- Summary

- Table Of Content

- Methodology

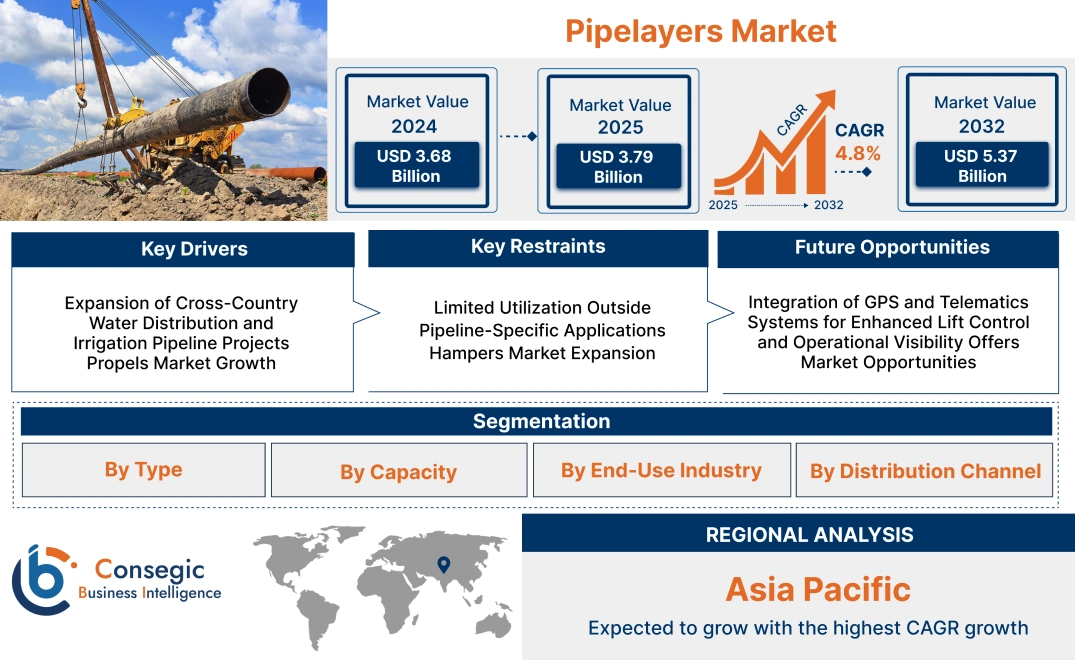

Pipelayers Market Size:

Pipelayers Market size is estimated to reach over USD 5.37 Billion by 2032 from a value of USD 3.68 Billion in 2024 and is projected to grow by USD 3.79 Billion in 2025, growing at a CAGR of 4.8% from 2025 to 2032.

Pipelayers Market Scope & Overview:

Pipelayers are specialized tracked machines engineered to lift, align, and lay large-diameter pipes during the construction of oil, gas, and water pipeline infrastructure. Equipped with side booms, counterweights, and load control systems, they are designed for heavy-duty handling of pipe sections in off-road and sloped terrains.

These machines offer high lifting capacities, 360-degree load visibility, and precise maneuverability, making them suitable for demanding job site conditions. Advanced models feature hydraulically operated winches, load moment indicators, and integrated safety systems for controlled lifting and placement.

Pipelayers enhance operational efficiency by enabling simultaneous pipe positioning and welding preparation with minimal manual handling. Their rugged construction and compatibility with different pipe sizes make them essential assets for pipeline contractors working in both remote and urban environments. The ability to maintain balance under uneven ground conditions contributes to project safety, speed, and reduced downtime in pipeline installation workflows.

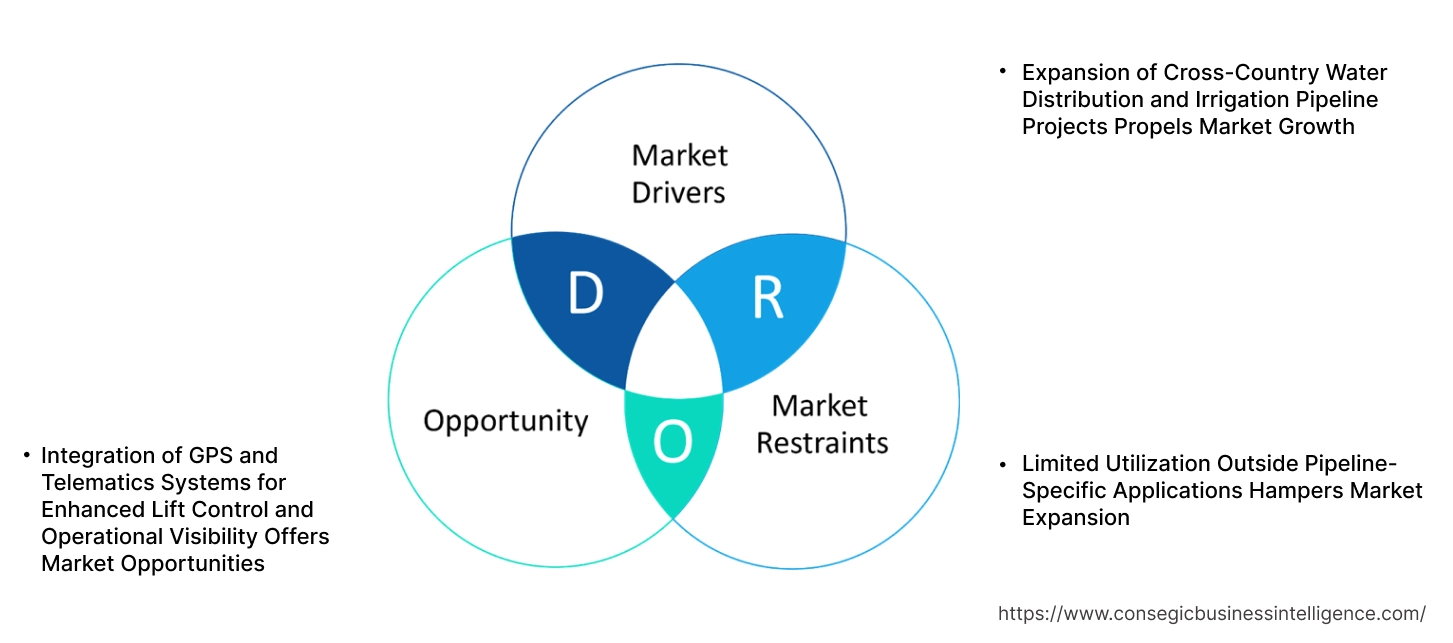

Pipelayers Market Dynamics - (DRO) :

Key Drivers:

Expansion of Cross-Country Water Distribution and Irrigation Pipeline Projects Propels Market Growth

Large-scale irrigation initiatives and cross-regional water transport programs are driving the deployment of heavy-duty pipelaying equipment across developing nations. Governments in Asia-Pacific, the Middle East, and Africa are investing in water infrastructure to address agricultural needs, mitigate drought impact, and improve access to potable water. These projects often involve long-distance trenching and installation of large-diameter pipelines across challenging terrains. Pipelayers are preferred in such operations due to their lifting stability, extended reach, and ability to maneuver on slopes or uneven ground. Their role is crucial in placing and aligning pipeline sections accurately and efficiently under tight project schedules. With climate resilience, rural development, and agricultural sustainability becoming national priorities, demand for durable and high-capacity pipelaying equipment is growing steadily. This surge in hydraulic infrastructure development is expected to fuel long-term pipelayers market expansion.

Key Restraints:

Limited Utilization Outside Pipeline-Specific Applications Hampers Market Expansion

Pipelayers are highly specialized machines designed primarily for lifting, aligning, and placing large-diameter pipes in trenching projects. Unlike general-purpose lifting equipment, they lack versatility in non-pipeline-related construction activities. Their dedicated function reduces utilization rates across diversified job sites, which limits their appeal to rental fleets and smaller contractors. For many operators, investing in multipurpose machinery offers greater return on capital, especially in markets with fluctuating pipeline activity. This restricted use-case scenario slows equipment turnover and reduces overall fleet expansion. Additionally, in urban or compact job sites, contractors often opt for cranes or excavators with pipelaying attachments for added flexibility. Despite increasing demand for energy and water infrastructure, the limited cross-functional value of these machines continues to restrain pipelayers market growth in broader construction environments.

Future Opportunities :

Integration of GPS and Telematics Systems for Enhanced Lift Control and Operational Visibility Offers Market Opportunities

Modern pipeline construction increasingly relies on digital tools to improve accuracy, safety, and operational oversight. Manufacturers are now equipping pipelayers with GPS-based positioning systems and telematics platforms to monitor lift parameters, pipe alignment, and load tracking in real time. These integrations enhance operator visibility, reduce manual errors, and support faster execution in large-scale projects. Remote diagnostics and fleet management capabilities allow contractors to optimize uptime, plan preventive maintenance, and manage multiple units across dispersed locations. As demand rises for productivity-focused equipment, digitally enabled ones offer a compelling value proposition. Additionally, the ability to log and document lift operations improves compliance with safety regulations and project reporting requirements.

- For instance, in December 2020, John Deere launched the 700L PL40 Pipelayer Machine with greater hydraulic power and added controls like Eco Mode, Auto Idle, and Auto Shutdown. Furthermore, the machines are equipped with JDLink telematics for five years in base.

These advancements in machine intelligence and connectivity are unlocking pipelayers market opportunities driven by growth in smart construction and infrastructure digitalization.

Pipelayers Market Segmental Analysis :

By Type:

Based on type, the market is divided into general and multifunctional pipelayers.

The general segment accounted for the largest pipelayers market share in 2024.

- The general ones are typically used for basic pipeline construction tasks, such as lifting and placing pipes in various environments.

- These machines are reliable, cost-effective, and widely adopted in standard oil & gas, construction, and mining projects.

- They provide strong stability and load handling, making them ideal for simpler, large-scale pipeline laying projects.

- As per the pipelayers market analysis, the segment remains dominant due to its wide applicability and robust performance in conventional pipeline projects.

The multifunctional segment is projected to grow at the fastest CAGR during the forecast period.

- Multifunctional versions offer additional capabilities beyond pipe handling, including lifting, moving, and assembling heavy components.

- These advanced machines are particularly useful in complex pipeline projects in remote or difficult-to-reach areas, where versatility is crucial.

- With the increasing need for sophisticated machinery in large-scale infrastructure projects, multifunctional models are seeing higher adoption.

- According to pipelayers market trends, the segment's growth is driven by the demand for higher efficiency, multi-tasking, and advanced technical features in modern construction and energy projects.

By Capacity:

Based on capacity, the pipelayers market is segmented into below 100 tons, 100–300 tons, and above 300 tons.

The 100–300 tons segment held the largest revenue share in 2024.

- Models with a capacity of 100–300 tons are widely used in medium to large-scale construction, oil & gas, and utility projects.

- These machines are versatile, offering the right balance of lifting capacity and operational flexibility for diverse pipeline projects.

- The 100–300 tons range is preferred in situations where high capacity is required but the equipment size needs to remain manageable for urban and site-specific constraints.

- As per pipelayers market analysis, this segment is dominant due to its applicability across a wide range of industries, including oil & gas, mining, and construction.

The above 300 tons segment is projected to experience the fastest CAGR during the forecast period.

- Machines with capacities above 300 tons are typically used in large-scale infrastructure and energy projects, including deepwater oil extraction and large pipeline installations.

- These machines are required in demanding environments, such as offshore platforms, remote areas, or large construction zones where high lifting capacity is critical.

- Increasing investments in oil & gas exploration and major infrastructure development projects are expected to drive the requirement.

- According to pipelayers market trends, the need for high-capacity machines is expected to surge as large-scale energy and infrastructure projects grow globally.

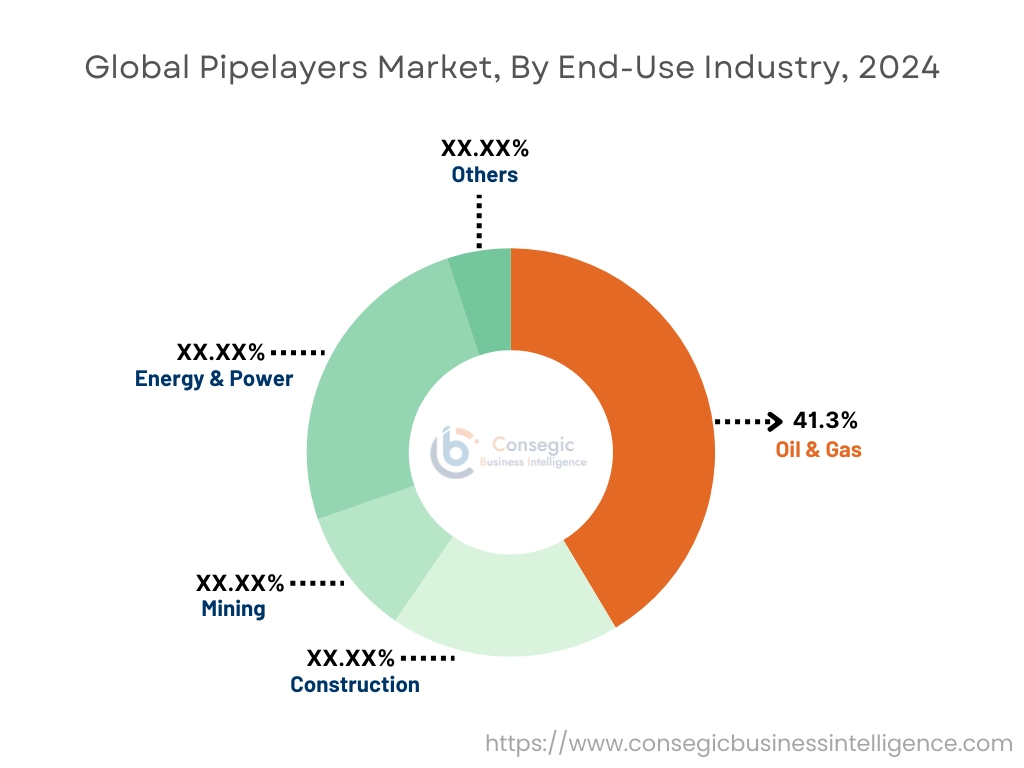

By End-Use Industry:

Based on end-use industry, the market is segmented into energy & power, oil & gas, construction, mining, and others.

The oil & gas segment accounted for the largest pipelayers market share of 41.3% in 2024.

- The oil & gas sector remains the primary end-user of pipelayers, as pipeline construction, maintenance, and expansion are critical to energy production.

- They are heavily utilized in upstream and midstream oil & gas projects, including pipeline transportation systems and infrastructure maintenance.

- As global oil exploration and pipeline development increase, the need for reliable, high-capacity machines continues to rise.

- Thus, the oil & gas segment continues to dominate due to the persistent need for infrastructure expansion and maintenance in the energy sector, driving pipelayers market growth.

The construction segment is expected to grow at the fastest CAGR during the forecast period.

- In addition to pipeline laying, pipelayers are used in construction projects for moving and positioning heavy materials in trenching and deep excavation.

- The rising need for new urban infrastructure, especially in emerging economies, is fueling its adoption in construction.

- As cities expand and industrial projects increase, they are becoming a key part of the machinery lineup for major construction projects.

- Hence, the construction sector is expected to see the fastest growth due to the increased need for machinery in large-scale urban projects and infrastructure development, bolstering pipelayers market expansion.

By Distribution Channel:

Based on distribution channel, the market is segmented into OEMs, aftermarket, online retail, and dealers & distributors.

The OEM segment accounted for the largest revenue share in 2024.

- Original Equipment Manufacturers (OEMs) supply them directly to large construction and energy companies, ensuring compatibility with complex projects and machinery fleets.

- OEMs provide product warranties, customized solutions, and after-sales services, fostering long-term customer relationships.

- The segment benefits from the increasing complexity of modern projects and the requirement for specific, high-performance machines designed for particular applications.

- As per pipelayers market demand, OEMs remain the dominant distribution channel due to their ability to deliver highly specialized equipment for large-scale and high-capacity projects.

The dealers & distributors segment is expected to witness the fastest CAGR during the forecast period.

- Dealers and distributors play a crucial role in ensuring their availability to a wide range of end users, including small and medium-sized companies.

- This channel offers more flexible financing options, extended warranties, and local service agreements, making it attractive for companies in emerging markets.

- Additionally, the presence of local dealers facilitates timely deliveries and after-sales support, which is essential for maintaining operational efficiency.

- According to segmental trends, the growth of this segment is fueled by the expansion of small to mid-sized projects in developing economies.

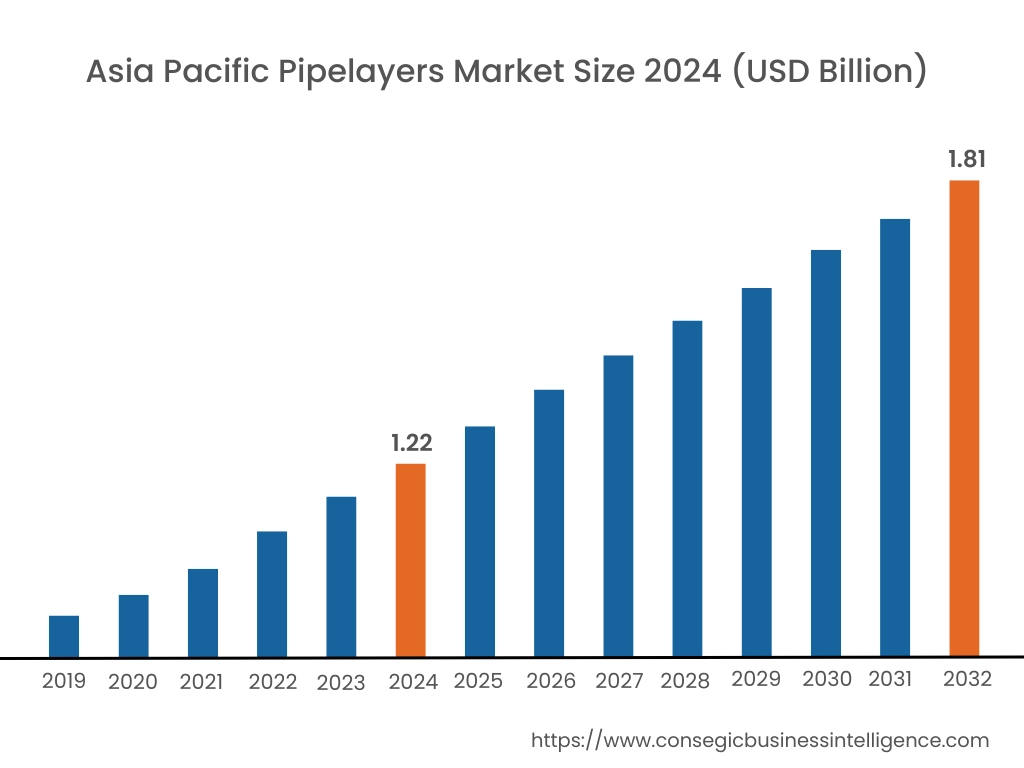

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

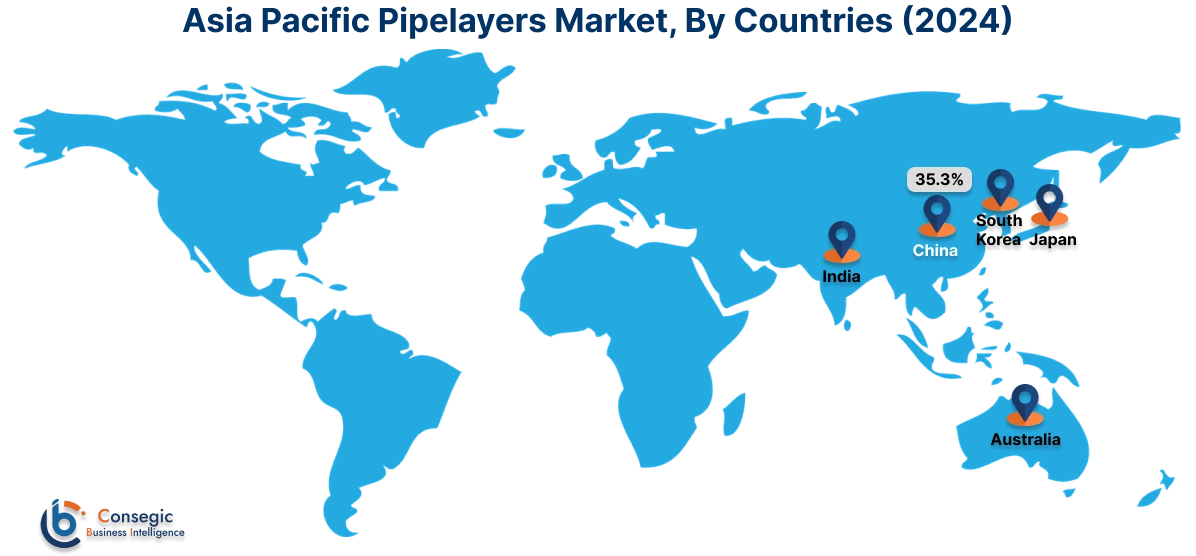

Asia Pacific region was valued at USD 1.22 Billion in 2024. Moreover, it is projected to grow by USD 1.26 Billion in 2025 and reach over USD 1.81 Billion by 2032. Out of this, China accounted for the maximum revenue share of 35.3%. Asia-Pacific is experiencing rapid growth in the pipelayers industry, driven by extensive urbanization, expansion of natural gas infrastructure, and large-scale water distribution projects. China, India, and Australia are key contributors to the market demand, as governments invest in new pipeline corridors for energy and water access in underserved regions. Market analysis indicates high utilization in cross-country pipeline installations and growing procurement of high-capacity vehicles suitable for varied terrain. Technological advancement in control systems and operator comfort is becoming more prominent as the want increases. The region’s infrastructure boom and the diversification of energy supply chains continue to underpin sustained market expansion.

North America is estimated to reach over USD 1.58 Billion by 2032 from a value of USD 1.08 Billion in 2024 and is projected to grow by USD 1.11 Billion in 2025. In North America, they are widely utilized in both transmission and distribution segments of oil, gas, and water networks. The United States and Canada have established markets where the focus is shifting toward upgrading aging pipeline infrastructure and deploying new routes to support domestic energy production. Market analysis highlights a growing preference for technologically advanced machines with GPS-based control systems, improved safety features, and emissions-compliant engines. The need for these machines is reinforced by major pipeline replacement programs and increased scrutiny on pipeline integrity and environmental impact, especially in densely populated or ecologically sensitive zones.

Europe presents a highly regulated market, where pipelayers are predominantly used in the energy transport sector and municipal water projects. Countries such as Germany, the UK, and Norway are investing in underground pipeline upgrades to support cleaner fuel transitions, including hydrogen-ready infrastructure. Market analysis shows the need for compact design, maneuverability in tight urban corridors, and enhanced load stability. In addition, electrification and hybridization trends are shaping equipment specifications. Furthermore, current efforts in Europe are focused on modernizing outdated pipeline systems, meeting decarbonization targets, and supporting regional energy security initiatives through resilient pipeline networks.

Latin America is demonstrating growing pipelayers market demand, particularly in Brazil, Mexico, and Argentina, where oilfield development and pipeline rehabilitation projects are progressing. Market analysis suggests that contractors prioritize equipment with strong lifting capabilities and operational stability on uneven ground. The region also faces rising requirement for rural water pipelines and sanitation infrastructure in expanding urban peripheries. Opportunities are emerging as governments partner with private entities to boost capacity in energy transport and water management systems. Growth is supported by regional policy shifts toward infrastructure self-sufficiency and increased allocation of public resources for long-term capital projects.

The Middle East and Africa present a high-potential landscape for pipelayers, fueled by oil and gas exploration, transnational pipeline construction, and water delivery initiatives in arid zones. In the Gulf region, they are deployed in petrochemical complexes and new energy corridors, while in countries like South Africa and Egypt, water conveyance projects drive utilization. Market analysis points to increasing need for durable, serviceable units that can withstand extreme climate and remote operation challenges. The pipelayers market opportunity in this region lies in expanding local manufacturing support, streamlining import logistics, and delivering specialized solutions for infrastructure projects tied to national development goals.

Top Key Players and Market Share Insights:

The pipelayers market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global pipelayers market. Key players in the pipelayers industry include -

- Komatsu Ltd. (Japan)

- Volvo Construction Equipment (Sweden)

- Hitachi Construction Machinery Co., Ltd. (Japan)

- CNH Industrial (Case Construction Equipment) (United Kingdom)

- Hydrema A/S (Denmark)

- XCMG Group (China)

- SANY Group (China)

- Liebherr Group (Germany)

- Zoomlion Heavy Industry Science & Technology Co., Ltd. (China)

- Doosan Infracore (South Korea)

Recent Industry Developments :

Acquisitions:

- In April 2023, Borusan Mannesmann acquired Berg Pipe in the United States, strengthening its presence in the global market.

Pipelayers Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 5.37 Billion |

| CAGR (2025-2032) | 4.8% |

| By Type |

|

| By Capacity |

|

| By End-Use Industry |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Pipelayers Market? +

Pipelayers Market size is estimated to reach over USD 5.37 Billion by 2032 from a value of USD 3.68 Billion in 2024 and is projected to grow by USD 3.79 Billion in 2025, growing at a CAGR of 4.8% from 2025 to 2032.

What specific segmentation details are covered in the Pipelayers Market report? +

The Pipelayers market report includes specific segmentation details for type, capacity, end-use industry and distribution channel.

What are the end-use industries of the Pipelayers Market? +

The end-use industries of the Pipelayers Market are energy & power, oil & gas, construction, mining, and others.

Who are the major players in the Pipelayers Market? +

The key participants in the Pipelayers market are Komatsu Ltd. (Japan), Volvo Construction Equipment (Sweden), XCMG Group (China), SANY Group (China), Liebherr Group (Germany), Zoomlion Heavy Industry Science & Technology Co., Ltd. (China), Doosan Infracore (South Korea), Hitachi Construction Machinery Co., Ltd. (Japan), CNH Industrial (Case Construction Equipment) (United Kingdom) and Hydrema A/S (Denmark).