- Summary

- Table Of Content

- Methodology

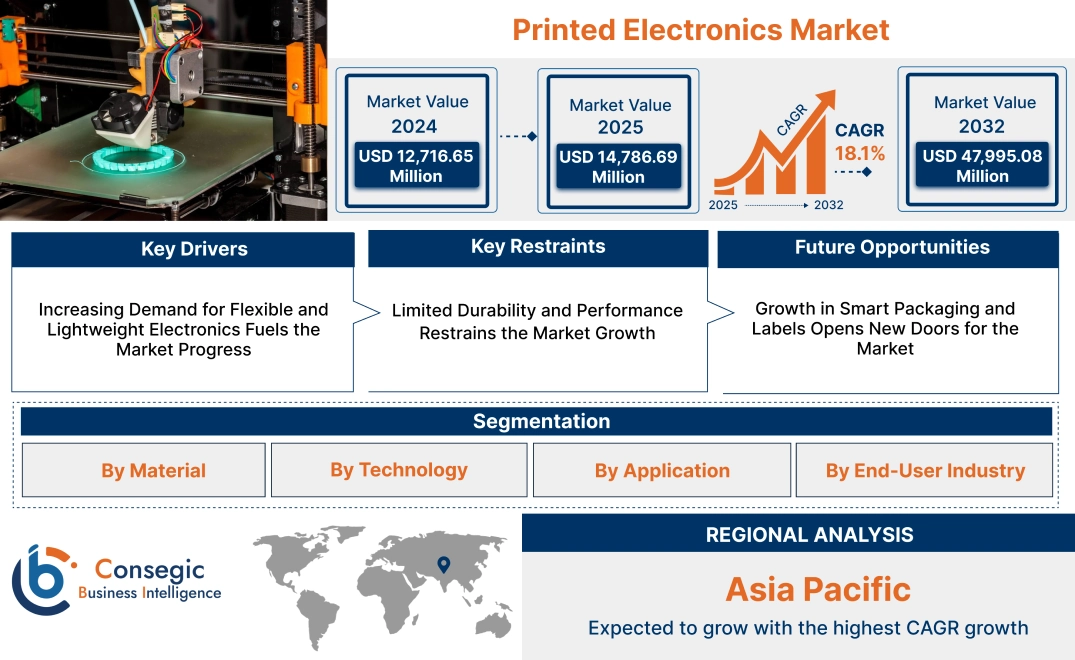

Printed Electronics Market Size:

Printed Electronics Market size is estimated to reach over USD 47,995.08 Million by 2032 from a value of USD 12,716.65 Million in 2024 and is projected to grow by USD 14,786.69 Million in 2025, growing at a CAGR of 18.1% from 2025 to 2032.

Printed Electronics Market Scope & Overview:

Printed electronics refer to a manufacturing process where electronic devices are created using printing techniques to deposit conductive materials onto substrates such as paper, plastic, or glass. This technology enables the production of lightweight, flexible, and cost-effective electronic components, making it suitable for applications in industries such as consumer electronics, healthcare, automotive, and packaging.

These electronics include components like sensors, antennas, displays, and photovoltaic cells, which are fabricated using methods such as screen printing, inkjet printing, and gravure printing. These electronics are designed for high scalability and adaptability, allowing seamless integration into various products. They support innovative designs, such as flexible displays, wearable devices, and smart labels, enhancing their usability across multiple sectors.

The end-users include manufacturers of smart devices, medical equipment, and automotive components, where compact, efficient, and flexible electronic solutions are critical. These electronics play a pivotal role in advancing next-generation devices and enabling cost-effective production of innovative technologies.

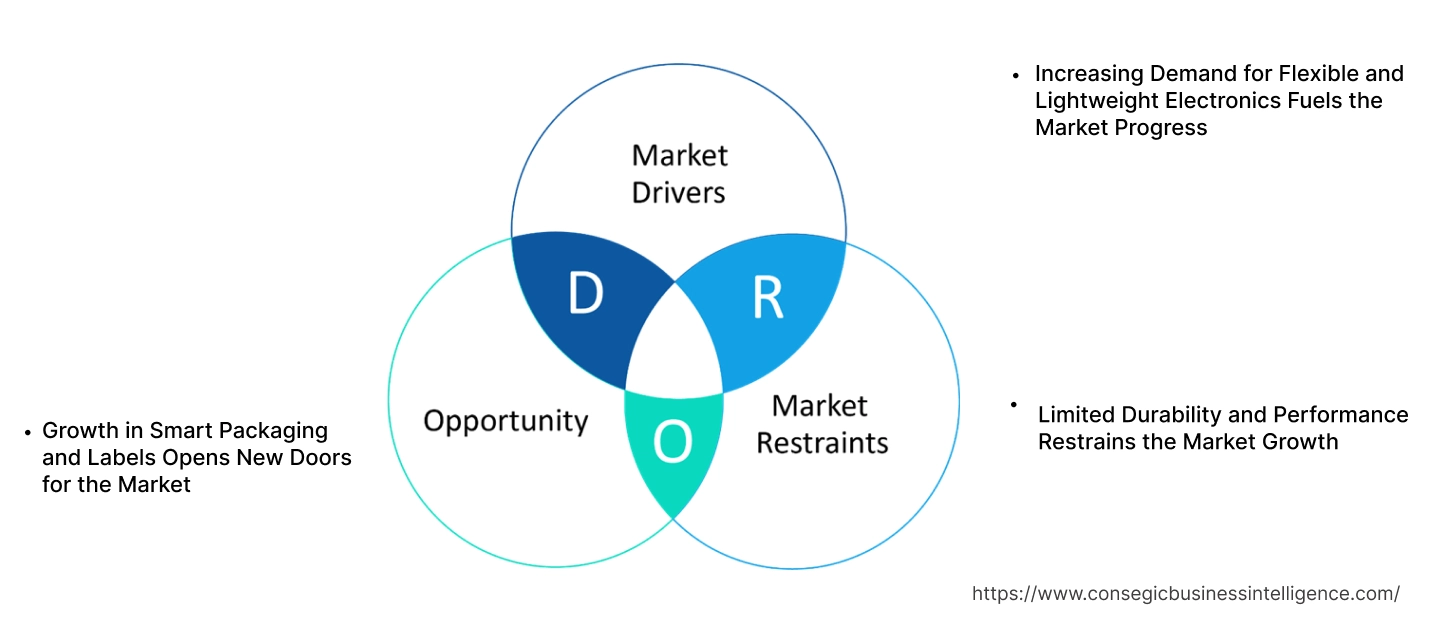

Printed Electronics Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Flexible and Lightweight Electronics Fuels the Market Progress

The increasing demand for lightweight, flexible, and wearable electronics is driving the printed electronics market growth. As consumer preferences shift towards more portable and adaptable devices, printed electronics, which utilize printed technologies on flexible substrates, offer a solution that meet these requirements. These components are perfect for applications such as smart clothing, flexible displays, and wearable sensors. In the consumer electronics sector, these electronics enable the development of slim, flexible devices that are more comfortable and convenient for everyday use. In healthcare, these technologies power innovative medical wearables and sensors for continuous monitoring. Additionally, the fashion sector is exploring the potential of integrating these electronics into clothing for dynamic features like embedded lighting or monitoring systems. This trend towards lightweight and flexible electronics is boosting the adoption of these electronics across various industries, primarily driven by their ability to combine functionality with convenience and design flexibility.

Key Restraints:

Limited Durability and Performance Restrains the Market Growth

A key restraint for printed electronics is their relatively lower durability and performance compared to traditional semiconductor-based components. These devices often struggle with limitations in electrical conductivity, thermal management, and lifespan. The materials used in these electronics, such as conductive inks and flexible substrates, typically offer lower conductivity and heat dissipation than conventional metals and semiconductors, impacting their ability to perform efficiently in high-power or high-temperature environments. As a result, they are not suitable for applications that require long-term reliability and high performance, such as in advanced computing, automotive, or industrial systems. Additionally, they suffer from shorter lifespans, especially when exposed to harsh conditions like humidity, vibration, or prolonged use. These performance and durability constraints limit the printed electronics market demand, hindering their ability to replace traditional components in demanding, high-performance sectors.

Future Opportunities :

Growth in Smart Packaging and Labels Opens New Doors for the Market

By integrating sensors and NFC (Near Field Communication) tags into packaging, printed electronics enable real-time monitoring of product conditions such as temperature, humidity, and exposure to light. This technology enhances product traceability, allowing brands to track product authenticity and ensure quality during transportation and storage. For consumers, NFC-enabled labels provide easy access to digital information, such as product details, usage instructions, and promotional content, enhancing the customer experience and engagement. In industries like retail, logistics, and pharmaceuticals, these capabilities offer improved inventory management, anti-counterfeiting measures, and compliance with regulatory requirements. The ability to incorporate cost-effective, flexible, and functional electronics directly into packaging materials makes them an attractive solution for businesses looking to innovate in packaging, improve operational efficiency, and enhance brand interaction with consumers. Thus, the aforementioned factors create significant printed electronics market opportunities.

Printed Electronics Market Segmental Analysis :

By Material:

Based on material, the market is segmented into inks, substrates, conductive polymers, organic materials, and others.

The inks segment accounted for the largest revenue of the total printed electronics market share in 2024.

- Inks are essential in printed electronics due to their conductivity and compatibility with various printing technologies, enabling the production of high-performance displays, sensors, and RFID antennas.

- Conductive inks, including silver, carbon-based, and nanoparticle inks, are extensively used for creating intricate electronic circuits in a range of applications.

- Industries such as automotive, consumer electronics, and healthcare rely on advanced ink formulations for efficient and reliable printed electronic components.

- As per printed electronics market analysis, continuous innovations in ink technologies, including hybrid formulations, support enhanced performance and broaden the application scope of printed inks in advanced manufacturing.

The substrates segment is projected to grow at the fastest CAGR during the forecast period.

- Substrates, including flexible plastics, glass, and paper, are key materials in manufacturing lightweight and durable printed electronic components.

- Flexible substrates are widely adopted in wearable devices and foldable displays, aligning with trends toward miniaturization and portable electronics.

- The development of eco-friendly and biodegradable substrates is attracting industries prioritizing sustainability in electronic manufacturing.

- As per printed electronics market trends, rising demand for durable and cost-efficient substrates is driving innovations in material compositions, contributing to segment expansion.

By Technology:

Based on technology, the market is segmented into screen printing, inkjet printing, gravure printing, flexographic printing, and others.

The screen printing segment accounted for the largest revenue of the total printed electronics market share in 2024.

- Screen printing is highly valued for its ability to handle large-volume production of sensors, lighting components, and displays with superior precision and scalability.

- Industries such as automotive and aerospace depend on screen printing to produce robust and reliable components that meet stringent quality standards.

- The capability of screen printing to deposit thick ink layers ensures high conductivity, supporting its dominance in applications like printed circuits and touch sensors.

- Continuous advancements in screen printing equipment and materials enhance its adaptability for high-performance applications, fueling the printed electronics market expansion.

The inkjet printing segment is anticipated to witness the fastest CAGR during the forecast period.

- Inkjet printing offers precise and customizable production, making it ideal for low-volume, high-complexity applications like wearable electronics and RFID tags.

- This technology supports material efficiency by depositing ink only where needed, minimizing wastage and improving cost-effectiveness.

- Advancements in inkjet printheads and conductive ink formulations expand its application in creating intricate and high-resolution electronic designs.

- As per market trends, the adoption of inkjet printing for personalized and flexible electronic devices is driving printed electronics market growth.

By Application:

Based on application, the market is segmented into displays, sensors, batteries, RFID antennas, lighting, and others.

The displays segment accounted for the largest revenue share in 2024.

- Printed electronics play a critical role in manufacturing OLED and LCD displays, offering lightweight, flexible, and cost-efficient solutions for consumer electronics and automotive applications.

- The use of printed displays in smartphones, televisions, and wearable devices drives their prominence in the market.

- The integration of flexible displays in foldable smartphones and smart home devices further enhances their requirement in advanced electronics.

- As per printed electronics market analysis, the growth in need for energy-efficient and high-performance display technologies supports the segment’s leadership.

The RFID antennas segment is expected to register the fastest CAGR during the forecast period.

- RFID antennas manufactured using printed electronics provide lightweight, durable, and cost-effective solutions for inventory tracking, asset management, and logistics.

- The rise of IoT applications and smart supply chain systems has significantly driven the adoption of printed RFID technologies across various industries.

- Innovations in conductive ink formulations improve the efficiency and performance of RFID antennas, expanding their application scope.

- As per printed electronics market trends, increasing investments in smart logistics and automated tracking solutions are propelling the growth of RFID antennas.

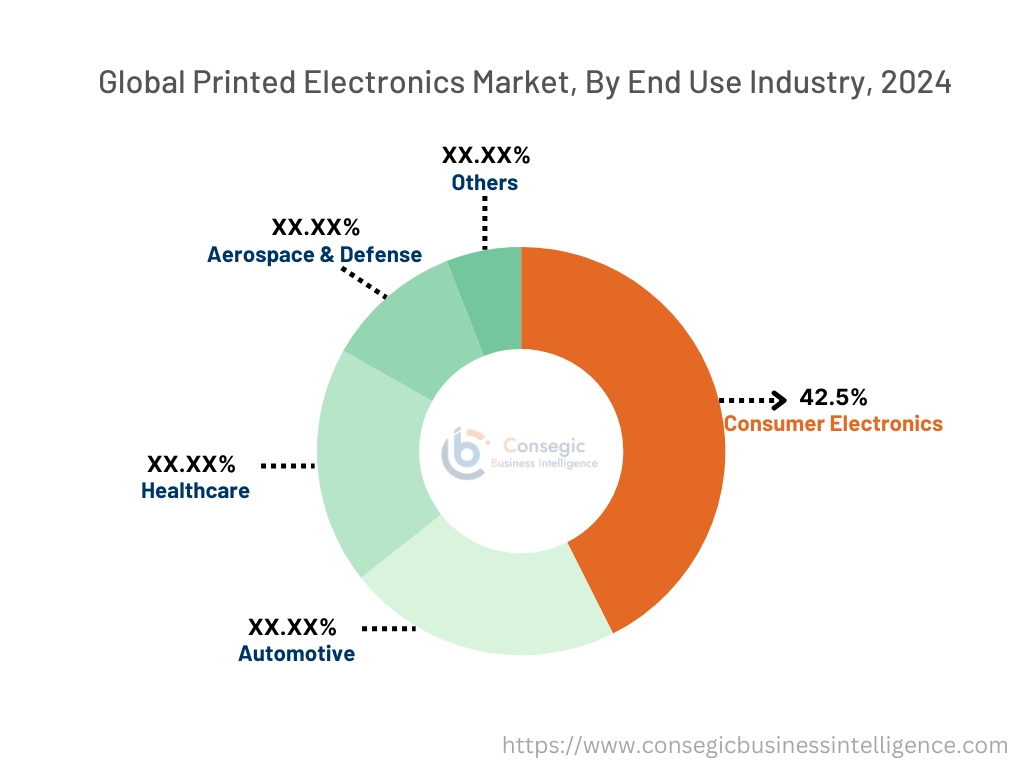

By End-User Industry:

Based on end-user industry, the market is segmented into consumer electronics, automotive, healthcare, and aerospace & defense, and others.

The consumer electronics segment accounted for the largest revenue of 42.5% share in 2024.

- Printed electronics are integral to manufacturing lightweight and compact components used in smartphones, tablets, and wearable devices.

- The demand for high-performance consumer electronics with advanced features drives significant investment in printed electronic technologies.

- Integration of printed sensors and flexible displays in smart home devices and personal gadgets boosts the segment’s leadership.

- Thus, the rising consumer need for innovative and energy-efficient electronic devices reinforces the prominence of this segment, driving the printed electronics market demand.

The automotive segment is projected to grow at the fastest CAGR during the forecast period.

- Printed electronics enable advanced features in vehicles, such as touch sensors, flexible displays, and OLED lighting, enhancing driver comfort and functionality.

- The transition to electric vehicles (EVs) has increased the use of printed components in battery systems, infotainment, and interior designs.

- Automotive manufacturers adopt these electronics for their cost-efficiency and lightweight nature, aligning with goals for improved fuel efficiency and performance.

- As per market trends, innovations in printed materials and production techniques drive the adoption of these electronics in automotive manufacturing.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

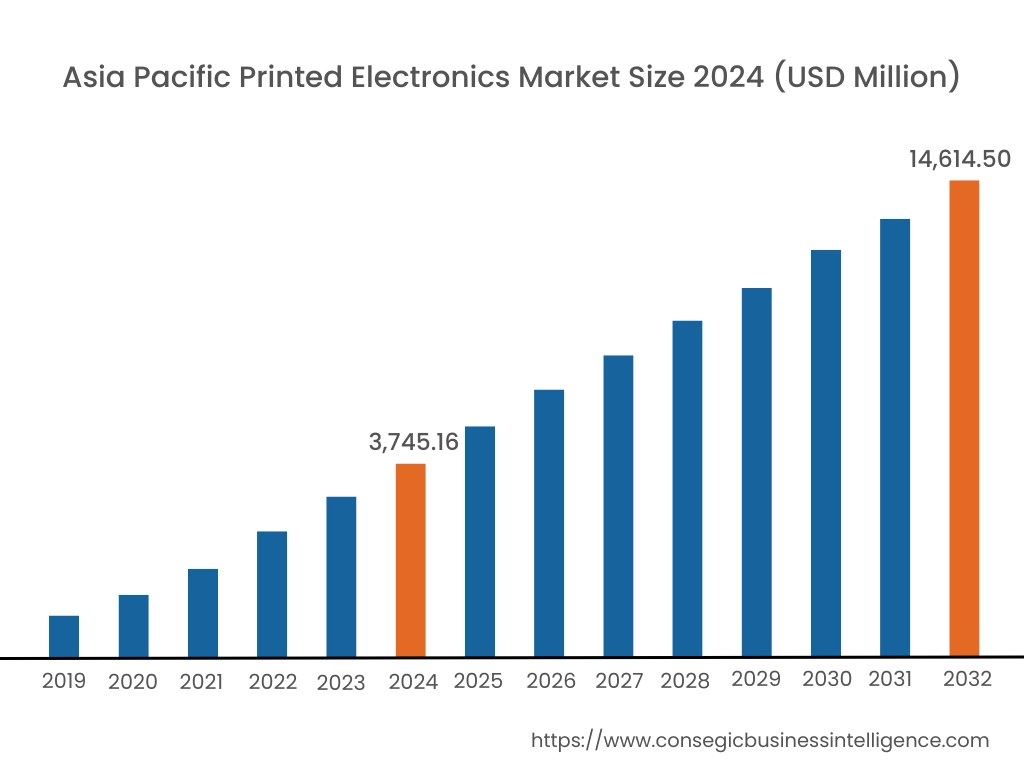

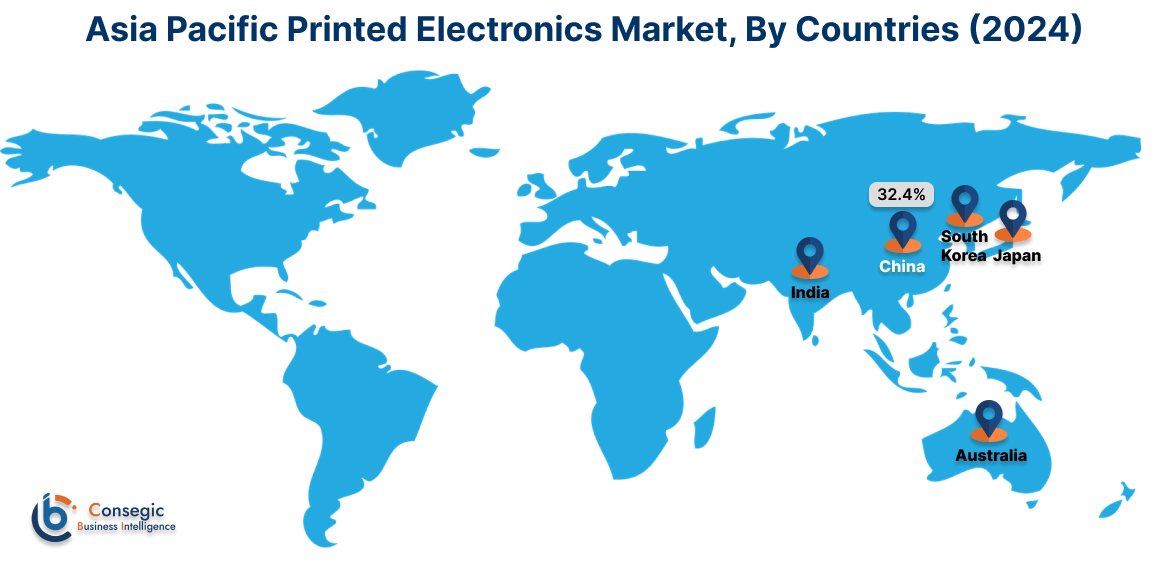

Asia Pacific region was valued at USD 3,745.16 Million in 2024. Moreover, it is projected to grow by USD 4,367.11 Million in 2025 and reach over USD 14,614.50 Million by 2032. Out of this, China accounted for the maximum revenue share of 32.4%. The Asia-Pacific region dominates the printed electronics market, attributed to rapid industrialization and a strong manufacturing base. A prominent trend is the substantial investments in these electronics segment for applications in consumer electronics, photovoltaics, and wearable devices. Analysis indicates that countries like China, Japan, and South Korea are leading in technological advancements and production capacities, supported by government initiatives promoting local electronics manufacturing, further fueling the printed electronics market expansion.

North America is estimated to reach over USD 15,555.21 Million by 2032 from a value of USD 4,218.22 Million in 2024 and is projected to grow by USD 4,895.49 Million in 2025. This region maintains a significant position in the printed electronics sector, driven by robust research and development activities and the presence of key industry players. A notable trend is the increasing adoption of these electronics in consumer electronics and healthcare applications, leveraging the flexibility and cost-effectiveness of printed components. Analysis indicates that collaborations between research institutions and industry stakeholders are fostering innovation, leading to the development of advanced materials and printing techniques, creating significant printed electronics market opportunities.

European countries are pivotal in the printed electronics market, emphasizing sustainability and the integration of advanced technologies. A significant trend is the focus on developing eco-friendly printing materials and processes, aligning with the region's stringent environmental regulations. Analysis suggests that the automotive sector in Europe is increasingly incorporating these electronics for applications such as flexible displays and sensors, enhancing vehicle functionality and user experience.

In the Middle East and Africa, the market is influenced by the adoption of advanced technologies to support infrastructure development and industrial diversification. The focus is on utilizing these electronics in energy-efficient solutions and smart building applications. Market analysis suggests that collaborations with international technology providers are facilitating the transfer of knowledge and expertise, aiding in the establishment of local manufacturing capabilities.

Latin American countries are increasingly recognizing the potential of printed electronics in sectors such as packaging, healthcare, and agriculture. A notable trend is the exploration of printed sensors for environmental monitoring and smart packaging solutions to enhance supply chain efficiency. Analysis indicates that regional partnerships and investments in research and development are crucial in overcoming challenges related to technological adoption and market penetration.

Top Key Players and Market Share Insights:

The Printed Electronics market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Printed Electronics market. Key players in the Printed Electronics industry include -

- Samsung Electronics Co., Ltd. (South Korea)

- LG Display Co., Ltd. (South Korea)

- BASF SE (Germany)

- NovaCentrix (USA)

- E Ink Holdings Inc. (Taiwan)

- Molex, LLC (USA)

- Agfa-Gevaert Group (Belgium)

- Palo Alto Research Center Incorporated (PARC) (USA)

- DuPont de Nemours, Inc. (USA)

- Nissha Co., Ltd. (Japan)

Recent Industry Developments :

Acquisitions & Mergers:

- In December 2024, Interlink Electronics acquired UK-based Conductive Transfers Limited (CT) and Global Print Solutions (GPS), strengthening its capabilities in printed electronics and smart textiles. The acquisition includes CT’s patented e-textile technologies used in healthcare, automotive, and apparel, such as wearable heaters and medical electrodes. Interlink plans to leverage CT’s Sheffield-based R&D facility to develop advanced sensors for pressure, temperature, and moisture detection, targeting high-growth markets in wearables and functional textiles.

Partnerships & Collaborations:

- In November 2024, Henkel, Covestro, and Quad Industries partnered to advance medical wearables using printed electronics. This collaboration integrates Henkel’s material expertise, Covestro’s polymer solutions, and Quad Industries’ printed electronics capabilities to enhance stretchable and flexible healthcare applications. The partnership aims to accelerate customer development and drive innovation in wearable medical devices, expanding the adoption of next-generation printed electronics in healthcare.

- In March 2024, Heraeus Printed Electronics and SUSS MicroTec signed a Joint Development Agreement to enable digital inkjet printing of metallic coatings for semiconductor mass production. The partnership integrates Heraeus’ Prexonics® inkjet technology and metallic inks with SUSS MicroTec’s automation and JETx platform, optimizing cost and efficiency. This collaboration aims to revolutionize semiconductor manufacturing by introducing scalable, high-precision digital printing solutions for EMI shielding, conductive structures, and heat dissipation.

Printed Electronics Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 47,995.08 Million |

| CAGR (2025-2032) | 18.1% |

| By Material |

|

| By Technology |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Printed Electronics Market? +

The Printed Electronics Market size is estimated to reach over USD 47,995.08 Million by 2032 from a value of USD 12,716.65 Million in 2024 and is projected to grow by USD 14,786.69 Million in 2025, growing at a CAGR of 18.1% from 2025 to 2032.

What are the key segments in the Printed Electronics Market? +

The market is segmented by material (inks, substrates, conductive polymers, organic materials, and others), technology (screen printing, inkjet printing, gravure printing, flexographic printing, and others), application (displays, sensors, batteries, RFID antennas, lighting, and others), and end-user industry (consumer electronics, automotive, healthcare, aerospace & defense, and others).

Which segment is expected to grow the fastest in the Printed Electronics Market? +

The RFID antennas segment is expected to register the fastest CAGR during the forecast period, driven by the rise of IoT applications and smart supply chain systems.

Who are the major players in the Printed Electronics Market? +

Key players in the Printed Electronics market include Samsung Electronics Co., Ltd. (South Korea), LG Display Co., Ltd. (South Korea), Molex, LLC (USA), Agfa-Gevaert Group (Belgium), Palo Alto Research Center Incorporated (PARC) (USA), DuPont de Nemours, Inc. (USA), Nissha Co., Ltd. (Japan), BASF SE (Germany), NovaCentrix (USA), E Ink Holdings Inc. (Taiwan).