- Summary

- Table Of Content

- Methodology

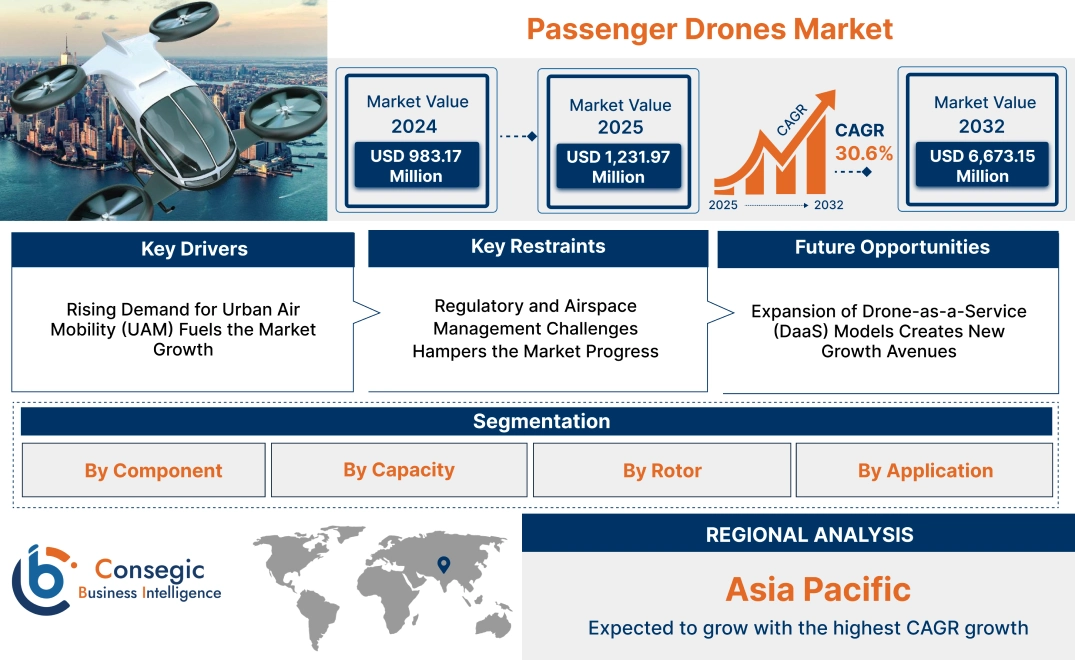

Passenger Drones Market Size:

Passenger Drones Market size is estimated to reach over USD 6,673.15 Million by 2032 from a value of USD 983.17 Million in 2024 and is projected to grow by USD 1,231.97 Million in 2025, growing at a CAGR of 30.6% from 2025 to 2032.

Passenger Drones Market Scope & Overview:

Passenger drones are autonomous or semi-autonomous aerial vehicles designed to transport individuals or small groups over short to medium distances. These drones are equipped with advanced navigation systems, safety features, and electric propulsion technologies, offering an innovative mode of air transportation. They are widely envisioned for applications such as urban air mobility, emergency response, and personal commuting.

These aerial vehicles come in various configurations, including multicopters and fixed-wing designs, tailored for specific use cases. These drones are engineered with systems such as collision avoidance, GPS navigation, and redundant power systems to ensure safety and reliability during operations. Their compact design and vertical takeoff and landing (VTOL) capabilities make them suitable for use in urban environments and confined spaces.

End-users include transportation service providers, government agencies, and private operators exploring new solutions for mobility and logistics. These drones play a transformative role in advancing the concept of urban air mobility and addressing challenges in modern transportation systems.

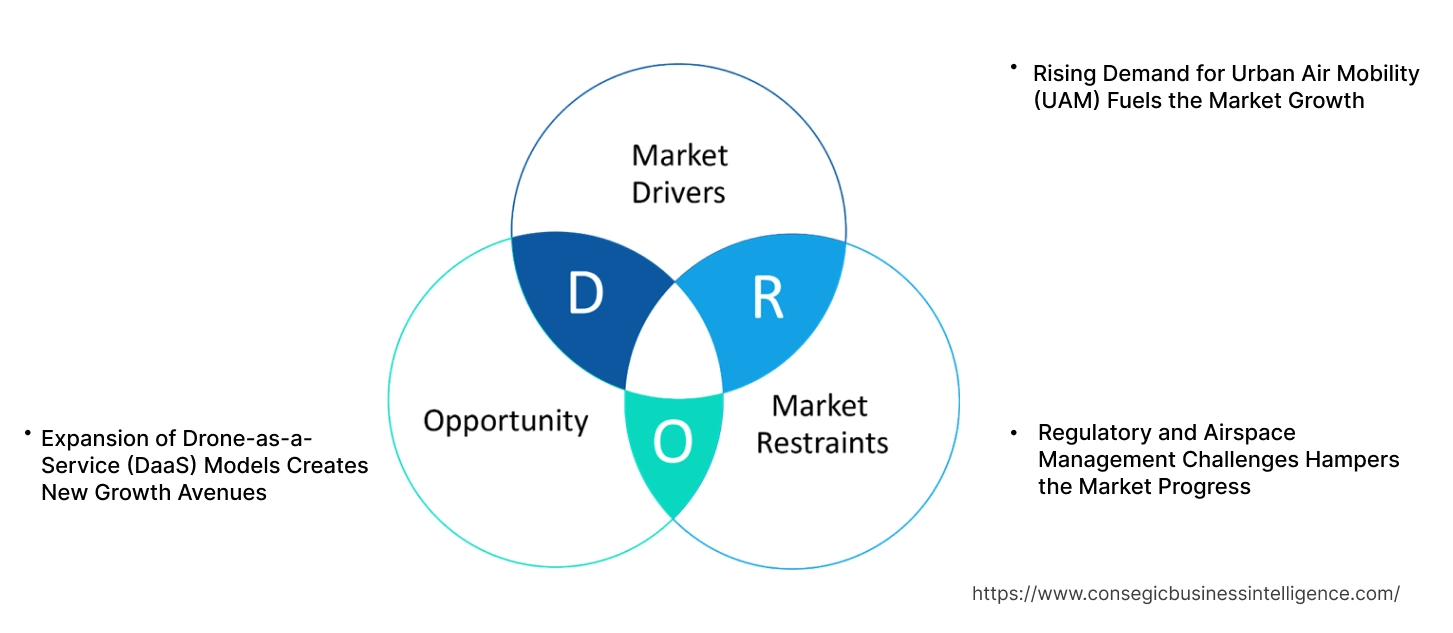

Passenger Drones Market Dynamics - (DRO) :

Key Drivers:

Rising Demand for Urban Air Mobility (UAM) Fuels the Market Growth

The rapid pace of urbanization and worsening traffic congestion in metropolitan areas have amplified the need for innovative transportation solutions, driving the demand for Urban Air Mobility (UAM). Passenger drones, with their ability to bypass ground traffic, offer a faster, more efficient, and scalable alternative for intra-city travel. These electric or hybrid-powered aerial vehicles are particularly appealing for densely populated cities, reducing commute times and alleviating pressure on overburdened road networks. UAM solutions integrate seamlessly into smart city frameworks, addressing mobility challenges while aligning with sustainability goals. These drones are being positioned as a key component of future urban transportation systems, supported by advancements in autonomous navigation, battery technology, and infrastructure development. Governments and private stakeholders are increasingly investing in UAM pilot programs and projects, showcasing the potential of the drones to revolutionize urban mobility, further driving the passenger drones market growth.

Key Restraints:

Regulatory and Airspace Management Challenges Hampers the Market Progress

The absence of standardized regulations and structured frameworks for drone operations presents a critical barrier to the passenger drone market. Urban airspace, already congested with traditional aircraft and commercial aviation, lacks the infrastructure and protocols to safely integrate passenger drones. Air traffic management for drones in densely populated areas is particularly difficult, as it requires precise coordination to prevent collisions, ensure safety, and minimize disruptions. Furthermore, regulations regarding drone certification, pilot licensing (for semi-autonomous operations), and operational safety standards vary significantly across regions, complicating international deployment. The lack of global regulatory alignment slows the adoption of these drones, delaying investments and development. Thus, the aforementioned factors are hindering the passenger drones market demand.

Future Opportunities :

Expansion of Drone-as-a-Service (DaaS) Models Creates New Growth Avenues

The expansion of Drone-as-a-Service (DaaS) models is revolutionizing the passenger drone market by offering flexible, subscription-based, or pay-per-use solutions. These models make passenger drones more accessible and affordable for individuals and businesses by eliminating the need for ownership and reducing upfront costs. DaaS enables users to leverage the drones for specific purposes, such as on-demand transportation, emergency services, or cargo delivery, without the financial and logistical burden of maintenance, operation, and infrastructure. This scalability is particularly attractive for urban air mobility, where demand fluctuates based on location and timing. Service providers optimize fleet utilization, improve cost-efficiency, and expand their customer base through tailored DaaS offerings. Additionally, the DaaS model fosters collaboration between drone manufacturers, service operators, and urban planners, creating an ecosystem that accelerates the integration of these drones into smart cities and next-generation mobility networks. Therefore, the above mentioned factors are creating substantial passenger drones market opportunities.

Passenger Drones Market Segmental Analysis :

By Component:

Based on component, the market is segmented into airframe, controller system, navigation system, propulsion system, and others.

The airframe segment held the largest revenue of the total passenger drones market share in 2024.

- The dominance of the airframe segment is driven by advancements in lightweight materials, such as carbon fiber composites, which enhance energy efficiency and flight performance.

- Increasing investments in durable and aerodynamic airframe designs support long-term operational safety and cost-effectiveness.

- Innovations in modular airframe designs facilitate easy maintenance and scalability for various drone models.

- As per the market trends, the need for advanced airframes is bolstered by their ability to support autonomous flight systems and heavy payloads, contributing to the passenger drones market expansion.

The propulsion system segment is anticipated to grow at the fastest CAGR during the forecast period.

- Electric and hybrid propulsion systems are increasingly adopted for their lower environmental impact and operational efficiency.

- Innovations in battery technologies are enabling longer flight durations and enhancing the feasibility of passenger drones for urban air mobility.

- The integration of distributed propulsion systems contributes to improved stability and noise reduction, further driving adoption.

- As per the passenger drones market analysis, growth in awareness of sustainable and clean energy solutions fuels the adoption of advanced propulsion technologies.

By Capacity:

Based on capacity, the market is bifurcated into up to 100 kg and over 100 kg.

The up to 100 kg segment accounted for the largest revenue of the total passenger drones market share in 2024.

- Lightweight drones in this category are widely adopted for single-passenger transportation and recreational purposes.

- Their compact design and energy efficiency make them a preferred choice for urban air mobility solutions.

- Increasing use in short-distance commuting applications further supports the dominance of this segment.

- As per the passenger drones market trends, regulatory frameworks and certifications for lightweight passenger drones are advancing, easing their market penetration.

The over 100 kg segment is expected to register the fastest CAGR during the forecast period.

- This segment is driven by rising adoption of multi-passenger drones for logistics, medical emergencies, and inter-city transportation.

- Higher load-bearing capacities enable applications in heavy cargo delivery and urban air taxi services.

- Continuous advancements in power systems and materials support the development of high-capacity drones.

- Thus, increasing investments in commercial and industrial use cases further enhance the segment's potential, fueling the passenger drones market growth.

By Rotor:

Based on rotor type, the market is segmented into less than 10 and more than 10 rotors.

The less than 10 rotors segment held the largest revenue share in 2024.

- This rotor configuration is widely used in lightweight and cost-efficient passenger drones for urban air mobility.

- Lower rotor counts reduce operational complexity and manufacturing costs, making them more accessible to consumers.

- Enhanced fuel efficiency and aerodynamic benefits also support their widespread adoption in the transportation industry.

- Thus, as per the market trends these drones are increasingly favored for recreational and short-distance applications, further driving the passenger drones market demand.

The more than 10 rotors segment is projected to grow at the fastest CAGR during the forecast period.

- Higher rotor counts offer superior stability and redundancy, ensuring safe operations even in adverse conditions.

- This configuration is ideal for multi-passenger drones and heavy payload applications in emergency response and logistics.

- The growing focus on safety and operational reliability drives the need for drones with advanced rotor systems.

- As per the passenger drones market analysis, expanding use cases in industrial and defense industry further boost adoption of this segment.

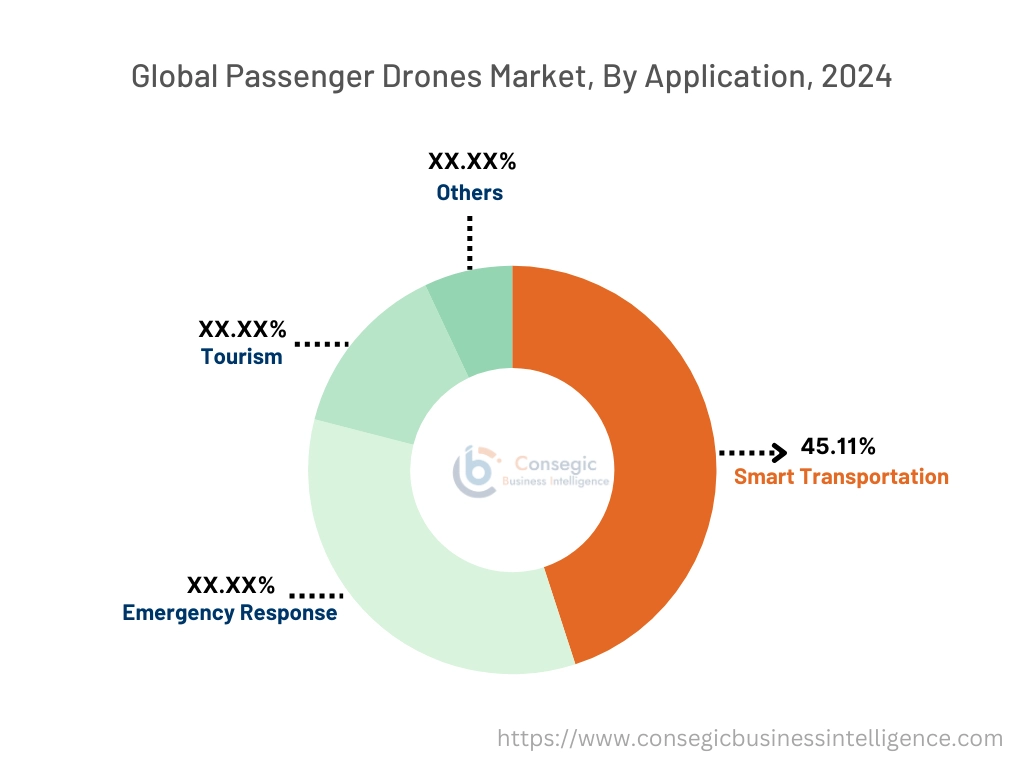

By Application:

Based on application, the market is segmented into smart transportation, emergency response, tourism, and others.

The smart transportation segment accounted for the largest revenue of 45.11% share in 2024.

- Increasing urbanization and congestion in cities have driven demand for innovative mobility solutions, including passenger drones.

- Smart transportation initiatives supported by government funding and private investments bolster adoption.

- These drones are increasingly integrated with IoT platforms for seamless connectivity and route optimization.

- As per the passenger drones market trends, partnerships between drone manufacturers and transportation service providers enhance the feasibility of these solutions.

The emergency response segment is expected to grow at the fastest CAGR during the forecast period.

- Passenger drones are gaining traction for rapid deployment in disaster relief and medical emergencies, where speed and accessibility are critical.

- Increased use of drones for search-and-rescue operations in remote or hazardous areas further supports growth.

- Investments in advanced navigation and payload delivery systems enhance the utility of drones for emergency applications.

- The segment’s growth is also fueled by the adoption of drones in fire-fighting, law enforcement, and humanitarian missions, which further facilitates the passenger drones market expansion.

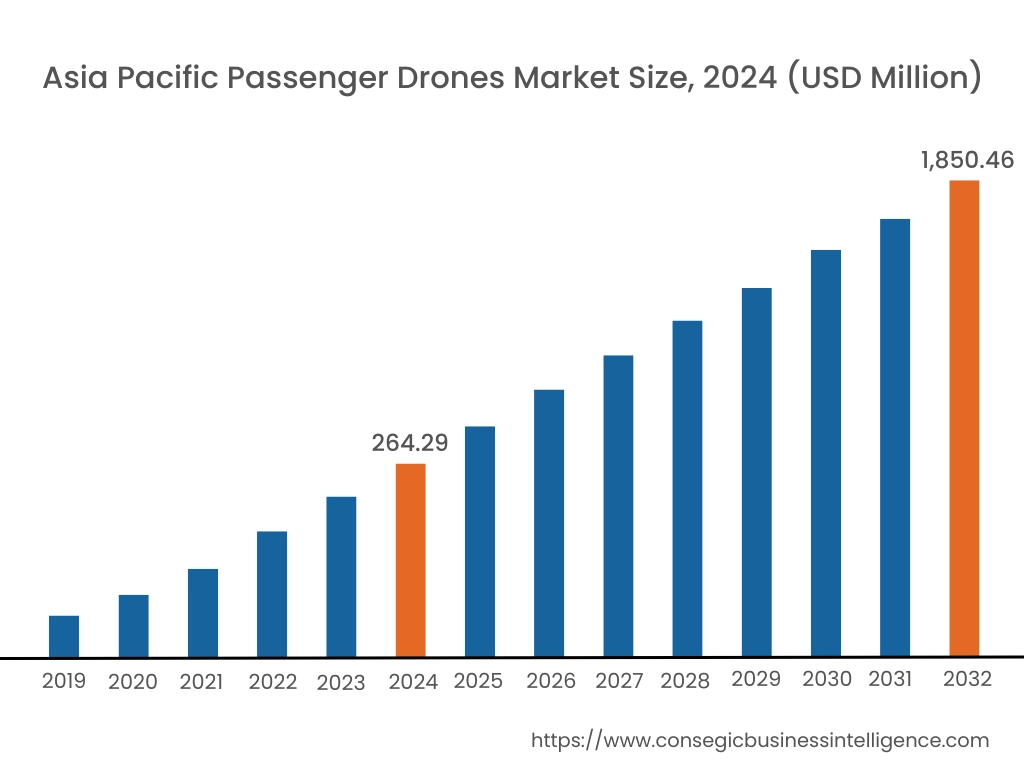

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

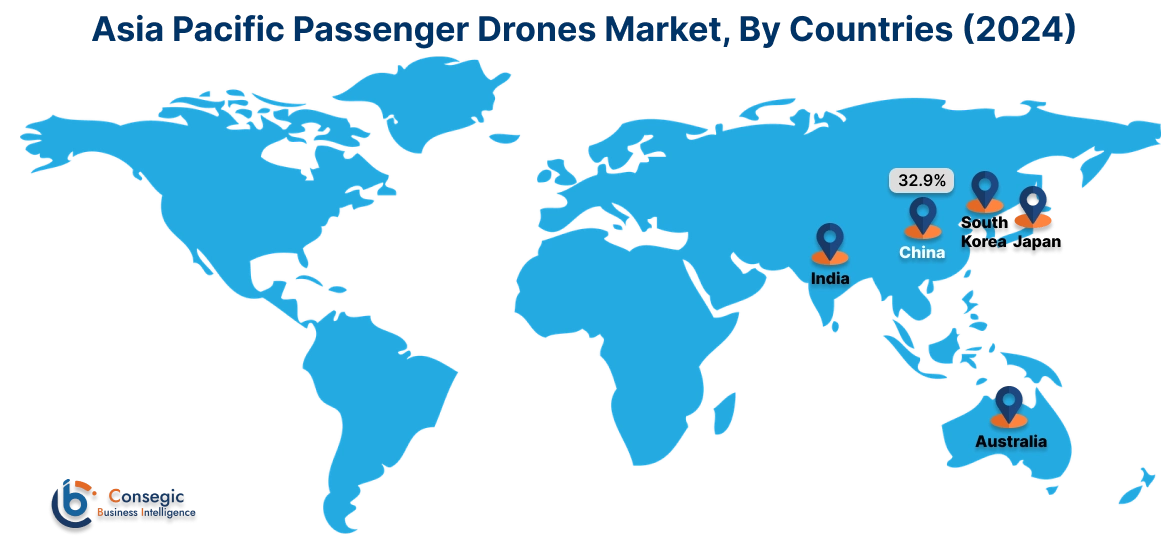

Asia Pacific region was valued at USD 264.29 Million in 2024. Moreover, it is projected to grow by USD 332.04 Million in 2025 and reach over USD 1,850.46 Million by 2032. Out of this, China accounted for the maximum revenue share of 32.9%. The Asia-Pacific region is witnessing rapid advancements in passenger drone technology, with countries like China leading the charge. A prominent trend is the development and testing of large cargo drones and air taxis, supported by government initiatives to promote a low-altitude economy. Analysis suggests that easing airspace restrictions and government incentives are facilitating the integration of these drones into the transportation network, promising faster and more cost-effective services, thereby creating new passenger drones market opportunities.

North America is estimated to reach over USD 2,150.75 Million by 2032 from a value of USD 319.19 Million in 2024 and is projected to grow by USD 399.72 Million in 2025. This region commands a substantial share of the passenger drones market, driven by the presence of leading technology firms and a supportive regulatory framework. A notable trend is the increasing investment in research and development to enhance drone capabilities and ensure safety. Analysis indicates that the integration of drones into urban air mobility solutions is progressing, with companies conducting test flights and collaborating with regulatory bodies to achieve certification.

European countries are actively exploring passenger drone technologies to address urban congestion and environmental concerns. A significant trend is the collaboration between governments and private companies to develop infrastructure and regulatory standards for passenger drones. However, safety concerns have led to delays in some projects.

In the Middle East, nations are investing in passenger drone technologies to enhance urban mobility and tourism experiences. The focus is on developing pilot projects to assess the feasibility and public acceptance of passenger drones. In Africa, the market is gradually evolving, with efforts to utilize drones for passenger transport in remote areas. Analysis indicates that infrastructure development and regulatory frameworks are crucial factors influencing the adoption of passenger drones in these regions.

Latin American countries are exploring passenger drones to address urban transportation challenges. A notable trend is the interest in deploying drones for short-distance travel to alleviate traffic congestion. Nonetheless, economic constraints and regulatory hurdles may impact the pace of adoption. Analysis suggests that partnerships with international companies and investments in infrastructure could play a pivotal role in advancing the passenger drones market in this region.

Top Key Players and Market Share Insights:

The Passenger Drones market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global Passenger Drones market. Key players in the Passenger Drones industry include –

- EHang (Guangzhou, China)

- Volocopter GmbH (Bruchsal, Germany)

- Urban Aeronautics Ltd. (Yavne, Israel)

- Vertical Aerospace Ltd. (Bristol, UK)

- Airbus S.A.S. (Leiden, Netherlands)

- Joby Aviation (Santa Cruz, California, USA)

- Archer Aviation (Palo Alto, California, USA)

- Wisk Aero (Mountain View, California, USA)

- Lilium GmbH (Munich, Germany)

Passenger Drones Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 6,673.15 Million |

| CAGR (2025-2032) | 30.6% |

| By Component |

|

| By Capacity |

|

| By Rotor |

|

| By Application |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the size of the Passenger Drones Market? +

The Passenger Drones Market size is estimated to reach over USD 6,673.15 Million by 2032 from a value of USD 983.17 Million in 2024 and is projected to grow by USD 1,231.97 Million in 2025, growing at a CAGR of 30.6% from 2025 to 2032.

What are the key segments in the Passenger Drones Market? +

The market is segmented by component (airframe, controller system, navigation system, propulsion system, etc.), capacity (up to 100 kg, over 100 kg), rotor type (less than 10, more than 10), and application (smart transportation, emergency response, tourism, etc.).

Which segment is expected to grow the fastest in the Passenger Drones Market? +

The emergency response segment is expected to grow at the fastest CAGR during the forecast period, driven by increased use of drones for medical emergencies, disaster relief, and search-and-rescue operations.

Who are the major players in the Passenger Drones Market? +

Key players in the Passenger Drones market include EHang (Guangzhou, China), Volocopter GmbH (Bruchsal, Germany), Joby Aviation (Santa Cruz, California, USA), Archer Aviation (Palo Alto, California, USA), Wisk Aero (Mountain View, California, USA), Lilium GmbH (Munich, Germany), Urban Aeronautics Ltd. (Yavne, Israel), Vertical Aerospace Ltd. (Bristol, UK), and Airbus S.A.S. (Leiden, Netherlands).