- Summary

- Table Of Content

- Methodology

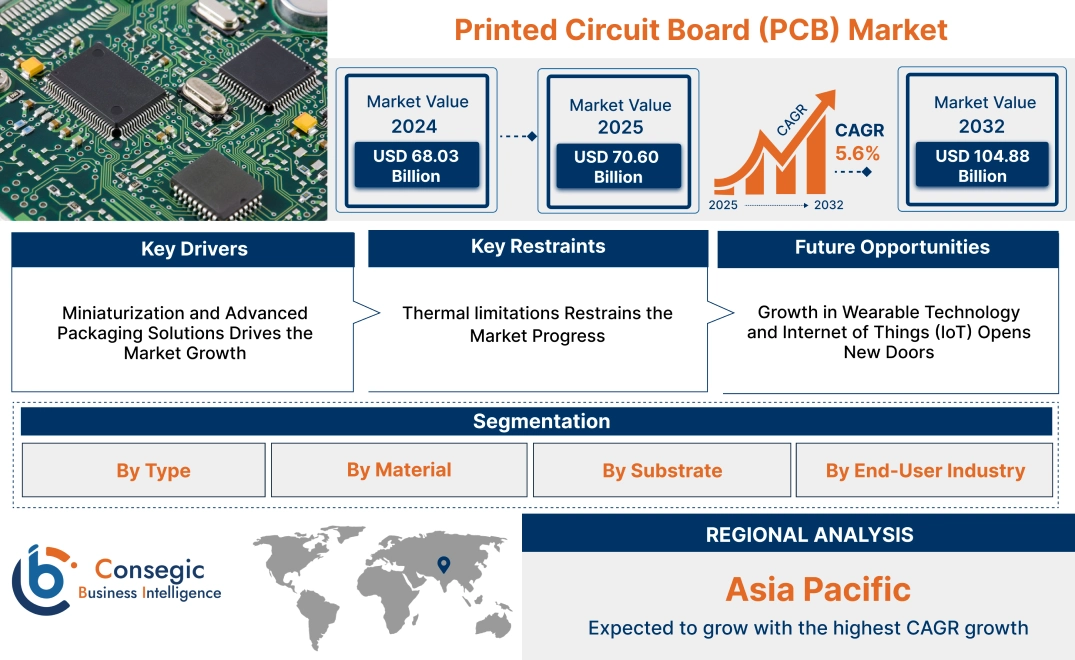

Printed Circuit Board (PCB) Market Size:

Printed Circuit Board (PCB) Market size is estimated to reach over USD 104.88 Billion by 2032 from a value of USD 68.03 Billion in 2024 and is projected to grow by USD 70.60 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

Printed Circuit Board (PCB) Market Scope & Overview:

A printed circuit board (PCB) is a foundational component in electronic devices, providing the mechanical and electrical framework for connecting various electronic components. It consists of conductive pathways etched onto a non-conductive substrate, enabling efficient signal transmission and power distribution within a circuit. PCBs are essential in applications ranging from consumer electronics and industrial equipment to automotive and aerospace systems.

These boards are available in different configurations, including single-layer, double-layer, and multi-layer designs, each tailored to specific performance and space requirements. Advanced PCBs incorporate flexible and rigid-flex structures, allowing integration into compact and complex electronic systems. They are manufactured using materials such as fiberglass, composite epoxy, and specialized laminates to ensure durability and reliability under various operational conditions.

End-users include industries such as telecommunications, medical devices, and automotive manufacturing, where reliable electronic circuitry is critical. PCBs play a fundamental role in modern electronics, supporting the functionality and performance of a wide range of devices.

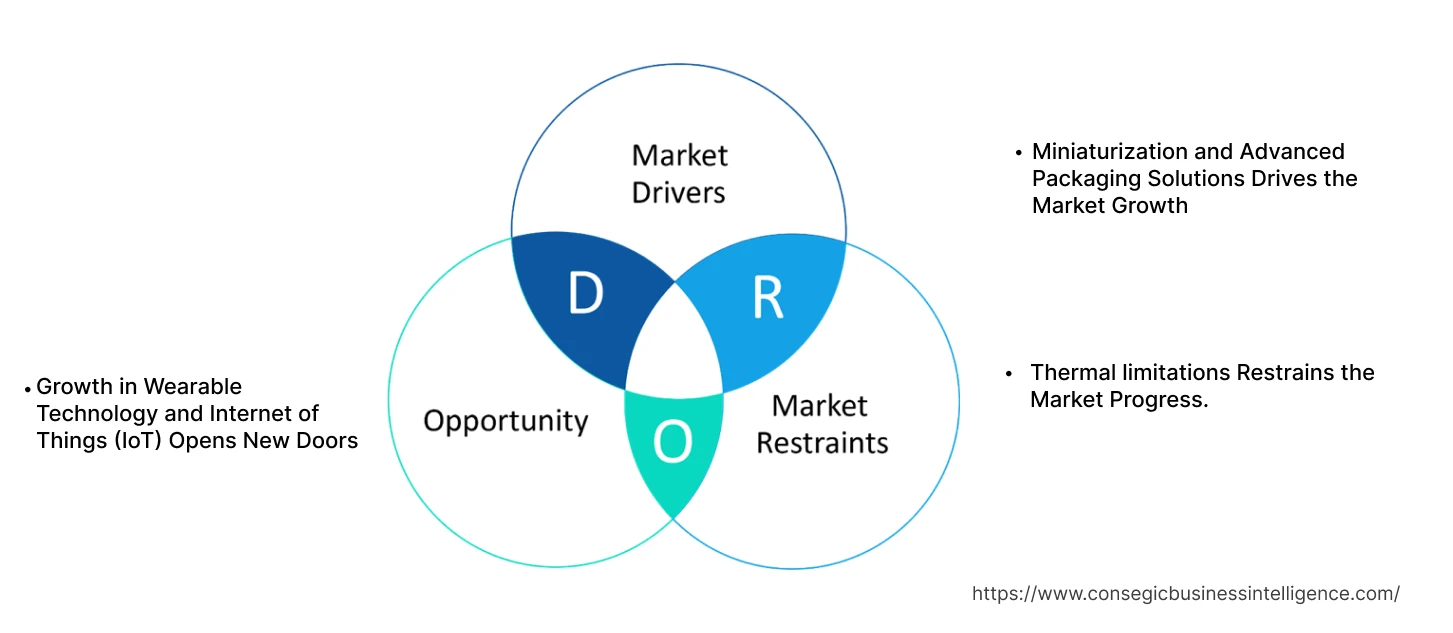

Printed Circuit Board (PCB) Market Dynamics - (DRO) :

Key Drivers:

Miniaturization and Advanced Packaging Solutions Drives the Market Growth

The growing demand for smaller, more powerful electronic devices is driving the need for advanced packaging solutions in printed circuit boards (PCBs). As industries like consumer electronics, medical devices, and telecommunications continue to prioritize miniaturization, manufacturers are required to develop compact PCBs that integrate complex functionalities into smaller spaces. Advanced packaging technologies such as System-in-Package (SiP) and Chip-on-Board (COB) enable multiple components, such as microchips, sensors, and other electronics, to be integrated into a single compact unit. These technologies allow for improved performance, reduced size, and enhanced efficiency, meeting the needs of modern electronic devices that require both portability and high functionality. As the demand for high-performance, compact devices grows across various sectors, the market for miniaturized PCBs with advanced packaging solutions is expected to expand, driving the printed circuit board market growth.

Key Restraints:

Thermal limitations Restrains the Market Progress

One significant restraint of printed circuit board is the challenge of heat management due to densely packed components. As electronic devices become smaller and more powerful, the components on the PCB are often packed closely together, leading to increased heat generation. Without proper thermal management, such as the integration of heat sinks or advanced thermal design techniques, excessive heat accumulates, potentially shortening the lifespan of components. This heat build-up causes performance degradation, malfunctions, or even permanent damage to the PCB and surrounding components. The need for efficient heat dissipation solutions adds complexity and cost to the PCB design process, especially in high-performance applications like telecommunications, automotive, and consumer electronics. Effective thermal management is essential for ensuring the reliability, durability, and optimal performance of electronic devices, presenting a significant challenge for manufacturers in meeting the growing demand for compact, high-functioning PCBs. Thus, the above mentioned factors limit the printed circuit board market expansion.

Future Opportunities :

Growth in Wearable Technology and Internet of Things (IoT) Opens New Doors

Wearables, such as smartwatches, fitness trackers, and healthcare monitoring devices, require compact, lightweight, and highly efficient PCBs to support their advanced functionality while maintaining portability. Additionally, IoT devices, which are becoming increasingly prevalent in smart homes, industrial applications, and healthcare systems, also demand miniaturized and flexible PCBs that handle multiple interconnected components. As these technologies continue to proliferate, the need for specialized PCBs designed to meet the unique requirements of small form factors, low power consumption, and high reliability is set to increase. The growth of these sectors is driving innovation in PCB designs, pushing manufacturers to develop cutting-edge solutions that support the seamless integration of sensors, communication chips, and other components. This trend is expected to further accelerate need for advanced PCBs, creating printed circuit board market opportunities.

Printed Circuit Board (PCB) Market Segmental Analysis :

By Type:

Based on type, the market is segmented into Standard Multilayer PCBs, Rigid 1-2 Sided PCBs, HDI/Micro-via/Build-up, Flexible PCBs, Rigid-Flex PCBs, and Others.

The Standard Multilayer PCBs segment accounted for the largest revenue of the total printed circuit board market share in 2024.

- Standard multilayer PCBs are widely used in complex electronic devices, offering enhanced circuit density and improved electrical performance.

- These PCBs provide better signal integrity and are crucial for applications in data centers, telecommunication networks, and industrial control systems.

- The segment benefits from increased adoption in high-speed computing, where efficient power distribution and reduced electromagnetic interference are essential.

- As per printed circuit board market analysis, ongoing innovations in PCB fabrication techniques, including advanced via structures and impedance control, have contributed to the segment’s widespread adoption.

The HDI/Micro-via/Build-up segment is expected to register the fastest CAGR during the forecast period.

- High-Density Interconnect (HDI) PCBs support miniaturization trends in consumer electronics by enabling higher circuit densities within compact designs.

- These PCBs improve signal transmission and are extensively used in 5G communication devices, portable medical equipment, and high-performance computing systems.

- HDI technology enhances PCB durability and functionality while reducing power consumption, making it ideal for next-generation smart devices.

- As per printed circuit board market trends, increasing investment in IoT-enabled devices and AI-driven systems is expected to drive further advancements in HDI PCB technologies.

By Material:

Based on material, the market is segmented into FR-4, Polyimide, PTFE, Metal-Based, and Others.

The FR-4 segment accounted for the largest revenue of the total printed circuit board market share in 2024.

- FR-4 is the most commonly used PCB material due to its excellent electrical insulation, high mechanical strength, and cost-effectiveness.

- It provides high thermal resistance and flame retardancy, making it suitable for various consumer electronics, industrial controls, and networking equipment.

- The material supports multilayer designs, allowing for compact and durable PCB configurations in diverse electronic applications.

- Thus, the widespread availability and cost-efficiency of FR-4 substrates make them a preferred choice for large-scale PCB manufacturing, fueling the printed circuit board market demand.

The Polyimide segment is expected to register the fastest CAGR during the forecast period.

- Polyimide-based PCBs offer superior flexibility, thermal stability, and chemical resistance, making them ideal for aerospace, medical, and military applications.

- These PCBs are extensively used in flexible circuit designs, enabling advanced wearable technology and high-reliability automotive electronics.

- The requirement for lightweight and high-performance electronic components has increased the adoption of polyimide PCBs in mission-critical applications.

- Therefore, continued advancements in flexible PCB materials are expected to enhance the durability and performance of next-generation electronic devices, fueling the printed circuit board market expansion.

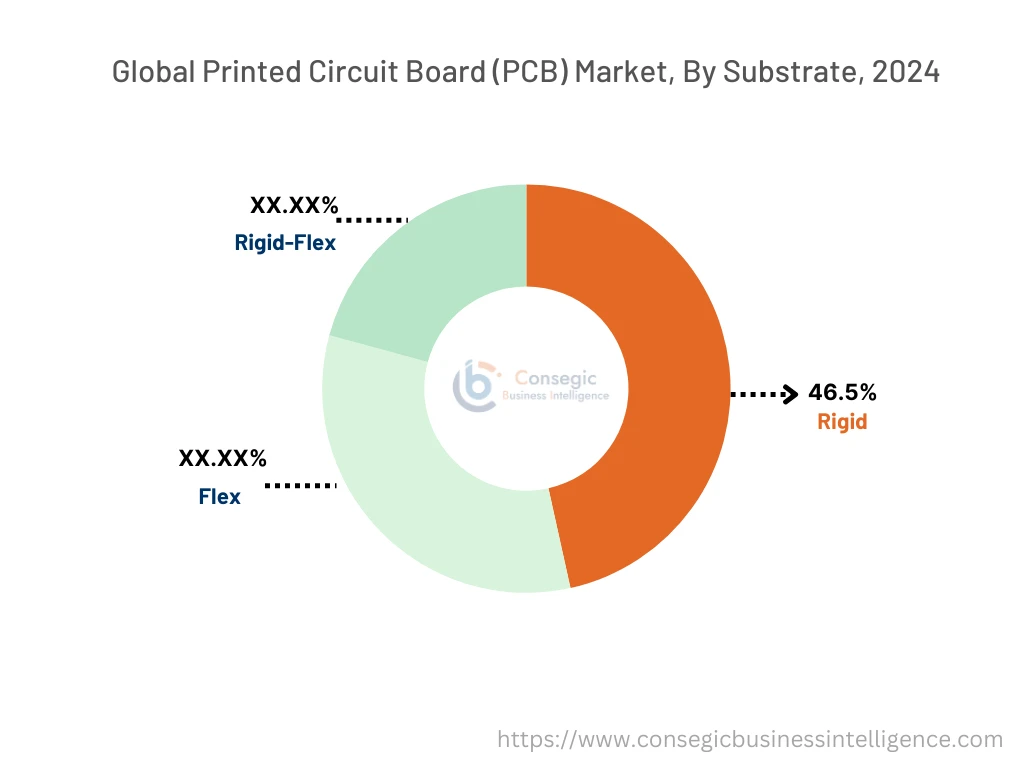

By Substrate:

Based on substrate, the market is segmented into Rigid, Flex, and Rigid-Flex.

The Rigid segment accounted for the largest revenue of 46.5% share in 2024.

- Rigid PCBs are widely used in computing, telecommunications, and industrial applications due to their stability, high durability, and ease of mass production.

- These PCBs provide excellent electrical conductivity and mechanical strength, ensuring reliable performance in electronic circuits.

- Rigid PCBs are commonly found in devices such as desktop computers, televisions, automotive control units, and power management systems.

- As per printed circuit board market analysis, the continuous advancements in multilayer rigid PCB technologies are improving circuit density and signal integrity for high-performance electronics.

The Rigid-Flex segment is expected to register the fastest CAGR during the forecast period.

- Rigid-Flex PCBs combine the durability of rigid boards with the adaptability of flexible circuits, providing space-saving and weight reduction benefits.

- These substrates are widely adopted in medical implants, aerospace systems, and high-end consumer electronics where design efficiency and reliability are crucial.

- The integration of rigid-flex PCBs into wearable technology, including smartwatches and fitness trackers, has further expanded their application scope.

- Thus, the development of advanced hybrid PCB designs is expected to improve reliability in mission-critical electronic systems, further driving the printed circuit board market demand.

By End-User Industry:

Based on end-user industry, the market is segmented into Electronics, Automotive, Aerospace & Defense, Healthcare, and Others.

The Electronics segment accounted for the largest revenue share in 2024.

- PCBs are integral to the consumer electronics sector, powering devices such as smartphones, tablets, laptops, and gaming consoles.

- The increasing need for compact, lightweight, and energy-efficient electronic products has fueled advancements in PCB miniaturization and high-frequency capabilities.

- Manufacturers are integrating advanced PCB materials and surface-mount technologies to enhance device performance and reduce power consumption.

- Therefore, as per the printed circuit board market trends, the continued expansion of the consumer electronics sector ensures the dominant position of PCBs in the global market.

The automotive segment is expected to register the fastest CAGR during the forecast period.

- The shift toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) has increased the reliance on high-performance automotive PCBs.

- PCBs in automotive applications must withstand extreme temperatures, vibrations, and electromagnetic interference, requiring specialized materials and designs.

- The integration of PCBs in infotainment systems, battery management units, and vehicle connectivity solutions has expanded their role in next-generation automobiles.

- Thus, ongoing developments in vehicle electrification and autonomous driving technologies are expected to drive PCB innovations in the automotive sector, boosting printed circuit board market opportunities.

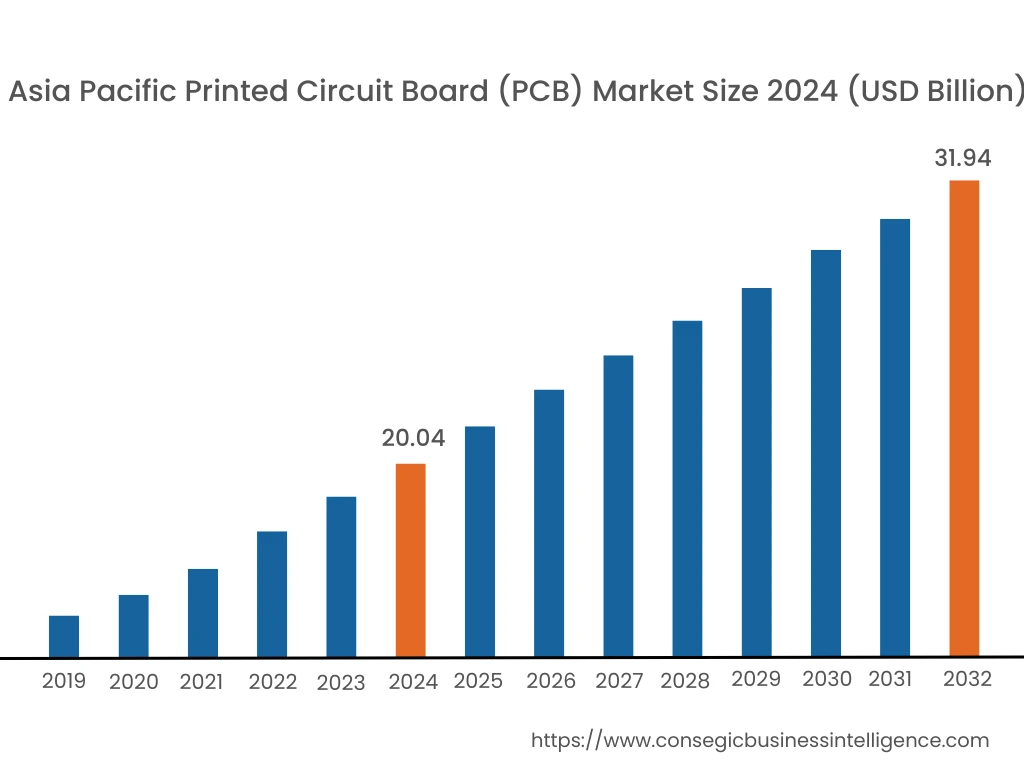

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

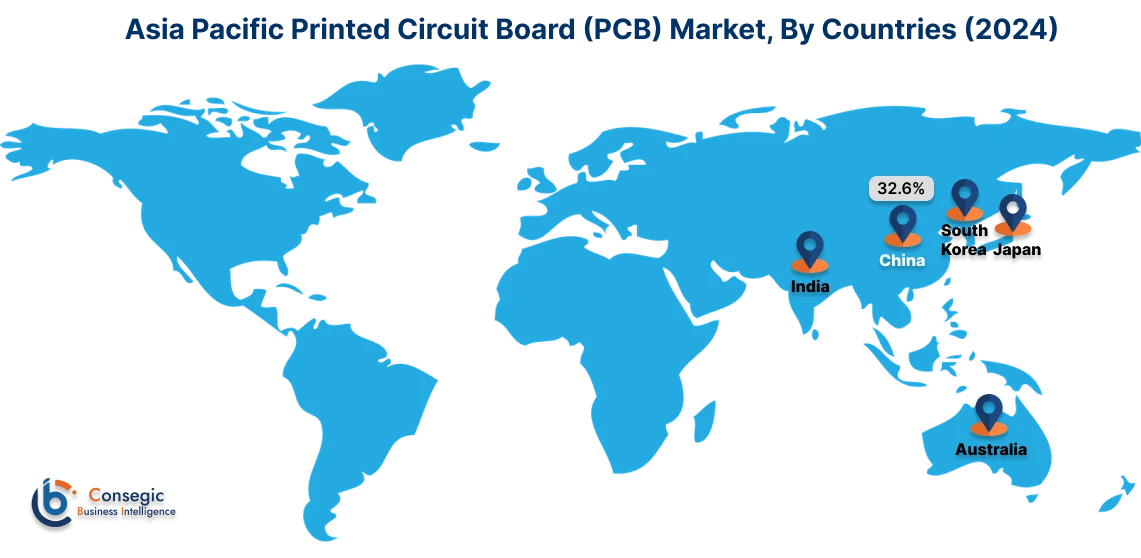

Asia Pacific region was valued at USD 20.04 Billion in 2024. Moreover, it is projected to grow by USD 20.85 Billion in 2025 and reach over USD 31.94 Billion by 2032. Out of this, China accounted for the maximum revenue share of 32.6%. The Asia-Pacific region is characterized by a vibrant printed circuit board market, underpinned by rapid industrialization and a robust commitment to technological innovation. A notable trend is the widespread adoption of cutting-edge manufacturing techniques that improve reliability and functionality across diverse applications. Another major shift is the development of localized production capabilities, as companies tailor advanced technologies to meet varied market requirements. Analysis indicates that supportive government policies and substantial investments in research and development are driving these shifts.

North America is estimated to reach over USD 33.99 Billion by 2032 from a value of USD 22.57 Billion in 2024 and is projected to grow by USD 23.38 Billion in 2025. In North America, the printed circuit board market thrives as a hub of technological innovation and advanced manufacturing. A notable trend is the integration of automation and digital technologies in production processes, which enhances design precision and operational efficiency. The shift towards environmentally friendly production methods, reflects a commitment to sustainability. Analysis indicates that strategic investments in research and development by industry leaders are continually refining product quality.

European markets distinguish themselves with a strong focus on quality and sustainability in printed circuit board manufacturing. A key trend is the incorporation of advanced materials and sophisticated design techniques that boost performance while minimizing environmental impact. Additionally, the collaborative approach between research institutions and industry players, drives innovation and the adoption of state-of-the-art production methods. Analysis suggests that stringent regulatory frameworks help maintain high manufacturing standards and encourage sustainable practices.

In the Middle East and Africa, the printed circuit board market is evolving as traditional manufacturing meets modern technological adoption. A prominent trend is the gradual integration of advanced production techniques aimed at improving product quality and reducing environmental impact. Another trend is the emerging focus on digital transformation to streamline manufacturing processes and boost operational efficiency. Analysis reveals that increased investments in upgrading industrial infrastructure are shaping the market, while comprehensive analysis suggests that ongoing regulatory reforms and strategic initiatives are aligning local practices with global standards.

Latin American markets are increasingly embracing modern manufacturing practices in the printed circuit board sector. A key trend is the rising emphasis on energy efficiency and sustainability, which drives manufacturers to adopt advanced materials and eco-friendly processes. Another notable shift is the growth in collaboration between local companies and international technology providers, fostering innovation and knowledge transfer. Analysis indicates that such collaborative efforts, along with supportive policy frameworks, play a critical role in driving the printed circuit board market growth.

Top Key Players and Market Share Insights:

The Printed Circuit Board (PCB) market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Printed Circuit Board (PCB) market. Key players in the Printed Circuit Board (PCB) industry include -

- Zhen Ding Technology Holding Limited (China)

- Nippon Mektron Ltd. (Japan)

- TTM Technologies, Inc. (USA)

- AT&S Austria Technologie & Systemtechnik AG (Austria)

- Tripod Technology Corporation (Taiwan)

- Compeq Manufacturing Co., Ltd. (Taiwan)

- Shennan Circuits Co., Ltd. (SCC) (China)

- Ibiden Co., Ltd. (Japan)

- HannStar Board Corporation (Taiwan)

Recent Industry Developments :

Product Developments:

- In December 2024, OKI Circuit Technology developed a multi-layer PCB with stepped copper coin insertion, achieving 55 times better heat dissipation than conventional PCBs. Designed for environments where air cooling is impractical, such as outer space, this innovation enhances heat conduction for compact and high-performance electronic components. The stepped copper coins come in circular and rectangular forms to optimize compatibility. As semiconductor miniaturization increases, this solution addresses overheating challenges in high-speed data processing.

Acquisitions & Mergers:

- In November 2024, Carlyle acquired Kyoden, a Japanese PCB manufacturer known for small-lot, high-variety production with quick turnaround times. Founded in 1983, Kyoden operates in Japan and Thailand, serving industries such as semiconductors, automotive, and communications. The company specializes in high-multilayer and build-up PCBs, responding to increasing demand for miniaturization. Carlyle aims to support Kyoden’s growth by enhancing its manufacturing capabilities and expanding internationally.

Business Expansion:

- In June 2023, Schweitzer Engineering Laboratories (SEL) has opened a new $100M, 162,000-square-foot printed circuit board factory in Moscow, Idaho. The facility, one of the few PCB plants built in the U.S. in the past decade, is expected to rank among the top 10 U.S. PCB producers. The factory enhances SEL’s supply chain and manufacturing capabilities while incorporating advanced automation and environmentally friendly processes.

Printed Circuit Board (PCB) Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2032 |

| Market Size in 2032 | USD 104.88 Billion |

| CAGR (2025-2032) | 5.6% |

| By Type |

|

| By Material |

|

| By Substrate |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the printed circuit board market? +

The Printed Circuit Board (PCB) Market size is estimated to reach over USD 104.88 Billion by 2032 from a value of USD 68.03 Billion in 2024 and is projected to grow by USD 70.60 Billion in 2025, growing at a CAGR of 5.6% from 2025 to 2032.

What are the key segments in the printed circuit board market? +

The key segments in the Printed Circuit Board (PCB) market are categorized by type, material, substrate, and end-user industry. By type, the market includes Standard Multilayer PCBs, Rigid 1-2 Sided PCBs, HDI/Micro-via/Build-up, Flexible PCBs, Rigid-Flex PCBs, and others. By material, it includes FR-4, Polyimide, PTFE, Metal-Based, and others. The substrate segment consists of Rigid, Flex, and Rigid-Flex, while the end-user industries include Electronics, Automotive, Aerospace & Defense, Healthcare, and others.

Which segment is expected to grow the fastest in the printed circuit board market? +

The HDI/Micro-via/Build-up segment is expected to experience steady growth during the forecast period. This is driven by the increasing demand for miniaturization in consumer electronics, especially in applications such as 5G communication devices, portable medical equipment, and high-performance computing systems.

Who are the major players in the printed circuit board market? +

Major players in the Printed Circuit Board (PCB) market include Zhen Ding Technology Holding Limited (China), Nippon Mektron Ltd. (Japan), TTM Technologies, Inc. (USA), AT&S Austria Technologie & Systemtechnik AG (Austria), Tripod Technology Corporation (Taiwan), Compeq Manufacturing Co., Ltd. (Taiwan), Shennan Circuits Co., Ltd. (SCC) (China), Ibiden Co., Ltd. (Japan), and HannStar Board Corporation (Taiwan).