes, apartments, and multi-unit dwellings in search of dependable space heating during winter periods. Their versatility and efficiency make them the hub of contemporary residential HVAC installations.

Residential Furnace Market Dynamics - (DRO) :

Key Drivers:

Increased Replacement of Aging Oil and Electric Furnaces in Retrofit Projects Bolsters Market Growth

A substantial share of North American and European residential heating systems are based on old oil-fired or low-efficiency electric furnaces. These old systems are commonly linked with high energy usage, uneven heating, and antiquated control interfaces. With increasing energy costs and stricter emission regulations, homeowners are upgrading to new gas-fired or dual-stage high-efficiency furnaces. Retrofit work, most notably in suburban and rural properties constructed prior to 2000, is propelling a healthy replacement cycle. New furnaces provide improved modulation, zoning adaptability, and smart thermostat compatibility—things that enhance indoor comfort and operating savings. In areas where there are rebate programs and energy efficiency requirements, replacement activity is being increased even more. This mass-scale upgrade phenomenon is adding substantially to increasing demand throughout the industry and is a main driver of residential furnace market expansion.

Key Restraints:

High Initial Installation Costs for High-Efficiency Furnaces Hinder Market Expansion

The expense of purchasing and installing high-efficiency furnaces, particularly condensing models, is still a primary deterrent to broad-based adoption, especially in existing homes that need additional venting work or condensate drainage systems. The units are much more expensive than base models, and the labor, permits, and component upgrades required drive the total installation costs well above homeowner budgets. For non-qualifying properties, the payback period for return on investment is longer, constraining appeal to cost-conscious consumers. For areas with infrequent heating demand, or where electric space heating alternatives are possible, customers are less inclined to invest in premium installations. This price difference slows the rate of equipment turnover, particularly in older buildings with few energy-efficient upgrades. Consequently, even as awareness of energy savings increases, affordability limitations are still a fundamental barrier to in the residential furnace market growth.

Future Opportunities :

Development of Hybrid Furnace-Heat Pump Systems for Dual-Fuel Operation Offers New Market Opportunities

Hybrid heating systems with a high-efficiency furnace and electric heat pump are becoming popular in markets where climate conditions are variable, and energy prices seasonally fluctuate. These systems balance performance by running the heat pump in less extreme outside temperatures and running the furnace when the temperature is severely cold, offering a balance of energy savings and consistent comfort. Utilities and HVAC contractors are increasingly suggesting dual-fuel systems to homeowners as a way to lower carbon emissions without completely giving up gas infrastructure. Smart controls have improved to enable smooth switching between heat sources according to outdoor temperature, cost per BTU, or occupancy schedules. Flexible and efficient heating is in growing demand across retrofit and new construction segments. This trend coincides with regulatory changes towards fuel diversity and electrification—locating hybrid systems as a leading facilitator of residential furnace market opportunity fueled by necessity and long-term growth.

Residential Furnace Market Segmental Analysis :

By Fuel Type:

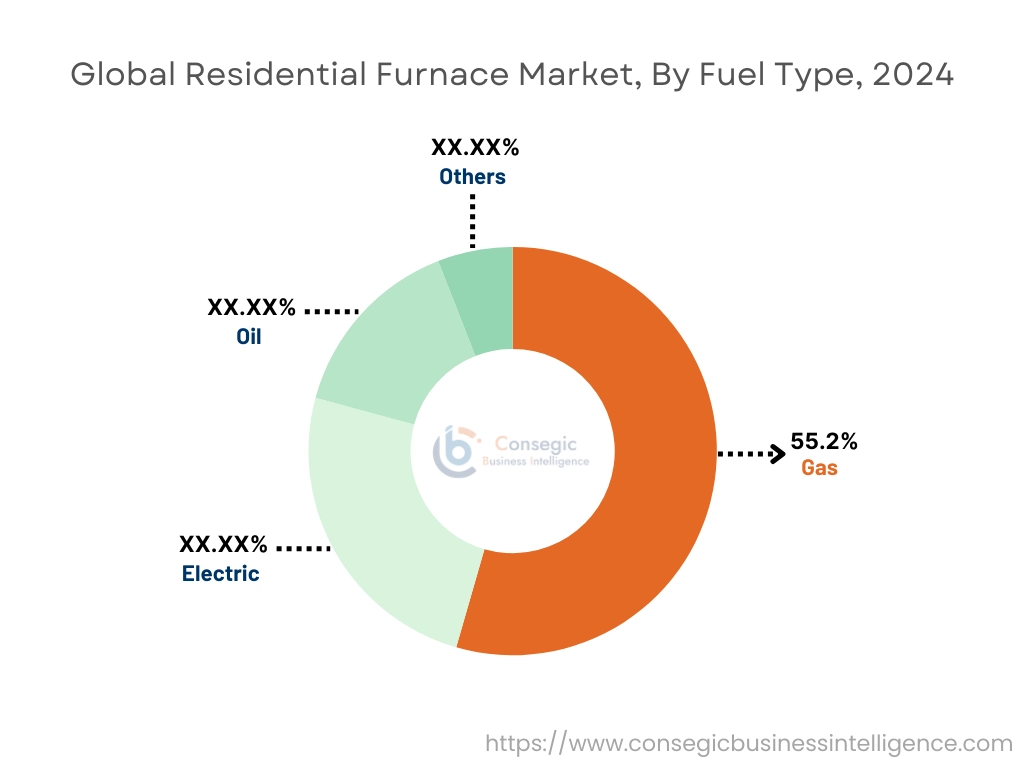

Based on fuel type, the residential furnace market is segmented into gas, electric, oil, and others.

Gas furnaces held the largest share of 55.2% in 2024.

- Gas furnaces are preferred for their rapid heat generation and lower operating costs compared to electric or oil-based systems, particularly in North America.

- Technological enhancements in condensing gas furnaces have improved energy utilization, contributing to increased adoption.

- The combination of efficient combustion and compatibility with existing HVAC ductwork boosts gas furnace deployment across suburban households.

- The residential furnace market demand is further driven by regulatory support for cleaner combustion technologies in this segment.

The electric furnace segment is projected to witness the fastest CAGR during the forecast period.

- Electric furnaces are gaining traction due to their ease of installation, reduced emissions, and suitability for homes without access to natural gas.

- Rising trends in electrification and renewable power integration align with the adoption of electric heating systems.

- The minimal maintenance requirements and safer operation of electric furnaces appeal to modern residential developments.

- As per residential furnace market analysis, growth in off-grid and energy-efficient housing units is favoring this segment.

By Installation Type:

Based on installation type, the market is segmented into new installation and replacement installation.

Replacement installation accounted for the largest residential furnace market share in 2024.

- Aging residential infrastructure and rising energy costs are driving the replacement of outdated and inefficient furnaces.

- Government incentives promoting energy-efficient upgrades further support residential furnace market expansion through replacements.

- Replacement installations are cost-effective for homeowners already equipped with ducted systems and ventilation pathways.

- Trends in smart home integration are boosting replacement necessity for advanced models with programmable thermostats and energy-monitoring capabilities.

New installations are projected to grow significantly with the fastest CAGR over the forecast period.

- Population growth and urbanization in emerging economies are fueling residential construction, requiring new heating systems.

- Sustainability goals and modern building codes are emphasizing installation of high-efficiency furnaces in new homes.

- Technological trends such as remote-controlled systems and zoned heating are enhancing new installation appeal.

- According to the residential furnace market analysis, green building certifications and HVAC system design optimization contribute to this segment’s growth.

By Distribution Channel:

By distribution channel, the residential furnace market is segmented into direct sales, HVAC contractors & installers, retail (home improvement stores), and online retail.

HVAC contractors & installers held the dominant share in 2024.

- Consumers rely on professional installers for system selection, proper sizing, and performance assurance.

- HVAC contractors often form partnerships with manufacturers, providing exclusive access to advanced models and maintenance packages.

- This channel supports both retrofitting and custom installations for varying household needs and preferences.

- Residential furnace market demand is maintained through scheduled servicing and seasonal upgrades by professional installers.

Online retail is forecasted to register the fastest CAGR during the forecast period.

- Digital platforms offer extensive product choices, transparent pricing, and convenience, appealing to DIY homeowners and tech-savvy consumers.

- Manufacturers are strengthening their online presence with virtual configuration tools and smart integration packages.

- E-commerce platforms are expanding reach in suburban and rural areas with reliable logistics and installation support.

- As highlighted in residential furnace market trends, this channel benefits from rising online shopping habits, particularly among younger homeowners.

By Efficiency Rating:

Based on efficiency rating, the market is categorized into standard efficiency, mid-efficiency, high efficiency, and ultra-high efficiency.

The high efficiency segment held the leading residential furnace market share in 2024.

- These systems typically operate at 90%-96% AFUE (Annual Fuel Utilization Efficiency), offering substantial energy savings.

- Energy Star certifications and local rebates are propelling the adoption of high-efficiency models across key regions.

- Enhanced features like sealed combustion chambers and secondary heat exchangers contribute to both safety and performance.

- Hence, the rising favor of high-efficiency units by customers due to long-term cost savings and environmental considerations is driving residential furnace market growth.

The ultra-high efficiency segment is anticipated to experience the fastest CAGR in the coming years.

- These units exceed 97% AFUE, supported by dual heat exchangers and modulating burners for optimal control.

- Need for net-zero energy homes and passive building technologies aligns with ultra-high efficiency solutions.

- For instance, in November 2023, Navien began shipping their latest innovation, the NPF Hydro-furnace. First launched in September 2023, the NPF Hydro-furnace is available in upflow and horizontal configurations, and two sizes -60,000 BTU/h and 100,000 BTU/h. with an efficiency of 97% AFUE, it also meets the SCAQMD rule 1111 requirements.

- Innovations in furnace design and integration with renewable sources like solar-assisted HVAC are driving interest.

- As per residential furnace market trends, stringent emission regulations and climate commitments are influencing buyers to adopt these advanced systems.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

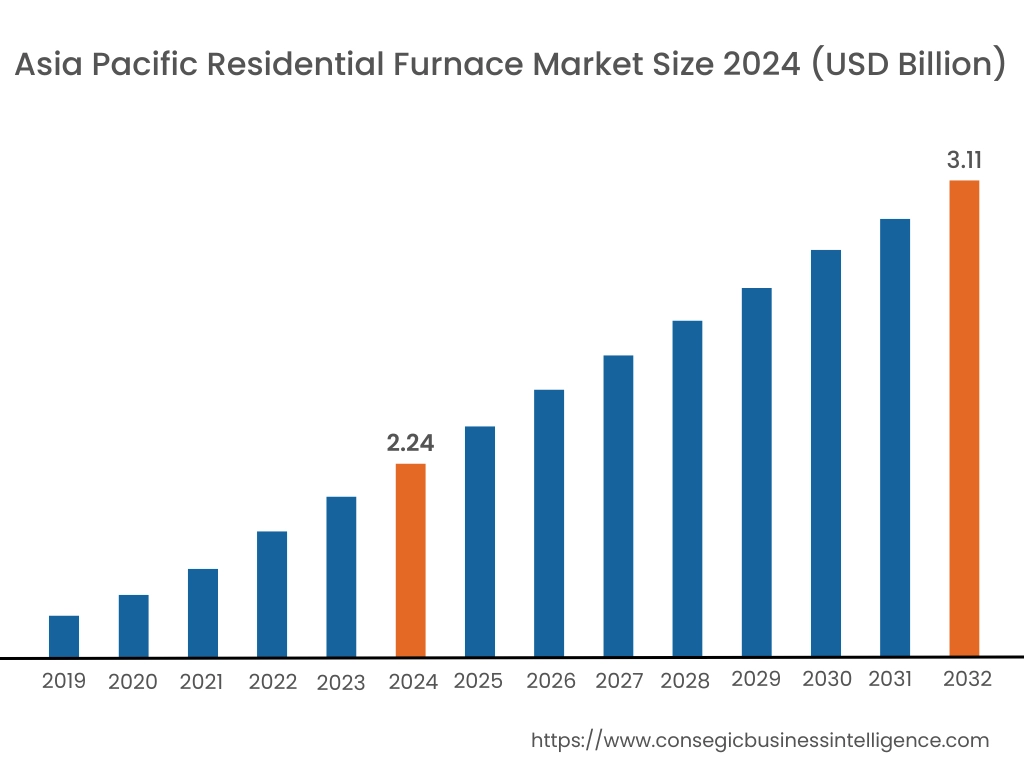

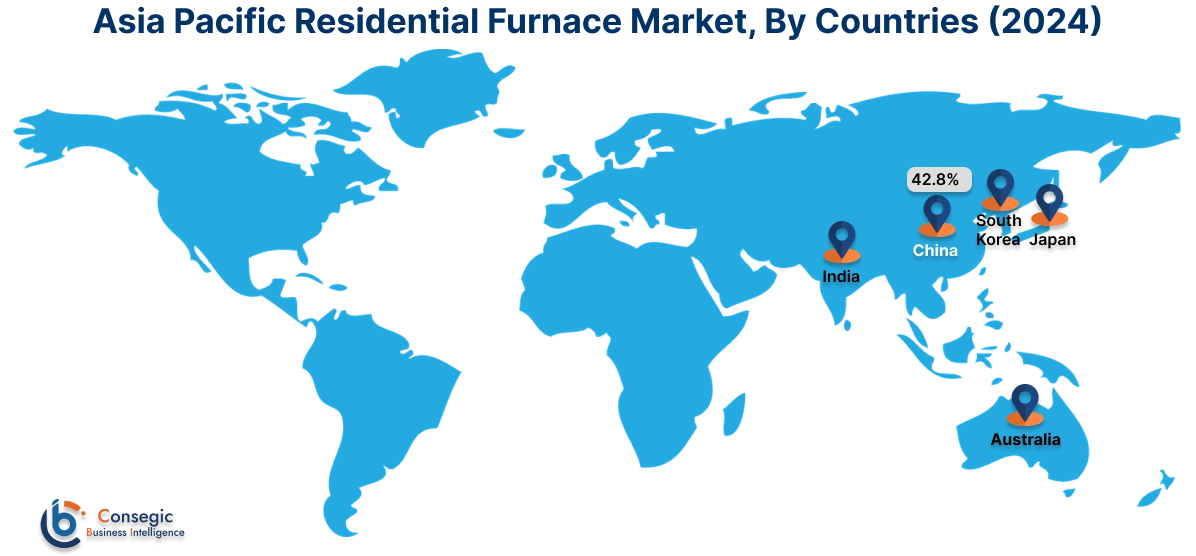

Asia Pacific region was valued at USD 2.24 Billion in 2024. Moreover, it is projected to grow by USD 2.29 Billion in 2025 and reach over USD 3.11 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. The region is experiencing rapid growth in the residential furnace industry, especially in countries with colder winters like northern China, South Korea, and sections of Japan. Urbanization and growing middle-class incomes are fueling investments in space heating technologies that combine comfort and efficiency. Market trends show increasing demand for electric and gas-powered systems for small houses and apartments, particularly in new residential complexes. In addition, government-mandated energy-saving standards and air quality regulations are driving the uptake of low-emission and energy-saving heating products. Local manufacturing capacity and increased awareness of clean indoor air are influencing the competitive environment.

North America is estimated to reach over USD 3.31 Billion by 2032 from a value of USD 2.52 Billion in 2024 and is projected to grow by USD 2.57 Billion in 2025. North America is a major region, particularly in cold climates, where centralized heating is still a necessity. For a long time, the United States and Canada have been dependent on gas- and oil-burning furnaces in suburban residential dwellings, but recent regulatory initiatives are pushing the industry to high-efficiency electric and hybrid configurations. Market research indicates robust replacement demand as older equipment is retired and replaced with ENERGY STAR-certified and low-NOx emission variants. Moreover, home heating electrification in aid of decarbonization plans is also creating prospects for condensing furnaces and interfacing with intelligent thermostats. Expansion within this area is also supported by state rebate policies and more stringent building energy regulations.

Europe is characterized by a highly developed but gradually evolving market driven by the phase-out of fossil fuels and the utilization of renewable heating sources. These nations, like Germany, France, and Sweden, are increasingly departing from conventional furnace systems and opting for low-carbon solutions such as heat pumps and pellet-based systems. Observations indicate that although traditional systems continue to be available in aged homes, renovation schemes and penalties against emissions are inhibiting new installations. Yet, hybrid options blending furnaces with renewable technologies are becoming popular. The European residential furnace market hence has to conform to the climate goals of the EU, focusing on ultra-efficiency designs and integration with green heating infrastructures.

Latin America has a fairly moderate market, mainly scattered across the higher altitudes and southern regions of nations such as Chile, Argentina, and Brazil. The market is still fragmented, and heating requirements is seasonal and mostly fulfilled by portable or decentralized systems. Nevertheless, as urban areas become more modernized and housing projects rise in colder regions, analysis indicates growing interest in fixed heating installations with better thermal efficiency. Residential furnace opportunity here is being backed by diversification of energy policies and initiatives for enhancing residential standards of living. Flexible, compact units needing minimal infrastructure are increasingly popular with middle-income households.

Demand for residential furnaces is restricted in the Middle East and Africa by largely warm climates, although niche uses are found in mountainous areas and colder countries such as Turkey, Iran, and South Africa. Where there is a requirement, it is most often in hybrid applications or newly constructed upscale residential developments focused on indoor thermal comfort. Market analysis indicates the potential for uptake in colder seasons, especially where electricity grids are solid and fuel prices are not excessive. This growth in this region will be selective, driven by new home construction and conformance with energy efficiency codes rather than broad replacement cycles.

Top Key Players and Market Share Insights:

The residential furnace market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global residential furnace market. Key players in the residential furnace industry include -

- Daikin Industries Ltd. (Japan)

- Bosch Thermotechnology (Germany)

- Fujitsu General Limited (Japan)

- Mitsubishi Electric Corporation (Japan)

- Ferroli S.p.A. (Italy)

- Viessmann Group (Germany)

- Vaillant Group (Germany)

- Wolf Steel Ltd. (Napoleon) (Canada)

- Groupe Atlantic (France)

- Baxi Heating (United Kingdom)

Recent Industry Developments :

Product Launches:

- In October 2023, Carrier unveiled an upgraded lineup of gas furnaces with Near Field Communication (NFC). This technology enables the modification of installation settings and the checking of diagnostic information using a mobile device. It also provides verification and troubleshooting tips.

Residential Furnace Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 10.21 Billion |

| CAGR (2025-2032) | 3.8% |

| By Fuel Type |

|

| By Installation Type |

|

| By Distribution Channel |

|

| By Efficiency Rating |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Residential Furnace Market? +

Residential Furnace Market size is estimated to reach over USD 10.21 Billion by 2032 from a value of USD 7.60 Billion in 2024 and is projected to grow by USD 7.75 Billion in 2025, growing at a CAGR of 3.8% from 2025 to 2032.

What specific segmentation details are covered in the Residential Furnace Market report? +

The Residential Furnace market report includes specific segmentation details for fuel type, installation type, distribution channel and efficiency rating.

What are the distribution channels of the Residential Furnace Market? +

The distribution channels of the Residential Furnace Market are direct sales, HVAC contractors & installers, retail (home improvement stores) and online retail.

Who are the major players in the Residential Furnace Market? +

The key participants in the Residential Furnace market are Daikin Industries, Ltd. (Japan), Bosch Thermotechnology (Germany), Fujitsu General Limited (Japan), Mitsubishi Electric Corporation (Japan), Viessmann Group (Germany), Vaillant Group (Germany), Wolf Steel Ltd. (Napoleon) (Canada), Groupe Atlantic (France), Baxi Heating (United Kingdom) and Ferroli S.p.A. (Italy).