- Summary

- Table Of Content

- Methodology

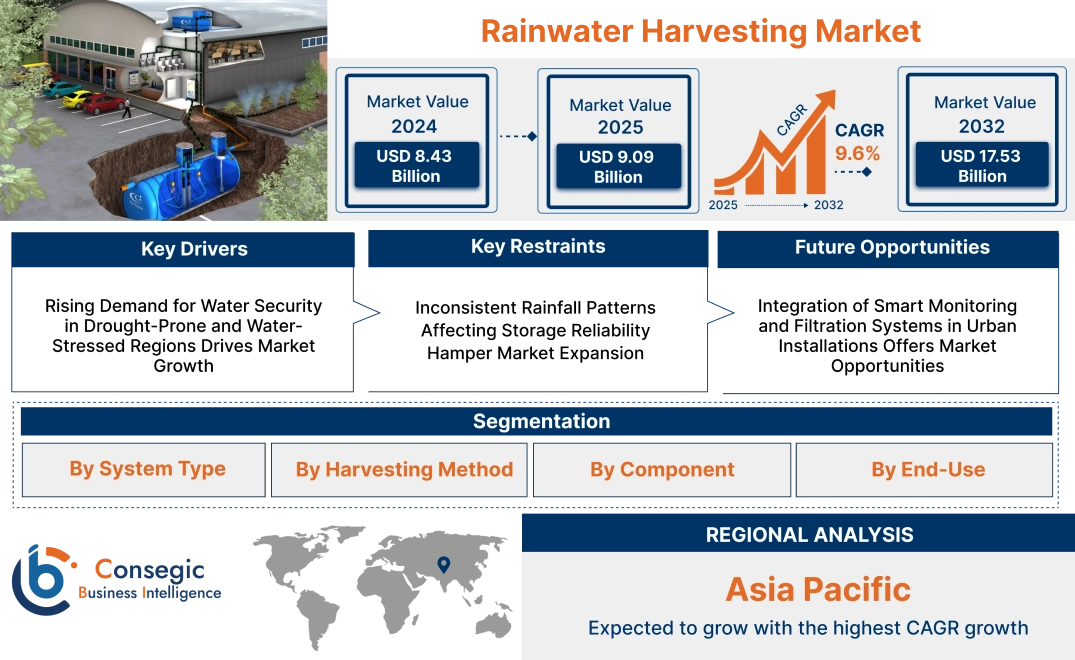

Rainwater Harvesting Market Size:

Rainwater Harvesting Market size is estimated to reach over USD 17.53 Billion by 2032 from a value of USD 8.43 Billion in 2024 and is projected to grow by USD 9.09 Billion in 2025, growing at a CAGR of 9.6% from 2025 to 2032.

Rainwater Harvesting Market Scope & Overview:

Rainwater harvesting is the collection and storage of rainwater from roofs, land surfaces, or other catchment surfaces for subsequent use in residential, commercial, agricultural, and industrial purposes. These systems are designed to collect runoff, screen debris, and convey water into storage tanks or underground reservoirs.

Core elements are catchment surfaces, conveyance systems, filtration units, storage tanks, and distribution lines. Designs can be as straightforward as barrel systems or more sophisticated systems with automated controls, UV disinfection, and real-time monitoring.

It provides advantages of decreased reliance on centralized water sources, lower utility bills, and enhanced groundwater recharging. The system is applicable for irrigation, flushing, washing, and small potable purposes when treated properly. It is expandable, flexible to both urban and rural environments, and helps in sustainable water management strategies. Through the use of underutilized rainfall resources, it offers a cost-effective, environmentally friendly method of augmenting traditional water supply systems.

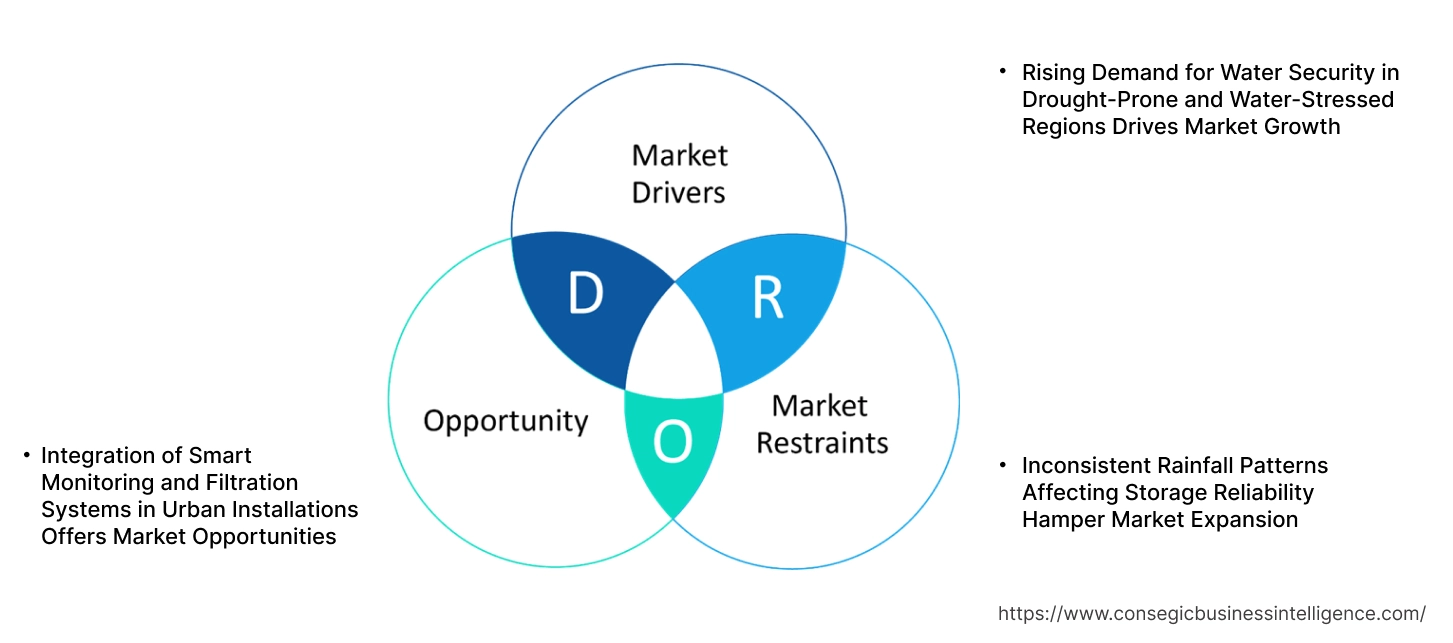

Rainwater Harvesting Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Water Security in Drought-Prone and Water-Stressed Regions Drives Market Growth

Water scarcity is mounting across regions that are facing depleting aquifers, recurring droughts, and congested municipal systems. Neighborhoods in portions of California, Western Australia, Northern India, and Sub-Saharan Africa are experiencing frequent watering restrictions and mounting dependence on non-traditional sources. As a response, residential, agricultural, and institutional consumers are implementing rainwater harvesting systems to collect and store rainwater for household use, irrigation, and landscaping. The systems offer a decentralized, affordable buffer during water cuts and dry periods. As the pressure mounts on conventional infrastructure and the call for resilient water strategies, stakeholders are giving priority to rooftop collection systems, storage tanks, and surface runoff reservoirs.

- For instance, in March 2024, Marico Limited, one of India’s leading FMCG brands, achieved the ‘Water Neutral’ certification from DNV Business Assurance India at their Jalgaon facility. This meant that their total water credited was greater than the debited, resulting in a positive water balance status. Furthermore, their freshwater intake was lower than the rainwater harvested for community use. This was possible due to the Water Stewardship Program- Jalashay, which created 12.4 crore litre rainwater conservation potential in the water-scarce region through comprehensive water conservation measures, including rainwater harvesting, infrastructure development and community engagement initiatives.

The increasing focus on site- and household-level water autonomy is driving adoption in both rural and urban areas, ultimately driving long-term rainwater harvesting market expansion.

Key Restraints:

Inconsistent Rainfall Patterns Affecting Storage Reliability Hamper Market Expansion

Rainfall unpredictability and changing climate patterns are eroding the reliability of rainwater harvesting system performance. In most regions, seasonal rainfall is becoming more unpredictable, with delayed monsoons, short-duration rainfall events, or extended dry periods impacting storage predictability. Historical rainfall-based design systems do not provide satisfactory water availability season-wise. Systems in arid and semi-arid regions with fewer rainfall events translate into empty tanks and poor system utilization, degrading the investment return. In regions where there is heavy but short-duration rainfall, the lack of adequate infrastructure to capture and store the water results in loss through runoff. These difficulties are diminishing users' and developers' confidence, especially in areas where investment in water infrastructure heavily relies on the reliability of systems. In spite of increasing demand for decentralized water solutions, erratic rainfall still holds back rainwater harvesting market growth.

Future Opportunities :

Integration of Smart Monitoring and Filtration Systems in Urban Installations Offers Market Opportunities

Urban planners and building owners are installing sophisticated rainwater collection systems with smart sensors, real-time monitoring, and computer-controlled flow filtration units. Such attributes enable users to monitor water levels, rates, and tank capacity remotely, enabling timely maintenance and maximum usage. Filtered water quality is enhanced through automated filters and UV purification units for non-potable end uses like flushing toilets, irrigating landscapes, and cooling towers. As urban infrastructure shifts towards green certification compliance and digital transformation, the demand for IoT-enabled water systems is rising. Rainfall forecast-responsive smart controllers and adjust capture settings help improve system efficiency and minimize overflow loss. Technology convergence with water management is emerging in high-density housing, institutional campuses, and commercial buildings.

- For instance, in September 2023, Pipelife launched smart rainwater harvesting solution for homeowners. This included a complete stormwater management solution that covers the roof and drains and also offers a smart monitoring and control system. It allows for the local storage and reuse of rainwater for irrigation, flushing toilets, or even washing laundry.

The increasing demand for sustainable, networked infrastructure is developing solid rainwater harvesting market opportunities fueled by digital connectivity and long-term operational expansion.

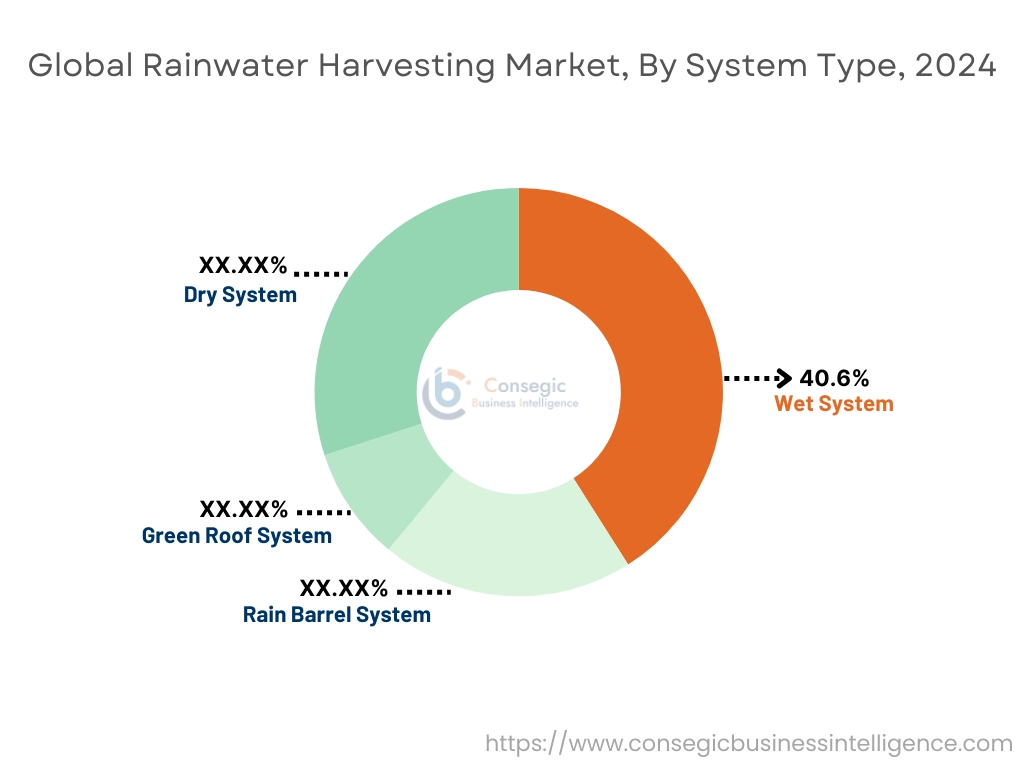

Rainwater Harvesting Market Segmental Analysis :

By System Type:

Based on system type, the market is segmented into dry system, wet system, rain barrel system, and green roof system.

The wet system segment accounted for the largest rainwater harvesting market share of 40.6% in 2024.

- Wet rainwater harvesting systems feature underground or concealed pipes that maintain a continuous water path from the roof catchment to the storage tank, even when the tank is located at a distance.

- These systems are ideal for larger residential, commercial, and institutional properties with aesthetic constraints and space limitations near the collection point.

- The enclosed piping setup prevents exposure to debris and contaminants, improving water quality when combined with first flush diverters and filtration units.

- As per rainwater harvesting market analysis, the wet system segment dominates due to its widespread adoption in large-scale and permanent installations across urban landscapes.

The green roof system segment is projected to witness the fastest CAGR during the forecast period.

- Green roof systems integrate vegetation with rainwater retention layers, enhancing stormwater management and building insulation.

- These systems are favored in urban settings for their dual benefits of reducing runoff and mitigating urban heat islands.

- As cities adopt climate-resilient infrastructure, the implementation of green roofs is gaining policy support and funding.

- According to rainwater harvesting market trends, green roofs are key to sustainable architecture, driving innovation and segment growth.

By Harvesting Method:

Based on harvesting method, the rainwater harvesting industry is divided into above-ground and underground systems.

The above-ground segment accounted for the largest market share in 2024.

- Above ground systems are easy to install and maintain, making them suitable for small-scale and residential applications.

- Storage tanks are often made of plastic or fiberglass and are used for garden irrigation, toilet flushing, and greywater reuse.

- These systems require minimal excavation, reducing upfront installation costs significantly.

- As per rainwater harvesting market trends, increasing water conservation awareness among homeowners supports steady above-ground adoption.

The underground segment is expected to grow at the fastest CAGR during the forecast period.

- Underground systems offer better protection against temperature extremes and UV degradation, extending tank lifespan.

- These systems are preferred in commercial and institutional setups where space-saving and large-volume storage are essential.

- Their concealed installation allows for dual land use, especially in parking lots and recreational areas.

- Rainwater harvesting market expansion in dense urban areas is driven by the adoption of underground systems with automated pumping solutions.

By Component:

Based on component, the market is segmented into conveyance systems, storage tanks, filtration systems, pumps, first flush devices, and others.

The storage tanks segment held the largest rainwater harvesting market share in 2024.

- Storage tanks are central to every rainwater harvesting system, determining capacity, quality, and accessibility.

- Tanks are available in varied sizes and materials (plastic, steel, concrete), tailored to specific site needs and collection volumes.

- Demand for modular and collapsible tank designs is increasing in mobile and temporary setups.

- As per rainwater harvesting market analysis, innovations in tank materials and manufacturing processes enhance durability and efficiency.

The filtration systems segment is projected to grow rapidly during the forecast period.

- Filtration is critical for removing debris, sediment, and contaminants before storage or reuse, especially in potable applications.

- Advanced filters including UV, carbon, and membrane technologies are being adopted in urban and industrial systems.

- Increasing regulatory standards around water reuse quality are driving investments in multi-stage filtration solutions.

- Rainwater harvesting market growth is supported by rising health and safety awareness in water recycling initiatives.

By End Use:

Based on end-use, the rainwater harvesting market is segmented into residential, commercial, industrial, agricultural, and institutional.

The residential segment accounted for the largest revenue share in 2024.

- Homeowners are adopting these systems to reduce utility costs, ensure water security, and support sustainable living.

- Municipal subsidies and tax incentives encourage residential system installations across water-stressed regions.

- Most installations support landscape irrigation, toilet flushing, and emergency water supply.

- Rainwater harvesting market demand from the residential sector remains consistent due to affordability and regulatory encouragement.

The commercial segment is expected to register the fastest CAGR during the forecast period.

- Commercial facilities such as malls, office complexes, and hotels implement harvesting systems to meet ESG goals and reduce operational costs.

- High-volume rooftop collection, paired with underground tanks and automated controls, improves water use efficiency.

- Building codes and green certifications increasingly require rainwater management solutions.

- The commercial sector plays a pivotal role in scaling sustainable water practices and is expected to grow the rainwater harvesting market demand.

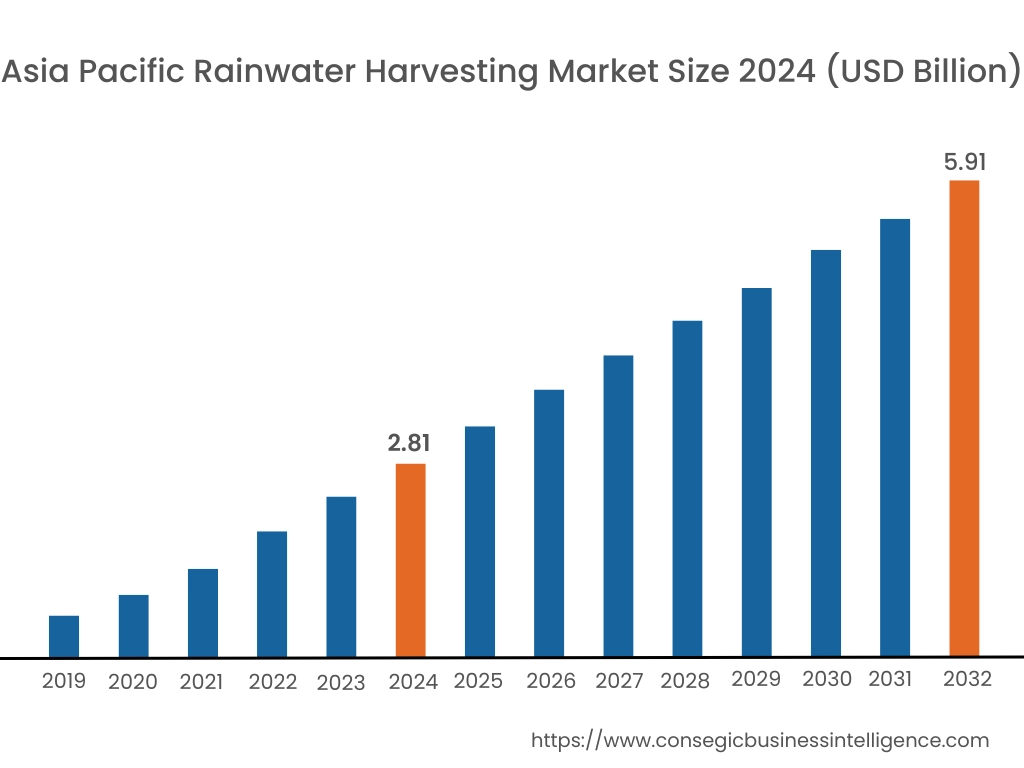

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

Asia Pacific region was valued at USD 2.81 Billion in 2024. Moreover, it is projected to grow by USD 3.03 Billion in 2025 and reach over USD 5.91 Billion by 2032. Out of this, China accounted for the maximum revenue share of 34.8%. Asia-Pacific is undergoing rapid growth, supported by high population density, uneven rainfall patterns, and overexploited groundwater resources. India, China, and Australia are at the forefront of initiatives with governments mandating rainwater recharge requirements for new developments and rural programs. Market analysis points to extensive use in agricultural irrigation, school sanitation systems, and urban water conservation measures. Japan and South Korea are investing in smart rainwater collection systems combined with building automation and flood control infrastructure. In Southeast Asia, the market is growing through community-based rainwater harvesting initiatives in regions without a centralized water supply. The region's fast urban growth and climate resilience planning continue to drive future market potential.

North America is estimated to reach over USD 5.17 Billion by 2032 from a value of USD 2.48 Billion in 2024 and is projected to grow by USD 2.67 Billion in 2025. In North America, the market is increasingly becoming pertinent as cities in the western and southern United States experience periodic droughts and water table depletion. California, Texas, and Arizona states are embracing rain capture regulations and providing incentives to encourage decentralized water storage for both residential and commercial applications. Market research indicates rising incorporation of such systems into green building designs and LEED-registered projects. Canada, however, focuses on rainwater harvesting for non-drinking purposes within rural and sensitive environmental zones. Development in the area is principally encouraged by the municipal sector, increased water fees, and shifting priorities towards drought-resistant landscaping within areas of low precipitation.

Europe is a highly regulated and innovation-minded area, with rainwater catchment systems regularly being incorporated within green building codes and stormwater management policies. Germany, the United Kingdom, and the Netherlands are among the leading countries in terms of adoption, with the systems being popularly installed in urban renewal areas and green infrastructure projects. Analysis in the market indicates a mature supply ecosystem with technical standards that aim at minimizing surface runoff, enhancing flood resilience, and reducing the amount of potable water used in homes and public buildings. Europe's market opportunity is to scale up adoption by retrofitting existing older infrastructure and growing usage in industrial processes that aim to be resource-efficient.

Latin America is experiencing growing adoption, especially in nations such as Brazil, Mexico, and Colombia, where rural water access issues and rainfall variability during seasons make sound justification for localized water storage systems. Market research reveals residential and agricultural sectors as significant users, with rooftop catchment systems becoming increasingly common in peri-urban and drought-prone communities. In Brazil, rainwater harvesting is also being encouraged through sustainability-linked building incentives. The rainwater harvesting market opportunity here is inextricably linked with government incentives for water sustainability, NGO-initiated pilot schemes, and increasing awareness among municipal planners about climate adaptation measures.

The Middle East and Africa are new markets where water scarcity and harsh climatic conditions render rainwater harvesting a strategic imperative. In the Middle East, nations like the UAE and Saudi Arabia are combining rooftop and subsurface cistern systems in smart cities and water-neutral developments. Market research indicates that it is gaining popularity in commercial buildings and agricultural greenhouses where the water supply is irregular. In Africa, countries such as Kenya, Ethiopia, and South Africa are making decentralized rainwater systems in schools, clinics, and farms a priority through donor-funded infrastructure programs. With low access to centralized water utilities in most areas, expansion in this region is based on affordability, modular system design, and policy-driven adoption.

Top Key Players and Market Share Insights:

The rainwater harvesting market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global rainwater harvesting market. Key players in the rainwater harvesting industry include -

- Kingspan Group plc (Ireland)

- Watts Water Technologies, Inc. (USA)

- Ecozi Ltd (United Kingdom)

- Water Field Technologies Pvt. Ltd. (India)

- Heritage Water Tanks (Australia)

- Graf Group GmbH (Germany)

- WISY AG (Germany)

- Innovative Water Solutions LLC (USA)

- D&D Ecotech Services (India)

- Stormsaver Ltd (United Kingdom)

Recent Industry Developments :

Product Launches:

- In February 2023, Stormsaver launched two new residential rainwater harvesting systems designed for housing developers.

Acquisitions:

- In February 2025, Apollo Pipes acquired an additional 0.5% stake in Kisan Mouldings, following their acquisition of 53.57% share capital in March 2024.

Rainwater Harvesting Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 17.53 Billion |

| CAGR (2025-2032) | 9.6% |

| By System Type |

|

| By Harvesting Method |

|

| By Component |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Rainwater Harvesting Market? +

Rainwater Harvesting Market size is estimated to reach over USD 17.53 Billion by 2032 from a value of USD 8.43 Billion in 2024 and is projected to grow by USD 9.09 Billion in 2025, growing at a CAGR of 9.6% from 2025 to 2032.

What specific segmentation details are covered in the Rainwater Harvesting Market report? +

The Rainwater Harvesting market report includes specific segmentation details for system type, harvesting method, component and end-use.

What are the end-use of the Rainwater Harvesting Market? +

The end-use of the Rainwater Harvesting Market is residential, commercial, industrial, agricultural, and institutional.

Who are the major players in the Rainwater Harvesting Market? +

The key participants in the Rainwater Harvesting market are Kingspan Group plc (Ireland), Watts Water Technologies, Inc. (USA), Graf Group GmbH (Germany), WISY AG (Germany), Innovative Water Solutions LLC (USA), D&D Ecotech Services (India), Stormsaver Ltd (United Kingdom), Ecozi Ltd (United Kingdom), Water Field Technologies Pvt. Ltd. (India) and Heritage Water Tanks (Australia).