- Summary

- Table Of Content

- Methodology

Packaging Materials Market Size:

Packaging Materials Market size is growing with a CAGR of 3.1% during the forecast period (2024-2031), and the market is projected to be valued at USD 1,107.65 Billion by 2031 from USD 866.43 Billion in 2023.

Packaging Materials Market Scope & Overview:

Packaging materials encompass a range of materials used to enclose, protect, and transport products. Common types of materials include paper & cardboard, plastics, metal, and glass amongst others. The materials come in various product types, such as cans, drums, wraps, films, boxes, crates, and jars amongst others. These materials protect products from damage, contamination, and environmental factors during storage and transportation. Moreover, it maintains product quality, freshness, and shelf life. Additionally, it facilitates better handling, storage, and distribution. Furthermore, they aid in providing essential product information such as ingredients, usage instructions, and expiration dates. Also, they are durable, tamper-evident, and offer good barrier properties.

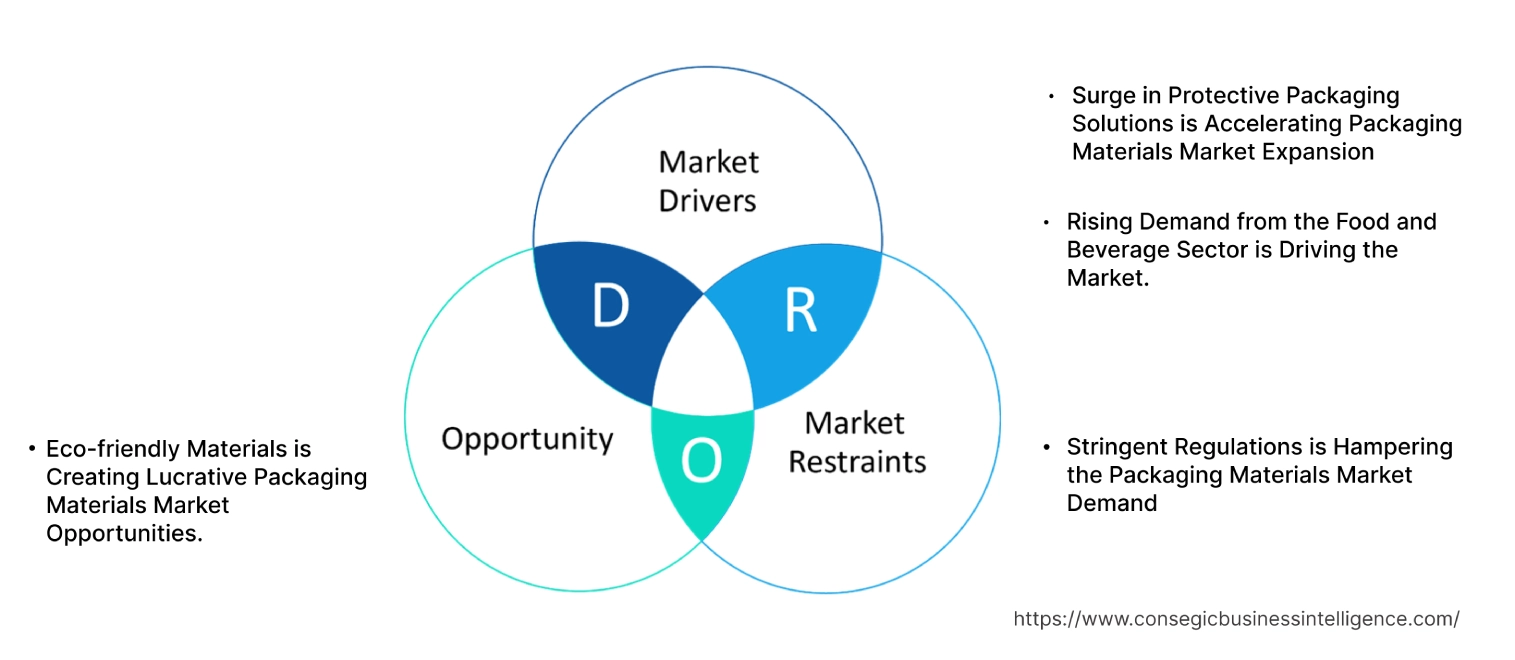

Packaging Materials MarketDynamics - (DRO) :

Key Drivers:

Surge in Protective Packaging Solutions is Accelerating Packaging Materials Market Expansion

Protective packaging includes materials and solutions designed to prevent physical, environmental, and chemical damage, ensuring product integrity. Different types of protective materials include bubble wrap made of plastic, foam, corrugated boxes, and air cushions amongst others.

In the healthcare sector, sensitive products such as vaccines, medical devices, and pharmaceuticals require specialized protective packaging solutions to maintain efficacy and meet regulatory standards. Additionally, the electronics sector relies on anti-static and shock-absorbent materials to protect high-value goods during transit.

Moreover, with increased internet penetration, the convenience of online shopping, and owing to a wider range of products available, there is a rise in the E-commerce sector, resulting in a higher volume of shipments.

- For instance, according to SellersCommerce, a software company in the United States, the country’s eCommerce sales surpassed the USD 1 trillion threshold for the first time in 2022, reaching a total of USD 1.01 trillion, marking a 6.5% rise compared to the prior year. Thus, protective packaging ensures that products reach consumers in pristine condition, reducing the likelihood of damage and associated costs, and influencing the market positively.

Overall, the rising preference for protective packaging solutions such as bubble wraps, molded foams, and air pillows in the healthcare, electronics, and e-commerce sectors, is driving the packaging materials market expansion.

Rising Demand from the Food and Beverage Sector is Driving the Market.

The food and beverage sector utilizes various materials, each offering unique advantages. Lightweight and versatile plastics are widely used for bottles, pouches, and containers. They offer durability and flexibility for resealing.

Moreover, glass provides excellent barrier properties, preserving flavor and freshness. Additionally, metal cans and aluminum foil provide superior protection against light, moisture, and oxygen, ensuring a longer shelf life for beverages and canned foods. Rising disposable incomes, and busy lifestyles driving the need for ready-to-eat meals, snacks, and functional beverages have led to an increase in the food and beverage sector.

- For instance, according to an article published in The Institute of Food Technologists, in 2022, global revenues from fortified and functional foods increased by approximately 6.5% from 2020 to 2021. Thus, this has required materials for packaging that preserve the nutritional value and sensory properties of these products, positively impacting packaging materials market trends.

Overall, growing food and beverage sectors require materials to ensure product safety and quality, and extended shelves are accelerating the global packaging materials market growth.

Key Restraints :

Stringent Regulations is Hampering the Packaging Materials Market Demand

Stringent regulations are a significant restraint in the market due to increasing government and environmental agency efforts to reduce pollution, waste, and resource depletion. Regulations such as the European Union's Single-Use Plastics Directive, bans on certain non-biodegradable materials, and requirements for extended producer responsibility (EPR) compel manufacturers to shift towards sustainable and eco-friendly packaging solutions.

These policies require the use of recyclable, compostable, or biodegradable materials, which increase production costs. For example, transitioning from traditional plastics to bioplastics or paper-based alternatives involves higher raw material and processing expenses. Regulations also impose stricter controls on the use of hazardous chemicals, such as Bisphenol A (BPA), in food and beverage packaging. Companies must invest in research and development (R&D) to develop compliant materials, which are time-consuming and costly. Furthermore, varying regulatory frameworks across regions create challenges for global players, further hindering packaging materials market demand.

Overall, analysis shows that the stringent regulations, aimed at promoting sustainability and reducing environmental impact, impose significant costs and complexities to the market, hampering the packaging materials market trends.

Future Opportunities :

Eco-friendly Materials is Creating Lucrative Packaging Materials Market Opportunities.

Eco-friendly packaging materials are sustainable alternatives designed to minimize environmental impact. They are typically made from biodegradable, compostable, or recyclable materials such as paper, cardboard, bioplastics, plant-based fibers, and reusable glass or metal.

These materials aim to lower carbon emissions compared to conventional packaging such as plastics. Many eco-friendly materials decompose naturally, reducing landfill accumulation. Moreover, many materials use renewable resources and conserve non-renewables such as petroleum.

Climate change, pollution, and resource depletion have heightened public awareness and regulatory pressure. Owing to this, consumers are increasingly seeking sustainable products and brands that align with their values. In addition to that, governments worldwide are implementing stricter environmental regulations, incentivizing sustainable practices.

- For instance, in New Jersey, from 2024, the state government-mandated minimum thresholds for recycled content. 10% for rigid plastic containers, 15% for plastic beverage containers, 35% for glass containers, 40% for paper carryout bags, and 20% for plastic carryout bags. Additionally, S2515 prohibits the use of polystyrene packing peanuts. This will significantly boost the requirements for eco-friendly materials, creating potential for global packaging materials market growth in the upcoming years.

Overall, the increasing emphasis on sustainability, driven by environmental concerns and regulatory pressures, is creating lucrative packaging materials market opportunities.

Packaging Materials Market Segmental Analysis :

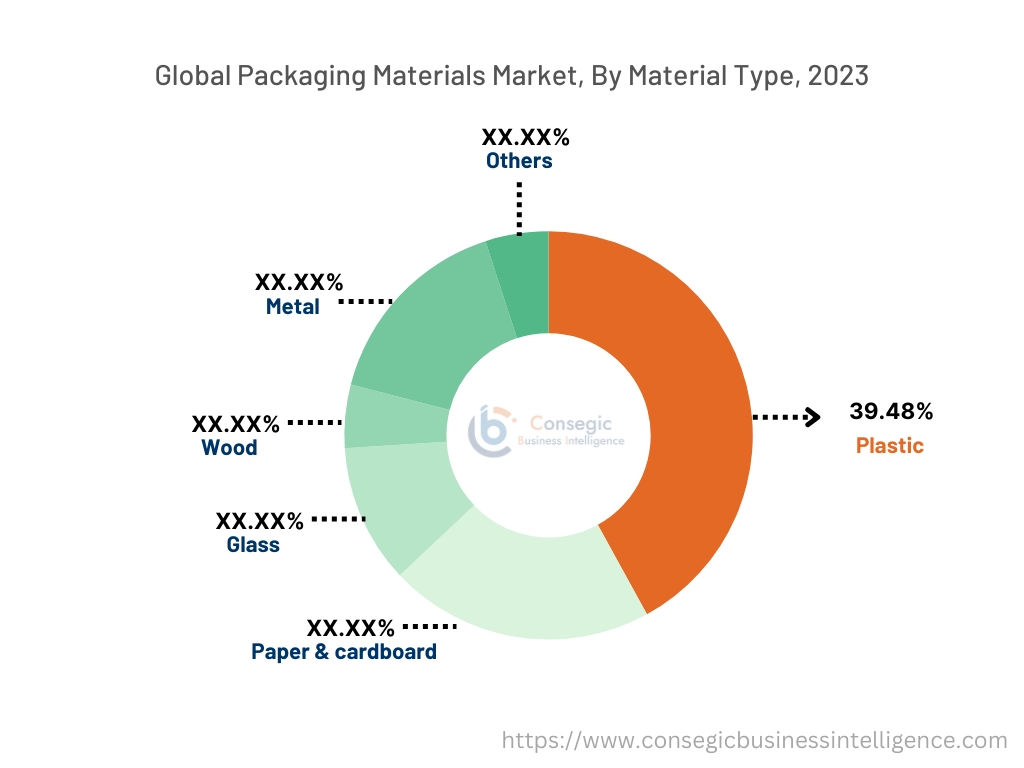

By Material Type:

Based on material type, the market is categorized into plastic, paper & cardboard, glass, wood, metal, and others.

Trends in the Material Type:

- Growing adoption of packaging made from recycled plastic.

- Rising focus on biodegradable packaging solutions to minimize waste.

The plastic segment accounted for the largest market share of 39.48% in 2023.

- Plastic packaging is a widely used material. It is primarily made from polymers such as polyethylene, polypropylene, polystyrene, and polyethylene terephthalate. It is cost-effective, scalable, and highly adaptable, making it ideal for large-scale production.

- Plastic packaging is categorized into several types, each serving specific purposes. Rigid plastic is commonly used for products such as bottles, containers, and trays, offering structural integrity and protection. Flexible plastic is used for films, pouches, and bags, providing ease of use, cost-efficiency, and the ability to conform to product shapes.

- Advancements in plastic packaging technologies have led to the development of innovative and sustainable packaging solutions.

- For instance, all 500-mL sparkling beverage bottles offered by The Coca‑Cola Company in Canada will utilize 100% recycled plastic by the beginning of 2024. This has boosted the recycled plastic material requirements for packaging, thus positively influencing the market.

- Overall, as per the market research analysis, plastic material for packaging, with its versatility, cost-effectiveness, and sustainability advancements, continues to be a dominant force, driving the segment.

The paper & cardboard segment is expected to grow at the fastest CAGR over the forecast period.

- Paper and cardboard are widely used in packaging due to their versatility, cost-effectiveness, and sustainability. Paper is made from wood pulp, while cardboard is a thicker, more rigid material, made by layering paper. These materials are commonly used in packaging for food, retail products, and shipping.

- Paper and cardboard are biodegradable, recyclable, and made from renewable resources, making them eco-friendly alternatives to plastic packaging. They are lighter than other materials, reducing shipping costs and energy consumption during transportation.

- Moreover, paper and cardboard are easily printed on, offering branding accessibility with high-quality graphics and text. Additionally, cardboard, in particular, provides excellent cushioning, ensuring the safe transportation of goods. Also, paper and cardboard are affordable, making them accessible for businesses of all proportions.

- As per the market research analysis, the segment of paper and cardboard for the upcoming years is driven by the increasing consumer awareness of sustainability, the expansion of e-commerce, and the rising need for convenient packaging solutions.

By Packaging Type:

The packaging type segment is categorized into primary packaging, secondary packaging, and tertiary packaging.

Trends in the Packaging Type

- Integration of smart packaging technology on materials.

- Increasing focus on versatile and lightweight flexible packaging for various products.

The primary packaging segment accounted for the largest market share in 2023.

- Primary packaging refers to the material that directly surrounds and protects the product itself. It is the first point of contact between the product and the consumer, typically including bottles, cans, jars, and blister packs.

- Materials used for primary packaging protect products from air, light, moisture, bumps, and vibrations. This helps to preserve food, ensure food safety, and maintain the integrity of the other products.

- Furthermore, primary packaging serves as the main driver of brand identity, with customized designs enhancing consumer recognition and differentiation in the market. Aging populations, increasing health consciousness, and advancements in technology have led to the rising food and healthcare sector.

- For instance, in 2022, the total healthcare spending in the S. increased to USD 4.5 trillion, which is a 4.1% increase from the previous year. A significant share of this amount is allocated to medical devices and pharmaceutical products. This drives the need for materials for primary packaging for pharmaceutical products, medical devices, and diagnostic kits.

- Overall, rising healthcare and food sectors initiate the need for innovative and sustainable primary packaging solutions, driving the segment in the packaging materials Industry.

The secondary packaging segment is expected to grow at the fastest CAGR over the forecast period.

- Secondary packaging is a layer of packaging that groups multiple primary packages together or holds products together. It's designed to protect the product and primary packaging and to make it easier to handle, store, and transport.

- Common materials used for secondary packaging include corrugated cardboard, plastic films (shrink wrap, stretch wrap), and paperboard. These materials have various advantages such as durability, shock absorption, moisture resistance, and cost-effectiveness.

- Additionally, secondary packaging is customized with branding and marketing messages, enhancing product visibility and brand recognition.

- As economies grow and more people move to urban areas, there is a greater requirement for a wide range of consumer goods.

- For instance, according to the Bureau of Labor Statistics, average yearly spending for all consumer goods rose by 9.0 percent from 2021 to 2022, which is comparable to the 9.1 percent rise observed from 2020 to 2021.

- Overall,the increasing demand for consumer goods, coupled with the need for efficient and protective packaging, will drive the segment in the market for the upcoming years.

By End-User Industry:

The end-use industry segment is categorized into food and beverage, healthcare & pharmaceuticals, consumer goods, personal care & cosmetics, electrical & electronics, and others.

Trends in End-Use Industry:

- The E-commerce boom is driving the adoption of durable and protective packaging for shipping.

- The industrial sector requires robust and corrosion-resistant packaging.

The food & beverage segment accounted for the largest market share in 2023.

- Various materials, such as plastic, glass, metal, paper, and biodegradable options, are employed in food and beverage packaging to ensure product safety, freshness, and consumer appeal while considering factors such as cost-effectiveness, sustainability, and regulatory compliance.

- Glass is inert, impermeable to gases and vapors, and a neutral oxygen barrier. It's used for liquids and acidic foods. Moreover, paper is used for dry goods. Premium products use elegant paper packaging. Additionally, metal cans are used for canned goods.

- Also, materials such as compostable trays or vacuum-sealed pouches ensure freshness and prevent spoilage. Advancements in food technology and packaging have enabled longer material quality, positively driving the segment.

- For instance, in November 2024, UPM Specialty Papers and Eastman launched a new recyclable paper-based food packaging material with a compostable biopolymer coating. Thus, the rising adoption of sustainable materials in the sector for packaging will require these innovative solutions, driving the segment.

- Overall, the analysis indicates that the increasing need for sustainable and innovative packaging solutions, coupled with the growing food and beverage sector, is driving the segment.

The healthcare & pharmaceuticals segment is expected to grow at the fastest CAGR over the forecast period.

- The healthcare and pharma sector encompasses the production and distribution of medicines and medical devices.

- Packaging materials are crucial in this sector, ensuring product safety, efficacy, and patient compliance.

- They protect against contamination, moisture, light, and temperature fluctuations. Materials such as glass, plastic, and paperboard are commonly used. Glass offers excellent barrier properties, while plastics provide flexibility and durability.

- Paperboard is used for secondary packaging and labeling. These materials contribute to product integrity, brand recognition, and patient convenience.

- Aging populations, increasing prevalence of chronic diseases, technological advancements in drug discovery and delivery, and growing healthcare expenditure have led to growth in the healthcare and pharma sectors.

- Additionally, rising consumer awareness of health and wellness, coupled with stricter regulatory standards, is further propelling the growth of this sector. This will require packaging solutions for the future, driving segment in the upcoming years.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

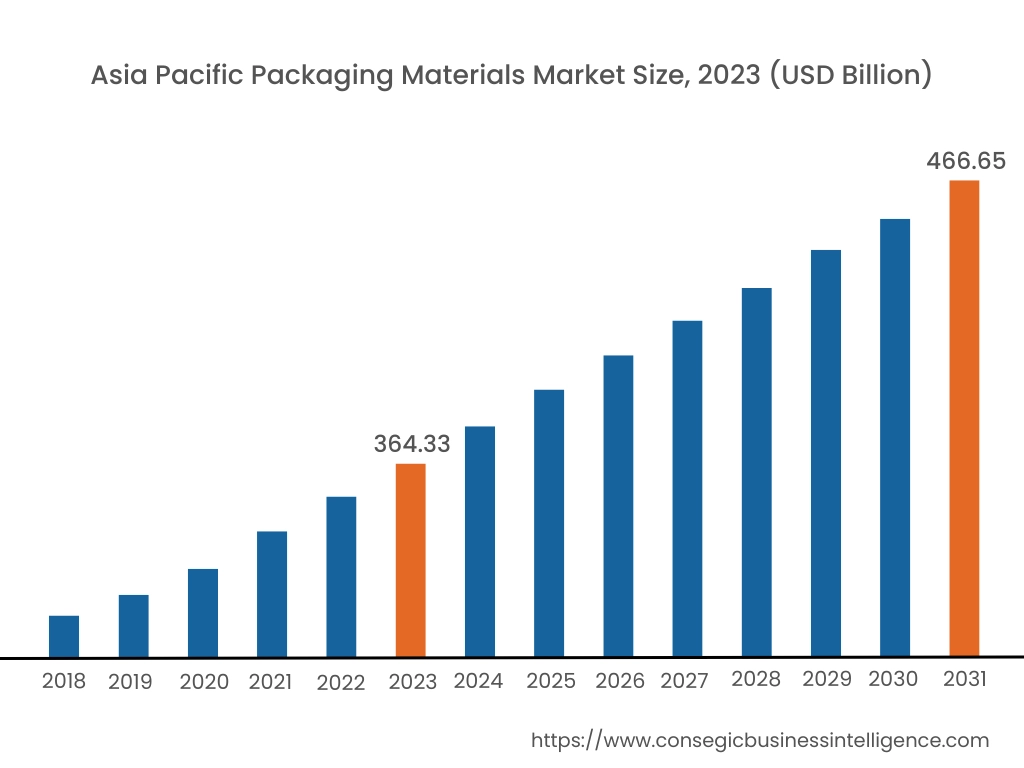

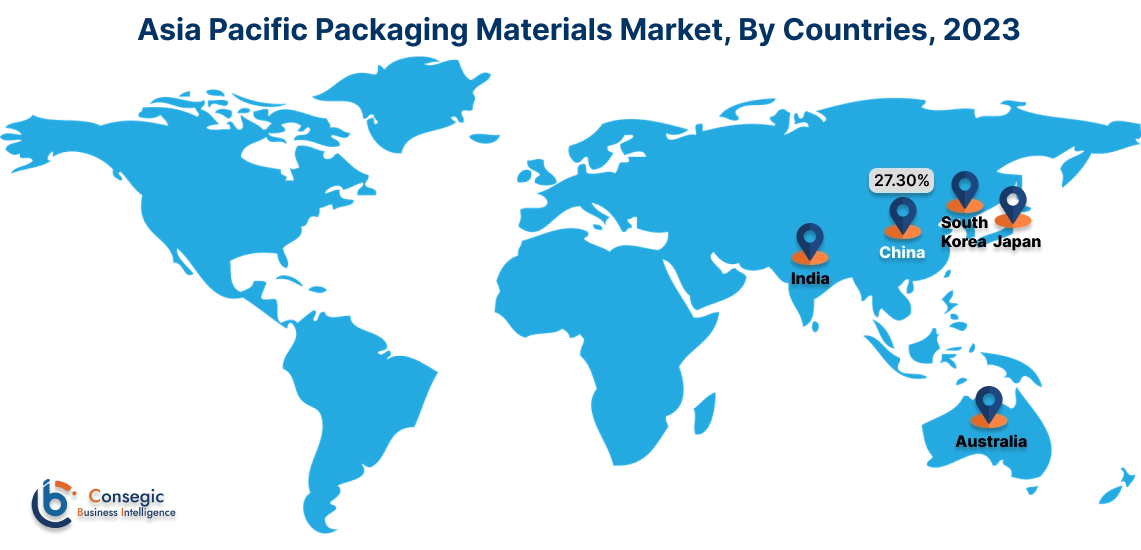

In 2023, Asia Pacific accounted for the highest packing materials market share at 42.05% and was valued at USD 364.33 Billion and is expected to reach USD 466.65 Billion in 2031. In Asia Pacific, China accounted for the highest packing materials market share of 27.30% during the base year of 2023. Countries such as China and India are experiencing rapid economic growth, leading to increased consumer spending and the need for packaged goods, driving the market. Moreover, the growing middle class in these countries is driving the adoption of branded and packaged products. Additionally, urbanization is leading to a shift towards packaged food and beverages.

- For instance, according to The Hindu, a newspaper company in India, in 2023, the market revenue of India's packaged food sector will grow at a rate of 14% CAGR from 2023 to 2029. This provides a lucrative opportunity, as people have less time for cooking and prefer convenience, there is increased demand for packed foods, influencing the need for materials for packaging, further boosting the market in the region.

Furthermore, lower labor costs in the region make it a cost-effective manufacturing hub for packaging materials. Overall, the rapid economic growth, rising middle class, urbanization, and increasing adoption of packaged goods in the Asia-Pacific region, are driving the market in the region.

In Europe, the packaging materials market is experiencing the fastest growth with a CAGR of 3.8% over the forecast period. The market is driven by several trends. The region has stringent regulations regarding packaging waste and sustainability, compelling manufacturers to adopt eco-friendly packaging solutions. Moreover, Europe boasts a well-developed manufacturing infrastructure, including a strong presence in the chemical and paper sectors. This provides a solid foundation for the production of diverse materials for packaging. Additionally, Europe is a hub for research and development in packaging technologies. Significant investments are made in developing advanced materials and packaging solutions that improve product protection, reduce waste, and enhance consumer experience.

North American packaging materials market analysis states several trends are responsible for the progress of the market in the region. The surge in online shopping has led to increased demand for efficient and protective packaging solutions. Moreover, consumers and businesses are increasingly prioritizing eco-friendly packaging options, driving the adoption of recyclable and biodegradable materials. Additionally, the region's thriving food and beverage sector necessitates innovative packaging solutions to maintain product freshness and extend shelf life. Furthermore, the integration of advanced technologies such as automation and smart packaging is enhancing efficiency and security within the packaging sector.

The Middle East and Africa (MEA) packaging materials market analysis states that this region is also witnessing a notable surge. The e-commerce sector is booming in the region, requiring innovative packaging materials to ensure product safety and customer satisfaction during shipping and delivery. Additionally, the MEA region has a diverse industrial landscape, including food and beverage, pharmaceuticals, and cosmetics, all of which require materials for packaging, further boosting the segment in the region. In addition to that, governments in several MEA countries are implementing policies to promote sustainable packaging practices, which is driving the adoption of eco-friendly materials.

In Latin America, the packaging materials market size is growing due to several trends. The surge in e-commerce and retail demand, driven by the region’s rising internet penetration and urbanization is the primary driver. By 2024, the Latin American e-commerce market exceeded USD 150 billion, requiring innovative packaging solutions to cater to online retail logistics. Moreover, the food and beverage sector, which accounts for over 40% of packaging consumption in the region, is experiencing robust growth, particularly in flexible and sustainable packaging formats. The increasing focus on sustainable materials, such as biodegradable plastics and recycled paper, is another driver.

Top Key Players & Market Share Insights:

The packaging materials market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global packaging materials market. Key players in the packaging materials industry include-

- Amcor Plc (Australia)

- Berry Global (U.S.)

- Sealed Air Corporation (U.S.)

- Tetra Pak (Switzerland)

- Sonoco Products Company (U.S.)

- ProAmpac (U.S.)

- Mondi Plc (UK)

- UPM-Kymmene Corp (Finland)

- Ball Corp (U.S.)

- WestRock Co. (U.S.)

- Crown Cork & Seal Co (U.S.)

Recent Industry Developments :

Product Launch:

- In October 2024, Mondi launched a new alternative to conventional free film paper bags for the construction sector. The company has unveiled its IntegoBag, which serves as an alternative to free film paper bags commonly utilized in the construction sector, claiming to cut plastic usage by as much as 50% while also preserving the shelf life of construction materials with its protective barrier coatings.

- In July 2024, ProAmpac, a frontrunner in flexible packaging and material science, unveiled its cutting-edge ProActive Recyclable Fresh Tray FT-1000. This revolutionary, patent-pending polypropylene tray is designated as plastic #5 and is certified for curbside recycling.

Packaging Materials Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 1,107.65 Billion |

| CAGR (2024-2031) | 3.1% |

| By Material Type |

|

| By Packaging Type |

|

| By End-Use Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Packaging Materials market? +

In 2023, the Packaging Materials market is USD 866.43 Billion.

Which is the fastest-growing region in the Packaging Materials market? +

Europe is the fastest-growing region in the Packaging Materials market.

What specific segmentation details are covered in the Packaging Materials market? +

Material Type and Packaging Type segmentation details are covered in the Packaging Materials market

Who are the major players in the Packaging Materials market? +

Amcor Plc (Australia), Berry Global (U.S.), Mondi Plc (UK), UPM-Kymmene Corp (Finland), Ball Corp (U.S.), WestRock Co. (U.S.), Crown Cork & Seal Co (U.S.), Sealed Air Corporation (U.S.), Tetra Pak (Switzerland), Sonoco Products Company (U.S.), and ProAmpac (U.S.)