Global Artificial Intelligence Chipset Market to Surpass USD 297.50 Billion by 2031 | CAGR of 26.7%

Category : Semiconductor And Electronics | Published Date : Nov 2024 | Type : Press Release

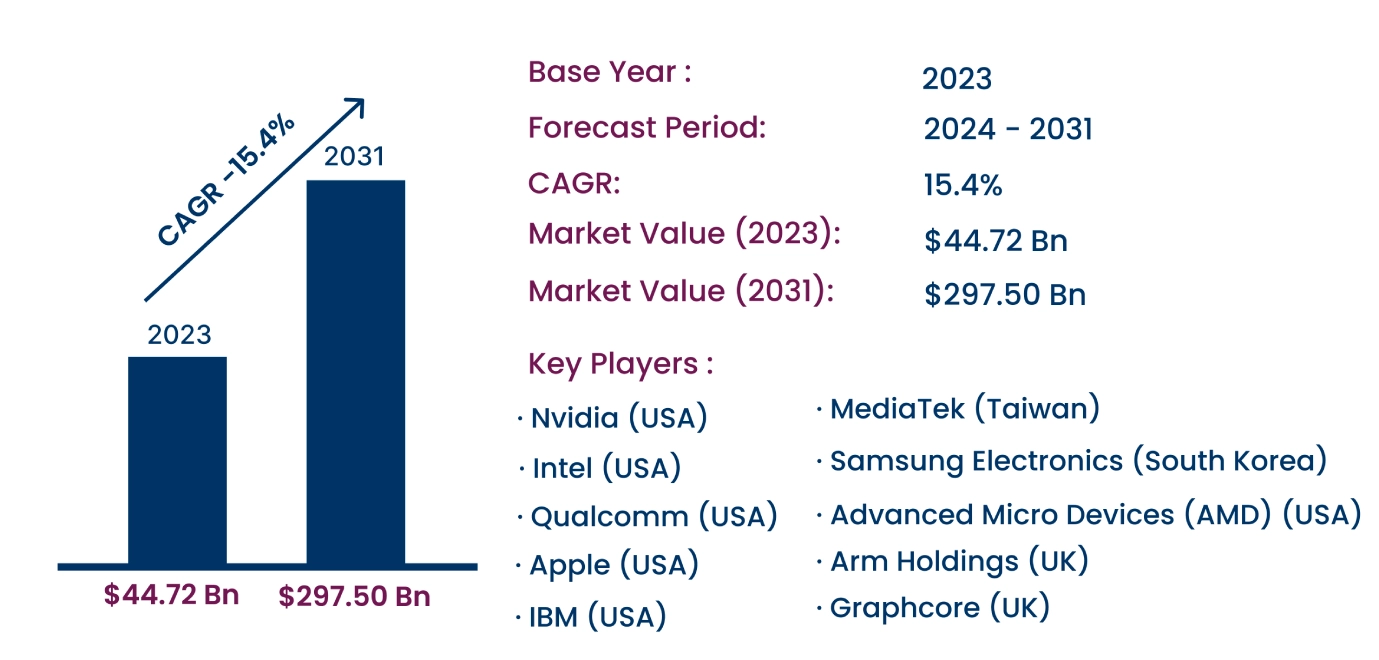

Artificial Intelligence Chipset Market Scope & Overview:

In the newly published report, Consegic Business Intelligence states that The Artificial Intelligence Chipset Market was valued at USD 44.72 Billion in 2023 and is projected to reach USD 297.50 Billion by 2031, growing at a CAGR of 26.7% from 2024 to 2031. Artificial Intelligence (AI) chipsets are specialized hardware components designed to enhance the efficiency and speed of AI applications, including machine learning and neural network operations. These chipsets are crucial in processing large datasets and performing complex computations, making them integral to sectors like automotive, healthcare, and consumer electronics.

The report comprises the Artificial Intelligence Chipset Market Share, Size & Industry Analysis, By Chipset Type (Graphics Processing Unit (GPU), Application-Specific Integrated Circuit (ASIC), Field-Programmable Gate Array (FPGA), Central Processing Unit (CPU), Others), By Technology (System-on-Chip (SoC), System-in-Package (SiP), Multi-Chip Module, Others), By Processing Type (Edge, Cloud, Hybrid), By Functionality (Training, Inference), By End-User Industry (Automotive, Consumer Electronics, Healthcare, Retail, IT & Telecom, Banking, Financial Services, and Insurance (BFSI), Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa), and Forecast, 2024–2031.

The report contains detailed information on Artificial Intelligence Chipset Market Trends, Opportunities, Value, Growth Rate, Segmentation, Geographical Coverage, Company Profile, In-depth Expert Analysis, Revenue Forecast, Competitive Landscape, Growth Factors, Restraint or Challenges, Environment & Regulatory Landscape, PESTLE Analysis, PORTER Analysis, Key Technology Landscape, Value Chain Analysis, and Cost Analysis.

Growing adoption of AI in cloud computing and data centers is a major factor driving market growth, while complex and expensive manufacturing processes remain a significant restraint.

Segmental Analysis :

By Chipset Type, the market is segmented into GPU, ASIC, FPGA, CPU, and others.

- GPU accounted for the largest market share of 40.62% in 2023, driven by its superior parallel processing capabilities, making it ideal for deep learning and complex AI workloads.

- ASIC is expected to register the fastest CAGR during the forecast period, attributed to its efficiency in specific AI applications such as speech recognition and image classification.

By Technology, the market includes SoC, SiP, Multi-Chip Module, and others.

- System-on-Chip (SoC) held the largest revenue share in 2023 due to its integration capabilities, crucial for powering compact AI-enabled devices.

- System-in-Package (SiP) is projected to grow rapidly, driven by the need for real-time AI processing in edge computing devices.

By Processing Type, the market is categorized into Edge, Cloud, and Hybrid.

- Cloud-based AI chipsets dominated the market share in 2023, owing to the rising reliance on cloud platforms for large-scale AI workloads.

- Edge processing is anticipated to exhibit the fastest growth, supported by increasing adoption of AI in autonomous systems and IoT devices requiring low-latency processing.

By Functionality, the market is bifurcated into Training and Inference.

- Training accounted for the largest share in 2023, driven by the high computational power required for developing AI models across sectors like healthcare and finance.

- Inference is expected to grow at the highest rate, fueled by the increasing deployment of AI applications in real-time environments.

By End-User Industry, the market segments include Automotive, Consumer Electronics, Healthcare, Retail, IT & Telecom, BFSI, and others.

- Automotive held the largest revenue share in 2023, propelled by the integration of AI in advanced driver assistance systems (ADAS) and autonomous vehicles.

- Healthcare is projected to witness the fastest growth, driven by the increasing adoption of AI in diagnostics, medical imaging, and personalized medicine.

Based on regions, the global market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America.

- North America led the market in 2023, supported by technological advancements and a strong presence of leading AI chipset manufacturers.

- Asia-Pacific is expected to exhibit the highest CAGR, driven by significant investments in AI technologies, particularly in China, Japan, and India.

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 297.50 Billion |

| CAGR (2024-2031) | 26.7% |

| By Chipset Type | GPU, ASIC, FPGA, CPU, Others |

| By Technology | SoC, SiP, Multi-Chip Module, Others |

| By Processing Type | Edge, Cloud, Hybrid |

| By Functionality | Training, Inference |

| By End-User | Automotive, Consumer Electronics, Healthcare, Retail, IT & Telecom, BFSI, Others |

| By Region | North America(U.S., Canada, Mexico) Europe(U.K., Germany, France, Spain, Italy, Russia, Benelux, Rest of Europe) APAC(China, South Korea, Japan, India, Australia, ASEAN, Rest of Asia-Pacific) Middle East & Africa(GCC, Turkey, South Africa, Rest of MEA) LATAM(Brazil, Argentina, Chile, Rest of LATAM) |

Top Key Players & Competitive Landscape :

The competitive landscape encompasses major innovators, aftermarket service providers, industry giants, and niche players, all of which are thoroughly examined by Consegic Business Intelligence in terms of their strengths, weaknesses, and value-addition potential. This report includes detailed profiles of key players, market share analysis, mergers and acquisitions, resulting market fragmentation, and emerging partnership trends and dynamics.

List of prominent players in the Artificial Intelligence Chipset Industry:

- Nvidia (USA)

- Intel (USA)

- Graphcore (UK)

- Arm Holdings (UK)

- MediaTek (Taiwan)

- Advanced Micro Devices (AMD) (USA)

- Qualcomm (USA)

- Samsung Electronics (South Korea)

- Apple (USA)

- IBM (USA)

Recent Industry Developments :

- In October 2024, AMD introduced the Ryzen AI Pro 300 series processors, aimed at business laptops, featuring enhanced AI capabilities and improved energy efficiency.

- In October 2024, Qualcomm launched Snapdragon 8 Elite, delivering superior performance for AI applications in premium smartphones with next-gen connectivity.

- In March 2024, Nvidia unveiled the Blackwell platform, offering advanced GPU architecture designed for large-scale AI workloads, promising significant improvements in efficiency and performance.