- Summary

- Table Of Content

- Methodology

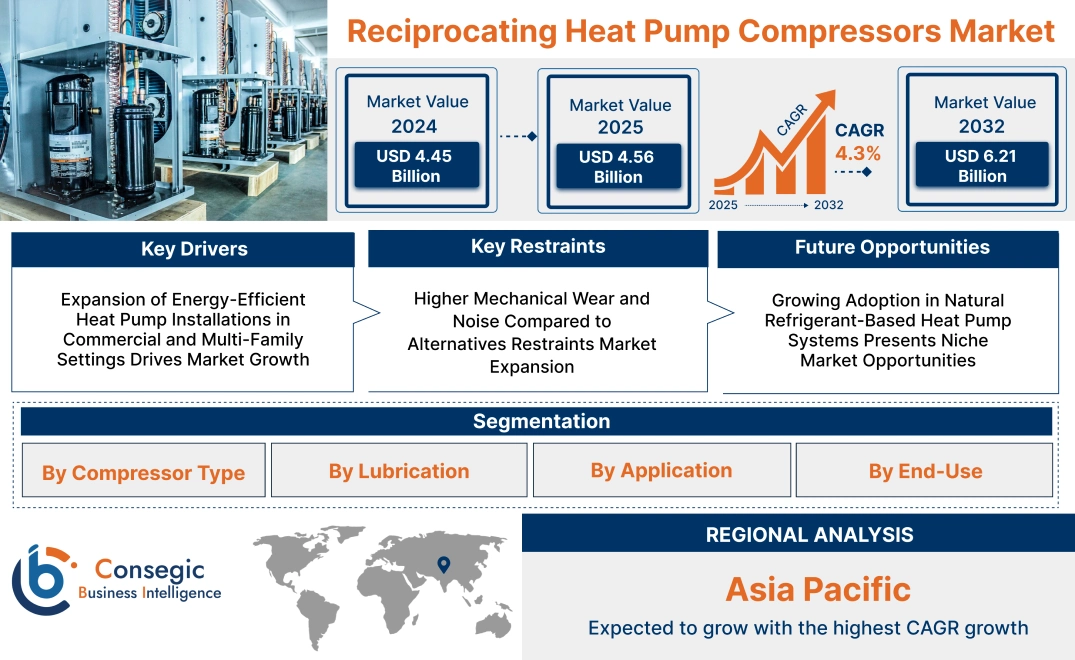

Reciprocating Heat Pump Compressors Market Size:

Reciprocating Heat Pump Compressors Market size is estimated to reach over USD 6.21 Billion by 2032 from a value of USD 4.45 Billion in 2024 and is projected to grow by USD 4.56 Billion in 2025, growing at a CAGR of 4.3% from 2025 to 2032.

Reciprocating Heat Pump Compressors Market Scope & Overview:

Reciprocating heat pump compressors are mechanical devices that transmit heat by compressing refrigerant through a piston-driven motion of sealed chambers. They are popularly used in residential, commercial, and light industrial heating and cooling systems due to their time-tested performance as well as the mechanical simplicity with which they have been developed.

Its characteristics include strong construction, capacity modulation under control, and compatibility with any refrigerant. Their compact and simple design enables easy integration into other heat pump arrangements, and multi-cylinder versions provide improved efficiency and operating balance.

Reciprocating heat pump compressors offer dependable thermal output and consistent performance under variable climate conditions. They are appreciated for their serviceability, cost-effectiveness, and capacity to satisfy moderate to high load requirements. Their flexibility to standard and custom system configurations makes them a critical component in new installations and retrofitted HVAC solutions in pursuit of reliable and controllable heating and cooling performance.

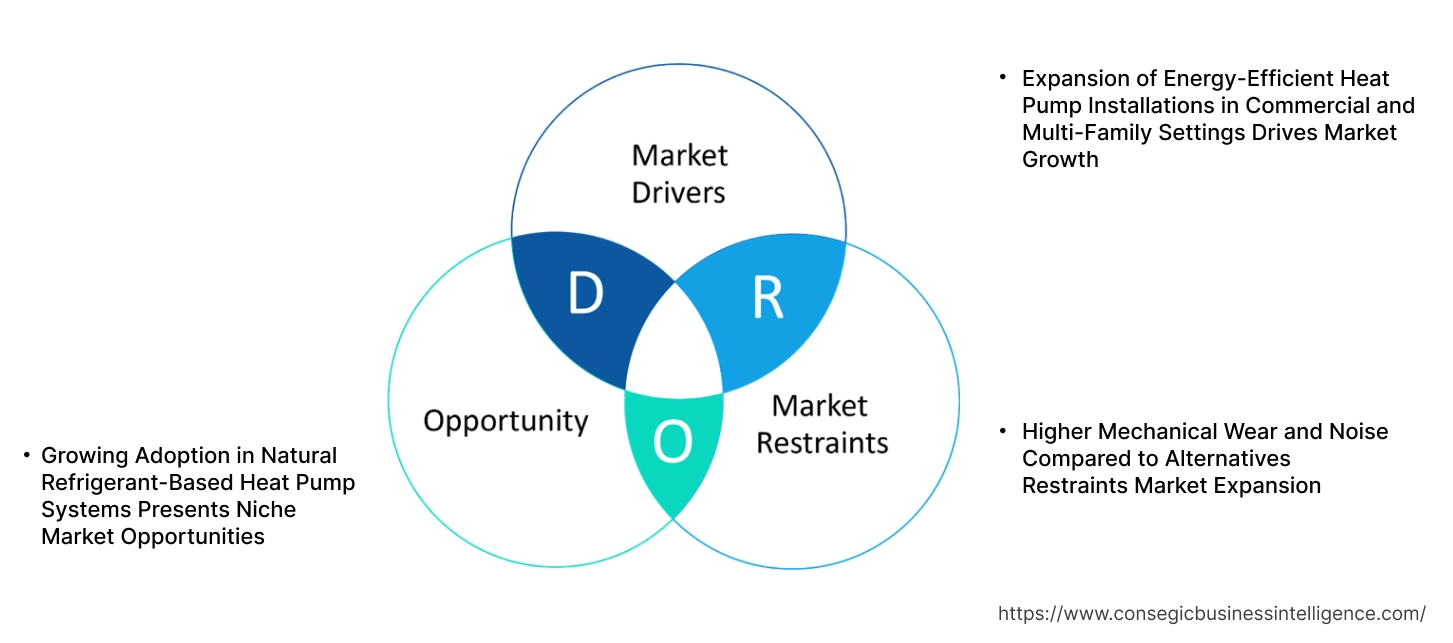

Reciprocating Heat Pump Compressors Market Dynamics - (DRO):

Key Drivers:

Expansion of Energy-Efficient Heat Pump Installations in Commercial and Multi-Family Settings Drives Market Growth

The push for building electrification and carbon reduction is hastening the adoption of energy-efficient heat pump systems in commercial offices, educational campuses, and multi-family housing. These systems increasingly depend on reciprocating compressors because they have strong performance under high-pressure conditions and can be used in medium-capacity applications. In multi-zone heating and cooling systems, reciprocating models offer modularity, redundancy, and simplicity of maintenance, making them well suited to decentralized plant rooms and rooftop applications. Their established reliability, easy servicing, and compatibility with legacy refrigerants have led them to be in used in retrofits and phased system upgrades. In addition, increasing the demand to meet energy performance directives like Europe's EPBD and North America's ASHRAE 90.1 is pushing developers to switch from fossil-fuel boilers to heat pumps. Increasing adoption of reciprocating compressors in such installations indicates a wider pattern of energy transition in the built environment, driving the reciprocating heat pump compressors market expansion.

Key Restraints:

Higher Mechanical Wear and Noise Compared to Alternatives Restraints Market Expansion

Reciprocating compressors function using pistons, valves, and crankshafts, which naturally create more mechanical friction and produce more acoustic emissions than scroll or rotary counterparts. This mechanical complexity causes more component wear, which requires regular maintenance to ensure peak performance. In contemporary building spaces where quiet operation and low maintenance are critical—like hospitals, high-end homes, and corporate headquarters—these disadvantages detract from system appeal. Moreover, the need for vibration dampening and acoustic insulation contributes to system installation expenses. Regardless of technological advancements, reciprocating systems continue to have higher maintenance intervals, particularly in part-load operation. In areas that implement noise regulations or green certification schemes, HVAC designers tend to prefer quieter alternatives with comparable efficiency at lower maintenance burden. These constraints decrease demand in premium segments, thus acting as a hindrance to broader adoption and eventually reciprocating heat pump compressors market growth.

Future Opportunities:

Growing Adoption in Natural Refrigerant-Based Heat Pump Systems Presents Niche Market Opportunities

Global shift toward sustainable refrigerants is promoting the use of heat pump systems running on natural products like CO₂, propane (R290), and ammonia. The refrigerants require compressors with the ability to withstand high discharge pressures, heat loads, and chemical reactivity. Reciprocating heat pump compressors have proven compatibility with such media, providing reliable performance and safety under harsh operating conditions. Their performance across system sizes makes them a strong value in industrial and residential large-volume applications where compliance to natural refrigerants is key. Low-GWP alternatives are becoming increasingly demanded as nations impose HFC phase-downs in line with the Kigali Amendment and regulate F-gases further. Compliance with climate-friendly refrigerants, with the capacity to deliver efficient and compliant performance, offers manufacturers a strategic back door into HVAC applications that will prove future-proof.

- For instance, in July 2024, Danfoss launched three new compressors for natural and low-GWP refrigerants: VZN inverter scroll, PSH scroll, and BOCK® semi-hermetic reciprocating HGX56 CO2 T. While the BOCK® HGX56 CO2 T is designed for large industrial heat pumps, the PSH scroll compressors is for reversible rooftop units and hydronic systems in cold climates, and the VZN inverter scroll compressors finds application in light commercial heat pumps. They offer clients flexibility and simplicity us use with any low-GWP or natural refrigerant heat pump.

This alignment with regulations and the environment is generating targeted reciprocating heat pump compressors market opportunities fueled by necessity and growth.

Reciprocating Heat Pump Compressors Market Segmental Analysis :

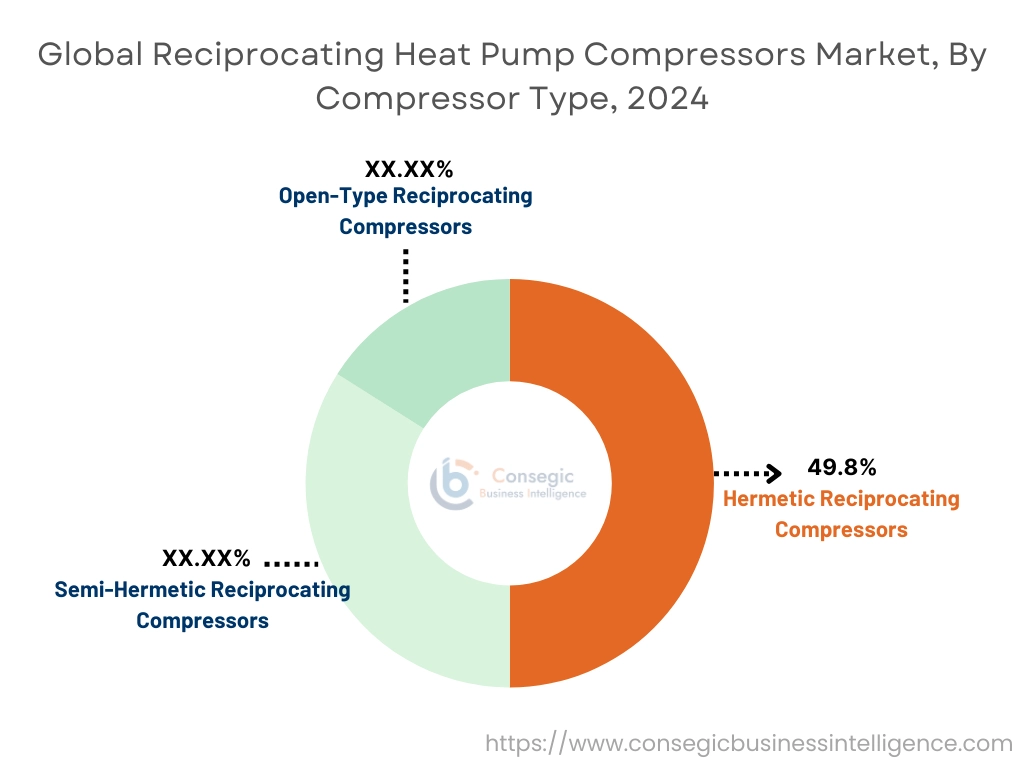

By Compressor Type:

Based on compressor type, the market is divided into hermetic reciprocating compressors, semi-hermetic reciprocating compressors, and open-type reciprocating compressors.

Hermetic reciprocating compressors accounted for the largest revenue share of 49.8% in 2024.

- Hermetic compressors are factory-sealed and optimized for compact applications such as residential heat pumps, offering ease of installation and minimal maintenance.

- The growing preference for compact, noise-reduced systems in urban residential developments is accelerating the demand for hermetic models.

- Advances in scroll and reciprocating integration, along with inverter-driven hermetic compressors, are boosting their energy performance in variable climate zones.

- As per the reciprocating heat pump compressors market analysis, this segment benefits from system-level integration with smart thermostats and high-efficiency heat pump designs.

The semi-hermetic reciprocating compressors segment is projected to witness the fastest CAGR over the forecast period.

- Semi-hermetic compressors provide ease of servicing and higher power capacity, making them suitable for commercial and industrial applications.

- These compressors are widely used in modular heating systems where accessibility and periodic maintenance are crucial.

- Increasing need for medium-capacity heat pump systems in hotels, data centers, and institutional buildings is driving segment trends.

- Reciprocating heat pump compressors market growth in this category is supported by the shift toward heat recovery-based systems and upgraded energy compliance standards.

By Lubrication:

Based on lubrication, the market is segmented into oil-filled and oil-free.

Oil-filled compressors held the largest reciprocating heat pump compressors market share in 2024.

- Oil-lubricated compressors are widely adopted for their high durability and capacity to handle elevated loads in heating operations.

- These units offer longer service life in high-duty cycles, especially in cold-climate industrial process heating.

- The availability of synthetic lubricants compatible with low-GWP refrigerants supports their sustainability appeal.

- As per the reciprocating heat pump compressors market analysis, the segment benefits from consistent demand in multi-unit heating applications.

The oil-free compressors segment is anticipated to grow at the highest CAGR during the forecast period.

- Oil-free technology is gaining traction in environmentally sensitive applications such as hospitals, food processing, and pharmaceutical industries.

- These systems reduce contamination risks and simplify system maintenance by eliminating oil change intervals.

- Reciprocating heat pump compressors market trends indicate rising adoption of Teflon-coated piston compressors in oil-free categories for critical clean-room installations.

- Increasing regulatory focus on sustainable HVAC systems with low operational emissions is propelling oil-free compressor requirement.

By Application:

Based on application, the market is segmented into space heating, water heating, industrial process heating, and district heating & cooling.

The space heating segment dominated the market in terms of revenue in 2024.

- Space heating applications benefit from the versatility of reciprocating compressors across residential, commercial, and institutional buildings.

- Government-led renovation programs to retrofit conventional boilers with heat pump systems are driving space heating system installations.

- Rapid urbanization and a shift toward low-emission heating solutions are contributing to space heating needs in colder geographies.

- Reciprocating heat pump compressors market trends indicate continued growth in hybrid heating applications integrating solar thermal and geothermal sources.

The industrial process heating segment is expected to grow at the fastest CAGR.

- Industrial operations require precise and consistent heat control, for which reciprocating compressors provide efficient cycling and load handling.

- High-temperature heat pump systems utilizing CO₂ or ammonia as working fluids are increasingly adopted in drying, washing, and pasteurization lines.

- The segment benefits from decarbonization efforts and energy recovery mandates in sectors such as pulp & paper, food processing, and chemicals.

- For instance, in July 2024, GEA Systems North America supplied a GEA RedGenium heat pump to a Canada-based, global dairy processor and distributor of cheeses, dairy products and grocery items. It has a heating capacity between 650 kW to 3230 kW, based on evaporative conditions.

- The reciprocating heat pump compressors market demand is expanding due to retrofit programs in Europe and North America promoting heat electrification in industrial processes.

By End-Use:

Based on end-use, the market is segmented into residential, commercial, industrial, and institutional.

The commercial segment accounted for the largest reciprocating heat pump compressors market share in 2024.

- Commercial buildings, including office spaces, retail outlets, and hospitality venues, require scalable and efficient heating systems, favoring reciprocating compressors.

- HVAC upgrades in aging building infrastructure across developed markets have accelerated the adoption of modern heat pumps.

- Increased awareness around energy certifications like LEED and BREEAM is driving commercial entities toward high-efficiency heating solutions.

- Reciprocating heat pump compressors market demand in this segment is sustained by the push for electrified heating to meet net-zero targets.

The institutional segment is expected to register the fastest CAGR.

- Institutions such as hospitals, schools, and government buildings require reliable and clean heating, with reciprocating compressors offering modular scalability.

- Programs promoting decarbonization in public sector buildings are fueling investments in renewable-based heat pump infrastructure.

- The resilience and serviceability of reciprocating compressors make them ideal for mission-critical applications in institutional settings.

- Reciprocating heat pump compressors market expansion in this segment is also driven by public-private collaborations aimed at improving energy performance and carbon savings.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

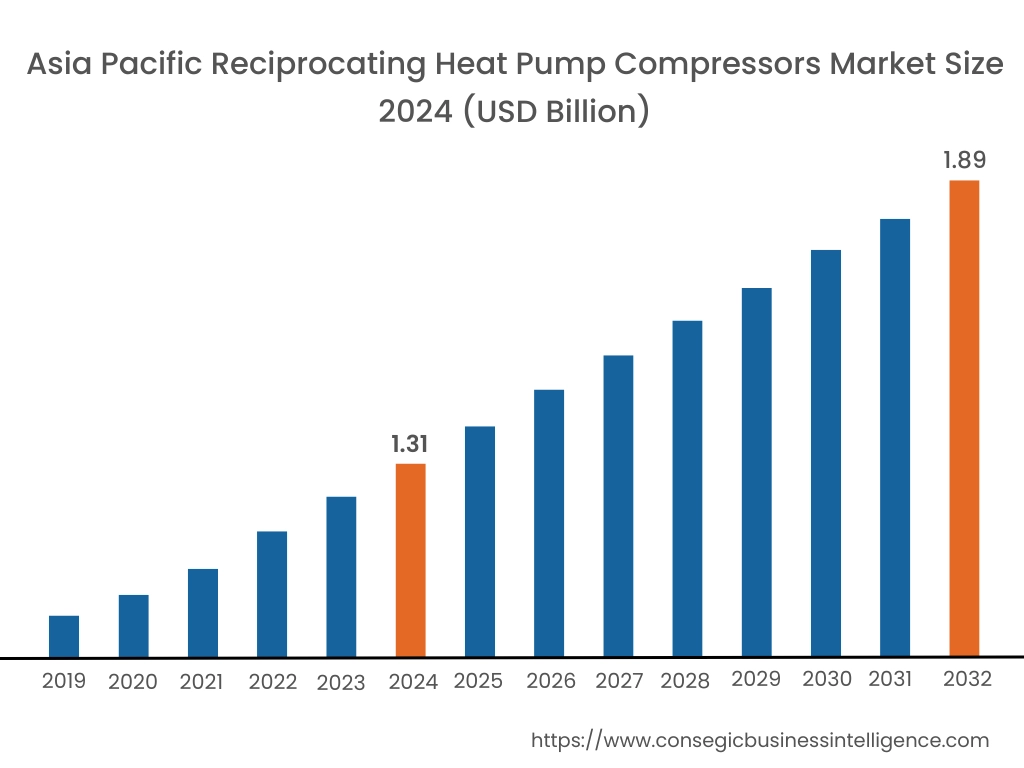

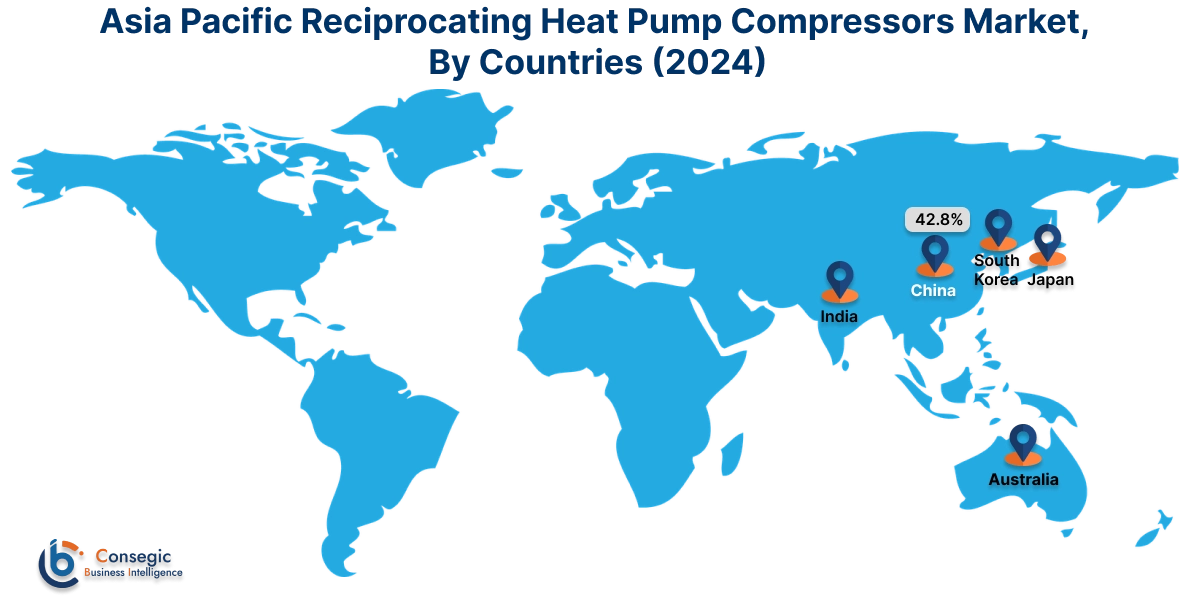

Asia Pacific region was valued at USD 1.31 Billion in 2024. Moreover, it is projected to grow by USD 1.35 Billion in 2025 and reach over USD 1.89 Billion by 2032. Out of this, China accounted for the maximum revenue share of 42.8%. This region is witnessing rapid growth in the reciprocating heat pump compressors industry due to increasing residential buildings, industrial energy retrofits, and climate change adaptation. China, Japan, South Korea, and India are demonstrating considerable uptake in residential and commercial spaces. Research identifies increasing application in hybrid heating-cooling systems and hot water production, particularly within high-density city dwellings. Local producers are ramping up production of efficient compressors to supply regional demand, while governments are encouraging low-emission heating options to minimize the use of fossil fuels. With growing consumer consciousness of climate-resilient technology, the potential for faster market penetration increases.

North America is estimated to reach over USD 2.01 Billion by 2032 from a value of USD 1.48 Billion in 2024 and is projected to grow by USD 1.51 Billion in 2025. North America dominates the market owing to mounting focus on residential space heating energy efficiency and retrofitting of HVAC systems in the colder parts of the world. Suburban and rural homes employing air-source and ground-source heat pumps in the United States and Canada are indicating stable requirements. According to analysis, the shift toward home heating electrification with support from tax credits and policy regulations is doubling up on reciprocating compressor demand in mini-systems. The use of variable-speed drives and noise-reduction technology is also supporting broader adoption in new construction developments and replacement scenarios.

Europe is a leader in the adoption of low-emission heating equipment, which makes it an advanced and mature region for reciprocating compressor applications. Germany, France, and the Netherlands have adopted strong climate policies that encourage the replacement of oil- and gas-fired systems with heat pumps. Regional analysis shows that demand is especially strong in multi-family homes and aging buildings with energy retrofits. The transition to natural refrigerants and stringent performance requirements is also fueling innovation in compressor technologies. Furthermore, broad government backing for decarbonizing buildings also supports long-term market stability.

Latin America is experiencing incremental adoption, driven by climate variability and urban energy reform in nations such as Brazil, Chile, and Mexico. While conventional air conditioning is the norm, reciprocating compressors are making inroads in combined heating and cooling systems appropriate to highland and temperate regions. Regional trends indicate that government energy efficiency programs and increased residential construction are driving segment growth. Nonetheless, issues of limited funding and the necessity for trained technical assistance could affect wider adoption unless countered by focused infrastructure initiatives.

The Middle East and Africa region is an emerging market wherein off-grid energy solutions, infrastructure growth, and institutionalization are driving adoption. Although cooling systems are predominant in most areas of the region, heating systems is slowly gaining traction in northern and high-altitude regions of countries such as Turkey, Iran, and South Africa. Analysis indicates that the growing popularity of modular construction, along with growing fuel costs and interest in alternative energy, is opening up niche applications for heat pump compressors. The reciprocating heat pump compressors market opportunity here is linked to energy diversification policies and foreign partnerships designed to extend access to sustainable HVAC.

Top Key Players & Market Share Insights:

The reciprocating heat pump compressors market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global reciprocating heat pump compressors market. Key players in the reciprocating heat pump compressors industry include –

- GEA Group (Germany)

- Sabroe (a brand of Johnson Controls) (Denmark)

- Mayekawa (MYCOM) (Japan)

- Bitzer SE (Germany)

- Fluid Aire Dynamics (USA)

- Kulthorn Kirby (Thailand)

- Siemens Energy (Germany)

- Carlyle Compressor (a brand of Carrier) (USA)

- M&M Carnot (USA)

- KAESER COMPRESSORS (Germany)

Recent Industry Developments :

Product Launches:

- In March 2024, Tecumseh launched an enhanced product portfolio to comply with lower GWP standards. This decision aligns with the Kigali Amendment, which outlines the gradual reduction in the use of HFCs globally. Tecumseh introduced two new standout rotary compressor offerings, the RG and HG compressors, compatible with R-454B.

Acquisitions:

- In March 2023, Danfoss completed the acquisition of German compressor manufacturer BOCK GmbH. This move aligns with Danfoss’ position as a preferred provider of greener cooling and heating solutions. BOCK’s team of 400 experts and specialists have become a part of the Danfoss Company.

Reciprocating Heat Pump Compressors Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6.21 Billion |

| CAGR (2025-2032) | 4.3% |

| By Compressor Type |

|

| By Lubrication |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Reciprocating Heat Pump Compressors Market? +

Reciprocating Heat Pump Compressors Market size is estimated to reach over USD 6.21 Billion by 2032 from a value of USD 4.45 Billion in 2024 and is projected to grow by USD 4.56 Billion in 2025, growing at a CAGR of 4.3% from 2025 to 2032.

What specific segmentation details are covered in the Reciprocating Heat Pump Compressors Market report? +

The Reciprocating Heat Pump Compressors market report includes specific segmentation details for compressor type, lubrication, application and end-use.

What are the end-uses of Reciprocating Heat Pump Compressors? +

The end-uses of Reciprocating Heat Pump Compressors are residential, commercial, industrial and institutional (hospitals, educational facilities, government buildings).

Who are the major players in the Reciprocating Heat Pump Compressors Market? +

The key participants in the Reciprocating Heat Pump Compressors market are GEA Group (Germany), Sabroe (a brand of Johnson Controls) (Denmark), Mayekawa (MYCOM) (Japan), Bitzer SE (Germany), Kulthorn Kirby (Thailand), Siemens Energy (Germany), Carlyle Compressor (a brand of Carrier) (USA), M&M Carnot (USA), KAESER COMPRESSORS (Germany) and Fluid Aire Dynamics (USA).