- Summary

- Table Of Content

- Methodology

Orthopedic Implants Market Size:

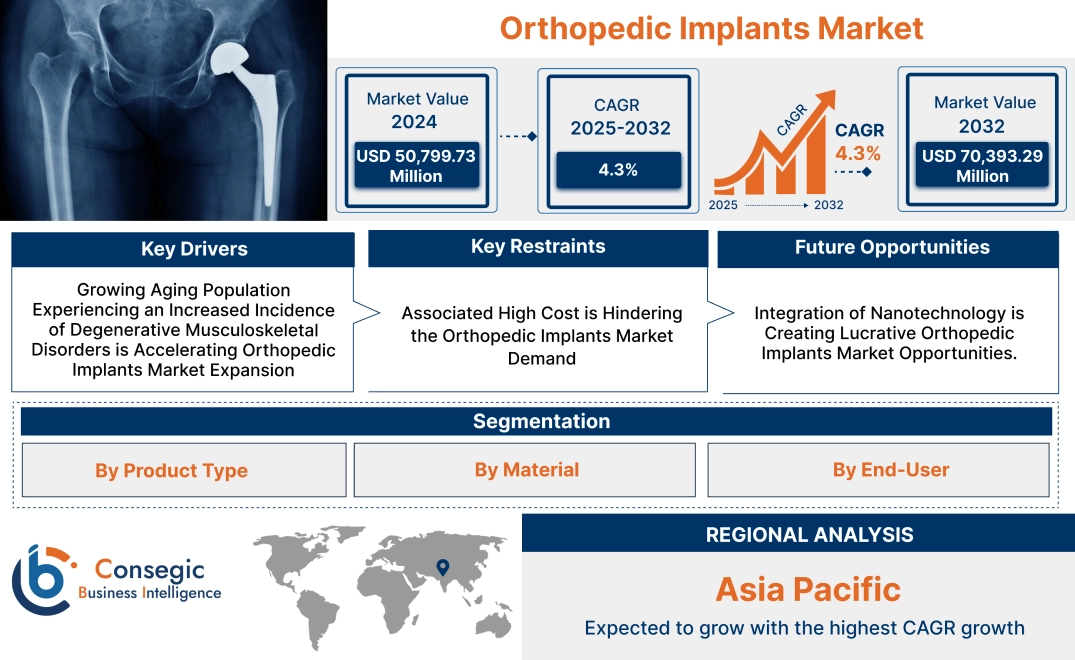

Orthopedic Implants Market size is growing with a CAGR of 4.3% during the forecast period (2025-2032), and the market is projected to be valued at USD 70,393.29 Million by 2032 from USD 50,799.73 Million in 2024.

Orthopedic Implants Market Scope & Overview:

Orthopedic implants are medical devices designed to replace or repair damaged or missing parts of the musculoskeletal system. This includes bones, joints, ligaments, and tendons. They are used to restore function, alleviate pain, and improve the quality of life for individuals with various conditions. The global orthopedic implants market growth is expected to have significant progress, driven by several trends. An aging population worldwide is experiencing an increased incidence of degenerative musculoskeletal disorders, creating a rising need for joint replacement surgeries.

The market is segmented into various categories, including joint reconstruction (hip, knee, shoulder, and others), spinal implants, trauma implants trauma implants amongst others. Furthermore, based on material, the market is classified into metals and metal alloys (titanium and titanium alloys, stainless steel, cobalt-chromium alloys, and others), ceramics, polymers, and composites. Moreover, the market is bifurcated into hospitals, ambulatory surgical centers, orthopedic clinics, and research and academic institutions based on end users.

Key players in the market include established players such as Johnson & Johnson, Stryker, Zimmer Biomet, Medtronic, and Smith & Nephew amongst others. These companies are actively involved in research and development, strategic acquisitions, and collaborations to maintain their market leadership and introduce innovative products.

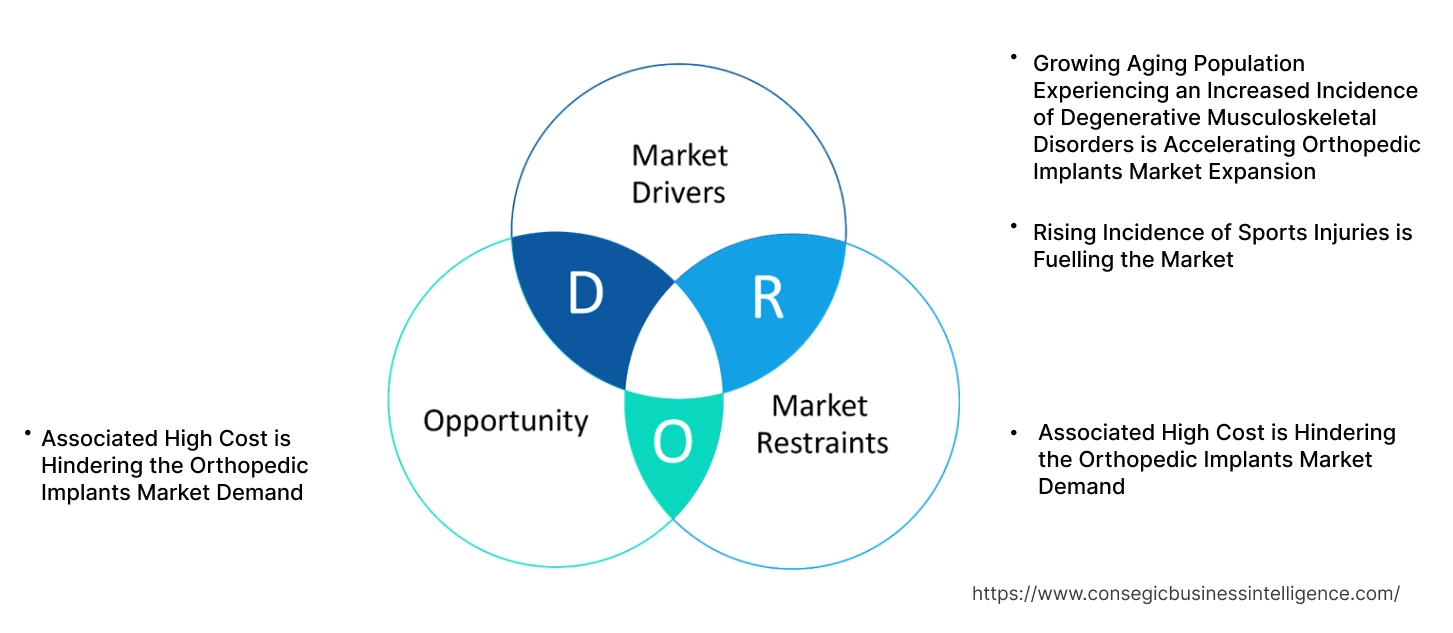

Orthopedic Implants Market Dynamics - (DRO) :

Key Drivers:

Growing Aging Population Experiencing an Increased Incidence of Degenerative Musculoskeletal Disorders is Accelerating Orthopedic Implants Market Expansion

Degenerative musculoskeletal disorders (MSDs) include a variety of conditions affecting the musculoskeletal system, including bones, joints, muscles, tendons, and ligaments. These disorders exert a substantial impact on individuals across all age groups, contributing significantly to global disability rates.

The escalating prevalence of MSDs is strongly correlated with an aging global demographic. Conditions such as osteoarthritis and osteoporosis exhibit a marked increase in incidence with advancing age. Furthermore, lifestyle factors, including obesity, sedentary behavior, and poor dietary habits, significantly elevate the risk of MSD development and progression.

- In 2022, the World Health Organization reported a global prevalence of approximately 1.71 Billion individuals living with musculoskeletal conditions. Furthermore, the organization highlighted that demographic shifts, such as population increase and aging, are exerting a significant and accelerating influence on the global burden of musculoskeletal conditions and associated functional limitations. This is positively influencing orthopedic implants market trends.

The impact of MSDs extends beyond individual health outcomes. These disorders frequently appear as chronic pain and functional limitations, adversely affecting an individual's capacity for work, social participation, and overall independence. Hence, the growing aging population experiencing an increased incidence of degenerative musculoskeletal disorders is accelerating the orthopedic implants market expansion.

Rising Incidence of Sports Injuries is Fuelling the Market

A sports injury is any type of bodily damage sustained during participation in athletic activities, whether competitive or recreational. These injuries can range from minor sprains and strains to more serious conditions like fractures and ligament tears. Increased participation in sports across all levels, from professional to recreational, coupled with the growing emphasis on fitness and active lifestyles, has led to a surge in sports-related injuries. Moreover, the increasing intensity and competitive nature of modern sports, particularly in high-impact sports like basketball, football, and soccer, further exacerbates the risk of injuries.

- In 2023, the National Safety Council reported that 3.7 million individuals globally sought treatment in emergency departments for injuries sustained while engaging in sports and recreational activities. It also stated that exercise, cycling, and basketball were among the activities most frequently associated with these injuries.

Hence, the growing prevalence of sports injuries is a significant factor driving the orthopedic implants market trends. Increased participation in sports across all levels, coupled with the growing emphasis on fitness and active lifestyles, has resulted in a notable increase in sports-related injuries.

Key Restraints:

Associated High Cost is Hindering the Orthopedic Implants Market Demand

The high cost of these implants presents a significant hurdle to access for many patients. These medical devices, such as artificial hips or knee replacements, are expensive. This high cost makes it difficult for many individuals to afford the necessary treatment, especially in countries with high healthcare costs.

This financial barrier not only impacts individual patients but also strains the healthcare system. Hospitals and clinics incur significant expenses when purchasing these expensive implants. This limits their resources and potentially impacts the overall quality of care they provide, further hampering orthopedic implants market demand.

- Knee replacement surgery in India typically costs between USD 3,900 and USD 9,500 per knee. If computer-assisted techniques are used, the cost can increase by an additional 5-10%.

Furthermore, even with health insurance, patients often face substantial out-of-pocket costs for these implants. This led to significant financial burdens for patients and their families, potentially impacting their ability to afford other essential needs.

Future Opportunities :

Integration of Nanotechnology is Creating Lucrative Orthopedic Implants Market Opportunities.

Nanotechnology is impacting the orthopedic implants market growth by enabling the incorporation of novel functionalities. Nanoparticles are utilized as delivery systems for growth factors that stimulate bone healing and minimize complications. Furthermore, these materials can be engineered to release medications, such as antibiotics, directly at the implant site, thereby reducing the risk of infection.

The ability to precisely control implant surface properties at the nanoscale offers unprecedented levels of customization. This allows for the development of implants tailored to specific patient needs and clinical situations, ultimately leading to improved patient outcomes. The integration of nanotechnology is offering significant innovation and creating lucrative orthopedic implants market opportunities.

- The Derwent World Patents Index revealed 301 patent applications for implants, including orthopedic implants, developed using nanotechnology.

In conclusion, the integration of nanotechnology is creating potential for the development of next-generation implants with enhanced performance, improved biocompatibility, and enhanced patient outcomes.

Orthopedic Implants Market Segmental Analysis :

By Product Type:

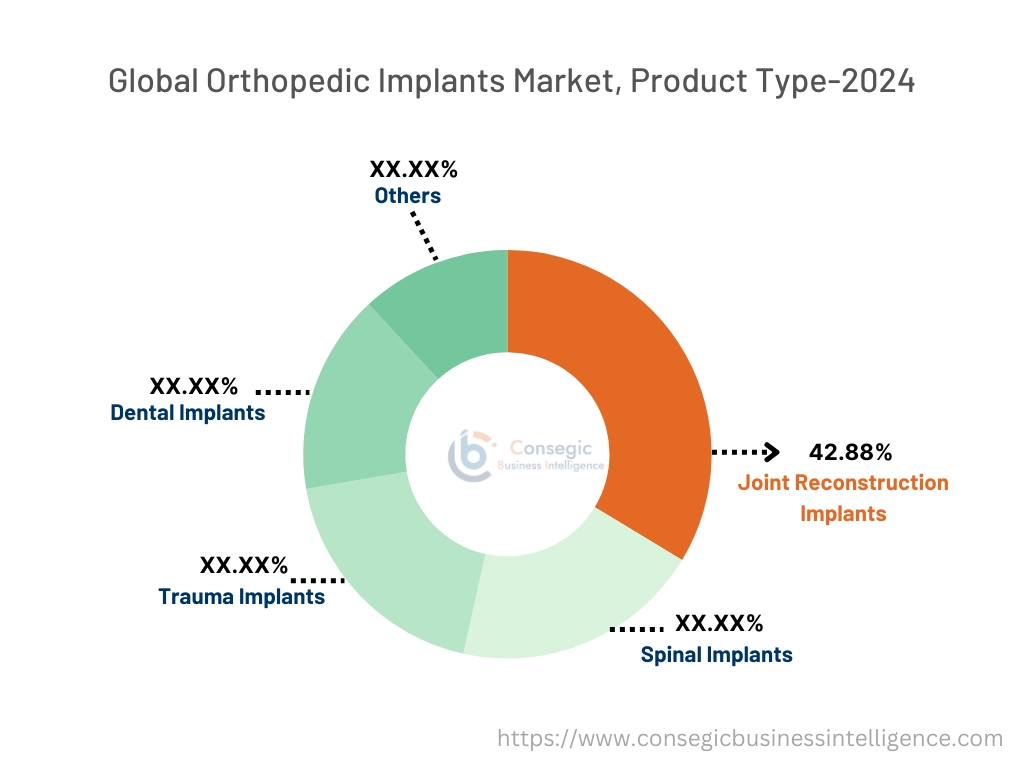

Based on product type, the market is categorized into joint reconstruction implants, spinal implants, trauma implants, dental implants, and others.

Trends in the Product Type:

- Demand for minimally invasive procedures like robotic-assisted surgery is increasing.

- 3D printing technology is gaining traction in the field of these implants, with the development of patient-specific implants becoming increasingly prominent.

The joint reconstruction implants segment accounted for the largest market share of 42.88% in 2024.

- Joint reconstruction implants are medical devices designed to replace damaged or diseased joints with artificial components. These implants aim to restore function, alleviate pain, and improve the quality of life for individuals suffering from conditions like osteoarthritis, rheumatoid arthritis, and trauma.

- Joint reconstruction implants are further classified into hip implants, knee implants, shoulder implants, and others.

- The segment’s dominance is due to several key factors. One of the key factors is the high prevalence of degenerative conditions like osteoarthritis, particularly within aging populations, which creates a significant requirement for joint replacement surgeries.

- In 2021, Zimmer Biomet launched Persona IQ, a smart knee implant. This innovative device incorporates sensors that capture crucial gait metrics, including functional knee range of motion, step count, and average walking speed. Notably, Persona IQ has received FDA approval for use as a knee replacement device. All these factors are driving segmental in the orthopedic implants industry.

The trauma implants segment is expected to grow at the fastest CAGR over the forecast period.

- Trauma implants are medical devices used to stabilize and repair broken bones (fractures). These implants are crucial for the successful treatment of various bone injuries, ensuring proper healing and restoring function.

- The rising incidence of trauma, driven by factors such as increased road accidents, sports injuries, falls, and workplace injuries, creates a substantial need for trauma implants.

- Additionally, the development of minimally invasive procedures for fracture fixation not only improves patient outcomes but also increases the need for these implants.

- Moreover, the aging population, with its increased susceptibility to fractures due to age-related bone density loss (osteoporosis), significantly contributes to the growing need for trauma implants.

- Furthermore, the development of innovative implant designs, such as locking plates and screws, enhances fracture stability and promotes faster healing, creating the potential for market.

By Material:

The material segment is categorized into metals and metal alloys, ceramics, polymers, and composites

Trends in the Material:

- Increasing use of ceramics in hip and knee replacements as bearing surfaces due to their low friction and wear characteristics.

- Growing focus on developing alloys with improved corrosion resistance, reduced wear and tear, and enhanced bio-integration.

The metals and metal alloys segment accounted for the largest market share in 2024.

- Metals and metal alloys are further classified into titanium and titanium alloys, stainless steel, cobalt-chromium alloys, and others. This dominance is from the inherent properties that make them well-suited for this critical application.

- Metals exhibit exceptional strength and durability, which are paramount for load-bearing implants that must withstand the stresses of daily activities within the human body. This ensures the longevity and reliability of the implant within the patient.

- Additionally, many metals and their alloys demonstrate excellent biocompatibility, minimizing the risk of adverse reactions within the human body. This is crucial for long-term implant success and patient well-being.

- For instance, MicroPort Orthopedics Inc., a global leader in orthopedic implants solutions, announced in 2024 the launch of Evolution Tibial Cones, a significant addition to its Evolution® Revision Knee System. These innovative cones, crafted from a titanium-based alloy, are specifically designed to address the critical challenges surgeons face during revision total knee arthroplasty (TKA) procedures, particularly in managing metaphyseal bone loss.

- Moreover, metals offer significant versatility in manufacturing. They are easily shaped and molded into a wide array of implant designs, catering to the diverse needs of various orthopedic procedures. These properties have established metals and metal alloys as the preferred choice for a wide range of orthopedic applications, including joint replacements, trauma implants, and spinal implants.

- Overall, as per the market analysis, metals and their alloys dominate the market due to their exceptional strength, durability, biocompatibility, and versatility in manufacturing, enabling the creation of reliable and effective implants for various orthopedic procedures.

The ceramics segment is expected to grow at the fastest CAGR over the forecast period.

- Ceramic implants, primarily made from materials like alumina and zirconia, are gaining significant traction in the market.

- This progress is primarily due to the exceptional wear resistance inherent to ceramic materials. Compared to traditional metal-on-metal or metal-on-polyethylene combinations, ceramics significantly minimize the generation of wear debris within the joint, thereby reducing the risk of complications like inflammation and pain.

- Additionally, market analysis states that the high biocompatibility of ceramics promotes excellent tissue integration and minimizes the risk of adverse reactions, enhancing patient outcomes and increasing patient satisfaction.

- Furthermore, the growing requirements for long-lasting and durable implants further fuel the adoption of ceramics, particularly in applications like hip and knee replacements where wear resistance is mandatory.

By End-User:

The end-user segment is categorized into hospitals, ambulatory surgical centers, orthopedic clinics, and research and academic institutions.

Trends in End-User:

- Increasing adoption of advanced technologies like robotics and AI in surgical procedures.

- Technological advancements enable more complex procedures to be performed in ASC settings.

- Increasing integration of technology, such as telemedicine and remote patient monitoring

The Hospitals segment accounted for the largest market share in 2024.

- Hospitals remain the dominant end-users within the market. This dominance stems from their comprehensive infrastructure, including advanced surgical suites, specialized equipment, and multidisciplinary teams, enabling them to effectively perform a wide range of complex orthopedic procedures.

- Additionally, hospitals are at the forefront of adopting advanced technologies, such as robotic-assisted surgery systems and image-guided navigation systems, which enhance surgical precision and improve patient outcomes.

- Moreover, hospitals are also uniquely positioned to handle complex cases that require specialized expertise and advanced surgical techniques.

- For instance, according to Curvo Labs, Inc., approximately 2 million hip and knee implant procedures were performed in the United States, with a majority of these procedures conducted within hospital settings.

- Furthermore, hospitals prioritize comprehensive patient care, encompassing pre-operative evaluation, surgical intervention, and post-operative rehabilitation, ensuring optimal patient outcomes.

- Thus, according to market analysis, hospitals remain the dominant end-users in the market due to their advanced infrastructure, access to specialized technologies, ability to handle complex cases, and focus on comprehensive patient care.

The orthopedic clinics segment is expected to grow at the fastest CAGR over the forecast period.

- Orthopedic clinics are expected to grow considerably within the market. This increase is driven by several key factors.

- The increasing emphasis on outpatient care, coupled with advancements in minimally invasive surgical techniques, is shifting the focus towards less invasive settings for orthopedic procedures.

- Moreover, the specialization of orthopedic clinics, along with the adoption of advanced technologies and a strong focus on patient-centered care, are contributing to the segment.

- Orthopedic clinics prioritize patient-centered care. They often provide personalized treatment plans, dedicated patient education programs, and comprehensive rehabilitation services, fostering a more patient-centric approach to care.

- These factors collectively contribute to the anticipated rapid increase of the orthopedic clinics segment within the market.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

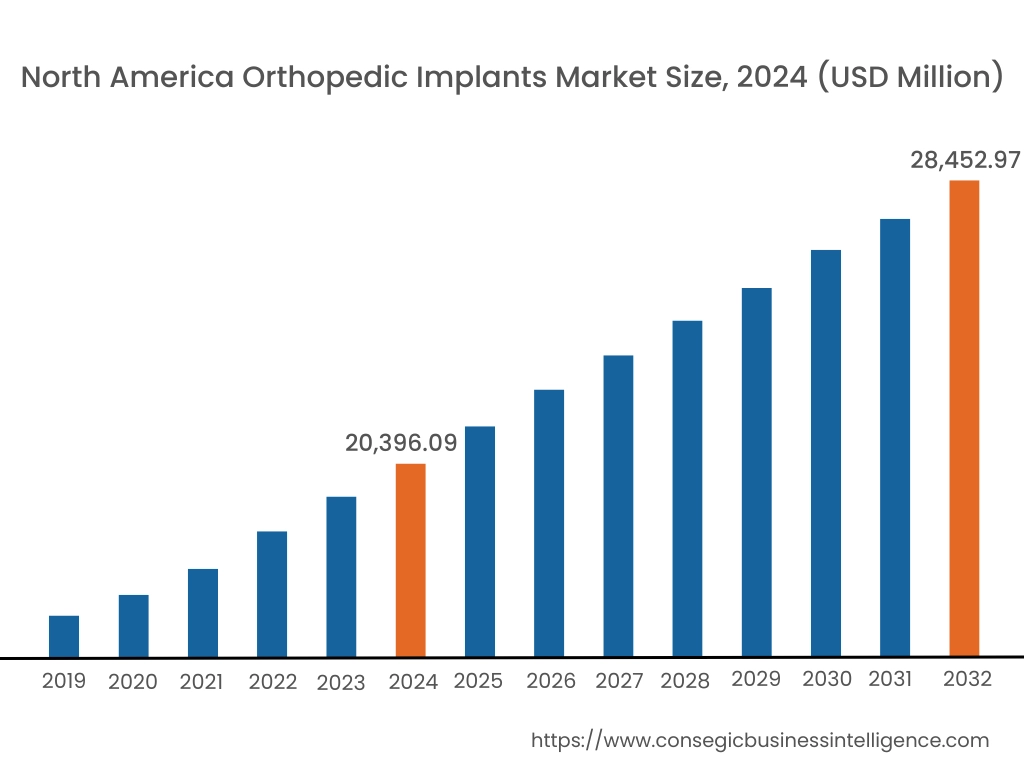

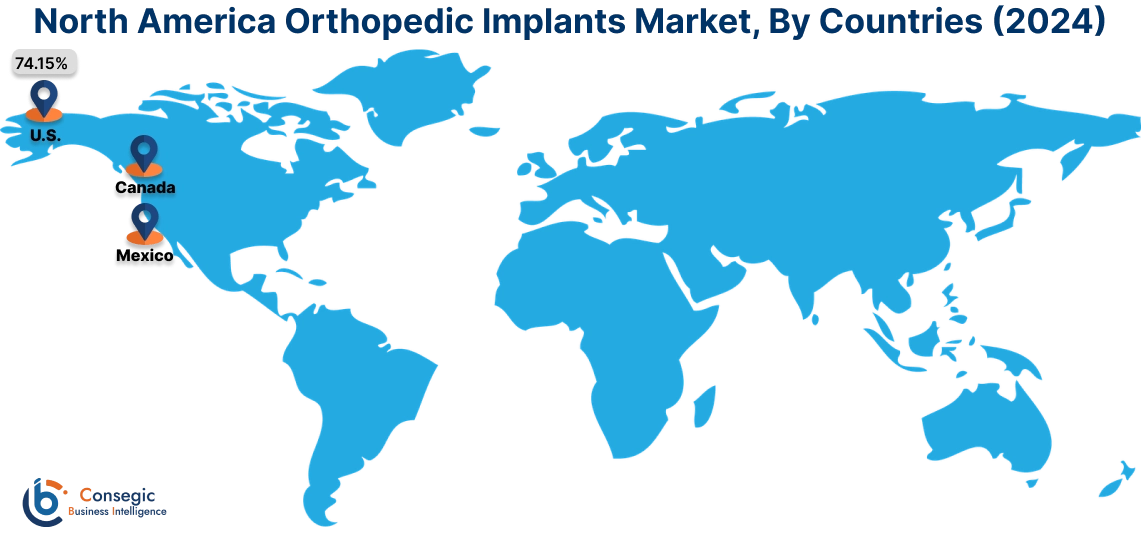

In 2024, North America accounted for the highest orthopedic implants market share at 40.15% and was valued at USD 20,396.09 Million and is expected to reach USD 28,452.97 Million in 2032. In North America, the U.S. accounted for the highest orthopedic implants market share of 74.15% during the base year of 2024.

North America currently dominates the global orthopedic implants market. This dominance is attributed to several key factors. The region boasts a well-developed healthcare infrastructure with advanced medical facilities, skilled surgeons, and access to cutting-edge technologies, facilitating the adoption and utilization of advanced implants. Additionally, North America experiences a high prevalence of musculoskeletal disorders, such as osteoarthritis and sports injuries, driving a significant demand for orthopedic interventions, including implant surgeries. Furthermore, the region is a hub for medical innovation, with significant investments in research and development of new implant technologies, materials, and surgical techniques.

- In 2023, Johnson & Johnson MedTech (US) received 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its TriLEAP System. This system encompasses a variety of specially shaped and standard plates designed to accommodate different screw ranges. Additionally, it includes instruments for reducing, fixing, and fusing bone fragments during surgical procedures.

Finally, the strong presence of leading manufacturers within North America, coupled with relatively comprehensive healthcare coverage in many parts of the region, further contributes to the market's dominance.

Asia Pacific, the nuclear imaging devices market is experiencing the fastest growth with a CAGR of 4.9% over the forecast period. The Asia Pacific region is experiencing a significant and rapidly aging population. This demographic shift leads to a surge in age-related musculoskeletal conditions such as osteoarthritis and osteoporosis, consequently increasing the demand for joint replacement surgeries and other orthopedic interventions. Additionally, the rise in lifestyle-related diseases, such as obesity and diabetes, within the Asia Pacific region is contributing to an increase in musculoskeletal disorders. Moreover, the region is witnessing substantial economic increase in many countries. This translates to increased healthcare spending and improved access to healthcare services. Coupled with growing awareness about the benefits of advanced orthopedic treatments and technologies, this economic development is fueling the market in the Asia Pacific region.

The European orthopedic implants market analysis states that several trends are responsible for the progress of the market in the region. The aging demographic within Europe leads to a surge in age-related musculoskeletal disorders like osteoarthritis and osteoporosis, creating a substantial need for joint replacements and other orthopedic interventions. This demographic shift, coupled with a well-developed healthcare infrastructure featuring advanced medical facilities and skilled surgeons, fosters a conducive environment for the adoption and utilization of advanced orthopedic implants. Furthermore, Europe boasts a robust regulatory framework for medical devices, ensuring high standards of safety and efficacy. This stringent regulatory environment encourages innovation and drives the development of cutting-edge orthopedic implant technologies. Additionally, significant investments in research and development within Europe contribute to advancements in implant materials, surgical techniques, and overall patient outcomes.

The Middle East and Africa orthopedic implants market analysis states that the region is also witnessing a notable surge region. Rapid population growth, particularly within younger demographics, is a key driver. This growing population, coupled with increasing urbanization and changing lifestyles, leads to a rise in sports injuries, trauma cases, and the emergence of lifestyle-related diseases such as obesity and diabetes, all of which contribute to the need for orthopedic interventions. Furthermore, significant investments in healthcare infrastructure and improvements in access to healthcare services are contributing to the market. However, several challenges hinder market penetration. Limited healthcare infrastructure in certain regions restricts access to quality care and advanced surgical facilities. Economic disparities within these regions create significant barriers to accessing necessary treatments for many individuals. Additionally, cultural and religious factors also influence healthcare decisions and access, potentially impacting the adoption of orthopedic implants.

The Latin American orthopedic implants market analysis states that the region is experiencing growth driven by several trends. The aging population is a key driver, leading to an increase in age-related conditions like osteoarthritis and osteoporosis. This necessitates a greater demand for joint replacement surgeries and other orthopedic interventions. Additionally, the rising prevalence of lifestyle diseases such as obesity and diabetes contributes to the development of musculoskeletal disorders. Furthermore, improvements in healthcare infrastructure and access to quality healthcare services are enabling better diagnosis and treatment of orthopedic conditions, driving the orthopedic implants market size. However, challenges remain, such as uneven healthcare access across the region and economic disparities that limit access to quality care for many patients.

Top Key Players and Market Share Insights:

The Orthopedic Implants Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global orthopedic implants market. Key players in the Orthopedic Implants industry include-

- Stryker Corporation (U.S.)

- Braun Melsungen AG (Germany)

- NuVasive Inc. (US)

- Orthopaedic Implant Company (US)

- Smith+Nephew (UK)

- Zimmer Biomet (US)

- CONMED Corporation (US)

- Globus Medical (US)

- Integra LifeSciences (US)

- Johnson & Johnson (US)

- Medtronic (Ireland)

Recent Industry Developments :

Product Launches:

- In 2024, Auxein launched a range of Innovative advanced Orthopedic and Arthroscopy Products. The range included AV-Wiselock Plates, Osteochondral Transfer System, Reusable Suture Passer, Ligament Augmentation Repair Instrument Set, Auxilock Silicon Cannula, Auxilock Rigid Threaded, Cannula, Reusable Suture Passer, Knee Escorpian Suture Passer, Bioabsorbable Interference screw, Bioabsorbable Anchors, GFS Ultimate Button with Brace/Tape System, etc.

- Globus Medical, Inc., a prominent player in musculoskeletal solutions, announces continued growth and expansion of its orthopedic trauma product portfolio. In 2024, Globus has introduced several new system extensions and received 510(k) clearance from the U.S. Food and Drug Administration for its TENSOR™ Suture Button System, its first suture-based product. Notably, the company has recently launched next-generation systems including ANTHEM™ II Distal Radius Volar Plates, AUTOBAHN™ Trochanteric Nail PRO Instruments, and CAPTIVATE™ SOLA Headless Screws.

Partnership:

- In 2024, Smith+Nephew (UK) entered into a partnership with Healthcare Outcomes Performance Company. This collaboration aimed to provide enhanced solutions for healthcare professionals, patients, and ambulatory surgery centers (ASCs) through the utilization of the Healthcare Outcomes Performance Company's digital and analytics platform.

Orthopedic Implants Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 70,393.29 Million |

| CAGR (2025-2032) | 4.3% |

| By Product Type |

|

| By Material |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Orthopedic Implants Market? +

In 2024, the Orthopedic Implants Market is USD 50,799.73 Million.

Which is the fastest-growing region in the Orthopedic Implants Market? +

Asia Pacific is the fastest-growing region in the Orthopedic Implants Market.

What specific segmentation details are covered in the Orthopedic Implants Market? +

Product Type, Material and End-User segmentation details are covered in the Orthopedic Implants Market.

Who are the major players in the Orthopedic Implants Market? +

Stryker Corporation (U.S.), Braun Melsungen AG (Germany), CONMED Corporation (US), Globus Medical (US), Integra LifeSciences (US), Johnson & Johnson (US), Medtronic (Ireland), NuVasive Inc. (US), Orthopaedic Implant Company (US), Smith+Nephew (UK), Zimmer Biomet (US).