- Summary

- Table Of Content

- Methodology

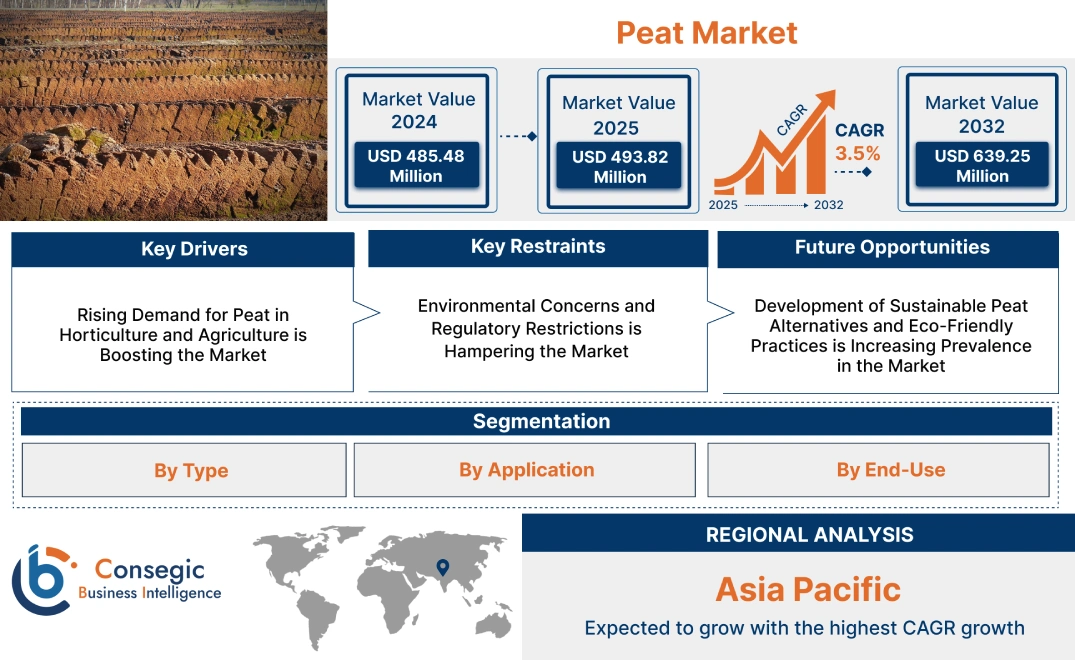

Peat Market Size:

Peat Market size is estimated to reach over USD 639.25 Million by 2032 from a value of USD 485.48 Million in 2024 and is projected to grow by USD 493.82 Million in 2025, growing at a CAGR of 3.5% from 2025 to 2032.

Peat Market Scope & Overview:

The peat is an organic material formed from partially decayed plant matter in waterlogged environments. Peat is widely used in agriculture, horticulture, energy generation, and environmental management due to its ability to retain moisture and nutrients. The market includes various types of peat, such as sphagnum peat moss, sedge peat, and woody peat, tailored for specific applications like soil amendments, growing media, and bioenergy.

Key characteristics of peat include high water-holding capacity, nutrient content, and acidic pH, making it a valuable resource for improving soil quality and plant growth. The benefits include enhanced crop yields, better water retention in soils, and its use as a renewable energy source in some regions.

Applications span horticulture (potting soils and garden amendments), agriculture (soil conditioners), energy (peat-fired power plants), and water treatment (pollutant filtration). End-users include farmers, gardeners, energy producers, and environmental agencies, driven by increasing peat market opportunities for sustainable agricultural practices, rising adoption of peat-based growing media, and expanding use of peat in ecological restoration projects.

Peat Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Peat in Horticulture and Agriculture is Boosting the Market

The growing peat market trends for peat in horticulture and agriculture are a significant driver for the market. Peat, known for its high water retention capacity, aeration properties, and ability to enhance soil fertility, is widely used as a soil conditioner and growing medium in nurseries, greenhouses, and landscaping. It is particularly valued in cultivating flowers, vegetables, and fruits, as it provides an ideal root environment. The increasing adoption of peat in sustainable and organic farming practices further supports market growth, as it is often used in organic compost production to improve soil health. The expansion of commercial agriculture and the growing popularity of home gardening, especially in urban areas, have fueled the trends for peat-based products.

Key Restraints:

Environmental Concerns and Regulatory Restrictions is Hampering the Market

The peat market faces significant challenges due to environmental concerns and stringent regulatory restrictions. Peat extraction is associated with ecological degradation, including habitat destruction and greenhouse gas emissions, as peatlands are important carbon sinks. Governments and environmental organizations are imposing stricter regulations on peat harvesting to protect natural ecosystems and mitigate climate change impacts. For example, several European countries have implemented policies to limit or phase out peat extraction. These restrictions, along with the rising awareness of sustainable alternatives, are compelling manufacturers and end-users to explore eco-friendly substitutes, which may limit peat market growth.

Future Opportunities :

Development of Sustainable Peat Alternatives and Eco-Friendly Practices is Increasing Prevalence in the Market

The development of sustainable alternatives and eco-friendly practices in peat extraction presents significant growth opportunities for the market. Innovations in substitute products, such as coir, wood fiber, and compost-based growing mediums, are gaining traction among environmentally conscious consumers and industries. Additionally, advancements in sustainable peat harvesting techniques, including reduced-impact extraction and restoration of peatlands post-harvest, are helping balance ecological preservation with peat market demands. The rising interest in carbon-neutral agricultural practices and the promotion of sustainable horticulture by governments and NGOs further support the development of eco-friendly peat products and alternatives.

These dynamics highlight the growing importance of peat in agriculture and horticulture while emphasizing the need to address environmental concerns. By adopting sustainable practices and developing innovative alternatives, the market can achieve long-term progress while aligning with global sustainability goals.

Peat Market Segmental Analysis :

By Type:

Based on type, the market is segmented into sod peat, coco peat, wood peat, and others.

The sod peat segment accounted for the largest revenue share in 2024.

- Sod peat is widely used in agriculture and horticulture due to its high water retention and nutrient absorption properties.

- Increasing demand for organic soil enhancers in sustainable farming practices supports this segment's dominance.

- Advancements in sod peat harvesting techniques improve efficiency and product availability.

- Expanding use of sod peat in landscaping and gardening enhances its market share.

The coco peat segment is anticipated to register the fastest CAGR during the forecast period.

- Coco peat, derived from coconut husks, is gaining popularity as an eco-friendly alternative to traditional peat.

- Its superior aeration and water retention capabilities make it ideal for hydroponics and modern horticultural practices.

- Increasing adoption in urban gardening and indoor plant care drives the peat market trends for coco peat.

- Rising consumer awareness about sustainable and renewable agricultural inputs boosts the segment's advancement.

By Application:

Based on application, the market is segmented into agriculture, horticulture, fuel & energy, water filtration, and others.

The agriculture segment accounted for the largest revenue share in 2024.

- Peat is widely used as a soil conditioner and organic fertilizer in agricultural practices to improve crop yield and soil quality.

- Increasing adoption of sustainable farming techniques drives demand for peat-based soil amendments.

- Rising need for water retention solutions in arid and semi-arid regions supports the use of peat in agriculture.

- Expanding global agricultural activities, particularly in emerging economies, propels trends as shown in the segmental analysis.

The water filtration segment is anticipated to register the fastest CAGR during the forecast period.

- Peat is increasingly used in water filtration systems for its natural ability to remove impurities and improve water quality.

- Growing awareness about water conservation and purification methods supports the demand for peat in this application.

- Expanding use of peat-based filters in industrial and municipal water treatment plants boosts growth.

- Rising focus on eco-friendly water treatment solutions enhances the market for peat in filtration applications.

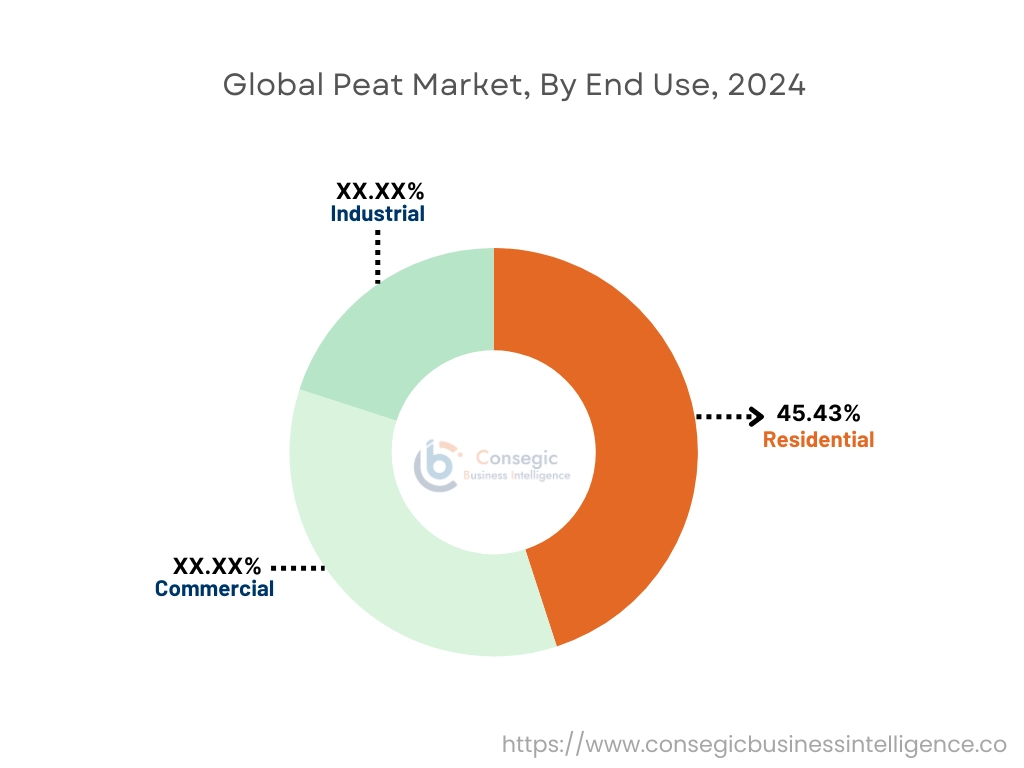

By End-Use:

Based on end-use, the market is segmented into residential, commercial, and industrial.

The residential segment accounted for the largest revenue share of 45.43% in 2024.

- Peat is extensively used in home gardening and landscaping due to its affordability and effectiveness as a soil conditioner.

- Increasing interest in indoor plants and urban gardening drives trends for peat among residential users.

- Growing consumer preference for organic gardening solutions enhances the adoption of peat in this segment.

- Expanding availability of packaged peat products tailored for residential use supports peat market growth.

The industrial segment is anticipated to register the fastest CAGR during the forecast period.

- Industrial applications, particularly in fuel & energy and water filtration, are driving demand for peat in large-scale operations.

- Increasing adoption of peat as a renewable energy source in biomass power plants supports this segment's rise.

- Expanding use of peat in industrial water treatment processes boosts its market potential.

- Rising investments in sustainable industrial practices and renewable resources propel advancement in the industrial process as shown in the segmental analysis.

Regional Analysis:

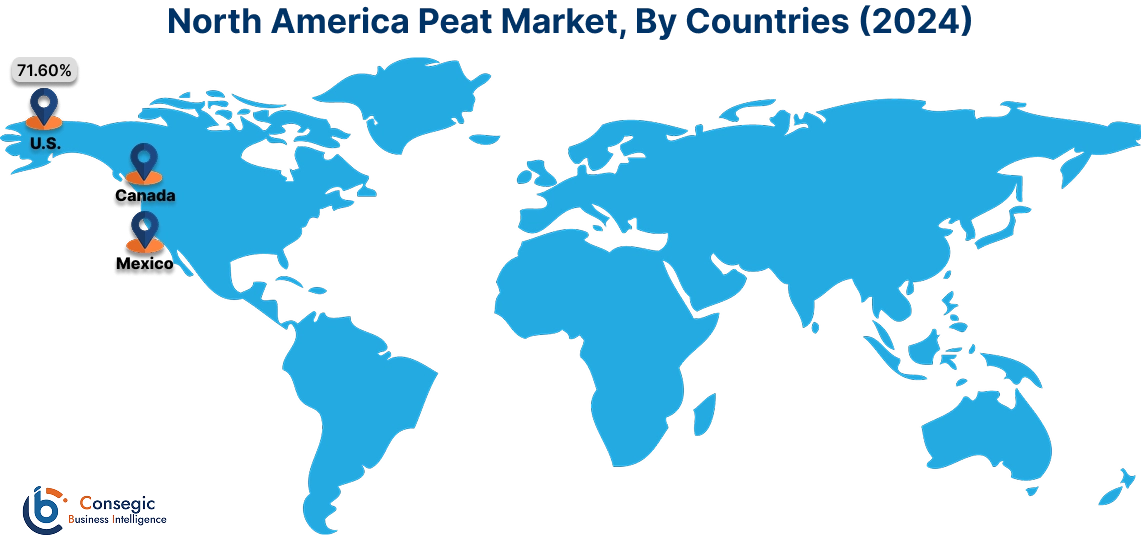

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

In 2024, North America was valued at USD 161.04 Million and is expected to reach USD 207.18 Million in 2032. In North America, the U.S. accounted for the highest share of 71.60% during the base year of 2024. North America holds a significant share in the global peat market, driven by increasing utilization in horticulture, energy generation, and water filtration applications. The U.S. leads the region due to its high trends for peat in landscaping, commercial greenhouses, and agricultural industries. Canada is a major supplier of peat, particularly sphagnum peat moss, due to its abundant natural resources and large-scale peat extraction projects. Market analysis highlights the region’s focus on sustainable peat harvesting practices to meet environmental regulations. However, growing concerns over the environmental impact of peat extraction may pose challenges to the market.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 3.9% over the forecast period. The peat market, is fueled by increasing agricultural activities, rising urbanization, and growing trends for peat in soil conditioning and substrate production in China, India, and Southeast Asia. China dominates the region with significant use of peat in greenhouse farming and organic crop production. India’s expanding agricultural sector and adoption of horticulture practices support the demand for peat as a soil enhancer. Japan focuses on advanced gardening techniques, leveraging imported peat for precision farming. However, limited domestic production and reliance on imports may challenge market expansion in some parts of the region.

Europe is a prominent market for peat, supported by its extensive use in gardening, agriculture, and energy generation. Countries like Germany, the UK, and Finland are key contributors. Germany drives trends for peat in commercial horticulture and organic farming, while the UK emphasizes peat-based soil amendments for gardening enthusiasts. The regional peat market analysis shows that Finland is a major producer, with a strong focus on using peat for bioenergy and industrial applications. Analysis reveals that stringent EU regulations on carbon emissions and sustainability are encouraging a shift toward renewable alternatives, which could impact traditional peat consumption patterns in the region.

The Middle East & Africa region is witnessing steady growth in the market, driven by the increasing adoption of peat in water filtration systems and its use in high-end landscaping projects. Countries like Saudi Arabia and the UAE are using imported peat for landscaping in urban development and hospitality projects. In Africa, South Africa is emerging as a key market, focusing on peat-based soil conditioners to improve agricultural productivity. The peat market analysis highlights challenges such as limited local production and high costs associated with peat imports, which may restrict broader adoption in the region.

Latin America is an emerging market for peat, with Brazil and Mexico leading the region. Brazil’s growing horticulture industry and rising demand for soil conditioning products drive the market for imported peat. Mexico focuses on expanding its agricultural productivity by adopting peat-based solutions for soil health improvement. The region benefits from increasing awareness about sustainable farming practices and partnerships with international peat suppliers. However, inconsistent distribution networks and economic instability in some countries may pose challenges to peat market expansion.

Top Key Players & Market Share Insights:

The peat market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global peat market. Key players in the peat industry include -

- Klasmann-Deilmann GmbH (Germany)

- Vapo Group (Finland)

- Elva E.P.T. Ltd. (Estonia)

- Torf Corporation (Poland)

- Global Peat Ltd. (Latvia)

- Premier Tech Ltd. (Canada)

- Bord na Mona (Ireland)

- Lambert Peat Moss Inc. (Canada)

- Sun Gro Horticulture (United States)

Recent Industry Developments :

Innovations:

- In September 2024, Neova Oy announced plans to enhance the availability of bedding peat in Finland. Recognizing a growing demand, the company is exploring the utilization of former energy peat production areas for bedding peat extraction. This initiative aims to repurpose existing resources to meet the increasing needs of livestock and poultry farms, ensuring a stable supply of bedding peat across the country.

Collaboration:

- In 2021, five EU transnational projects, Carbon Connects, Care-Peat, DESIRE, LIFE Peat Restore, and CANAPE, collaborated to release the "Peatlands Across Europe: Innovation and Inspiration" guide. This publication captures key recommendations, shares pioneering experiences in peatland restoration, and identifies gaps and priorities across Europe. The guide aims to inform and inspire peatland practitioners globally, emphasizing the critical role of peatlands in carbon storage, biodiversity conservation, and climate change mitigation.

Peat Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 639.25 Million |

| CAGR (2025-2032) | 3.5% |

| By Type |

|

| By Application |

|

| By End-Use |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the current and projected size of the Peat Market? +

Peat Market size is estimated to reach over USD 639.25 Million by 2032 from a value of USD 485.48 Million in 2024 and is projected to grow by USD 493.82 Million in 2025, growing at a CAGR of 3.5% from 2025 to 2032.

What are the main types of peat available in the market? +

The market is segmented into Sod Peat, Coco Peat, Wood Peat, and Others, with Sod Peat holding the largest market share in 2024.

Which type of peat is expected to grow the fastest? +

Coco Peat is anticipated to register the fastest CAGR due to its eco-friendly nature, superior aeration, and water retention properties, ideal for modern horticultural practices.

What are the primary applications of peat? +

Peat is widely used in agriculture, horticulture, fuel & energy, water filtration, and other areas, with agriculture holding the largest market share in 2024.