- Summary

- Table Of Content

- Methodology

Orthodontic Headgear Market Size:

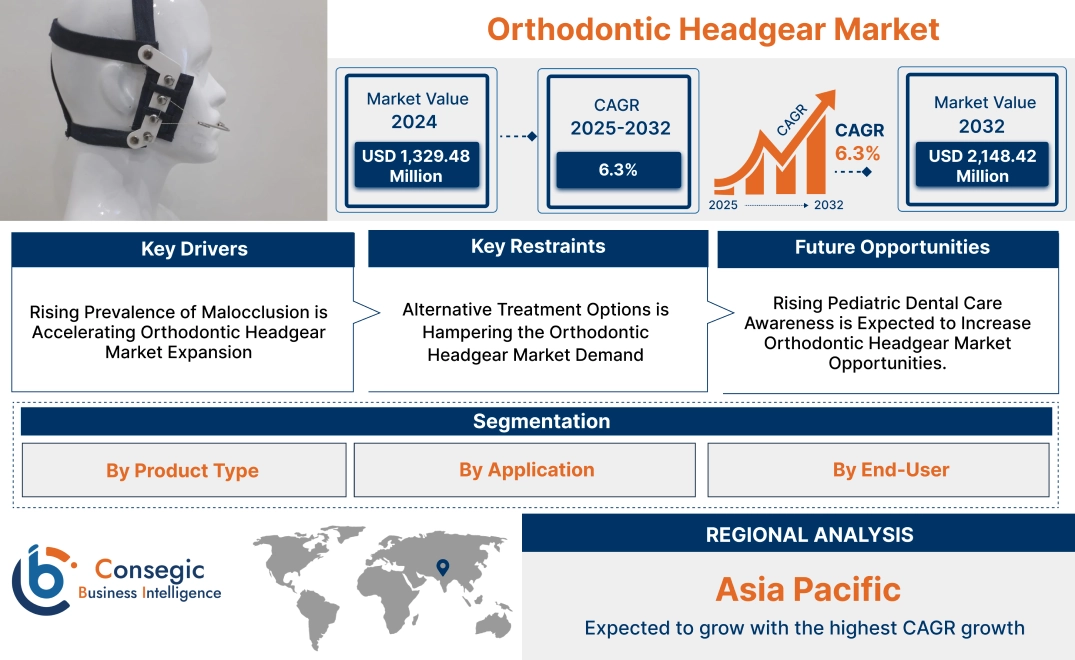

Orthodontic Headgear Market size is growing with a CAGR of 6.3% during the forecast period (2025-2032), and the market is projected to be valued at USD 2,148.42 Million by 2032 from USD 1,329.48 Million in 2024.

Orthodontic Headgear Market Scope & Overview:

Orthodontic headgear is a specialized dental appliance used to guide the development of the jaw in children and adolescents. It works by applying gentle and continuous pressure to the teeth and jaws, encouraging the jaw bones to align properly. Headgear typically consists of a headpiece with straps that attach to the head or neck. From this, a facebow extends to connect to the upper teeth via hooks and bands. This system exerts pressure on the upper molars, guiding their movement and influencing jaw development. The amount of wear time varies depending on the specific treatment plan, but typically ranges from 10-14 hours per day, and in some cases, up to 22 hours. This headgear is particularly effective in treating a variety of bite problems, including overjet, where the upper teeth protrude significantly beyond the lower teeth (often referred to as "buck teeth"), overbite, which occurs when the upper teeth excessively overlap the lower teeth, and underbite, a condition where the lower teeth protrude further than the upper teeth.

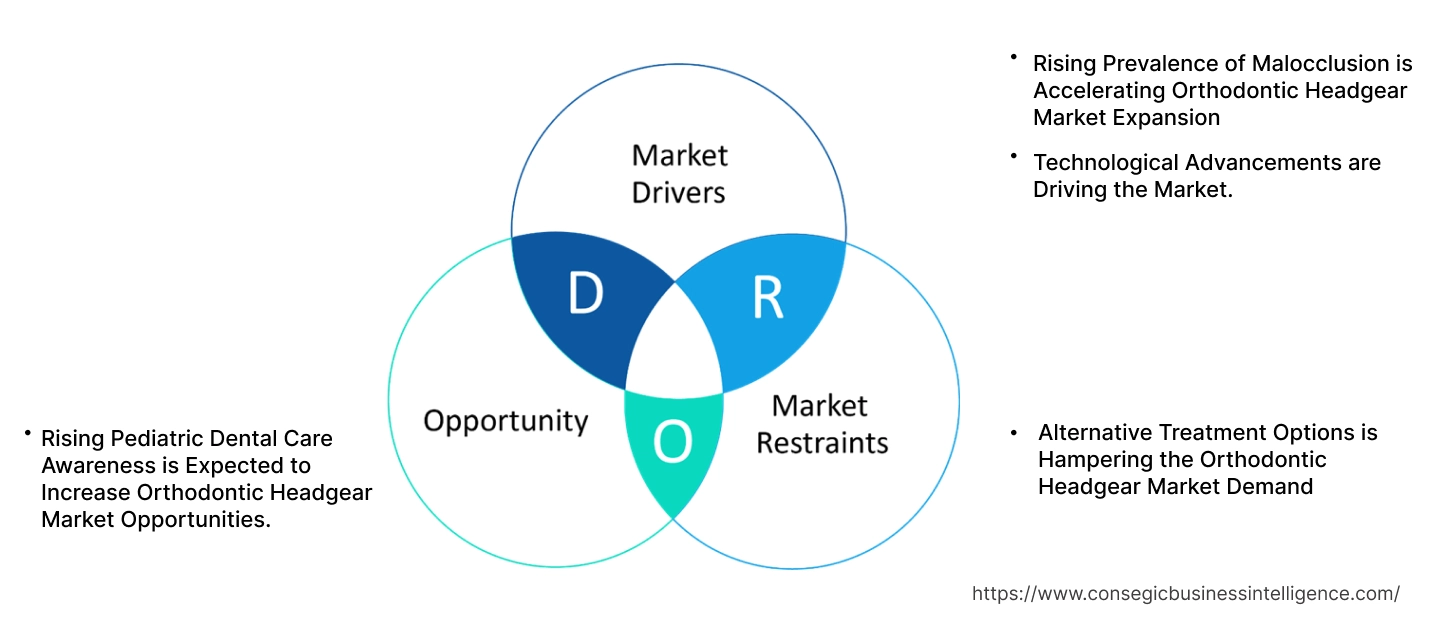

Orthodontic Headgear Market Dynamics - (DRO) :

Key Drivers:

Rising Prevalence of Malocclusion is Accelerating Orthodontic Headgear Market Expansion

Malocclusion, also known as a bad bite, is when the upper and lower teeth don't align properly when the mouth is closed. Headgear is primarily used in orthodontics to correct malocclusion by applying gentle pressure on the jaw. It effectively addresses issues such as class II malocclusion (overbite) by applying force to reposition the upper jaw backward, and class III malocclusion (underbite) by moving the lower jaw forward.

By correcting jaw alignment, headgear enhances facial aesthetics and profile symmetry. Moreover, by correcting malocclusion with headgear early on, the need for later jaw surgery is reduced. Genetics, poor oral habits during childhood, and early loss of primary teeth have led to an increased prevalence of malocclusion.

- According to an article published by the National Center for Biotechnology Information, in 2021, the WHO identifies malocclusion as a major oral health concern. Prevalence varies widely, affecting an estimated 39% to 93% of children and adolescents respectively. This has underscored the critical need for effective treatment options, positively influencing the orthodontic headgear market trends.

Overall, the high prevalence of malocclusion is significantly boosting the orthodontic headgear market expansion.

Technological Advancements are Driving the Market.

Orthodontic headgear has seen significant technological advancements. Traditional headgear has been replaced by models made from advanced materials such as titanium alloys and medical-grade plastics, reducing discomfort and improving patient compliance. Moreover, modern designs prioritize comfort, aesthetics, and efficiency.

- According to an article published by Families First Pediatrics, in 2023, modern headgear has evolved into more discreet and patient-friendly designs, featuring a thin wire framework with minimal supporting architecture, representing a significant departure from older, bulkier versions.

Additionally, digital technologies, including 3D imaging and computer-aided design (CAD), have revolutionized headgear customization. Orthodontists now create devices tailored to each patient’s anatomy, enhancing effectiveness and reducing treatment time, positively influencing orthodontic headgear market trends. Furthermore, advancements in biomechanics have led to the development of dynamic force systems, which apply consistent and controlled pressure to align teeth and correct jaw discrepancies. Also, the integration of smart technologies is another breakthrough. Some headgear now incorporates sensors to monitor wear time and provide real-time feedback to patients and orthodontists.

Overall, technological advancements, including the use of advanced materials, digital technologies, and innovative force systems are accelerating the global orthodontic headgear market growth.

Key Restraints:

Alternative Treatment Options is Hampering the Orthodontic Headgear Market Demand

The emergence of alternative orthodontic treatment options poses a significant restraint on the market. These include the herbst appliance, which stimulates jaw development by restricting lower jaw movement; the twin block appliance, which gently expands the upper and lower jaws; bionators, which guide jaw development by stimulating natural jaw movements.

Apart from all these, there are orthopedic correctors, designed to correct jaw development during childhood; MARA's (maxillary arch rapid expanders), which expand the upper jaw to correct crossbite; the jasper jumper, which promotes forward development of the upper jaw; and the forsus, which corrects overbites by gently pushing the upper molars back.

Perhaps the most recent advancement is the use of temporary anchorage devices (TADs). These are small screws surgically placed into the bone to provide a stable anchor point for orthodontic forces. TADs effectively achieve the same tooth movement as headgear without the need for external headgear components. These alternative approaches offer varying levels of comfort, convenience, and aesthetic appeal compared to traditional headgear.

Overall, analysis shows that the emergence of alternative orthodontic treatments presents a competitive landscape for traditional headgear, hampering the orthodontic headgear market demand.

Future Opportunities :

Rising Pediatric Dental Care Awareness is Expected to Increase Orthodontic Headgear Market Opportunities.

The rising awareness of pediatric dental care is creating potential for the market. Parents are now more informed about the long-term benefits of addressing dental issues early, such as preventing cavities, malocclusion, and gum diseases. This increasing emphasis on early oral health for their children has led to heightened demand for preventive and corrective dental services for children, including headgear requirements for jaw alignment issues.

Moreover, public health campaigns, school programs, and pediatrician recommendations have further amplified the requirements for specialized dental care for children, creating potential for headgear as it effectively guides jaw growth and facial development. Additionally, government initiatives aimed at improving children's access to dental care, prioritizing oral health, and rectifying existing issues will positively impact the market.

- The UK government announced in 2024, that they will launch "Smile for Life," a comprehensive initiative dedicated to promoting oral health and preventive measures in young children. This initiative will have an impact in the two upcoming years, resulting in earlier identification and intervention of malocclusion issues, thus increasing the need for orthodontic treatments such as headgear, creating the potential for the market.

Overall, the rising awareness of pediatric dental care, coupled with government initiatives is expected to increase orthodontic headgear market opportunities.

Orthodontic Headgear Market Segmental Analysis :

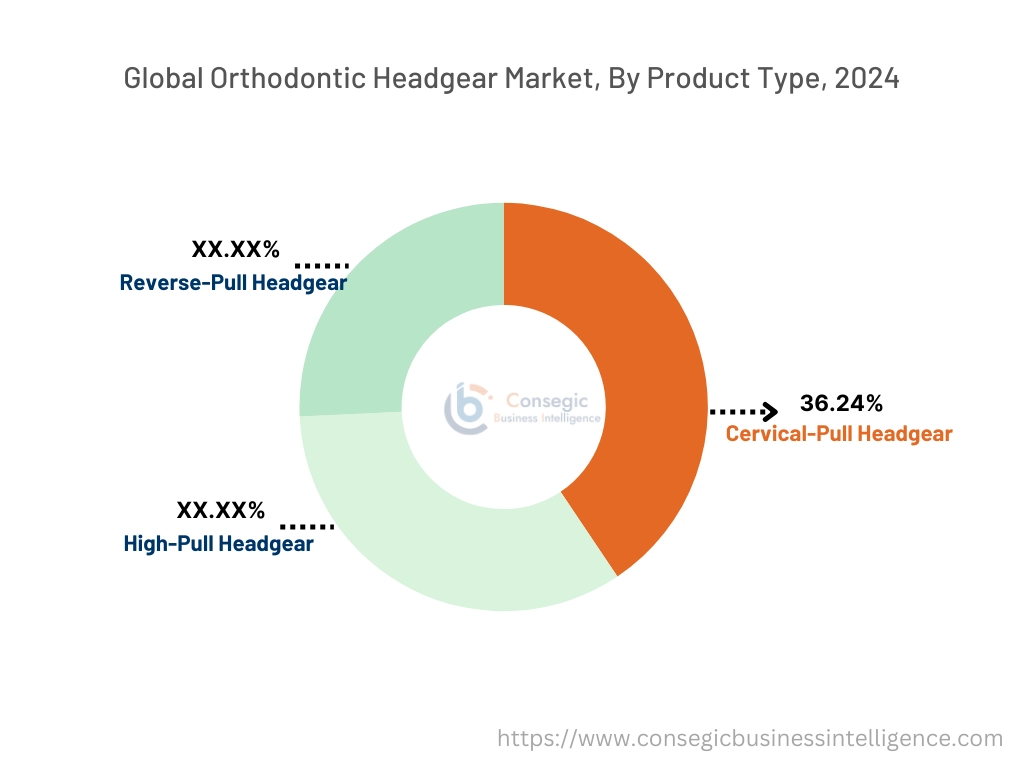

By Product Type:

Based on product type, the market is categorized into cervical-pull headgear, high-pull headgear, and reverse-pull headgear.

Trends in Product Type:

- Integration of advanced materials for durability and aesthetics.

- Customization options to better suit individual patient needs.

The cervical-pull headgear segment accounted for the largest market share of 36.24% in 2024.

- Cervical pull headgear is an orthodontic device used to correct an overbite or overjet in children and adults. It consists of a U-shaped wire, called a facebow, that attaches to the upper back teeth. A strap connects to the facebow and goes around the neck.

- This system applies downward and backward force to the upper molars, guiding them back into proper alignment. It also helps in tooth spacing after tooth extraction. Children wear this headgear for at least 14 hours a day.

- By guiding the alignment of the jaws, cervical pull headgear fosters a more balanced bite and improved facial aesthetics. This, in turn, contributes to enhanced self-esteem and overall quality of life for patients, positively impacting market trends.

- Overall, as per the market analysis, the rising prevalence of class II malocclusion (overbite), increased awareness of orthodontic treatment options, and advancements in headgear design and materials are driving the segment in the global orthodontic headgear market growth.

The high-pull headgear segment is expected to grow at the fastest CAGR over the forecast period.

- High-pull headgear, similar to cervical-pull headgear, treats overjet and overbite. However, it utilizes two head straps, one on the back and one on top, to exert upward and backward force on the upper jaw.

- High-pull headgear is particularly beneficial for cases where both vertical and horizontal control of the upper jaw is necessary. Moreover, this headgear is helpful in other orthopedic goals as well.

- For instance, according to a study published in the National Center for Biotechnology Information, in 2024, high-pull headgear adjusts anteroposterior skeletal connections and enhances or averts the deterioration of vertical skeletal connections.

- Additionally, by correcting the bite and influencing jaw development, high-pull headgear contributes to improved facial aesthetics and a more balanced facial profile.

- As per the market analysis, the increasing prevalence of malocclusion, particularly deep bites, in children and adolescents will drive the segment. Furthermore, the growing demand for aesthetic dentistry and the desire for straighter smiles further contribute to segmental growth for the forecasted years.

By Application:

The application segment is categorized into overbite, crossbite, underbite, and others.

Trends in the Application:

- Increased use of headgear for optimal overbitecorrection in growing children.

- Development of more comfortable and discreet headgear options for improved patient compliance in crossbite treatment.

The overbite segment accounted for the largest market share of 2024.

- Overbite occurs when your upper teeth excessively overlap your lower teeth, creating a vertical misalignment. This misalignment leads to various oral health problems, including jaw discomfort, tooth wear, and gum disease if not addressed.

- Headgear is an orthodontic appliance that is used to treat overbites, especially in growing children. It works by applying gentle pressure to the upper jaw, slowing its development and allowing the lower jaw to catch up. This helps to correct the bites and improve facial balance. The headgear also helps in putting less strain on jaw muscles which benefits oral health.

- For instance, according to an article published by Bateman Orthodontics, in 2023, headgear in overbite condition, also creates more space within the mouth. This allows teeth to shift into their proper positions, leading to a more aligned and aesthetically pleasing smile.

- Overall, as per the market analysis, rising awareness of cosmetic dentistry, and advancements in orthodontic treatment techniques are driving this segmental growth in the orthodontic headgear industry.

The underbite segment is expected to grow at the fastest CAGR over the forecast period.

- An underbite is a type of malocclusion where the lower front teeth protrude in front of the upper front teeth. This is caused by a variety of factors, including genetics, jaw growth, and thumb-sucking.

- Headgear works by applying gentle pressure to the upper jaw, gradually guiding it into the correct position.By starting treatment early, the headgear helps guide the development of the jaw.

- Additionally, correcting the underbite leads to a more balanced facial profile and a more confident smile. Furthermore, by addressing the underbite early with headgear, the need for more invasive surgical procedures later in life is significantly reduced.

- Furthermore, correcting the bite with headgear improves speech clarity and chewing function, leading to better overall oral health and quality of life.

- Increased public awareness about the importance of oral health and the availability of effective underbite treatment options create the potential for the segment in the upcoming years.

By End User:

The end-user segment is categorized into hospitals, dental clinics, and others.

Trends in End-User:

- Hospitals are fostering collaboration between orthodontists, oral surgeons, and other specialists for comprehensive patient care.

- Dental clinics are increasingly adopting digital technologies such as 3D imaging and intraoral scanners to enhance treatment planning and patient communication.

The hospitals segment accounted for the largest market share in 2024 and is expected to grow at the fastest CAGR over the forecast period.

- Hospitals dominate the market due to their comprehensive infrastructure, multidisciplinary approach, and ability to handle complex cases. They are well-equipped to manage severe orthodontic issues, such as skeletal discrepancies or malocclusions that require intervention.

- Moreover, in regions with centralized healthcare systems, hospitals serve as primary points of care, making them the preferred choice for orthodontic treatments. Additionally, public hospitals offer affordable treatment options through insurance coverage or government programs, increasing accessibility for a broader population.

- Furthermore, remote consultations and monitoring potentially increase accessibility, reducing costs. Rising healthcare costs, technological advancements, growing diseases, and government regulations have led to increases in hospitals.

- For instance, according toCEIC, the number of hospitals in China increased by 3.85% from 2022 to 2023, rising from 36 million units to 38 million units. Consequently, this surge in hospitals has contributed to a higher volume of diagnostics and treatments related to overbites, underbites, and other issues concerning jaw and tooth alignment, leading to an increased need for headgear, positively influencing the market.

- Also, the rising awareness of early orthodontic intervention further supports hospitals’ dominance, as parents trust hospitals for pediatric care. The availability of advanced diagnostic tools, such as 3D imaging and comprehensive treatment planning, attracts patients seeking precision and reliability.

- Overall, the increasing number of hospitals, driven by factors such as population growth and healthcare advancements, creates a favorable environment for the market, thus driving the segment.

Regional Analysis:

The regional segment includes North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

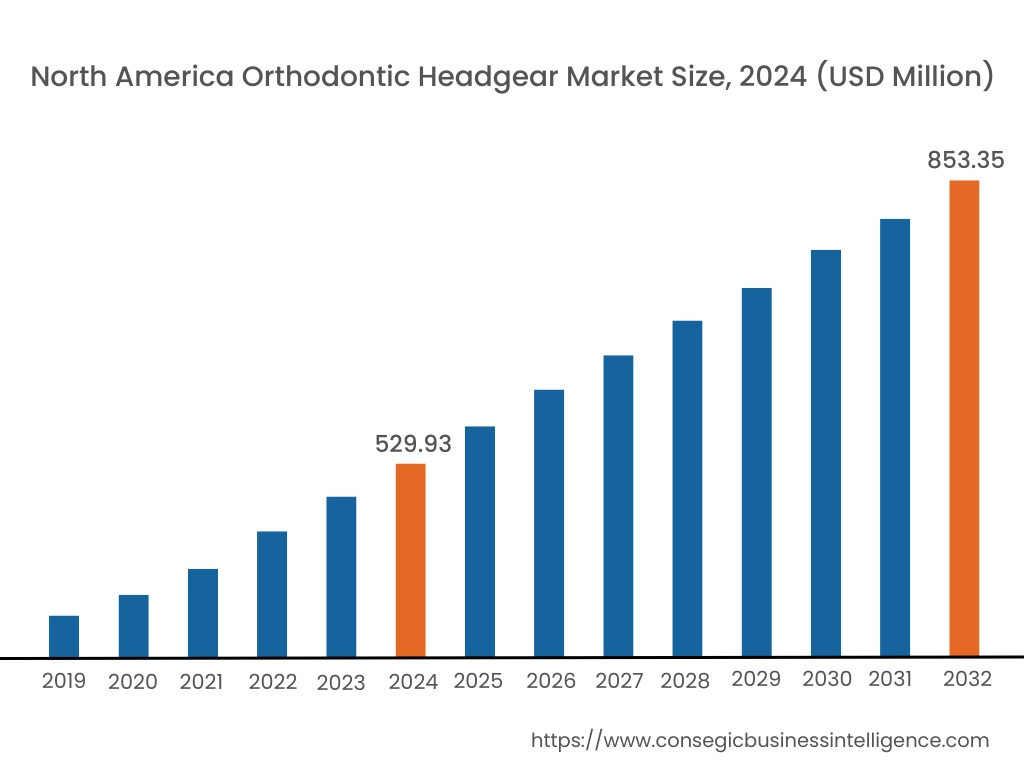

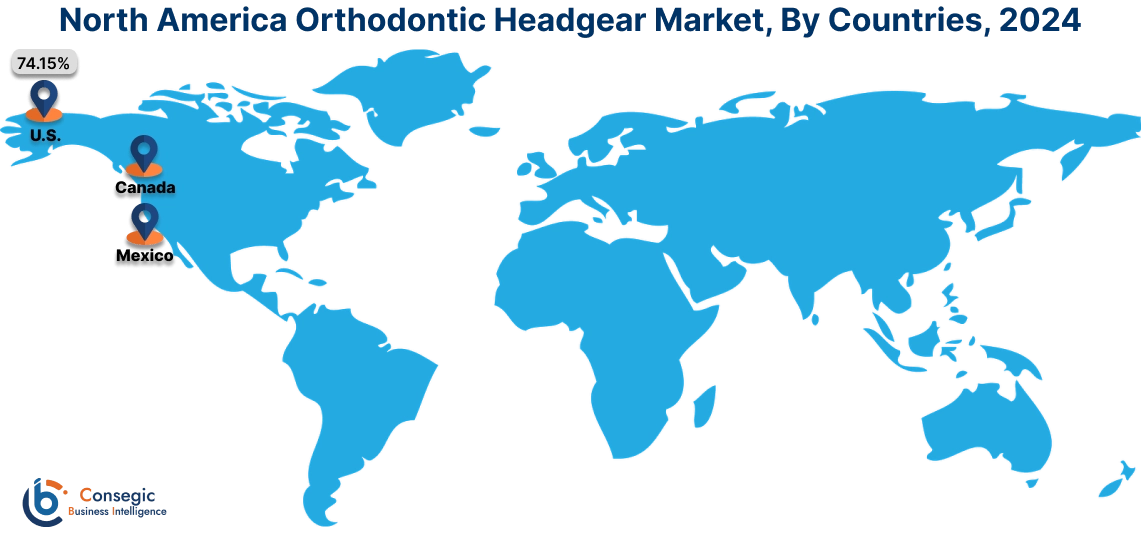

In 2024, North America accounted for the highest orthodontic headgear market share at 39.86% and was valued at USD 529.93 Million and is expected to reach USD 853.35 Million in 2032. In North America, the U.S. accounted for the highest orthodontic headgear market share of 74.15% during the base year of 2024. The region is dominated due to its advanced healthcare infrastructure and widespread adoption of cutting-edge technologies. Moreover, the region's well-established orthodontic practices and availability of skilled professionals contribute significantly to its leadership. In the U.S. and Canada, early intervention in dental care, especially among children, is a common practice, supported by robust public health campaigns. Additionally, there is increased awareness about orthodontic treatments in the region through various channels, including blogs, social media, and informative websites.

- Patuxent Orthodontics, published an article in 2023, explaining what orthodontic headgear is, the various types that are available, the advantages it offers, the conditions it treats, and the precautions to take while using it. This type of blog and articles have educated the public, encouraging them to seek professional orthodontic guidance, and positively influencing the demand for headgear.

Furthermore, insurance coverage and flexible payment plans further make treatments accessible to a wide demographic. The presence of major orthodontic device manufacturers fosters innovation that appeals to patients and practitioners alike. Overall, North America's dominance is attributed to a robust healthcare system, advanced technologies, early intervention practices, strong public awareness, and a favorable economic environment.

In Asia Pacific, the orthodontic headgear market is experiencing the fastest growth with a CAGR of 6.8% over the forecast period. A significant driver is the growing middle-class population in countries such as China, India, and Southeast Asia, which is increasingly prioritizing orthodontic treatments for children and adults, including headgear. Moreover, the region is witnessing a significant expansion of its healthcare infrastructure, with increased access to hospitals offering orthodontic services. The growing network of dental clinics is also making treatments more accessible, positively influencing the industry. Additionally, the rising trend of medical tourism in countries such as Thailand and Malaysia, where orthodontic treatments are offered at lower costs compared to Western markets, is another critical driver, attracting patients both domestically and internationally.

Europe's orthodontic headgear market analysis states that several trends are responsible for the progress of the market in the region. Countries such as Germany, France, and the UK have well-established orthodontic practices, with a strong focus on early intervention. Moreover, the region benefits from universal healthcare systems that subsidize or cover orthodontic treatments, enhancing accessibility. Additionally, the region is a hub for technological innovation in the healthcare industry, with advancements in orthodontic materials, techniques, and digital technologies further driving the market. Furthermore, the aging population in Europe, with an increasing prevalence of age-related dental issues, is creating a growing demand for orthodontic treatments, including headgear.

The Middle East and Africa (MEA) orthodontic headgear market analysis states that the region is also witnessing a notable surge. Gulf countries such as the UAE and Saudi Arabia lead due to higher disposable incomes. Moreover, technological advancements, such as CAD/CAM systems and 3D imaging, are widely adopted, ensuring precision and patient-specific treatment plans. Additionally, a growing emphasis on aesthetic dentistry and improved appearance is driving the market in the MEA region. Furthermore, the prevalence of malocclusion, or misaligned teeth, is on the rise in many parts of Africa, creating a significant need for orthodontic interventions, including headgear. However, dental education and affordability remain a challenge.

Latin America's orthodontic headgear market size is also emerging. Brazil, Mexico, and Argentina are key markets due to their large populations and improving access to orthodontic care. Moreover, dental tourism is a significant driver, particularly in Mexico and Costa Rica, offering affordable treatments to international patients. Additionally, the region places a strong emphasis on aesthetics and personal appearance, driving consumer requirements for improved smiles and contributing to the popularity of orthodontic treatments, including headgear. Improved access to healthcare services is making orthodontic treatments more readily available across the region. However, challenges such as uneven distribution of healthcare resources and economic disparities within the region hinder the market.

Top Key Players and Market Share Insights:

The Orthodontic Headgear market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D) and product innovation to hold a strong position in the global Orthodontic Headgear market. Key players in the Orthodontic Headgear industry include-

- Ortho Kinetics Corp (U.S.)

- Dentsply Sirona (U.S.)

- Treedental (China)

- Great Lakes Dental Technologies (U.S.)

- DENTAURUM (Germany)

- OrthoAmerica Holdings LLC (U.S.)

- Zhejiang Yamei Medical (China)

- Jaypee Dent. (India)

- DTC Medical Apparatus Co., Ltd. (China)

- Speed Dental Co., Ltd. (South Korea)

Orthodontic Headgear Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 2,148.42 Million |

| CAGR (2025-2032) | 6.3% |

| By Product Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Orthodontic Headgear market? +

In 2024, the Orthodontic Headgear market is USD 1,329.48 Million.

Which is the fastest-growing region in the Orthodontic Headgear market? +

Asia Pacific is the fastest-growing region in the Orthodontic Headgear market.

What specific segmentation details are covered in the Orthodontic Headgear market? +

Product Type and Application segmentation details are covered in the Orthodontic Headgear market

Who are the major players in the Orthodontic Headgear market? +

Ortho Kinetics Corp (U.S.), Dentsply Sirona (U.S.), OrthoAmerica LLC (U.S.), Zhejiang Yamei Medical Co., Ltd. (China), Jaypee Dent. (India), DTC Medical Apparatus Co., Ltd. (China), Speed Dental Co., Ltd. (South Korea), Treedental (China), Great Lakes Dental Technologies (U.S.), and DENTAURUM (Germany).