- Summary

- Table Of Content

- Methodology

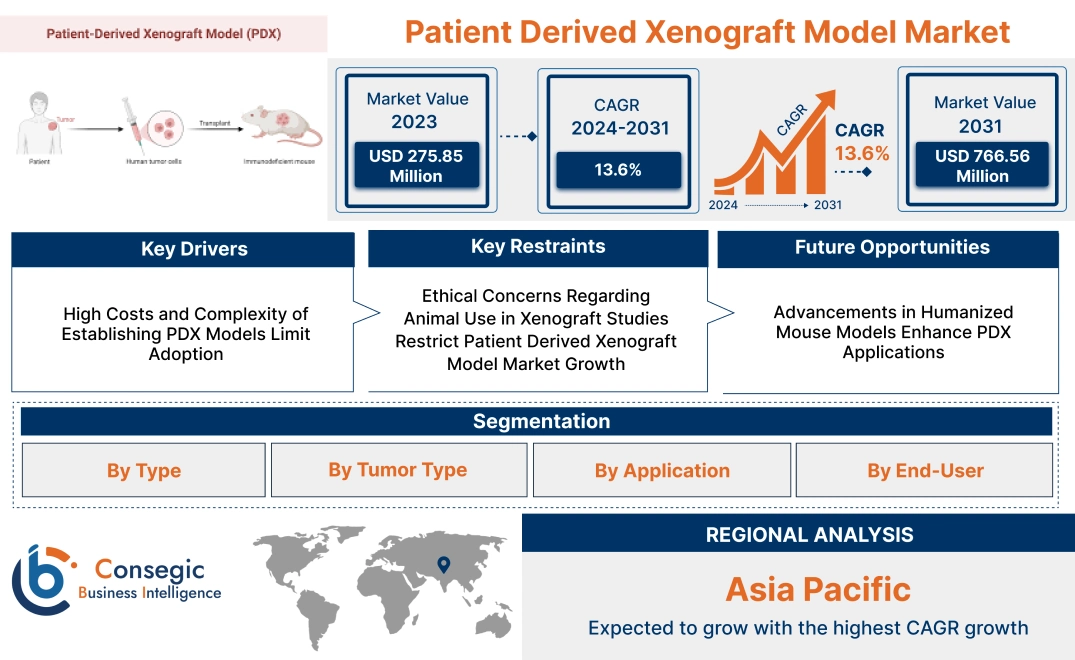

Patient Derived Xenograft Model Market Size:

Patient Derived Xenograft Model Market size is estimated to reach over USD 766.56 Million by 2031 from a value of USD 275.85 Million in 2023 and is projected to grow by USD 308.53 Million in 2024, growing at a CAGR of 13.6% from 2024 to 2031.

Patient Derived Xenograft Model Market Scope & Overview:

The patient-derived xenograft (PDX) model market focuses on advanced preclinical models created by implanting human tumor tissues into immunodeficient mice to study cancer biology and evaluate therapeutic responses. These models retain the genetic, histological, and molecular characteristics of the original patient tumors, providing a highly accurate platform for drug development and precision medicine. Key features of PDX models include their ability to mimic human tumor microenvironments, predict patient-specific responses, and support personalized treatment strategies. The benefits of PDX models are enhanced translational relevance, reduced failure rates in clinical trials, and accelerated drug discovery timelines. Applications span oncology research, drug efficacy testing, biomarker identification, and personalized medicine development. End-users include pharmaceutical companies, contract research organizations (CROs), and academic research institutions, driven by rising cancer prevalence, increasing surge for precise preclinical models, and advancements in oncology research.

Patient Derived Xenograft Model MarketDynamics - (DRO) :

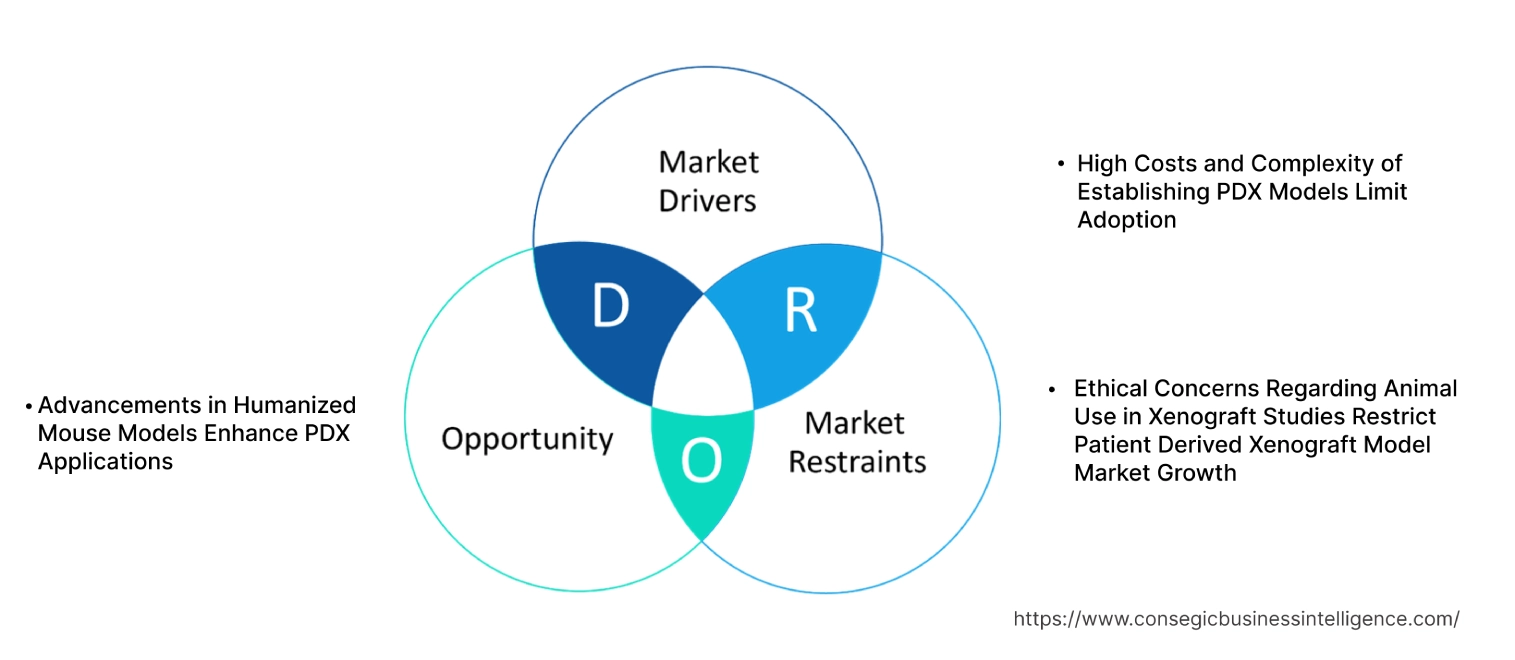

Key Drivers:

High Costs and Complexity of Establishing PDX Models Limit Adoption

The development and maintenance of Patient-Derived Xenograft (PDX) models are associated with high costs and operational complexity, creating a significant barrier to adoption, especially for smaller research institutions and laboratories. Establishing PDX models involves intricate procedures, such as sourcing patient-derived tumor tissues, ensuring ethical approval, and performing delicate implantation surgeries into immunocompromised animals. The specialized care required to maintain these models, including controlled environments, sterile conditions, and monitoring, further escalates operational expenses.

Moreover, the high cost of immunocompromised animals, such as nude or SCID mice, combined with advanced imaging and molecular patient derived xenograft model market analysis tools, makes PDX research financially demanding. Scaling up PDX models for high-throughput drug screening adds another layer of complexity, as it requires large cohorts of animals, extended timelines, and additional resources. In regions with limited research funding or infrastructure, these factors restrict the broader adoption of PDX models, limiting their use to well-funded pharmaceutical companies and research organizations.

Key Restraints :

Ethical Concerns Regarding Animal Use in Xenograft Studies Restrict Patient Derived Xenograft Model Market Growth

The use of animals in PDX research raises significant ethical concerns that act as a restraint for market expansion. Xenograft models require immunocompromised animals, such as SCID mice, which are surgically implanted with human or bovine-derived tumor tissues. Regulatory bodies like the Institutional Animal Care and Use Committee (IACUC) and European Directive 2010/63/EU impose stringent guidelines to ensure humane treatment, increasing the administrative and operational burden on researchers.

Additionally, growing public scrutiny and opposition to animal testing have led to calls for more ethical and alternative research methods. Advocacy for replacing animal-based studies with in vitro models, organoids, or computational simulations is gaining traction. As a result, some research institutions and funding bodies are shifting towards less controversial methods, potentially slowing the adoption of PDX models despite their relevance in translational research.

Future Opportunities :

Advancements in Humanized Mouse Models Enhance PDX Applications

The emergence of humanized mouse models has significantly enhanced the applicability of PDX models, creating a transformative opportunity for the market. Humanized mice are engineered to possess a functional human immune system, enabling researchers to study complex interactions between tumors and the immune microenvironment. This advancement is particularly valuable for immuno-oncology, where PDX models integrated with humanized mice allow for the evaluation of immune checkpoint inhibitors, adoptive cell therapies, and cancer vaccines in a realistic preclinical setting.

Moreover, humanized PDX models provide a robust platform for studying tumor resistance mechanisms and testing combination therapies, which are critical for addressing refractory cancers. These models are also being used to explore personalized treatment approaches, as they allow for patient-specific immune responses to be studied in vivo. The growing investment in immuno-oncology and precision medicine is expected to drive a surge for humanized PDX models, expanding their role in drug development pipelines and offering significant patient derived xenograft model market growth potential for the market.

Patient Derived Xenograft Model Market Segmental Analysis :

By Type:

Based on type, the patient derived xenograft (PDX) model market is segmented into mouse models and rat models.

The mouse models segment accounted for the largest revenue in patient derived xenograft model market share in 2023.

- Mouse models are extensively used in PDX studies due to their well-characterized genetics, ease of handling, and ability to replicate human tumor microenvironments effectively.

- Immunodeficient mice, such as NSG (NOD scid gamma) and nude mice, are commonly used for engraftment of patient-derived tumors, providing high tumor take rates and reproducibility.

- The widespread use of mouse models in oncology research, preclinical drug testing, and biomarker development supports their market dominance.

- Additionally, advancements in genetically engineered mouse models further enhance their relevance in personalized medicine research.

- Mouse models lead the market trends, driven by their effectiveness in replicating human tumor biology and their extensive use in preclinical oncology studies.

The rat models segment is anticipated to register the fastest CAGR during the forecast period.

- Rat models offer unique advantages, including larger body size and organ systems closer to human anatomy, enabling detailed physiological studies.

- These models are gaining traction in pharmacokinetics, toxicology, and specific cancer types where larger tumor volumes are required.

- The increasing adoption of humanized rat models for complex oncology and biomarker research is driving their rise.

- Rat models patient derived xenograft model market analysis are expected to grow rapidly, supported by their trends and utility in advanced physiological studies and emerging applications in biomarker and drug development research.

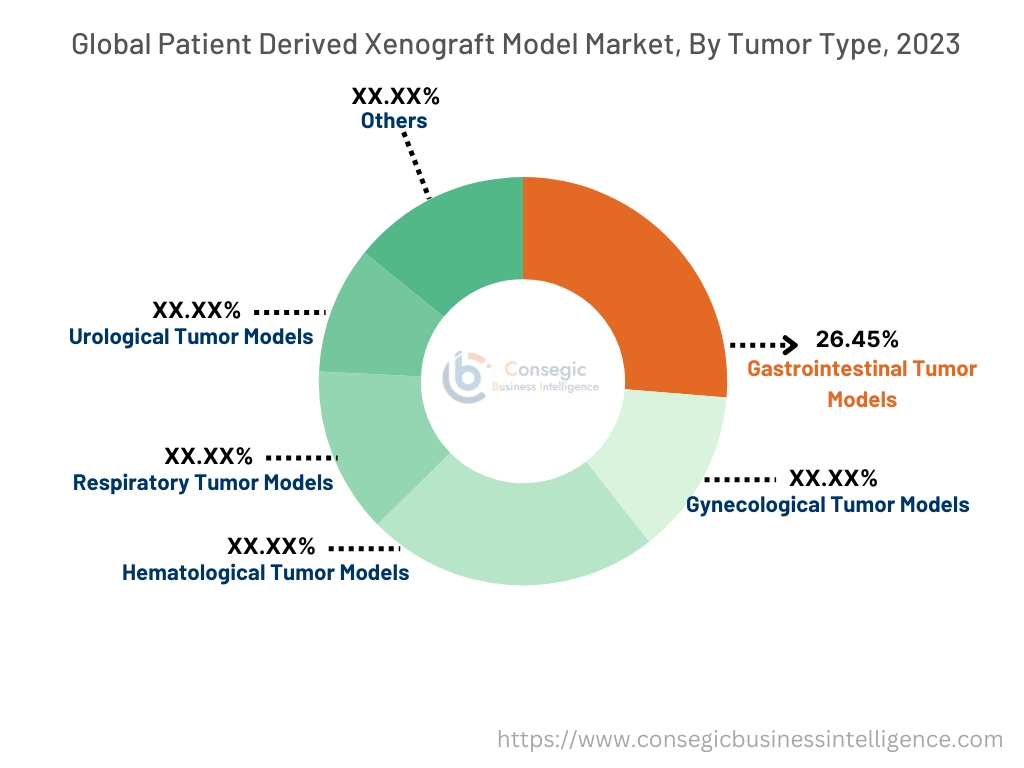

By Tumor Type:

Based on tumor type, the market is segmented into gastrointestinal tumor models, gynecological tumor models, hematological tumor models, respiratory tumor models, urological tumor models, and others.

The gastrointestinal tumor models segment accounted for the largest revenue share of 26.45% in 2023.

- Gastrointestinal tumors, including colorectal, gastric, and pancreatic cancers, are among the most commonly studied in PDX models due to their high global prevalence and complexity.

- These models enable the replication of tumor heterogeneity and progression, facilitating the development of novel therapies.

- The increasing focus on targeted therapies for colorectal and pancreatic cancers, coupled with the growing use of PDX models in preclinical trials, drives the dominance of these segmental trends.

- Gastrointestinal tumor models dominate the patient derived xenograft model market trends due to their extensive use in developing targeted therapies for high-prevalence cancers like colorectal and pancreatic tumors.

The hematological tumor models segment is anticipated to register the fastest CAGR during the forecast period.

- Hematological PDX models are critical for studying leukemia, lymphoma, and multiple myeloma.

- These models enable researchers to analyze the interaction between hematological malignancies and the bone marrow microenvironment, leading to the development of effective immunotherapies and targeted drugs.

- The rising adoption of humanized PDX models for immune-oncology studies, coupled with advancements in hematological cancer research, drives a surge in this segment.

- Hematological tumor models are expected to grow rapidly, driven by the increasing demand for immune-oncology research and advancements in hematological cancer treatment.

By Application:

Based on application, the market is segmented into preclinical drug development, biomarker analysis, research, and others.

The preclinical drug development segment accounted for the largest revenue in patient derived xenograft model market share in 2023.

- PDX models are the gold standard in preclinical oncology drug testing, offering accurate replication of human tumor biology and therapeutic responses.

- These models are widely used by pharmaceutical companies and CROs to evaluate the efficacy and safety of anticancer drugs.

- The increasing number of oncology clinical trials, coupled with the rising trends for predictive preclinical models, drives the adoption of PDX models in drug development.

- Furthermore, their role in reducing late-stage clinical failures enhances their importance in pharmaceutical R&D.

- Preclinical drug development leads the market trends, driven by the growing need for predictive models to improve oncology drug development outcomes.

The biomarker analysis segment is anticipated to register the fastest CAGR during the forecast period.

- PDX models are increasingly used for identifying and validating predictive biomarkers, enabling the development of personalized therapies.

- Their ability to maintain genetic and phenotypic characteristics of the original tumor makes them ideal for biomarker discovery and validation.

- The growing emphasis on precision medicine and the need for effective diagnostic and prognostic biomarkers are driving demand in this segment.

- Biomarker analysis is expected to grow rapidly, supported by the rising patient derived xenograft model market trends focus on precision medicine and the use of PDX models in personalized therapy development.

By End-User:

Based on end-user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, and contract research organizations (CROs).

The pharmaceutical & biotechnology companies segment accounted for the largest revenue share in 2023.

- Pharmaceutical and biotechnology companies are the primary users of PDX models, leveraging them for preclinical drug screening, biomarker validation, and translational research.

- These models enable companies to optimize drug pipelines and improve the success rates of clinical trials.

- The increasing number of new patient derived xenograft model market opportunities focus on oncology drug development and the rising investment in personalized medicine initiatives drive the dominance of this segment.

- Pharmaceutical & biotechnology companies lead the market trends due to their extensive use of PDX models in oncology drug development and translational research.

The contract research organizations (CROs) segment is anticipated to register the fastest CAGR during the forecast period.

- CROs are increasingly adopting PDX models to offer preclinical testing services to pharmaceutical companies, enabling cost-effective and efficient drug development.

- The growing trend of outsourcing preclinical research to CROs, driven by their expertise and advanced infrastructure, supports rapid development in this segment.

- The rising number of oncology clinical trials and the need for comprehensive preclinical data further fuel the demand for CRO services.

- CROs are expected to grow rapidly, driven by the increasing patient derived xenograft model market opportunities, resulting in outsourcing of preclinical research and their ability to provide advanced PDX-based services.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

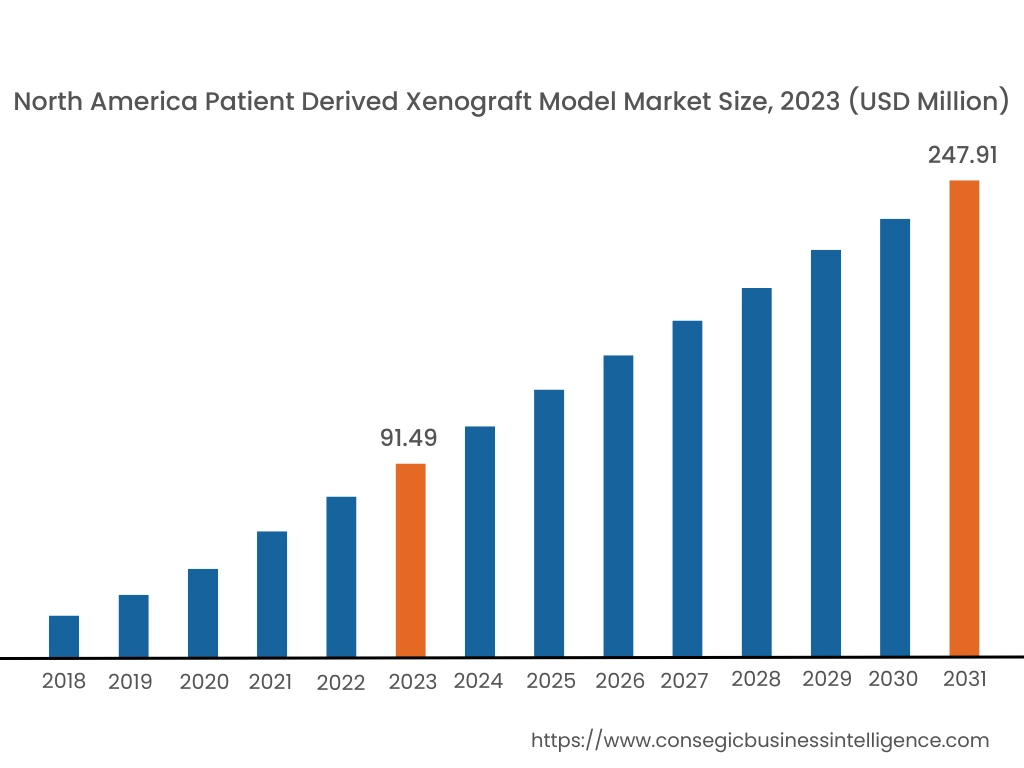

In 2023, North America was valued at USD 91.49 Million and is expected to reach USD 247.91 Million in 2031. In North America, the U.S. accounted for the largest share of 71.80% in 2023. North America dominates the patient-derived xenograft model market, driven by a strong focus on personalized medicine, cancer research, and advanced biotechnology infrastructure. The U.S. is at the forefront, with extensive use of PDX models in preclinical oncology studies to accelerate drug development and improve translational research. Major research institutions and pharmaceutical companies collaborate with contract research organizations (CROs) to leverage PDX models for testing the efficacy of novel cancer therapeutics. Canada is contributing to market growth with increasing investments in cancer research programs and the adoption of PDX models in academic and clinical studies. However, ethical concerns surrounding the use of animal models and high operational costs can hinder market expansion in the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 14.0% over the forecast period. Asia-Pacific is the fastest-growing region in the PDX model market, driven by increasing cancer prevalence, rising R&D investments, and a growing focus on personalized medicine in countries like China, Japan, and South Korea. China’s expanding pharmaceutical and biotechnology industry is leveraging PDX models for preclinical oncology research and drug screening. Japan’s advanced healthcare and research infrastructure supports the use of PDX models for precision cancer therapies, particularly for gastric and colorectal cancers. South Korea is focusing on integrating PDX models into its oncology research programs to enhance the drug development processes industry. However, limited awareness and high costs associated with establishing PDX platforms in emerging economies like India may hinder development.

Europe is a significant market for PDX models, supported by a strong emphasis on precision oncology and collaborative research projects between academic institutions and pharmaceutical companies. Countries like Germany, the UK, and France are leading, with high adoption rates of PDX models in cancer drug discovery and translational research. Germany’s advanced biotechnology sector and the UK’s focus on innovative cancer treatments drive patient derived xenograft model market demand. France is witnessing growth in the use of PDX models for studying rare and complex cancers. However, stringent animal welfare regulations in the European Union pose challenges for researchers, requiring strict compliance with ethical guidelines for animal use.

The Middle East & Africa region is witnessing steady growth in the PDX model market, primarily driven by increasing investments in cancer research and healthcare infrastructure in countries like the UAE and South Africa. The UAE’s focus on advanced cancer research and partnerships with international research organizations are boosting the adoption of PDX models for preclinical studies. In South Africa, rising cancer incidence and improving research capabilities are driving demand for PDX models in academic and clinical studies. However, the region faces challenges such as limited local expertise, high costs of PDX model development, and insufficient infrastructure for advanced research in several areas.

Latin America is an emerging market for PDX models, with Brazil and Mexico leading the region. Brazil’s growing emphasis on cancer research and collaborations between universities and pharmaceutical companies are driving patient derived xenograft model market demand for PDX models in preclinical studies. Mexico’s increasing investment in oncology research and clinical trials supports the adoption of PDX models to improve drug efficacy studies. However, limited funding for advanced cancer research and a lack of specialized research facilities in some countries present barriers to patient derived xenograft model market expansion. Efforts to improve research infrastructure and foster international collaborations could enhance the market’s potential in the region.

Top Key Players & Market Share Insights:

The patient derived xenograft model market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global patient derived xenograft model market. Key players in the patient derived xenograft model industry include -

- Charles River Laboratories (United States)

- The Jackson Laboratory (United States)

- EUROIMMUN AG (Germany)

- Oncodesign (France)

- HuMurine Technologies (United States)

- Crown Bioscience (United States)

- WuXi AppTec (China)

- Champions Oncology (United States)

- Xenopat (Spain)

- Horizon Discovery (United Kingdom)

Recent Industry Developments :

Product Development:

- In December 2024, Remix Therapeutics will present preclinical data on REM-422, a MYB mRNA degrader, at the 2024 EORTC-NCI-AACR Symposium. REM-422 shows tumor regression in adenoid cystic carcinoma (ACC) models and is in phase 1 trials for ACC and AML.

Patient Derived Xenograft Model Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 766.56 Million |

| CAGR (2024-2031) | 13.6% |

| By Type |

|

| By Tumor Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Patient-Derived Xenograft Model Market in 2023 and 2031? +

The market was valued at USD 275.85 million in 2023 and is projected to reach USD 766.56 million by 2031.

What drives the PDX Model Market? +

The increasing prevalence of cancer and the demand for precise preclinical models to improve drug development outcomes are key drivers.

What challenges does the market face? +

High costs, operational complexity, and ethical concerns regarding animal use are significant challenges.

What opportunities exist in the PDX Model Market? +

Advancements in humanized mouse models and increasing investment in immuno-oncology research present substantial opportunities.

Which type dominates the market? +

Mouse models dominate the market due to their widespread use in oncology research and ease of handling.