- Summary

- Table Of Content

- Methodology

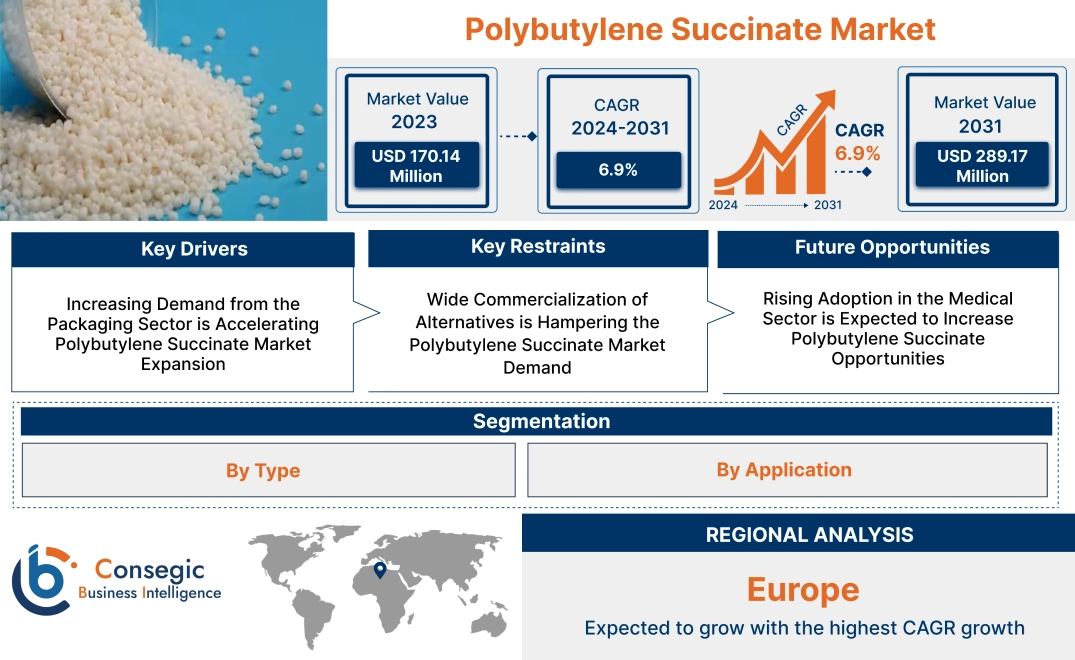

Polybutylene Succinate Market Size:

Polybutylene Succinate Market size is growing with a CAGR of 6.9% during the forecast period (2024-2031), and the market is projected to be valued at USD 289.17 Million by 2031 from USD 170.14 Million in 2023.

Polybutylene Succinate Market Scope & Overview:

Polybutylene Succinate (PBS) is a thermoplastic polyester derived from 1,4-butanediol and succinic acid. These raw materials are sourced from renewable biomass or petroleum-based feedstocks, making PBS versatile and sustainable. It is known for its eco-friendly attributes and is gaining attention as a solution to environmental concerns associated with conventional plastics. PBS exhibits excellent properties such as biodegradability, flexibility, and thermal stability, with a melting point of approximately 114°C. It is resistant to oils and greases, providing good chemical resistance. Additionally, its mechanical properties, such as tensile strength and elongation, make it suitable for various applications. Applications of PBS span multiple sectors, including packaging (e.g., food containers, bags, and films), agriculture (mulch films and plant pots), and biomedical uses (drug delivery systems and surgical sutures). It is also widely used in consumer goods such as disposable cutlery and cosmetic packaging.

Polybutylene Succinate Market Dynamics - (DRO) :

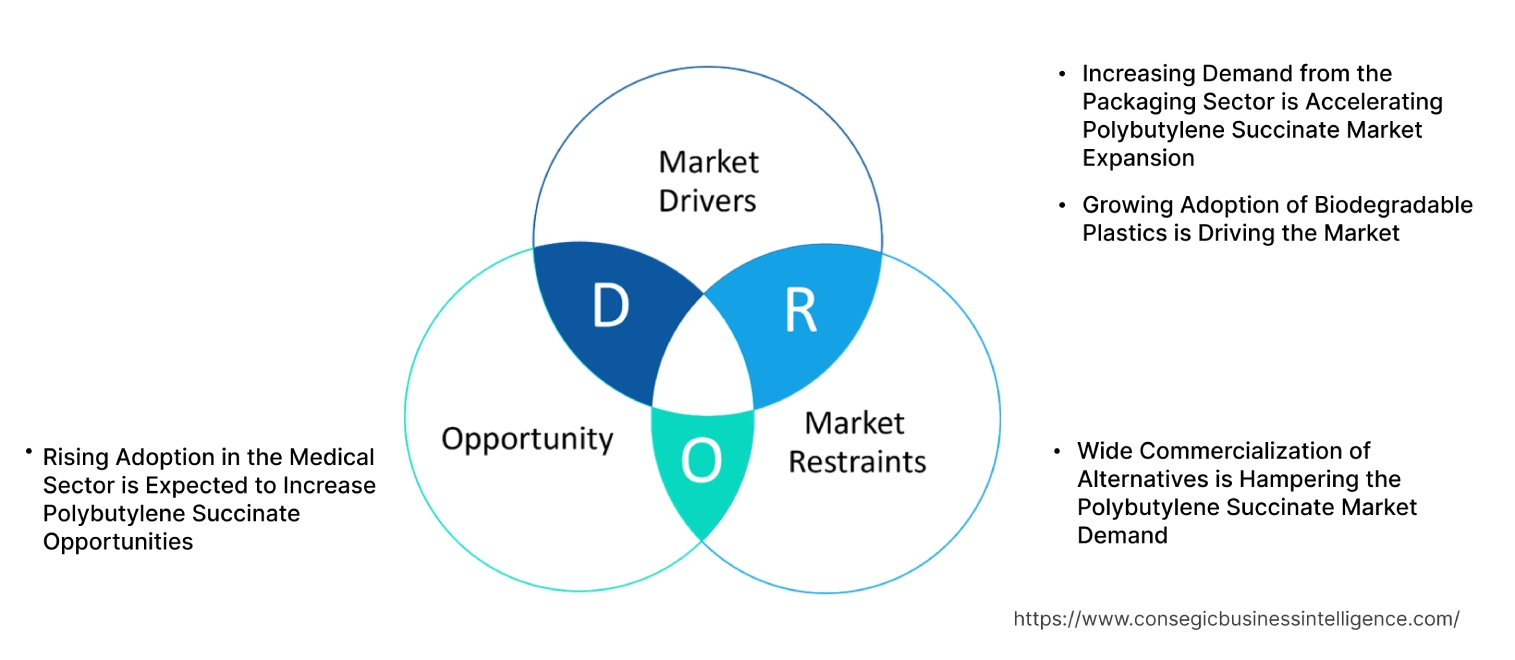

Key Drivers:

Increasing Demand from the Packaging Sector is Accelerating Polybutylene Succinate Market Expansion

The packaging sector encompasses the design, production, and distribution of materials used to enclose or protect products. In the food sector, PBS is utilized in the manufacturing of food wrapping films, storage bags, and containers. The water resistance, gas barrier qualities, and antibacterial features of PBS contribute to extending the freshness of food.

Moreover, in the cosmetic sector, PBS is utilized in manufacturing bottles, jars, and cosmetic tubes. The UV protection of PBS safeguards cosmetics from degradation. Rising disposable incomes, increasing urbanization, and changing consumer preferences towards health, wellness, and beauty have led to growth in the cosmetic and food & beverage sectors.

- For instance, according to the Bureau of Labor Statistics, in 2023, expenditure by consumers on food and non-alcoholic drinks rose by more than 12% in comparison to 2022. This includes processed foods, tetra-pack beverages, and packaged food items. This has boosted the packaging material requirements thus driving polybutylene succinate market expansion.

Overall, the growing food & beverage and cosmetic sectors, leading to increasing requirements for packaging solutions, are significantly boosting the market.

Growing Adoption of Biodegradable Plastics is Driving the Market

Biodegradable plastics are a type of plastic that is broken down by microorganisms into simpler substances such as water, carbon dioxide, and biomass. These plastics offer a sustainable alternative to traditional plastics, as they decompose naturally in the environment without leaving harmful residues.

Increasing global concern regarding plastic pollution and its detrimental impact on the environment has led to a significant focus on biodegradable plastics. Owing to this awareness consumers are seeking sustainable products and governments worldwide are imposing stricter regulations on plastic usage, including bans on single-use plastics.

- For instance, from, July 2021, The European Commission has implemented a regulation that requires all European member states to impose restrictions on specified single-use plastic (SUP) products, including plastic plates, cutlery, and straws. These policies have boosted the need for PBS, which is a biodegradable plastic, thus driving polybutylene succinate market trends.

Overall, increasing environmental concerns, stringent regulations, and growing consumer need for sustainable products are driving the market.

Key Restraints :

Wide Commercialization of Alternatives is Hampering the Polybutylene Succinate Market Demand

The market share faces significant competition from other plastics, which acts as a key restraint. Conventional plastics such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET) dominate the market due to their low cost, high availability, and established production infrastructure. These plastics are widely used in applications where PBS is still exploring.

Additionally, engineering plastics such as polycarbonate (PC) and acrylonitrile butadiene styrene (ABS) offer superior mechanical and thermal properties compared to PBS, limiting its adoption in high-performance applications. The relatively higher production cost of PBS, due to its reliance on bio-based raw materials such as succinic acid and 1,4-butanediol, makes it less economically competitive against petroleum-based alternatives.

Another factor is the slower biodegradability of PBS in specific environments compared to other bioplastics such as polylactic acid (PLA), which leads manufacturers to favor alternatives depending on regulatory or environmental pressures, further hindering polybutylene succinate market trends.

Overall, analysis shows that the competition from traditional and emerging plastics, coupled with higher production costs and slower biodegradability in certain environments is hampering the polybutylene succinate market demand.

Future Opportunities :

Rising Adoption in the Medical Sector is Expected to Increase Polybutylene Succinate Opportunities

In the medical field, PBS is commonly used in the production of disposable medical items such as surgical sutures, drug delivery systems, and wound dressings. Its high tensile strength and flexibility enable the development of sutures that provide reliable performance and gradually degrade within the body, eliminating the need for removal. Additionally, PBS-based drug delivery systems offer controlled and sustained release of medication, enhancing treatment efficacy while reducing side effects.

Furthermore, PBS is used to create medical devices such as catheters, stents, and tissue engineering scaffolds. Its biocompatibility ensures minimal tissue irritation and immune response, while its mechanical properties provide the necessary strength and flexibility for these devices. Also, many other applications are emerging and are being explored to increase PBS usage in medicine.

- For instance, according to a study published by Science Direct, in 2024, PBS supports the healing of wounds, breaks down gradually, and shows potential as a biodegradable polymer. This provides companies with the option to manufacture wound dressing pads by incorporating PBS to protect wounds, thus creating the potential for the market.

Overall, market research analysis indicates that the combination of PBS's biodegradability, biocompatibility, and customizable properties for various medical applications is expected to increase polybutylene succinate opportunities.

Polybutylene Succinate Market Segmental Analysis :

By Type:

Based on type, the market is categorized into bio-based and petroleum-based.

Trends in the Type:

- Advances in production technologies are reducing the cost of bio-based PBS.

- Growing need for Bio-based PBS due to its superior biodegradability.

The bio-based segment accounted for the largest market share in 2023, and it is expected to grow at the fastest CAGR over the forecast period.

- Bio-based PBS is a biodegradable and renewable polymer derived from natural feedstock such as sugarcane, corn, or other biomass sources. It offers an alternative to traditional plastics. Its production relies on renewable resources, reducing dependence on fossil fuels.

- It is broken down by microorganisms into water, carbon dioxide, and biomass, reducing environmental pollution. Moreover, it meets stringent environmental standards, making it suitable for eco-conscious markets.

- For instance, in December 2023, plant-based compostable polymer BioPBS from Mitsubishi Chemical Group received marine biodegradability certification from the Japan Bioplastics Association. This way bio-based PBS contributes to lower greenhouse gas emissions.

- Additionally, it exhibits good mechanical strength, heat resistance, and processability, making it suitable for various applications including packaging, agriculture, and medical devices.

- Growing awareness of plastic pollution and its detrimental impact on the environment is driving the adoption of sustainable and biodegradable materials such as bio-based PBS.

- Overall, the increasing environmental concerns, coupled with the unique properties and sustainability benefits of bio-based PBS, are driving its adoption across various sectors, thus driving segmental inpolybutylene succinate market growth.

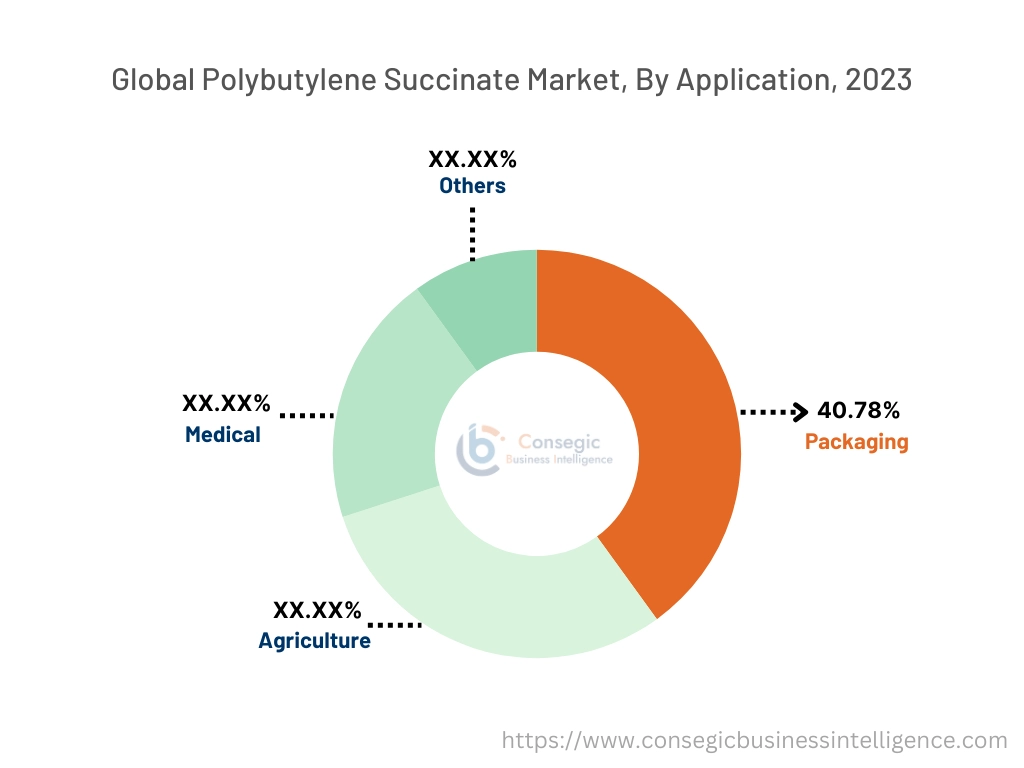

By Application:

The application segment is categorized into packaging, agriculture, medical, and others.

Trends in the Application:

- Increasingly used in food packaging due to its biodegradability and ability to maintain product freshness.

- PBS is being adopted for cosmetics packaging to reduce plastic waste and enhance brand sustainability.

The packaging segment accounted for the largest market share of 40.78% in 2023.

- PBS is a biodegradable plastic frequently used in packaging applications due to its environmentally friendly nature, as it breaks down naturally under the right conditions, making it a sustainable alternative to traditional plastics.

- It is used as a substitute for traditional plastics. PBS possesses water resistance, gas barrier properties, and antibacterial properties, helping to preserve and protect products. In food packaging, PBS is used to produce food wrapping films, storage bags, and containers, extending the freshness of food.

- Additionally, PBS finds applications in medical packaging for items such as medication pouches. In cosmetics packaging, PBS is used to create bottles, jars, and tubes. Global consumer spending on cosmetics has increased.

- For instance, according to an article published in Retail Dive, in 2024, a publication that provides news, sales of prestige beauty products in the U.S. increased by 8% compared to the previous year, reaching USD 15.3 billion in the first half of this year. This has influenced the PBS market, as it is used in packaging for cosmetics and personal care products.

- Overall, according to the market research analysis, increasing requirements from food, medical, and cosmetic packaging are driving the segment in the polybutylene succinate

The agriculture segment is expected to grow at the fastest CAGR over the forecast period.

- Derived from renewable resources, PBS is used in producing mulch films, seedling trays, and plant pots. These products decompose naturally into non-toxic byproducts, reducing environmental pollution compared to conventional plastics.

- In agriculture, PBS films help retain soil moisture, suppress weeds, and regulate soil temperature while degrading after the crop cycle, eliminating the need for removal and disposal. Seedling trays and plant pots made by PBS offer similar advantages, breaking down naturally after transplantation and enhancing soil health.

- The polymer's strength, flexibility, and compatibility with additives enable customization for specific agricultural needs. Additionally, PBS aligns with global efforts to adopt sustainable farming practices and meet regulatory standards for reducing plastic waste, making it a critical material for the future of eco-conscious agriculture.

- As per the market research analysis, in the polybutylene succinate market growth, the segment for the upcoming years is driven by increasing global population, rising income levels, changing dietary preferences, advancements in agricultural technology, climate change, and government policies supporting sustainable agriculture.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

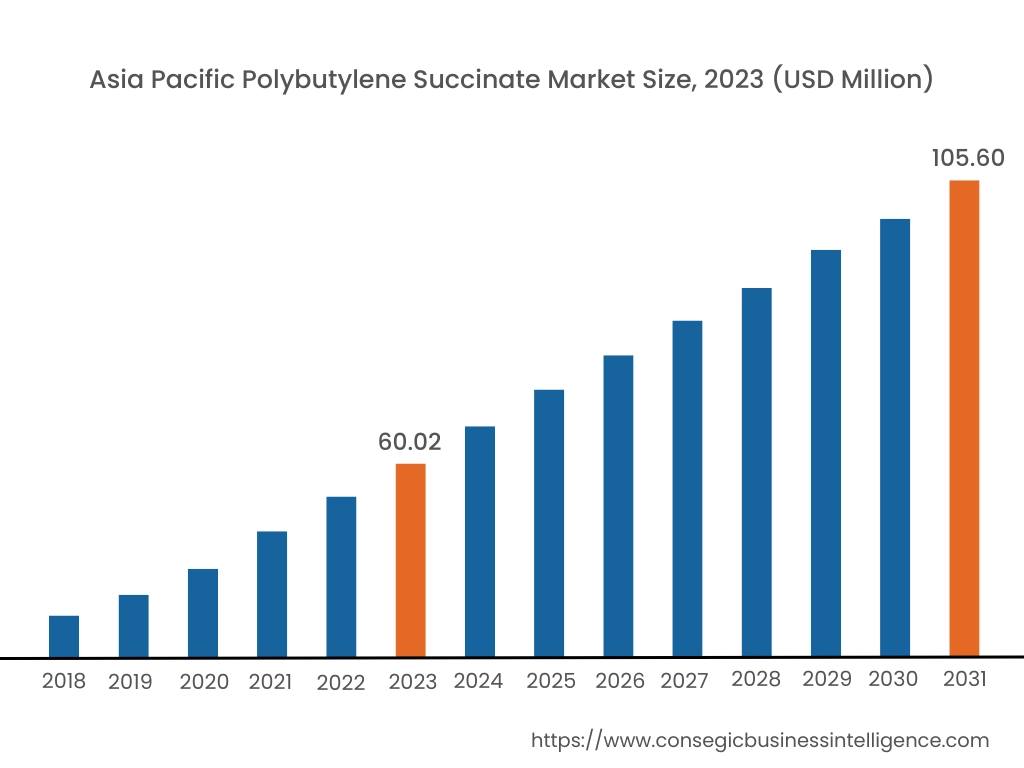

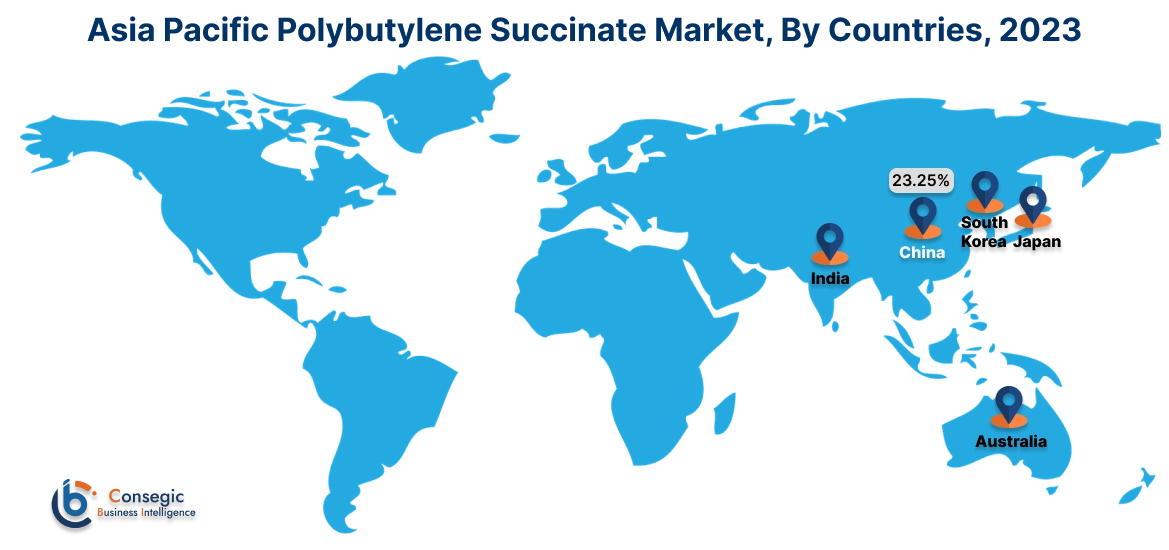

In 2023, Asia Pacific accounted for the highest polybutylene succinate market share at 36.45% and was valued at USD 62.02 Million and is expected to reach USD 105.60 Million in 2031. In Asia Pacific, China accounted for the highest polybutylene succinate market share of 23.25% during the base year of 2023. The dominance is driven by several key trends. The region's robust economic growth has led to increased consumer spending and industrialization, which is driving the requirements for packaging.

- For instance, according to an article published by Packaging Gateway, a company specializing in packaging and labeling. There was a notable 2.2% rise in primary packaging materials from January to October in Japan when compared to the corresponding timeframe of the prior year. PBS is used in primary packaging for food and cosmetics, offering sustainable alternatives to traditional plastics. This has influenced the adoption of polybutylene succinate.

Additionally, APAC's dominance is driven by the region's extensive infrastructure and cost-effective production, supported by key economies such as China, Japan, and South Korea. Moreover, many countries have implemented supportive policies and regulations to promote the use of biodegradable plastics, influencing the market positively. Furthermore, APAC's rapidly expanding food and beverage sector creates a significant need for biodegradable packaging solutions, one of PBS's primary applications. Also, the availability of raw materials, such as succinic acid, and advancements in PBS production technologies enhance the region's competitive edge. Overall, the combination of strong economic growth, supportive government policies, increasing consumer requirements, and favorable production conditions has solidified APAC's dominant position in the global PBS market.

In Europe, the polybutylene succinate market is experiencing the fastest growth with a CAGR of 7.3% over the forecast period. The market is driven by several trends. Europe has implemented stringent regulations on plastic usage, particularly single-use plastics, to address environmental concerns. This has led to increased demand for biodegradable and sustainable alternatives such as PBS. Moreover, European consumers and businesses are increasingly prioritizing sustainability and eco-friendly practices. This shift in consumer preferences is driving the adoption of PBS in various applications. Additionally, Europe has a strong research and development infrastructure, leading to advancements in PBS technology and the development of innovative applications. Furthermore, Europe's well-established recycling infrastructure facilitates the collection and recycling of PBS-based products, further promoting its adoption.

North American polybutylene succinate market analysis states several trends are responsible for the progress of the market in the region. North America is a hub for innovation and technological advancements. This has led to the development of new PBS-based products and applications, such as advanced packaging solutions and medical devices. Moreover, the region's well-established infrastructure, including strong logistics and distribution networks, facilitates the commercialization of PBS-based products. Additionally, government initiatives and policies aimed at promoting sustainable materials are further driving the growth of the PBS market in North America. Furthermore, governments and private sectors are prioritizing advanced waste management practices, creating potential for PBS as an alternative to non-degradable plastics.

The Middle East and Africa (MEA) polybutylene succinate market analysis states that this region is also witnessing a notable surge. Trends such as the region’s focus on modernizing agriculture create demand for biodegradable mulch films, where PBS plays a vital role. Moreover, with urbanization and rising consumerism, packaging solutions are gaining traction in MEA. Although PBS production is nascent in the MEA, international collaborations and investments are expanding access to biodegradable plastics. Additionally, increasing awareness of plastic pollution has led to bans on single-use plastics in countries such as Kenya and UAE, opening markets for PBS. However, challenges such as a lack of awareness about biodegradable plastics and limited infrastructure for recycling hinder the market.

Latin American polybutylene succinate market size is also emerging. The region’s food export sector is adopting PBS for sustainable packaging solutions to comply with international environmental standards. Moreover, Latin America’s large agricultural sector is driving the demand for PBS-based biodegradable films, reducing plastic waste in farming. Additionally, countries like Brazil and Chile are introducing policies to curb plastic waste, creating a favorable environment for PBS adoption. Furthermore, Latin America’s rich availability of biomass, a raw material for PBS, creates potential for regional manufacturing. Also, growing environmental consciousness among consumers in urban areas supports the demand for biodegradable plastics in various applications, including textiles and disposable products.

Polybutylene Succinate Market Competitive Landscape:

The polybutylene succinate market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global polybutylene succinate market. Key players in the polybutylene succinate industry include-

- Mitsubishi Chemical Group (Japan)

- Vizag Chemicals (India)

- Shandong Landian Biotechnology Co., Ltd (China)

- Xinjiang Blue Ridge Tunhe Polyester Co., Ltd (China)

- Hangzhou Tiankai Enterprise Co., Ltd. (China)

- Hengli Group Co., Ltd. (China)

- Hangzhou Peijin Chemical Co., Ltd. (China)

- Corvay Specialty Chemicals GmbH (Germany)

- Hefei TNJ Chemical Co., Ltd. (China)

- Unilong Co., Ltd. (China)

Polybutylene Succinate Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 289.17 Million |

| CAGR (2024-2031) | 6.9% |

| By Type |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Polybutylene Succinate market? +

In 2023, the Polybutylene Succinate market is USD 170.14 Million.

Which is the fastest-growing region in the Polybutylene Succinate market? +

Europe is the fastest-growing region in the Polybutylene Succinate market.

What specific segmentation details are covered in the Polybutylene Succinate market? +

Type and Application segmentation details are covered in the Polybutylene Succinate market

Who are the major players in the Polybutylene Succinate market? +

Mitsubishi Chemical Group (Japan), Vizag Chemicals (India), Hengli Group Co., Ltd. (China), Hangzhou Peijin Chemical Co., Ltd. (China), Corvay Specialty Chemicals GmbH (Germany), Hefei TNJ Chemical Co., Ltd. (China), Unilong Co., Ltd. (China), Shandong Landian Biotechnology Co., Ltd (China), Xinjiang Blue Ridge Tunhe Polyester Co., Ltd (China), and Hangzhou Tiankai Enterprise Co., Ltd. (China)