- Summary

- Table Of Content

- Methodology

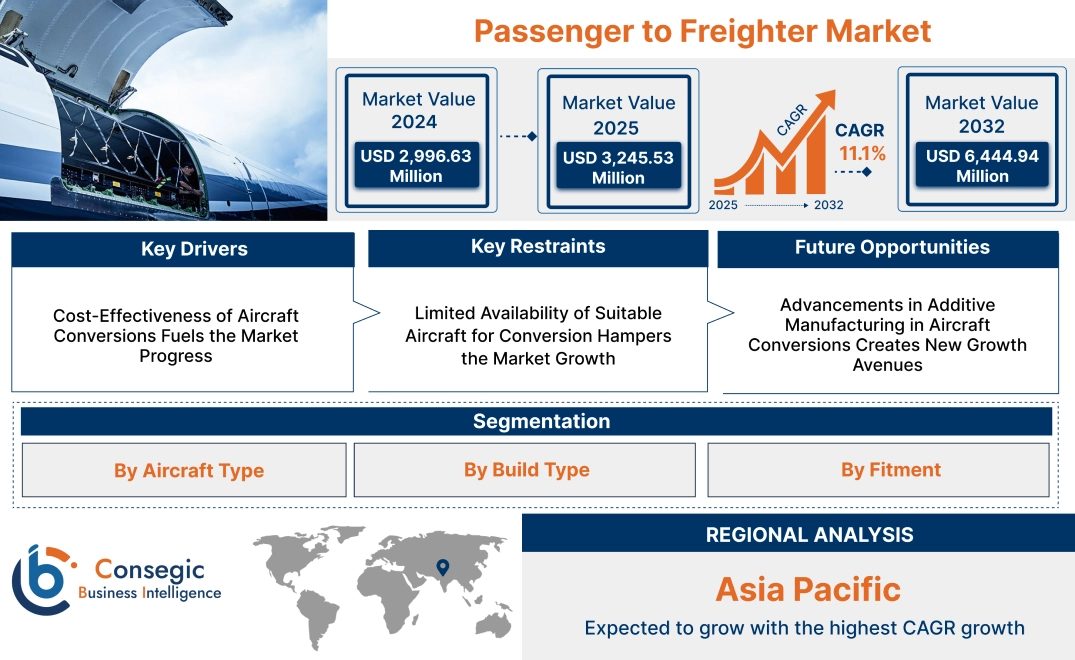

Passenger to Freighter Market Size:

Passenger to Freighter Market size is estimated to reach over USD 6,444.94 Million by 2032 from a value of USD 2,996.63 Million in 2024 and is projected to grow by USD 3,245.53 Million in 2025, growing at a CAGR of 11.1% from 2025 to 2032.

Passenger to Freighter Market Scope & Overview:

Passenger to freighter (P2F) conversion refers to the process of modifying passenger aircraft to accommodate cargo operations. This involves removing passenger seating, reinforcing flooring, installing large cargo doors, and optimizing the internal structure for cargo handling. P2F conversions provide a cost-effective solution for extending the operational lifespan of retired passenger aircraft, repurposing them for freight transportation.

These conversions are tailored to meet specific requirements, including the type of cargo, weight capacity, and operational range. The process also ensures compliance with aviation safety and regulatory standards while integrating advanced features like fire suppression systems, cargo tracking, and loading mechanisms. Converted aircraft are widely utilized for e-commerce, express delivery, and general cargo services.

End-users include cargo airlines, logistics companies, and leasing firms seeking efficient and economical solutions to expand their cargo operations. Passenger to freighter conversions play a critical role in addressing the growing demand for air freight capacity while maximizing asset utilization in the aviation industry.

Passenger to Freighter Market Dynamics - (DRO) :

Key Drivers:

Cost-Effectiveness of Aircraft Conversions Fuels the Market Progress

Converting passenger aircraft into freighters offers a cost-effective solution compared to purchasing new cargo planes, which are prohibitively expensive. Aircraft conversions allow airlines and leasing companies to maximize the value of aging passenger fleets by extending their operational life in the cargo sector. The conversion process typically involves modifying the fuselage, adding cargo doors, and reinforcing the structure to handle heavier loads, but it is still significantly cheaper than buying new freighter aircraft. This approach is especially appealing to companies looking to minimize capital expenditures while maintaining fleet flexibility. By opting for conversions, operators quickly expand their freighter capacity without waiting for new aircraft deliveries, making it an attractive option in the fast-growing air cargo market. Additionally, the relatively lower cost of conversions compared to new purchases helps to reduce the financial burden on airlines, enabling them to meet rising requirement for cargo services more efficiently. Thus, the aforementioned factors are driving the passenger to freighter market growth.

Key Restraints:

Limited Availability of Suitable Aircraft for Conversion Hampers the Market Growth

The declining availability of older passenger aircraft suitable for conversion is a key constraint for the P2F market. As airlines retire aging fleets, fewer aircraft with the ideal operational history and structural condition are available for conversion. Aircraft used for conversion must meet specific criteria, including minimal corrosion, manageable wear-and-tear, and sufficient remaining flight cycles to justify the investment. Additionally, the need for specific models, such as the Boeing 737 and Airbus A320 families, often exceeds supply, driving up acquisition costs. This shortage is further compounded by competition among airlines, leasing companies, and MRO providers seeking these aircraft for diverse purposes. The limited pool of suitable candidate’s impacts conversion timelines and increases project costs, making it difficult for P2F providers to meet the rising need for freighter capacity, particularly in regions experiencing rapid e-commerce growth and cargo expansion. Therefore, the above mentioned factors limit the passenger to freighter market demand.

Future Opportunities :

Advancements in Additive Manufacturing in Aircraft Conversions Creates New Growth Avenues

Advancements in additive manufacturing (3D printing) are transforming the Passenger to Freighter (P2F) conversion process by enabling the creation of lightweight, custom-designed parts and components. This technology allows manufacturers to produce intricate, high-performance components more quickly and cost-effectively than traditional methods. 3D printing reduces material waste, shortens production timelines, and offers the flexibility to design parts tailored specifically for freighter aircraft conversions. For example, custom brackets, reinforced structural components, or cargo hold modifications will be produced on demand, eliminating long lead times associated with sourcing traditional parts. Additionally, 3D printing enhance the overall structural efficiency of the converted freighter, contributing to weight reduction and improving fuel efficiency. As the technology continues to evolve, its integration into P2F conversions significantly streamline the conversion process, lower costs, and provide aircraft operators with more efficient, durable, and customized freighter solutions, thereby creating passenger to freighter market opportunities.

Passenger to Freighter Market Segmental Analysis :

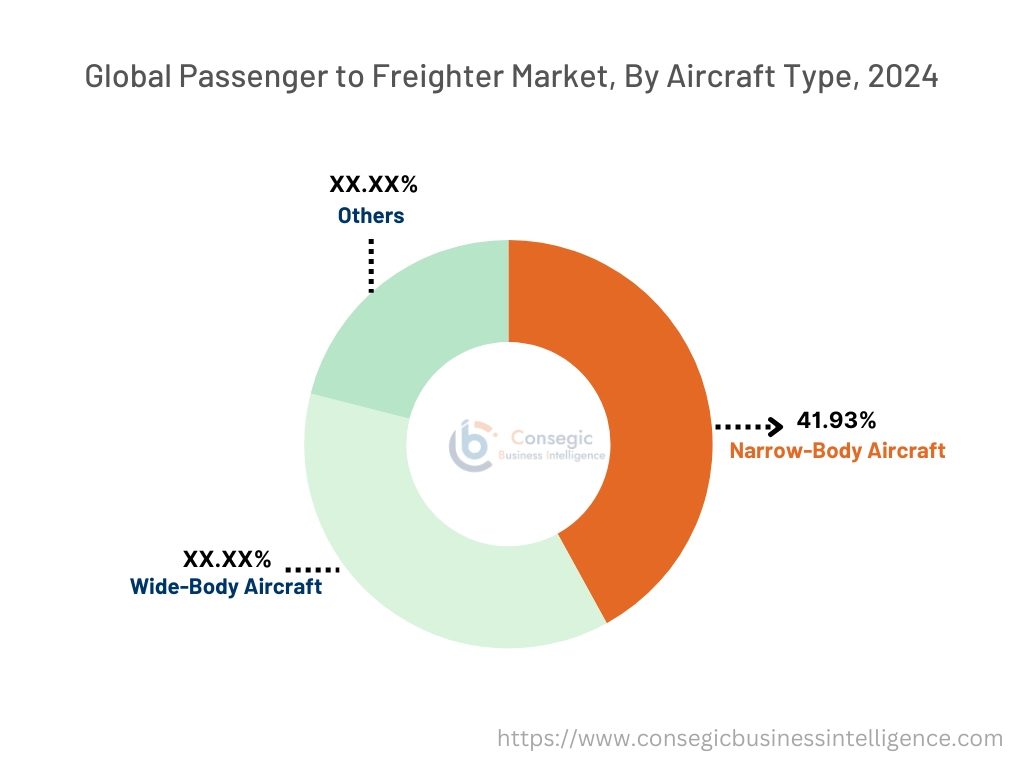

By Aircraft Type:

Based on aircraft type, the market is segmented into narrow-body aircraft, wide-body aircraft, and others.

The narrow-body aircraft segment held the largest revenue of 41.93% of the total passenger to freighter market share in 2024.

- Narrow-body aircraft are commonly converted into freighters due to their fuel efficiency and ability to handle medium-range transportation.

- These aircraft are highly preferred by cargo operators as they are cost-effective for shorter routes, making them ideal for express freight services.

- The narrow-body segment continues to dominate the market because of its versatile size, flexibility, and relatively lower conversion costs.

- As per the passenger to freighter market analysis, narrow-body aircraft remain crucial for regional logistics, contributing significantly to the global supply chain, and the segment’s extension reflects their need for cargo operations.

The wide-body aircraft segment is expected to grow at the fastest CAGR during the forecast period.

- Wide-body aircraft are increasingly being converted into freighters due to the growing need for high-capacity cargo transport, especially for international long-haul flights.

- Their larger cargo capacity makes them suitable for transporting bulk goods and oversized items, catering to sectors like e-commerce and automotive industries.

- Conversion of wide-body aircraft is supported by their ability to accommodate large, heavy cargo with increased payload capacity.

- The rise in global trade and the increasing requirement for large-scale cargo transportation are expected to boost the need for wide-body aircraft conversions, creating significant passenger to freighter market opportunities.

By Build Type:

Based on build type, the market is segmented into new build and refurbished.

The new build segment accounted for the largest market of the total passenger to freighter market share in 2024.

- New build aircraft are designed and built specifically for freight operations, offering advanced features and greater reliability for logistics operations.

- These aircraft are preferred by airlines and cargo operators looking for high-performance freighters with enhanced fuel efficiency and modern technologies.

- New builds are being increasingly used in the growing e-commerce and logistics sector, which requires optimized cargo solutions to handle large volumes.

- As per passenger to freighter market trends, the dominance of new build aircraft is attributed to their longer lifespan, reduced maintenance, and high operational efficiency.

The refurbished segment is expected to grow at the fastest CAGR during the forecast period.

- Refurbished aircraft offer a more cost-effective option for operators, particularly in regions with high demand for affordable cargo solutions.

- These aircraft are typically converted from older passenger planes, offering a more sustainable alternative to new builds.

- As need for affordable cargo capacity increases, many logistics companies are opting for refurbished aircraft due to their lower upfront cost and shorter lead time.

- Thus, refurbished aircraft are in high requirement, especially among smaller operators, and their market growth is being driven by the economic viability of the conversion process, contributing to the passenger to freighter market expansion.

By Fitment:

Based on fitment, the market is segmented into slot/retro fitment and line fitment.

The slot/retro fitment segment held the largest share in 2024.

- Slot/retro fitment is a popular option as it allows for the conversion of existing aircraft into freighters, which helps in meeting immediate freight need.

- This conversion process involves removing passenger cabins and replacing them with specialized cargo holds, making it an attractive choice for cost-conscious operators.

- The retro fitment market benefits from the availability of older, unused passenger aircraft, reducing the cost of conversion.

- According to industry trends, the slot/retro fitment segment is expected to maintain its dominance due to the flexibility and cost-effectiveness of converting existing aircraft, fueling the passenger to freighter market demand.

The line fitment segment is expected to grow at the fastest CAGR during the forecast period.

- Line fitment involves the direct integration of cargo systems into aircraft during their manufacturing process, which ensures higher-quality installations and greater operational efficiency.

- This approach is preferred for large fleet operators and airlines that require new-build freighters to meet growing global freight needs.

- Line fitment offers advantages in terms of faster delivery times and better optimized cargo configurations, which are especially useful for high-volume logistics.

- As per the market trends, as global trade continues to expand, demand for line fitment services is projected to increase due to the need for more efficient and modern freighter aircraft, driving the passenger to freighter market growth.

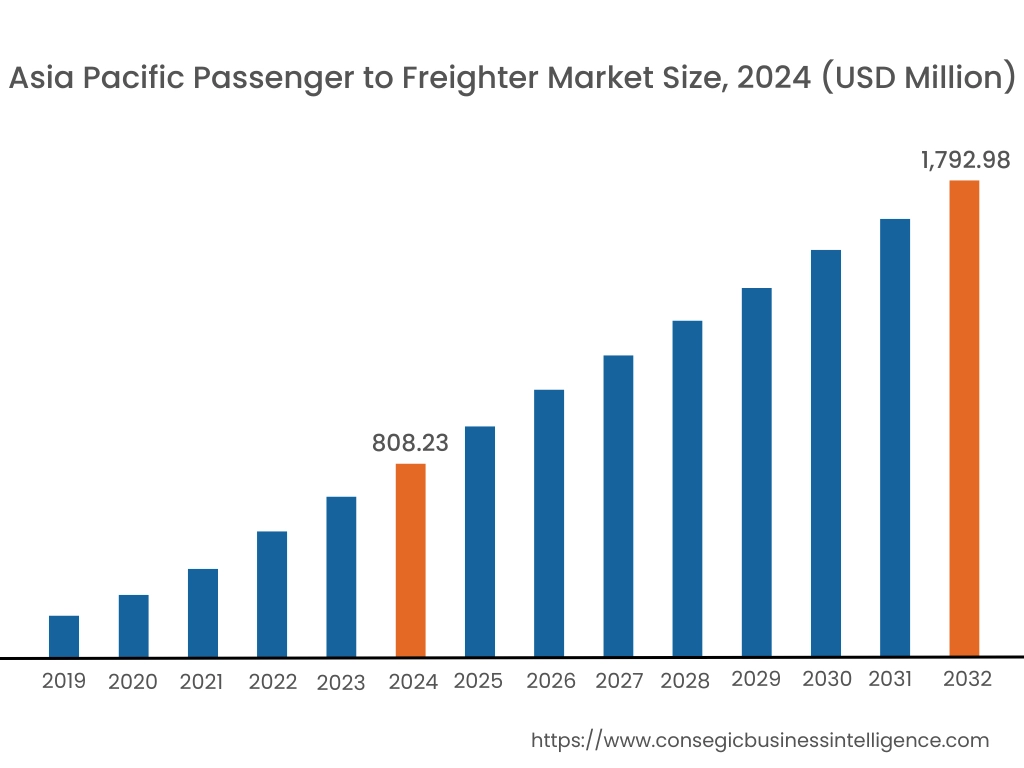

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

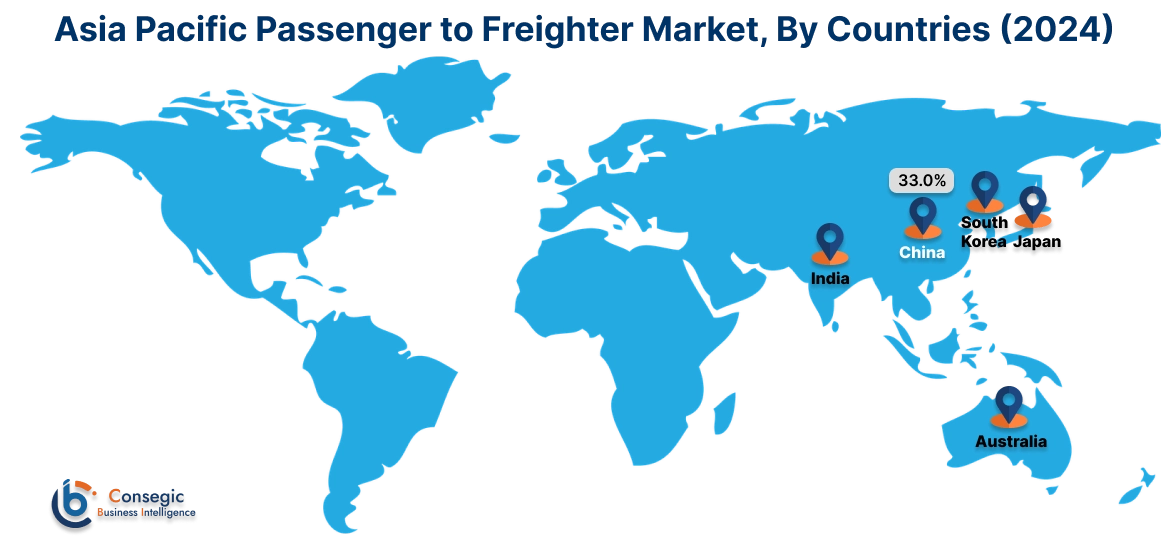

Asia Pacific region was valued at USD 808.23 Million in 2024. Moreover, it is projected to grow by USD 877.66 Million in 2025 and reach over USD 1,792.98 Million by 2032. Out of this, China accounted for the maximum revenue share of 33.0%. The Asia-Pacific region is witnessing rapid growth in the P2F market, propelled by increasing cargo activities and the extension of international trade. A prominent trend is the establishment of new conversion facilities to cater to the rising requirement. Analysis indicates that China and India are key players, with China holding the largest market share and India exhibiting the fastest growth in the region. As per the passenger to freighter market trends, government initiatives and investments in aviation infrastructure further facilitate this development.

North America is estimated to reach over USD 2,083.01 Million by 2032 from a value of USD 975.56 Million in 2024 and is projected to grow by USD 1,055.95 Million in 2025. This region holds a significant share of the P2F market, driven by the presence of major airlines and a robust aviation infrastructure. A notable trend is the increasing investment in freighter conversions to meet the rising demand for air cargo services. Analysis indicates that the U.S. market is particularly active, with airlines seeking cost-effective solutions to expand their cargo capacities. The availability of retired passenger aircraft suitable for conversion further drives the passenger to freighter market expansion.

European carriers are actively engaging in passenger-to-freighter conversions to enhance their cargo operations. A significant trend is the collaboration between airlines and conversion service providers to optimize fleet utilization. Analysis suggests that countries like Germany and the UK are leading in adoption, driven by the economic advantages and extended aircraft lifespan offered by conversions.

In the Middle East, airlines are exploring P2F conversions to diversify their operations and capitalize on cargo opportunities. The focus is on enhancing cargo capabilities to support economic diversification efforts. In Africa, the market is gradually evolving, with efforts to build local MRO (Maintenance, Repair, and Overhaul) capabilities to support conversions. Analysis suggests that partnerships with international conversion specialists and investments in infrastructure are crucial for market development in these regions.

Latin American airlines are recognizing the potential of P2F conversions to boost their cargo services. A notable trend is the interest in converting narrow-body aircraft to serve regional cargo needs. However, economic constraints and limited technological infrastructure may impact the pace of adoption. The passenger to freighter market analysis indicates that collaborations with global conversion providers and favorable government policies could play a pivotal role in advancing the P2F market in this region.

Top Key Players and Market Share Insights:

The Passenger to Freighter market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Passenger to Freighter market. Key players in the Passenger to Freighter industry include –

- PEMCO Conversions (USA)

- Precision Aircraft Solutions (USA)

- AIC JETS Corporation (USA)

- Kuehne + Nagel (Switzerland)

- Air Transport Services Group (ATSG) (USA)

- ST Engineering (Singapore)

- Aeronautical Engineers Inc. (AEI) (USA)

- Elbe Flugzeugwerke GmbH (EFW) (Germany)

- Israel Aerospace Industries (IAI) (Israel)

- Cascade Aerospace (Canada)

Recent Industry Developments :

Service Launch:

- In April 2024, Embraer's E190F, its first converted E-Jet freighter, completed its maiden flight in Brazil, marking a milestone in cargo aviation. The aircraft, leased to Regional One, offers over 50% more volume capacity than large turboprops, three times the range, and up to 30% lower operating costs compared to narrowbodies. With a maximum structural payload of 13,500 kg, the E190F, alongside the larger E195F, aims to meet the growing e-commerce need with enhanced agility and decentralized delivery capabilities. Testing continues before operational debut.

Partnerships & Collaborations:

- In August 2023, Boeing and Joramco announced a new Boeing Converted Freighter (BCF) line in Amman, Jordan, making Joramco the first Middle Eastern MRO provider to support 737-800BCF conversions for domestic and international aircraft. Strategically located, Joramco will serve operators across the Middle East, Europe, North Africa, and CIS. This collaboration highlights Boeing’s efforts to meet rising global need for freighter conversions, projected at over 1,300 standard-body freighters by 2042.

Passenger to Freighter Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6,444.94 Million |

| CAGR (2025-2032) | 11.1% |

| By Aircraft Type |

|

| By Build Type |

|

| By Fitment |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Passenger to Freighter Market? +

The Passenger to Freighter Market size is estimated to reach over USD 6,444.94 Million by 2032 from a value of USD 2,996.63 Million in 2024 and is projected to grow by USD 3,245.53 Million in 2025, growing at a CAGR of 11.1% from 2025 to 2032.

What are the key segments in the Passenger to Freighter Market? +

The market is segmented by aircraft type (narrow-body aircraft, wide-body aircraft, and others), build type (new build, refurbished), and fitment (slot/retro fitment, line fitment).

Which segment is expected to grow the fastest in the Passenger to Freighter Market? +

The wide-body aircraft segment is expected to grow at the fastest CAGR during the forecast period, driven by increasing demand for high-capacity cargo transport, especially for international long-haul flights.

Who are the major players in the Passenger to Freighter Market? +

Key players in the Passenger to Freighter market include PEMCO Conversions (USA), Precision Aircraft Solutions (USA), ST Engineering (Singapore), Aeronautical Engineers Inc. (AEI) (USA), Elbe Flugzeugwerke GmbH (EFW) (Germany), Israel Aerospace Industries (IAI) (Israel), Cascade Aerospace (Canada), AIC JETS Corporation (USA), Kuehne + Nagel (Switzerland), and Air Transport Services Group (ATSG) (USA).