- Summary

- Table Of Content

- Methodology

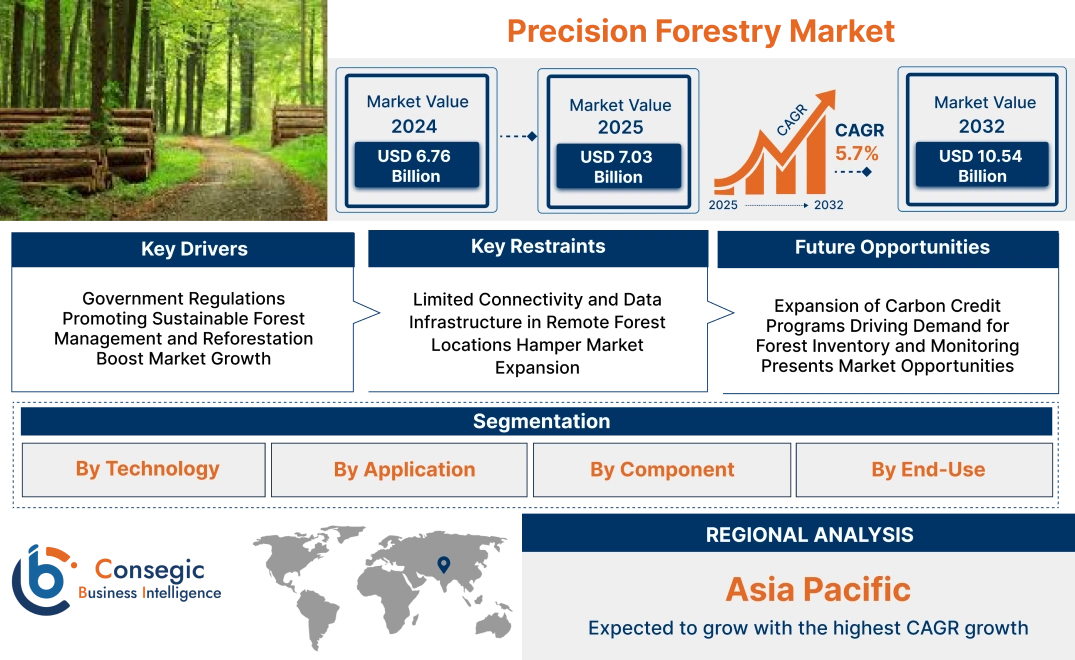

Precision Forestry Market Size:

Precision Forestry Market size is estimated to reach over USD 10.54 Billion by 2032 from a value of USD 6.76 Billion in 2024 and is projected to grow by USD 7.03 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Precision Forestry Market Scope & Overview:

Precision forestry is the utilization of sophisticated technologies like GPS, remote sensing, GIS, and data analysis to enhance forest management techniques. It aids in making informed decisions with real-time monitoring, precise mapping, and predictive modeling of forest status, inventory, and cycles of growth.

Main features encompass automated harvesting systems, drone-based inspections, yield prediction, and soil and vegetation health monitoring through sensors. They streamline operational processes, minimize resource loss, and enhance planning precision in harvesting, planting, thinning, and conservation processes.

It facilitates site-specific management, enhances timber production, and facilitates ecosystem monitoring with minimal disturbance to natural habitats. Its capacity for bringing digital technology into field operations enables forest managers and industry players to optimize workflows, enhance sustainability returns, and ensure compliance with regulatory requirements. The method constitutes a paradigm shift to data-driven forest resource management with enhanced transparency and long-term environmental responsibility.

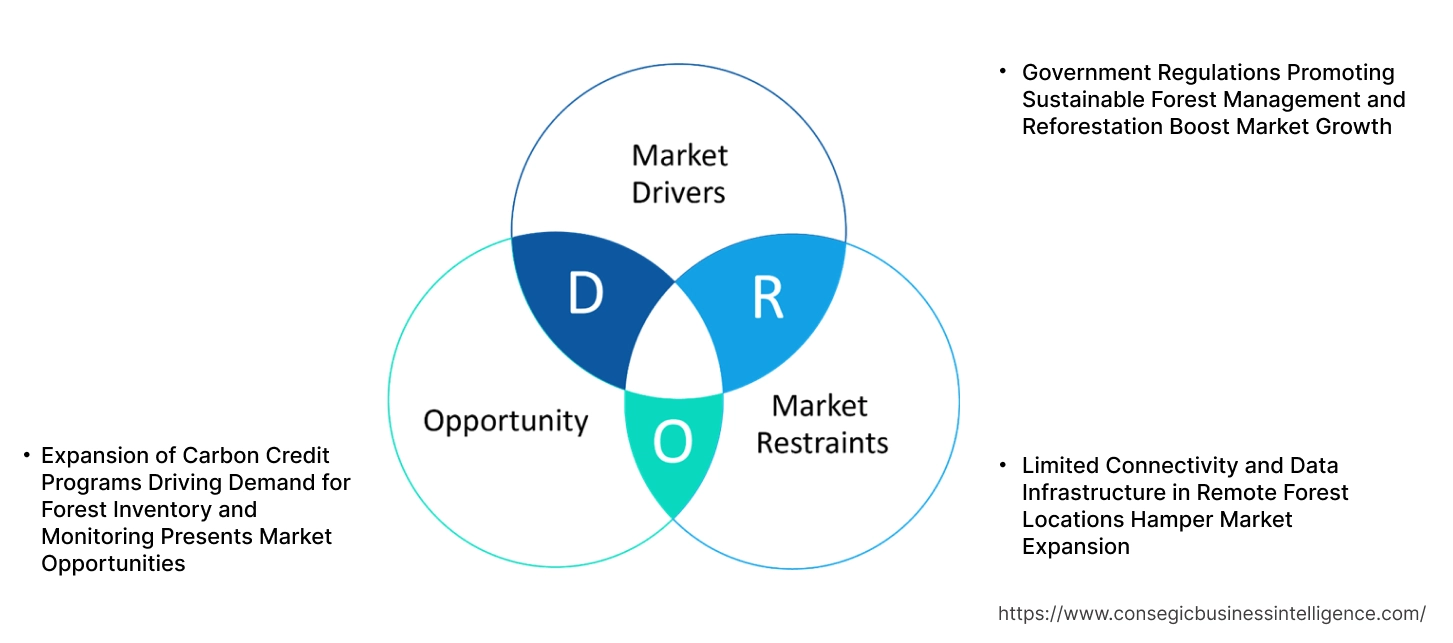

Precision Forestry Market Dynamics - (DRO) :

Key Drivers:

Government Regulations Promoting Sustainable Forest Management and Reforestation Boost Market Growth

Governments in Europe, North America, and Asia-Pacific are accelerating initiatives to support sustainable forestry through regulatory requirements and fiscal incentives. Initiatives such as the EU's Forest Strategy, Canada's Sustainable Forestry Initiative, and reforestation goals under India's Green India Mission are compelling the uptake of digital monitoring solutions and precision forest mapping technologies. Such regulations generally oblige forest operators and landowners to deliver verifiable information on replanting, logging activity, biodiversity conservation, and tree cover. Precision forestry technology such as LiDAR, geospatial analysis, and satellite imagery is facilitating transparent reporting and documentation for compliance. Traceability and carbon accounting are also increasingly being sought by certified timber producers who aim to obtain FSC or PEFC certification.

- For instance, the Government of India allocated the Environment, Forestry and Wildlife program, Rs 720 crore in the 2025-26 Union Budget, which is an increase of 22% compared to the 2024-25 allocation. This supports the procurement and application of advanced technologies for the proper management of the forests.

As environmental responsibility becomes key to both public and private forest management, the adoption of sophisticated forest monitoring platforms is expanding rapidly, leading to consistent precision forestry market expansion.

Key Restraints:

Limited Connectivity and Data Infrastructure in Remote Forest Locations Hamper Market Expansion

Most forestry activity occurs in secluded or mountainous areas with unsteady internet access, cloud capabilities, or cell phone networks. These locations often lack the digital infrastructure needed to facilitate real-time data synchronization, IoT device assimilation, and remote sensing platform software updates. Precision forestry technologies that rely on continuous data input and cloud computation perform suboptimally when internet connectivity is not consistent or altogether absent. This hurdle hinders UAV-based imaging, live equipment telemetries, and intelligent harvesting coordination adoption in underserved areas lacking proper infrastructure. Forestry contractors and governments operating in remote landscapes are also hindered by decision-making delays caused by latency in data fetching. Even as digital forestry solutions become more sought after, such technological constraints limit system performance and deployment potential—thereby hindering precision forestry market growth in underserved geographies.

Future Opportunities :

Expansion of Carbon Credit Programs Driving Demand for Forest Inventory and Monitoring Presents Market Opportunities

The fast expansion of voluntary and compliance carbon markets is generating huge demand for accurate instruments that measure forest biomass and carbon sequestration. Landowners, conservation organizations, and forest product manufacturers are increasingly adopting satellite-based canopy measurement, LiDAR mapping, and drone-assisted inventory systems to authenticate carbon offsets. Such technologies enable transparent, measurable, and reportable carbon accounting against standards like Verra, Gold Standard, and ART TREES. As carbon offset verification becomes integral to forestry-related climate finance, precision forestry solutions are increasingly vital for tracking forest condition, degradation, and growth cycles. This convergence of environmental sustainability and digital land management is creating new service models for platform providers, consultants, and equipment manufacturers.

- For instance, in September 2024, Planet Labs PBC, a trusted provider of regular Earth data and insights, launched Forest Carbon Monitoring, the world’s first global-scale forest monitoring system providing insights every quarter with a 3m resolution as powered by AI. The dataset estimates aboveground carbon, canopy height, and canopy cover globally, dating back to 2021, setting new standards for monitoring forest changes. This product helps users support voluntary carbon markets, regulatory compliance, and deforestation mitigation.

As the world's carbon economy hastens, so too does demand for high-quality forest data reveal scalable precision forestry market opportunities led by both compliance and expansion of climate-aligned investing.

Precision Forestry Market Segmental Analysis :

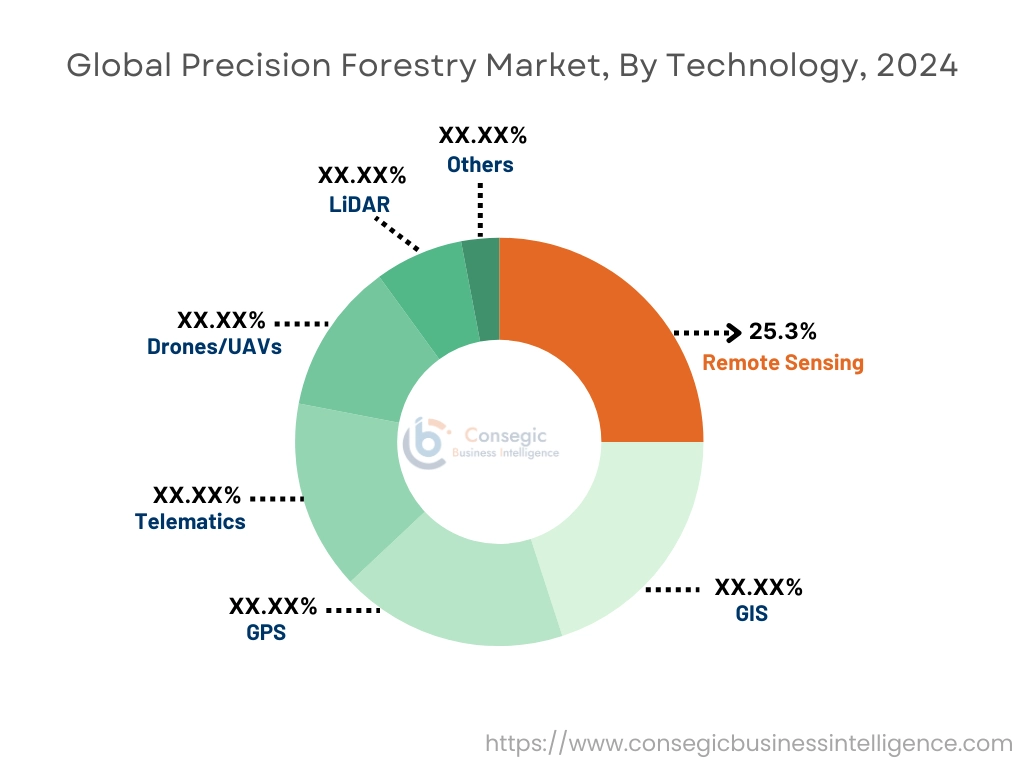

By Technology:

Based on technology, the market is segmented into remote sensing, GIS, GPS, telematics, drones/UAVs, LiDAR, and others.

The remote sensing segment held the largest revenue share of 25.3% in 2024.

- Remote sensing technologies provide large-scale forest cover data and track changes in canopy density, aiding in early deforestation detection.

- Satellite imagery and aerial data are used extensively for forest health monitoring, biomass estimation, and land use classification.

- These systems support long-term forest inventory and are widely adopted by governmental and conservation bodies.

- As per precision forestry market analysis, remote sensing remains the foundation of data-driven forest management operations.

The LiDAR segment is expected to witness the fastest CAGR during the forecast period.

- LiDAR provides accurate 3D forest structure data including tree height, volume, and canopy density, improving yield predictions.

- It is increasingly used in advanced mapping, habitat assessments, and post-harvest evaluation in industrial forests.

- Integration with drones enhances LiDAR's cost-efficiency and enables high-resolution analysis in inaccessible terrains.

- According to precision forestry market trends, rising interest in high-precision mapping tools is propelling LiDAR system investments.

By Application:

The market is segmented into forest management and planning, precision silviculture, wildlife habitat management, carbon sequestration, genetics and nurseries, fire management, harvesting management, and inventory & logistics management.

The forest management and planning segment accounted for the largest precision forestry market share in 2024.

- Forest management and planning involve the integration of GIS, remote sensing, and LiDAR technologies to optimize land use, species selection, and rotation cycles.

- This segment encompasses monitoring forest health, scheduling silvicultural operations, and defining zoning for conservation and utilization.

- Public and private forest managers rely on digital tools for regulatory compliance, environmental impact assessment, and sustainable yield forecasting.

- The dominance of this segment stems from its broad application across both industrial plantations and community-managed forest landscapes, addressing a large portion of the precision forestry market demand.

The inventory & logistics management segment is projected to witness the fastest CAGR during the forecast period.

- Inventory & logistics tools are critical for real-time tracking of timber volumes, harvest status, and transport coordination from forest to mill.

- These systems utilize RFID tagging, GPS-enabled machinery, and integrated supply chain software to minimize losses and ensure traceability.

- Logistics optimization reduces operational costs and improves carbon accounting, aligning with ESG goals and certification requirements.

- The segment’s rapid expansion is driven by industrial forestry firms adopting automation to streamline throughput, contributing significantly to precision forestry market growth.

By Component:

Based on component, the market is segmented into hardware, software, and services.

The hardware segment held the largest revenue share in 2024.

- Drones, sensors, GPS units, and harvesting equipment dominate capital investments in precision forestry.

- Ruggedized devices with connectivity features enhance in-field data capture reliability.

- Hardware providers are integrating IoT for real-time system diagnostics and uptime management.

- As per precision forestry market trends, scalable hardware platforms are foundational to full system deployments.

The software segment is projected to register the fastest CAGR.

- Mapping, planning, and analytics platforms enable data visualization and decision-making.

- AI-based modeling tools improve prediction accuracy for yield, fire risk, and health status.

- Cloud-based platforms support multi-stakeholder collaboration and remote asset control.

- Open API software fosters interoperability across forestry systems, supporting the increasing precision forestry market demand.

By End Use:

Based on end-use, the market is segmented into industrial forests, commercial plantations, government & community forestry, academic & research institutes, forestry contractors, and others.

The industrial forests segment accounted for the largest precision forestry market share in 2024.

- Large-scale operations adopt precision tools to meet sustainability mandates, maximize yield, and optimize labor.

- They invest in integrated harvesting, tracking, and carbon reporting platforms.

- These entities also leverage drone-based aerial surveys for large-area monitoring.

- As per precision forestry market analysis, industrial operators are leading the push toward full digital forestry adoption.

The forestry contractors segment is projected to grow at the fastest CAGR.

- Contractors serve as key adopters of portable, high-efficiency technologies to improve jobsite performance.

- They benefit from precision tools for logging, hauling, and reforestation, often integrated with client systems.

- Rising equipment rentals and service-based forestry models expand this segment's scope.

- Thus, contractor-driven innovation is expected to drive long-term precision forestry market expansion.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

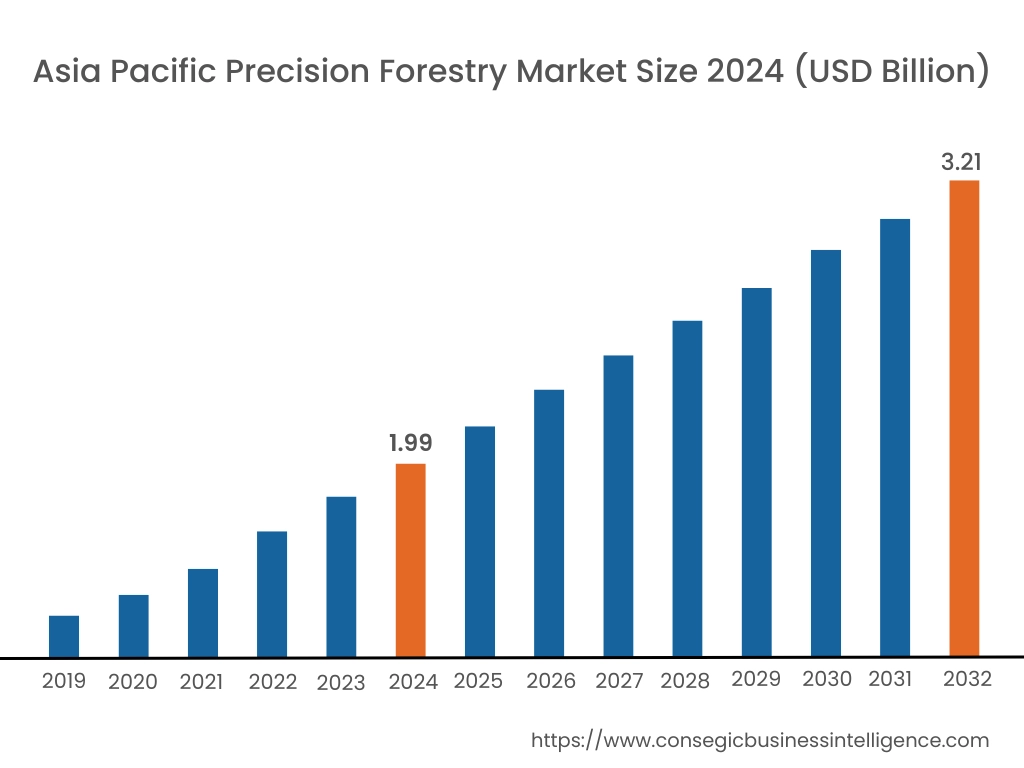

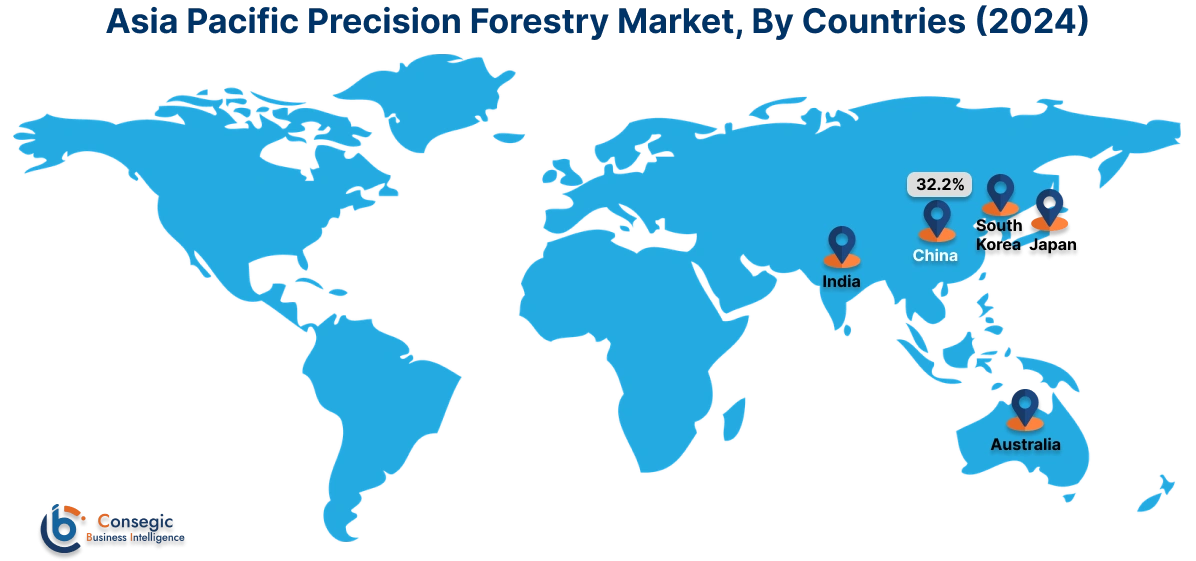

Asia Pacific region was valued at USD 1.99 Billion in 2024. Moreover, it is projected to grow by USD 2.07 Billion in 2025 and reach over USD 3.21 Billion by 2032. Out of this, China accounted for the maximum revenue share of 32.2%. Asia-Pacific is undergoing accelerated expansion in the precision forestry industry due to widening demand for timber, forest degradation issues, and extensive afforestation efforts. China, Japan, Australia, and South Korea are at the forefront of using satellite imagery, UAV canopy mapping, and IoT-enabled weather and soil sensors in plantation forests. Strong investment in reforestation monitoring and fire hazard modeling, driven by recent deforestation and wildfires, is indicated by market analysis. Australia is pushing the application of machine learning technologies to predict forest health, and Japan is working in the areas of robotics and automation for forested terrain. New and emerging economies in Southeast Asia are starting to use mobile forestry apps and digital log management systems to enhance productivity and transparency.

North America is estimated to reach over USD 3.42 Billion by 2032 from a value of USD 2.24 Billion in 2024 and is projected to grow by USD 2.33 Billion in 2025. North America is a highly active market for digital forestry solutions, especially in the United States and Canada, where commercial-scale forests and state-owned lands require efficient harvesting, reforestation, and inventory planning. Market research indicates robust adoption of LiDAR, GPS-harvesting systems, and predictive modeling platforms to maximize yield, reduce waste, and maintain sustainability certifications. Both public timber companies and government institutions are investing in drone mapping, real-time logging data, and satellite imaging for monitoring forest conditions. Continuous expansion is driven by climate resilience measures, carbon credit schemes, and the implementation of AI-based decision support systems.

Europe is a premier market given its sophisticated forestry management and high environmental commitments under the EU Green Deal. Sweden, Finland, Germany, and France are implementing precision technologies to improve multi-functional forest management, such as biodiversity conservation, timber productivity, and carbon sequestration. Market analysis indicates extensive adoption of geospatial mapping, automated harvester guidance systems, and digital twin technologies to provide traceability and maximize timber extraction. Digital forest inventories are becoming more common for long-term planning within sustainable forest management systems. The European precision forestry market opportunity lies in scaling up innovations to smaller, privately owned forests and scaling up interoperability with EU-scale sustainability platforms.

Latin America has an increasingly expanding market based on its expansive tropical and subtropical forest reserves, with Brazil, Chile, and Colombia proactively embracing technologies to tackle illegal logging, sustainable harvesting, and reforestation. Market analysis indicates close partnership between technology providers and public forestry institutions to digitalize forest maps, implement drone surveillance, and incorporate blockchain-based wood tracing. The necessity to reconcile economic value with ecological responsibility is creating interest in remote sensing technologies for canopy cover and biodiversity indexing. The market opportunity in precision forestry here is in scaling low-cost, affordable solutions for community-managed forests and export-oriented plantations looking for environmental certifications.

The Middle East and Africa are just starting to adopt precision forestry technologies, although potential is growing in areas like South Africa, Kenya, and parts of the Middle East with afforestation and green infrastructure ambitions. Market research shows that deforestation, land degradation, and desertification challenges are creating demand for digital solutions that facilitate forest mapping, seedling tracking, and moisture-level analysis. Collaborations with NGOs and multilateral development banks are facilitating the pilot of remote sensing and GIS solutions for sustainable forest planning. With adequate infrastructure development and training, the area could become a growth center for precision forestry for climate mitigation and land restoration activities.

Top Key Players and Market Share Insights:

The precision forestry market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global precision forestry market. Key players in the precision forestry industry include -

- Deere & Company (USA)

- Trimble Inc. (USA)

- Raven Industries (USA)

- Ecolog (Sweden)

- Sampo Rosenlew Ltd. (Finland)

- Tigercat International Inc. (Canada)

- Ponsse Plc (Finland)

- Komatsu Forest AB (Sweden)

- Treemetrics Ltd. (Ireland)

- Rottne Industri AB (Sweden)

Recent Industry Developments :

Product Launches:

- In July 2024, GeoCue, a specialist in geospatial solutions, added TrueView GO to its product lineup. This new addition is a handheld mapping arena, establishing new standards for portable, high-precision geospatial data collection. The product features GNSS RTK, LiDAR scanning, cameras and visual SLAM technologies for the seamless creation of digital twins in real-time.

Acquisitions:

- In June 2021, AFRY acquired MosaicMill Oy, a leading Finnish company that utilized drone and satellite image data for forest inventory services. This decision enabled AFRY to come closer to becoming a global leader in offering smart forestry digital solutions.

Partnerships:

- In January 2021, Metsä Group and the University of Helsinki entered into a partnership agreement for academic research and to bridge the gap between scientific knowledge and business needs. This collaboration aimed to inculcate necessary skills, solve technological and sustainable challenges and promote sustainable forestry.

Precision Forestry Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 10.54 Billion |

| CAGR (2025-2032) | 5.7% |

| By Technology |

|

| By Application |

|

| By Component |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Precision Forestry Market? +

Precision Forestry Market size is estimated to reach over USD 10.54 Billion by 2032 from a value of USD 6.76 Billion in 2024 and is projected to grow by USD 7.03 Billion in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

What specific segmentation details are covered in the Precision Forestry Market report? +

The Precision Forestry market report includes specific segmentation details for technology, application, component and end-use.

What are the end-use of the Precision Forestry Market? +

The end-use of the Precision Forestry Market are industrial forests, commercial plantations, government & community forestry, academic & research institutes, forestry contractors, and others.

Who are the major players in the Precision Forestry Market? +

The key participants in the Precision Forestry market are Deere & Company (USA), Trimble Inc. (USA), Raven Industries (USA), Tigercat International Inc. (Canada), Ponsse Plc (Finland), Komatsu Forest AB (Sweden), Treemetrics Ltd. (Ireland), Rottne Industri AB (Sweden), Ecolog (Sweden) and Sampo Rosenlew Ltd. (Finland).