- Summary

- Table Of Content

- Methodology

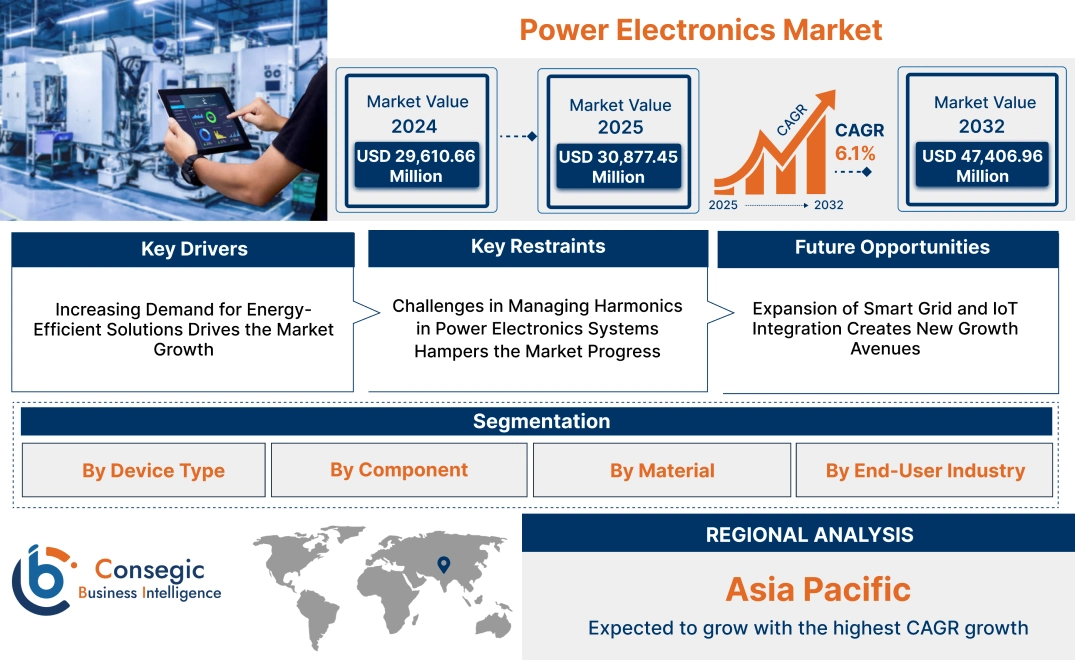

Power Electronics Market Size:

Power Electronics Market size is estimated to reach over USD 47,406.96 Million by 2032 from a value of USD 29,610.66 Million in 2024 and is projected to grow by USD 30,877.45 Million in 2025, growing at a CAGR of 6.1% from 2025 to 2032.

Power Electronics Market Scope & Overview:

Power electronics refers to the branch of electrical engineering that deals with the control, conversion, and management of electrical power using semiconductor devisces. These systems are essential for efficiently converting electrical energy into usable forms, ensuring optimal performance in a wide range of applications. They are widely used in industries such as automotive, renewable energy, consumer electronics, and industrial automation.

These systems include components such as inverters, converters, rectifiers, and power management integrated circuits (PMICs), each designed for specific functionalities. They are engineered for high efficiency, reliability, and compact design, enabling seamless integration into devices and systems. These systems also support advanced features such as energy saving, precise control, and compatibility with modern technologies.

End-users include manufacturers of electric vehicles, industrial equipment, and renewable energy systems, where efficient power management is critical. They play a vital role in advancing energy-efficient technologies and supporting modern electrical infrastructure.

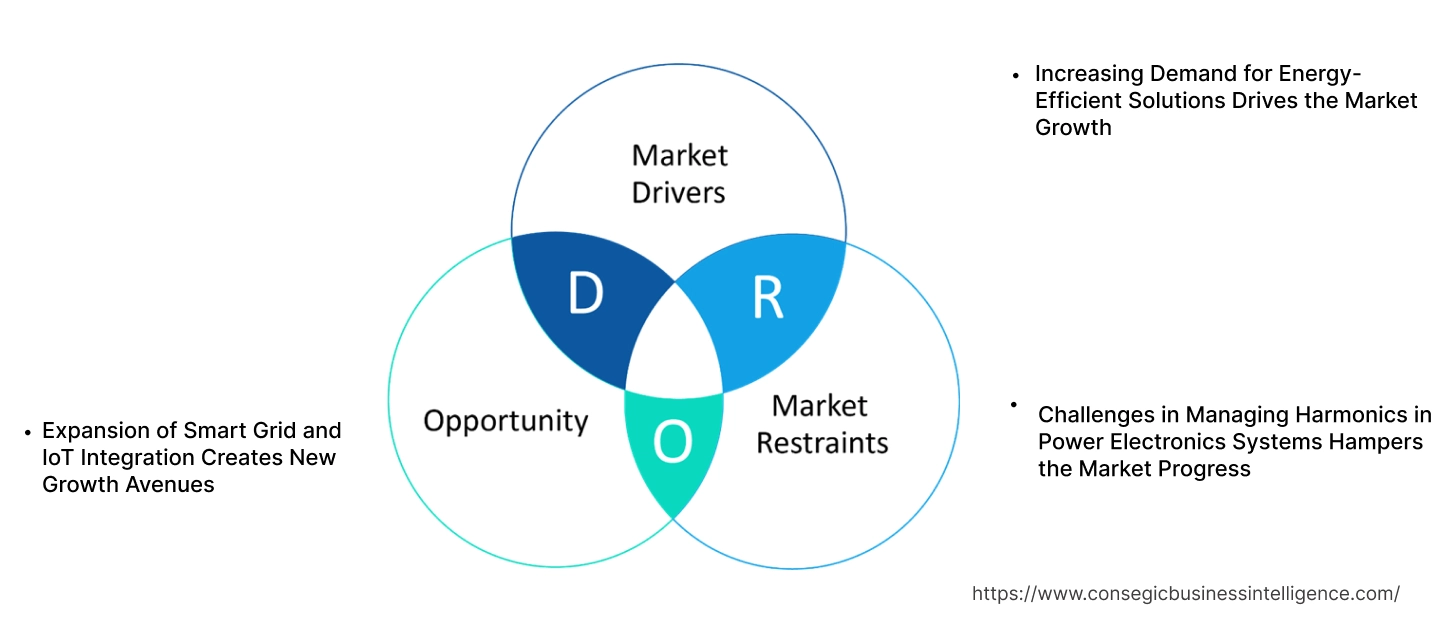

Power Electronics Market Dynamics - (DRO) :

Key Drivers:

Increasing Demand for Energy-Efficient Solutions Drives the Market Growth

The growing emphasis on energy efficiency across industries is significantly driving the power electronics market demand. These components play a crucial role in enhancing energy conversion, reducing losses, and optimizing power distribution, which is essential in achieving greater energy savings and reducing environmental impact. In renewable energy systems, power electronics ensure efficient energy conversion from solar panels and wind turbines to usable power. In electric vehicles (EVs), these systems manage battery charging, power distribution, and motor control, improving overall vehicle efficiency. Similarly, in industrial automation, it helps optimize the operation of machinery, reduce energy waste, and increase operational efficiency. As industries continue to prioritize sustainability and cost reduction, power electronics are becoming indispensable in enabling energy-efficient solutions that meet the growing need for cleaner, more efficient energy use across various sectors. This trend is expected to continue as global energy efficiency standards become more stringent.

Key Restraints:

Challenges in Managing Harmonics in Power Electronics Systems Hampers the Market Progress

One of the significant restraints is the generation of harmonics by the devices. These harmonics distort the waveform of electrical systems, leading to a range of issues such as overheating and premature aging of components. Over time, the presence of harmonics causes increased energy losses, reducing overall system efficiency and affecting the long-term reliability of power infrastructure. This is particularly concerning in industries with sensitive equipment or high power demands, where even small inefficiencies have considerable operational costs. The generation of harmonics also leads to potential damage to other electrical devices and systems connected to the grid, increasing maintenance requirements and reducing system longevity. As a result, the presence of harmonics poses a restraint in maintaining optimal performance and operational stability, limiting power electronics market growth.

Future Opportunities :

Expansion of Smart Grid and IoT Integration Creates New Growth Avenues

The integration of power electronics with smart grids and IoT systems offers a significant opportunity to enhance the efficiency and reliability of power distribution networks. Smart grids, equipped with advanced sensors, communication systems, and real-time monitoring capabilities, rely on these systems to manage voltage regulation, load balancing, and energy distribution more efficiently. By integrating IoT-enabled devices, they facilitate predictive maintenance, allowing utilities to identify issues before they cause system failures. Additionally, real-time data analysis helps optimize energy flow, reduce transmission losses, and improve the overall resilience of the grid. The combination of power electronics and smart grids supports dynamic power management, improves energy consumption forecasting, and enables better integration of renewable energy sources. As the requirement for more sustainable, flexible, and reliable energy systems grows, the adoption of these integrated technologies is expected to significantly enhance grid performance and drive the development of smarter power infrastructures. Thus, the aforementioned factors are driving the power electronics market opportunities.

Power Electronics Market Segmental Analysis :

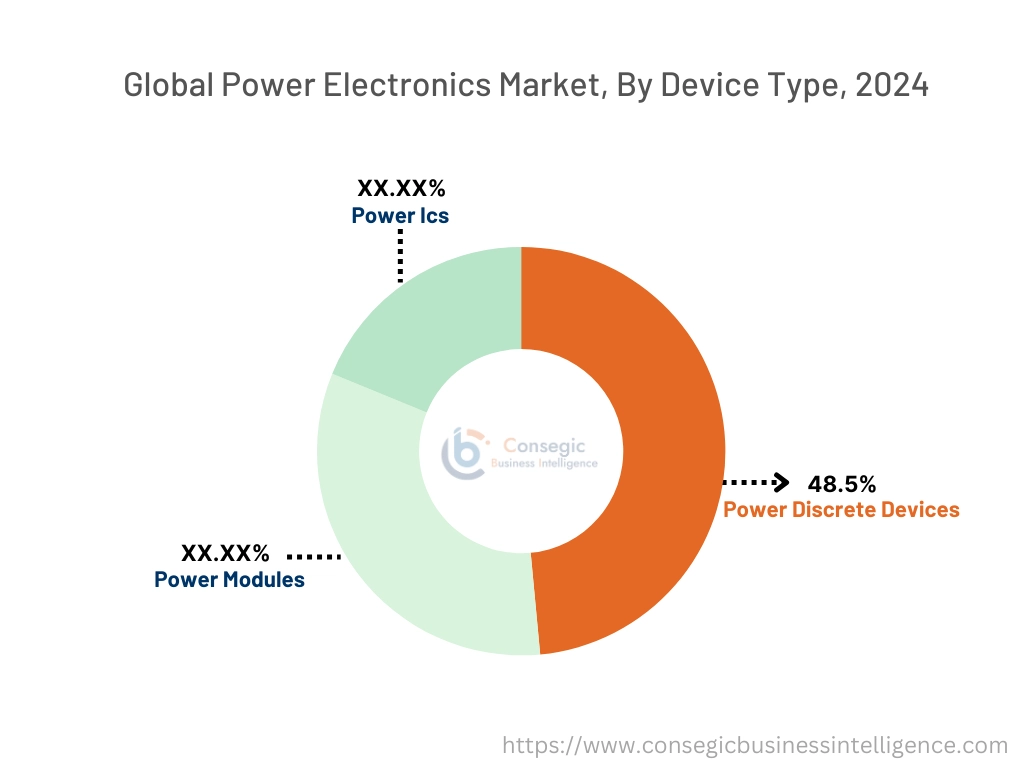

By Device Type:

Based on device type, the market is segmented into power discrete devices, power modules, and power ICs.

The power discrete devices segment accounted for the largest revenue of 48.5% of the total power electronics market share in 2024.

- Power discrete devices are widely used across multiple applications due to their cost-effectiveness and reliability in handling specific power requirements.

- Their dominance is attributed to the increasing adoption in automotive and industrial manufacturing sectors for controlling voltage and current levels.

- The demand for power discrete devices is supported by advancements in energy-efficient technologies and their integration into smart devices.

- As per the power electronics market analysis, these devices are essential for optimizing performance in renewable energy systems, driving significant adoption globally.

The power modules segment is projected to register the fastest CAGR during the forecast period.

- Power modules offer higher integration and compact designs, making them ideal for high-power and space-constrained applications.

- The rising adoption of electric vehicles and renewable energy systems drives need for power modules, particularly in inverters and converters.

- Technological advancements in power module designs, including improved thermal management, enhance their performance and reliability.

- Thus, increasing investment in infrastructure and industrial automation further accelerates the growth of this segment, contributing to the power electronics market expansion.

By Component:

Based on components, the market is segmented into thyristors, gate turn-off transistors, MCTs, silicon controlled rectifiers, AC/AD converters, static switches, MOSFETs, and others.

The MOSFET segment held the largest revenue of the total power electronics market share in 2024.

- MOSFETs are widely used in automotive, IT & telecom, and industrial applications due to their efficiency and ability to handle high-speed switching.

- The demand for MOSFETs is driven by their role in renewable energy systems, such as solar inverters and wind turbines.

- Advancements in MOSFET technology, including reduced power loss and improved heat dissipation, enhance their market position.

- As per the power electronics market trends, the adoption of electric vehicles globally has significantly boosted the utilization of MOSFETs in powertrain and battery management systems.

The silicon controlled rectifiers (SCRs) segment is anticipated to grow at the fastest CAGR during the forecast period.

- SCRs are critical components in high-voltage applications, including industrial drives and power control systems.

- Their ability to handle high current levels and provide reliable switching makes them a preferred choice in industrial manufacturing.

- Increasing investments in power distribution infrastructure and smart grid projects drive the adoption of SCRs.

- The segment benefits from ongoing research and development efforts to enhance SCR performance and expand application areas, fueling the power electronics market demand.

By Material:

Based on material, the market is segmented into silicon (Si), silicon carbide (SiC), gallium nitride (GaN), and others.

The silicon segment accounted for the largest revenue share in 2024.

- Silicon-based power devices dominate the market due to their affordability and well-established manufacturing processes.

- These devices are extensively used in consumer electronics, automotive, and industrial applications for efficient power management.

- The segment benefits from the widespread availability of silicon and its compatibility with various device designs.

- As per the power electronics market trends, continuous advancements in silicon technology, including improved thermal resistance, further support its dominance in the market.

The silicon carbide (SiC) segment is expected to grow at the fastest CAGR during the forecast period.

- SiC devices offer superior efficiency and thermal performance, making them ideal for high-power and high-temperature applications.

- The rapid adoption of electric vehicles and renewable energy systems accelerates the need for SiC-based power devices.

- SiC materials enable smaller, lighter, and more energy-efficient designs, enhancing their appeal across various industries.

- Thus, government initiatives promoting clean energy and energy-efficient technologies further drive the growth of this segment, boosting the power electronics market expansion.

By End-User Industry:

Based on end-user industry, the market is segmented into automotive, IT & telecom, energy & utilities, aerospace & defense, industrial manufacturing, and others.

The automotive segment held the largest revenue share in 2024.

- The growth in adoption of electric and hybrid vehicles significantly boosts the demand for power devices in automotive applications.

- Power devices play a crucial role in managing energy distribution and improving battery efficiency in electric vehicles.

- Rising investments in autonomous driving technology and connected vehicles further support the dominance of the automotive segment.

- As per the power electronics market analysis, increasing consumer preference for energy-efficient vehicles drives the utilization of advanced power components in automotive systems.

The energy & utilities segment is projected to grow at the fastest CAGR during the forecast period.

- The integration of renewable energy systems into the grid drives the requirement for power devices in energy and utility applications.

- Power devices are essential for improving the efficiency and reliability of power distribution and transmission networks.

- Growing investments in smart grids and energy storage systems accelerate the adoption of power devices in this sector.

- The segment benefits from government policies and incentives aimed at promoting clean energy and grid modernization, driving the power electronics market growth.

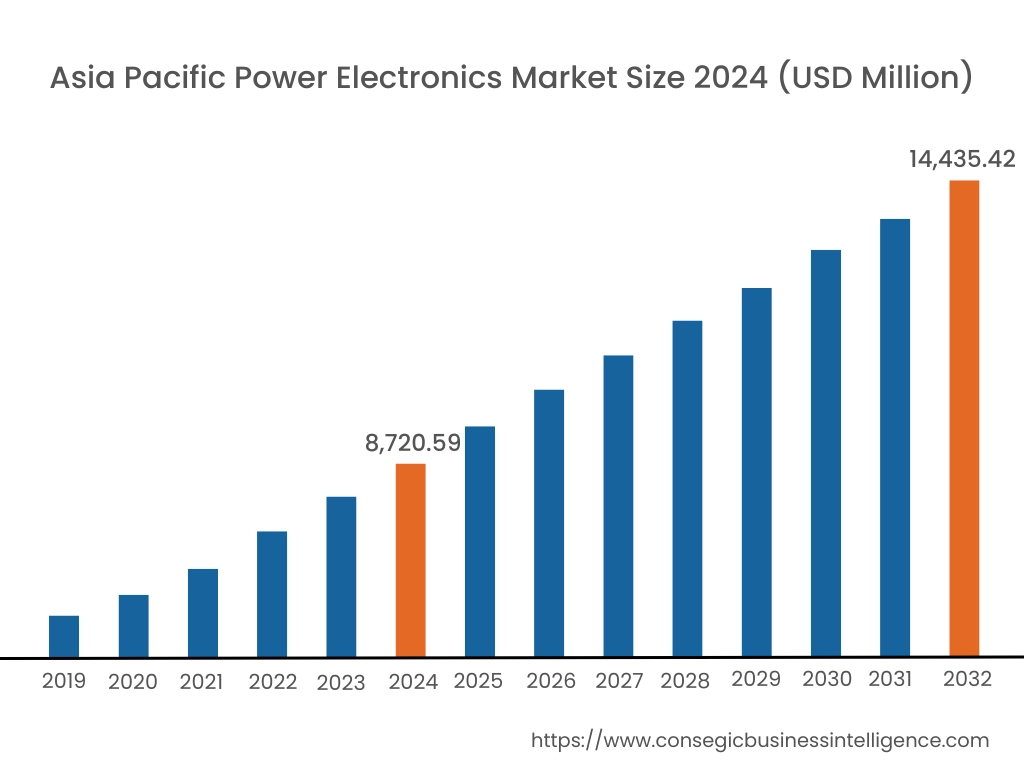

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

Asia Pacific region was valued at USD 8,720.59 Million in 2024. Moreover, it is projected to grow by USD 9,119.38 Million in 2025 and reach over USD 14,435.42 Million by 2032. Out of this, China accounted for the maximum revenue share of 31.6%. The Asia-Pacific region dominates the power electronics market, attributed to the rapid industrialization and urbanization leading to increased energy consumption. A prominent trend is the adoption of these systems in consumer electronics, automotive, telecom, and industrial applications. Analysis indicates that the region's focus on energy efficiency and the development of renewable energy infrastructure are contributing to power electronics market opportunities.

North America is estimated to reach over USD 15,364.60 Million by 2032 from a value of USD 9,822.10 Million in 2024 and is projected to grow by USD 10,222.73 Million in 2025. This region maintains a substantial position in the power electronics sector, propelled by the rapid expansion of renewable energy sources such as solar and wind power. The integration of these renewables necessitates efficient power conversion and management systems, roles fulfilled by power electronics. A notable trend is the increasing adoption of electric vehicles (EVs), which require sophisticated power electronics for energy use and battery management. Analysis indicates that investments in smart grid infrastructure and energy storage solutions further bolster the requirement in North America.

European countries are pivotal in the power electronics market, driven by a strong commitment to sustainability and renewable energy integration. The region emphasizes the development of high-efficiency power electronic devices to support green energy initiatives. A significant trend is the rise of smart grids and the increasing adoption of electric vehicles, amplifying the need for advanced power electronics. Analysis suggests that substantial investments in research and development foster innovation in power electronics, with collaborations between universities, research institutes, and industry players driving technological advancements.

In the Middle East and Africa, the power electronics market is influenced by the adoption of advanced electronic and semiconductor technologies across industries such as defense, telecommunications, and industrial automation. The focus is on enhancing energy efficiency and reliability through the implementation of sophisticated power electronics. Analysis suggests that investments in infrastructure development and the push for sustainable energy solutions are pivotal in shaping the market landscape in these regions.

Latin American countries are increasingly recognizing the importance of power electronics in improving energy efficiency and supporting industrial applications. A notable trend is the integration of power electronics in renewable energy projects and the modernization of power infrastructure. The market trends also indicates that economic development and the pursuit of sustainable energy solutions are key factors influencing the market in this region.

Top Key Players and Market Share Insights:

The Power Electronics market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Power Electronics market. Key players in the Power Electronics industry include -

- Infineon Technologies AG (Germany)

- ON Semiconductor Corporation (USA)

- NXP Semiconductors N.V. (Netherlands)

- Renesas Electronics Corporation (Japan)

- Toshiba Corporation (Japan)

- STMicroelectronics N.V. (Switzerland)

- Mitsubishi Electric Corporation (Japan)

- Vishay Intertechnology, Inc. (USA)

- Fuji Electric Co., Ltd. (Japan)

- Texas Instruments Incorporated (USA)

Recent Industry Developments :

Product Launches:

- In January 2025, Turntide Technologies has launched its latest power electronics and axial flux motors to support India’s growing EV market. The Gen 4, 5, and 6 series of inverters offer scalable, high-efficiency solutions for two-wheelers, three-wheelers, and hybrid vehicles. Engineered in the UK and locally manufactured at Kaynes Technology in Mysuru, these innovations align with the "Make in India" initiative.

Partnerships & Collaborations:

- In November 2024, Valeo and ROHM Semiconductor collaborated to co-develop next-generation power modules for electric motor inverters, integrating ROHM’s 2-in-1 Silicon Carbide (SiC) TRCDRIVE pack™. This collaboration enhances energy efficiency, thermal management, and reliability for battery electric and plug-in hybrid vehicles. Building on their partnership, the companies aim to optimize cost and performance in high-voltage inverters.

Power Electronics Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 47,406.96 Million |

| CAGR (2025-2032) | 6.1% |

| By Device Type |

|

| By Component |

|

| By Material |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Power Electronics Market? +

The Power Electronics Market size is estimated to reach over USD 47,406.96 Million by 2032 from a value of USD 29,610.66 Million in 2024 and is projected to grow by USD 30,877.45 Million in 2025, growing at a CAGR of 6.1% from 2025 to 2032.

What are the key segments in the Power Electronics Market? +

The market is segmented by device type (power discrete devices, power modules, power ICs), component (thyristors, gate turn-off transistors, MOSFETs, and others), material (silicon, silicon carbide, gallium nitride), and end-user industry (automotive, IT & telecom, energy & utilities, aerospace & defense, industrial manufacturing).

Which segment is expected to grow the fastest in the Power Electronics Market? +

The power modules segment is projected to register the fastest CAGR during the forecast period due to their higher integration and compact designs, making them ideal for high-power applications, particularly in electric vehicles and renewable energy systems.

Who are the major players in the Power Electronics Market? +

Key players in the Power Electronics market include Infineon Technologies AG (Germany), ON Semiconductor Corporation (USA), STMicroelectronics N.V. (Switzerland), Mitsubishi Electric Corporation (Japan), Vishay Intertechnology, Inc. (USA), Fuji Electric Co., Ltd. (Japan), Texas Instruments Incorporated (USA), NXP Semiconductors N.V. (Netherlands), Renesas Electronics Corporation (Japan), Toshiba Corporation (Japan).