- Summary

- Table Of Content

- Methodology

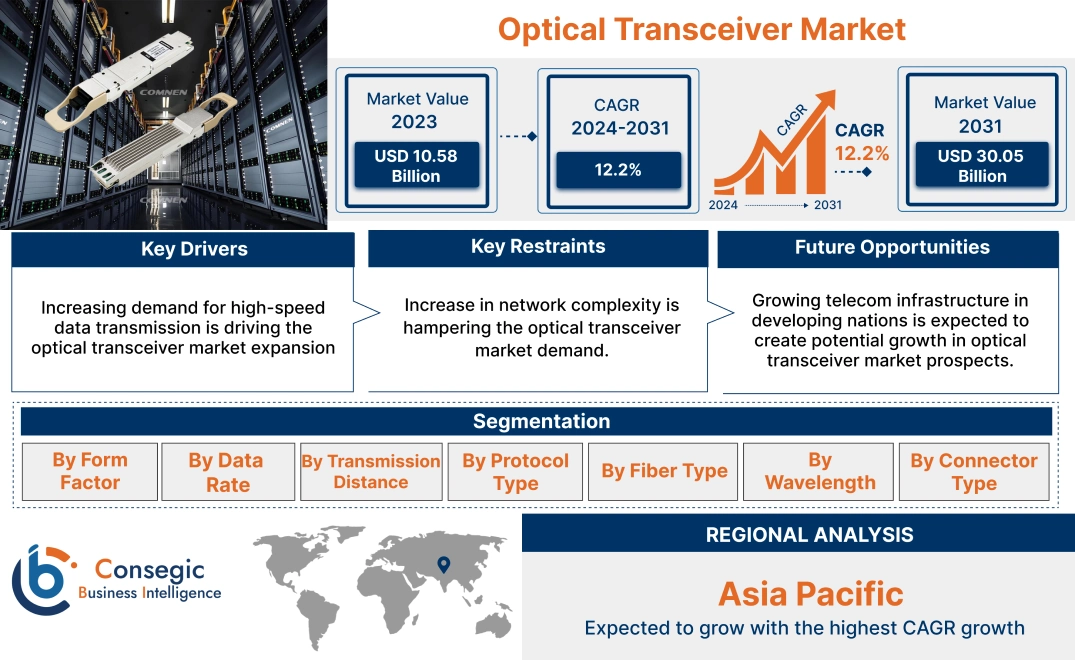

Optical Transceiver Market Size:

Optical Transceiver Market Size is estimated to reach over USD 30.05 Billion by 2032 from a value of USD 10.58 Billion in 2024 and is projected to grow by USD 11.95 Billion in 2025, growing at a CAGR of 12.2% from 2025 to 2032.

Optical Transceiver Market Scope & Overview:

Optical transceivers are crucial elements in contemporary telecommunication and data center networks. They connect electrical and optical signals, allowing swift data transmission over considerable distances using fiber optic cables. These transceivers are utilized across various industries, but their significance is particularly crucial in telecommunications due to their capability to convey substantial data volumes across a network.

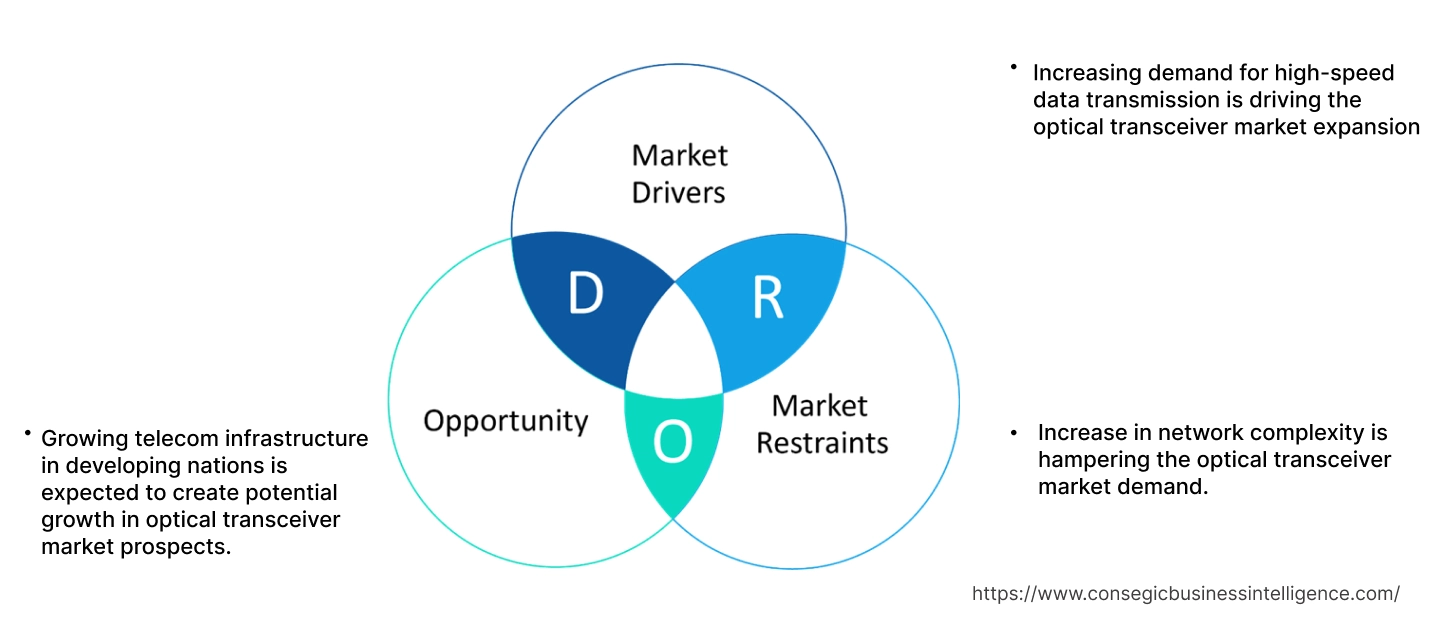

Optical Transceiver Market Dynamics - (DRO) :

Key Drivers:

Increasing demand for high-speed data transmission is driving the optical transceiver market expansion

The global optical transceiver market is witnessing considerable growth due to the rising need for high-speed data transmission. This need is mainly driven by the constantly changing digital environment where organizations and businesses continually search for quicker and more efficient ways to transfer large quantities of data. As global data production increases, traditional networks frequently struggle to manage the excess data, resulting in a bottleneck in processes. Transceivers present a practical solution as they offer enhanced transmission speeds, allowing for the rapid transfer of information across different platforms. Moreover, sectors such as telecommunications, data centers, and internet service providers are quickly growing their infrastructure to support the provision of faster internet services to users. This factor has prompted a stronger focus on upgrading current optical fiber networks and investing in cutting-edge transceiver technologies.

- For instance, in April 2024, Approved Networks, a division of Legrand, the leading supplier of optical networking technology, announced the public launch of its new OSFP 800G model of SR8 optical transceiver. This cutting-edge transceiver surpasses high-speed data transfer standards, providing an innovative solution for broadband providers and data centers to support data-intensive applications and allow real-time AI processing across networks.

Thus, according to the analysis, the increasing advancement associated with high-speed connectivity solutions is driving the optical transceiver market size.

Key Restraints:

Increase in network complexity is hampering the optical transceiver market demand.

There are several layers in data center networks, such as the core spine (distribution layer) and leaf layers (access layer). These layers contain transceivers. As these switches often become saturated with data traffic, the delivery of data packets to transceiver-receiver units can experience delays. These issues require more compact form factors to enhance compatibility and optimize network space.

Moreover, the existing network infrastructure is similarly fragmented, concentrating on domain-specific development instead of a cohesive consumer-focused strategy. Organizations need to implement a forward-thinking and network-oriented approach to simplify network complexity, which is hindering the optical transceiver market growth.

Future Opportunities :

Growing telecom infrastructure in developing nations is expected to create potential growth in optical transceiver market prospects.

The progress of telecommunications infrastructure will have a major beneficial effect on developing countries. With the rise of IoT, AI, and big data, the need for smart devices and connected applications is increasing. The introduction of optical transceiver-based fiber optical networks has facilitated high-bandwidth and low-latency communication between cities, replacing the older copper cable network. In addition to this, developing countries, such as China and South Korea, have already improved their network systems by installing advanced communication networks across their regions. Moreover, countries in the Middle East and Africa are investing in telecom infrastructures to support 5G network advancements. Some mobile networks in Japan, Qatar, China, and Kuwait now offer 5G service. The implementation of the 5G network requires the integration of high-bandwidth fiber optic cables with these transceivers for secure and dependable data transmission.

- According to the Ministry of Communications, India has a total internet subscribers of around 954.40 million as of March 2024, with 398. 35 million subscribers from rural regions. Of the country’s 6.44 lakh villages, 6.12 lakh, or 95. 15%, are facilitated with 3G/4G mobile connectivity, providing them with Internet access. Additionally, under the Digital India Initiative, the government is actively striving to expand connectivity beyond major metropolitan areas, targeting tier-2 and tier-3 cities, along with rural and remote areas.

Thus, expanding telecom infrastructure in developing nations is driving the optical transceiver market opportunities.

Optical Transceiver Market Segmental Analysis :

By Form Factor:

Based on the form factor, the market is segmented into CFP (C Form-factor Pluggable), QSFP (Quad Small Form-factor Pluggable), QSFP+, QSFP28, SFP (Small Form-factor Pluggable), SFP+ (Enhanced Small Form-factor Pluggable), XFP (10 Gigabit Small Form-factor Pluggable), and Others (QSFP-DD and QSFP112).

Trends in the Form Factor:

- With the rising need for 10 Gigabit Ethernet and 8G fiber channels, along with the growth of data centers, enterprise networks, and telecommunications centers, the form factor segment is consistently expanding and is expected to grow significantly in the near future.

- The growing demand for higher data rates and bandwidth in data centers and corporate networks is leading to the use of advanced form factors. Further, ongoing advancements in these devices, such as the creation of coherent optical transceivers and photonic integrated circuits, are influencing optical transceiver market trends and are responsible for the rapid development of the segment.

The QSFP (Quad Small Form-factor Pluggable) segment accounted for the largest revenue in the year 2024.

- The global Quad Small Form-Factor Pluggable (QSFP) module segment is leading the way in enhancing data transmission technologies, providing high-speed, high-density interconnect solutions for contemporary networking applications.

- QSFP modules are small and are commonly utilized in data centers, telecommunications networks, and high-performance computing settings to facilitate rapid and efficient data communication.

- The rapid increase in data traffic, fuelled by developments in cloud computing, big data analytics, and the Internet of Things (IoT), has led to a heightened need for high-speed data transmission solutions. QSFP modules are essential in meeting this need by offering dependable, high-bandwidth connectivity alternatives for data transmission over both short and long distances. Their compact design facilitates greater port density, allowing for more effective utilization of constrained space within networking devices and data center settings.

- Thus, based on the above analysis, the improvements in QSFP module technology including better power efficiency, enhanced signal integrity, and support for advanced modulation techniques, are fostering innovation and broadening the market opportunity.

The SFP (Small Form-factor Pluggable) segment is anticipated to register the fastest CAGR during the forecast period.

- Advancements in optical and electronic technologies have continuously enhanced the functionality of Small Form Factor Pluggable (SFP) modules, resulting in the development of modules that are more compact, capable of higher data rates, and more cost-effective.

- Moreover, WDM technology enabled by optical advancements permits multiple light wavelengths to travel through a single optical fiber. This progress has resulted in SFP modules that can accommodate multiple channels within a single unit, enhancing capacity and adaptability in network configurations.

- Furthermore, advancements have allowed SFP modules to support a broad array of communication protocols, including Ethernet, fiber channels, SONET/SDH, and others.

- For instance, in April 2021, Eurotech Technologies introduced high-performance BestNet SFP Modules. These modules offer dual data rates of 1. 25Gbps/1. 0625Gbps, accommodate a 20km transmission range with SMF and are highly economical. The assembly comprises three components: an FP laser transmitter, a PIN photodiode combined with TIA, and an MCU control unit.

- Thus, based on the analysis the advancements in optical and electronic technology are driving the optical transceiver market size and growth.

By Data Rate:

Based on the data rate, the market is segmented into Less than 10 Gbps, 10 Gbps to 40 Gbps, 100 Gbps, and Greater than 100 Gbps.

Trends in Data Rate:

- The growing dependence on cloud services and the rise of data centers require high-bandwidth infrastructure, driving the need for transceivers.

- AI and ML applications necessitate large volumes of data to be processed and transmitted, creating a demand for high-speed devices.

The 100 Gbps segment is dominating the market share and is expected to register the highest CAGR during the forecast period.

- The swift development of data centers globally significantly promotes the adoption of 100 Gbps. These facilities need high-capacity infrastructure to accommodate the rising quantity of servers and storage devices.

- In fields such as engineering simulation, financial modeling, and scientific research, HPC environments necessitate high-bandwidth connections to manage extensive parallel computing tasks, and 100G FR can fulfill this requirement.

- The delivery of cloud services relies on a vast network infrastructure capable of processing and transmitting customer data in real-time. 100Gbps networks offer the essential high-speed connectivity for these services.

- The network utilized by CDN operators to deliver content to consumers globally also necessitates 100G FR rates to enhance user experience and minimize buffering or delay problems.

- Therefore, based on the optical transceiver market analysis, the 100 Gbps data rate is projected to dominate the market demand.

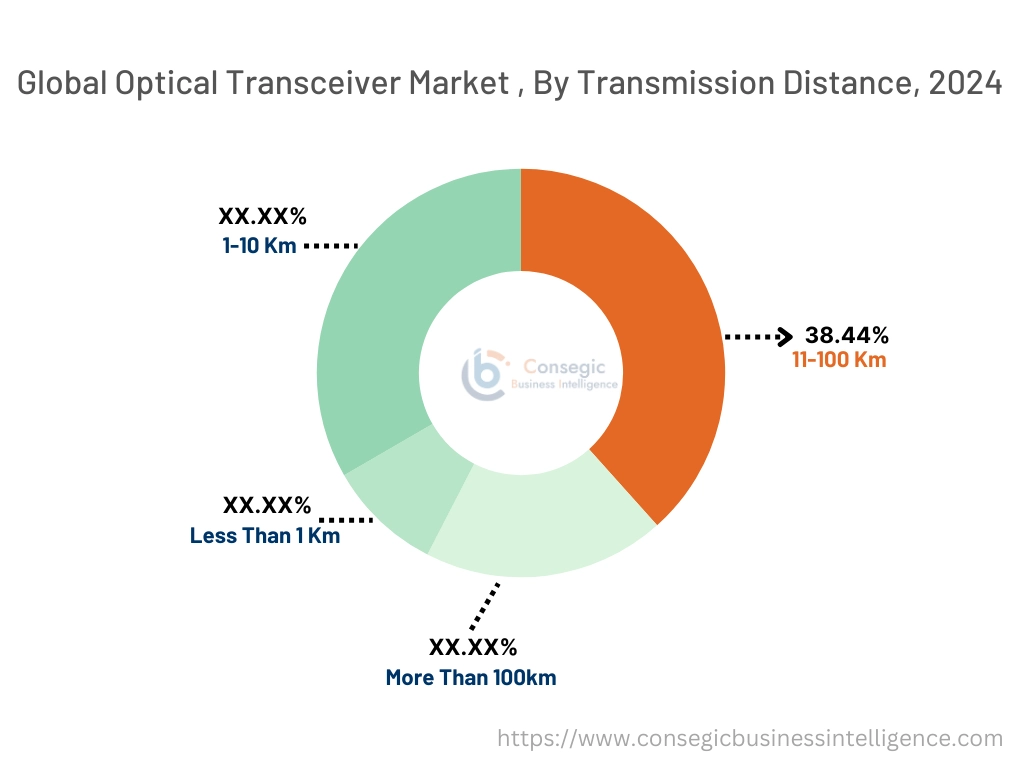

By Transmission Distance:

Based on the transmission distance, the market is segmented into less than 1 km, 1-10 km, 11-100 km, and more than 100km.

Trends in the transmission distance:

- The increasing requirement for high-bandwidth connections over extended distances is fuelling the need for long-reach for these devices. This is particularly noticeable in the development of data centers and the implementation of 5G networks.

- Coherent optics technology is gaining popularity for long-distance applications, which is influencing the optical transceiver market and is responsible for the rapid growth of the segment.

11-100 km accounted for the largest revenue share of 38.44% in the year 2024.

- The deployment of 5G networks necessitates robust backhaul and fronthaul infrastructure. These devices within the 11-100 km range are crucial for linking base stations and core network devices.

- These networks link data centers, central offices, and various network nodes within a metropolitan region.

- Moreover, the rising need for high-bandwidth services in urban areas is prompting the need for high-performance optical devices in this sector.

- Therefore, the aforementioned factors are further driving the optical transceiver market.

The more than 100 km segment is anticipated to register the fastest CAGR during the forecast period.

- The shift towards increased data rates, specifically 400 Gbps and 800 Gbps, is fuelling the need for more sophisticated coherent optical transceivers.

- PICs are being incorporated into these devices to enhance performance, decrease power consumption, and allow for greater integration levels.

- For instance, in December 2024, NEC Corporation launched the new 100G QSFP28 ZR4 BiDi, which increased transmission distance up to 80km. This new launch is an enhanced version of the two-fiber 100Gb/s optical transceiver that uses multiple fibers, facilitating bi-directional data transfer in both upstream and downstream directions via a single fiber.

- Thus, based on the analysis the advancements in transmission technology are projected to boost the optical transceiver market growth during the forecast period.

By Protocol Type:

Based on protocol type, the market is segmented into fiber channel, Ethernet, FTTx, CWDM/DWDM, and Others.

Trends in the protocol type:

- Ethernet is the most commonly utilized protocol, facilitating fast data transfer in local area networks (LANs) and wide area networks (WANs).

- Fiber to the Home (FTTH) is becoming increasingly prevalent, providing high-speed internet access to homes and businesses.

The Ethernet segment is dominating the market share and is expected to register the highest CAGR during the forecast period.

- The Ethernet segment is anticipated to retain its leadership throughout the forecast period. Ethernet-based devices are extensively utilized in multiple applications, such as data centers, enterprise networks, and telecommunications.

- With the increasing amount of data being produced and utilized, there is a need for dependable and efficient connectivity solutions, and Ethernet-based transceivers offer the required bandwidth and speed.

- The Ethernet protocol is extensively utilized in enterprise networks for local area network (LAN) connectivity, rendering Ethernet-based transceivers a favored option in this area.

- Additionally, the Ethernet segment benefits from the broad adoption of Ethernet standards and the existence of various Ethernet-based transceiver form factors, including SFP, QSFP, and CFP, which meet diverse network needs.

- These factors would further supplement the optical transceiver market during the forecast period.

By Fiber Type:

Based on fiber type, the market is segmented into single-mode fiber and multimode fiber.

Trends in the fiber type:

- The movement towards increased data rates, like 400 Gbps and 800 Gbps, is pushing the need for both SMF and MMF transceivers with enhanced performance.

- Smaller form factors like QSFP28 and OSFP are gaining popularity to support greater density in data centers and various applications.

Single-mode fiber accounted for the largest revenue share in the year 2024.

- Single-mode fiber typically leads the overall market because of the rising need for high-speed, long-range communication in data centers, telecom networks, and enterprises.

- The increasing need for high bandwidth to accommodate new technologies, such as 5G, IoT, and cloud computing, corresponds with the strengths of single-mode fiber and transceivers.

- Moreover, the escalating requirement for reliable technology for high-speed data transmission over long distances, wide-area networks (WANs), and the continuously growing telecom sector has resulted in a significant enhancement in the optical transceiver market share, which is expected to expand further in the coming years.

The multi-mode fiber segment is anticipated to register the fastest CAGR during the forecast period.

- One of the main growth drivers for the multimode fiber market is the increasing need for high-bandwidth connectivity.

- As businesses and consumers keep producing and using data at unmatched speeds, the need for effective and dependable data transmission solutions has increased significantly. Multimode fibers, known for their capacity to handle high data rates over short distances, have become a favored option for businesses, particularly in data centers and telecommunications networks.

- Another important factor for the market is the ongoing progress in fiber optic technology. Innovations such as the creation of OM5 multimode fiber have greatly enhanced the performance and efficiency of fiber optic networks. OM5 fibers, intended to handle higher data rates over greater distances, are being more frequently used in advanced network infrastructures.

- Furthermore, the continuous research and development efforts focused on improving multimode fibers are expected to generate new prospects for market development.

- For instance, OFS Fitel, LLC is a prominent supplier of fiber optic solutions and provides an extensive array of multimode fiber products for different uses. The company’s multimode fiber products feature high-performance fibers tailored to accommodate high data rates and extended transmission distances.

- Thus, based on the analysis, the advancements in fiber optic technology are driving the market during the forecast period.

By Wavelength:

Based on wavelength, the market is segmented into 850 nm, 1310 nm, 1550 nm, and Others.

Trends in the wavelength:

- The need for increased bandwidth and improved system flexibility has resulted in the creation of multi-wavelength and multi-mode optical transceivers. These transceivers can send multiple optical signals at the same time, allowing for higher data transfer speeds and meeting various application needs.

- Current research concentrates on creating advanced modulation methods, signal processing strategies, and wavelength-division multiplexing technologies to address existing challenges and fully leverage the advantages of multi-wavelength and multi-mode optical transceivers.

The 1310 nm segment is dominating the market share and is expected to register the highest CAGR during the forecast period.

- The 1310nm band wavelength transceivers are mainly utilized in 5G infrastructure for high-speed backhaul connections. These backhaul connections connect the main network with the cell site, which is vital for transferring and transmitting large volumes of data.

- The 1310nm band is advantageous as it has low attenuation and can carry the signal over long distances without considerable loss of signal strength.

- Furthermore, 1310nm transceivers are reasonably priced and readily accessible, making them an appealing option for network infrastructure developers.

- Thus, the above factors and benefits are fuelling the optical transceiver market share.

By Connector Type:

Based on connector type, the market is segmented into lucent connectors (LC), standard connectors (SC), ST connectors, ferrule connectors (FC), multi-position optical (MPO) connectors, and others.

Trends in the connector type:

- Continuous improvements in connector technology are resulting in enhanced reliability, decreased insertion loss, and superior performance.

- Fabricators manufacture fiber optic connectors in large quantities for long-range cabling applications. These connectors are crafted from ultra-pure quartz. The strong opportunity from sensing applications and the communication sector for various uses provides dynamic progress for industry advancement. These factors would further drive the optical transceiver market demand during the forecast period.

Lucent Connectors (LC) accounted for the largest revenue share in the year 2024.

- A lucent connector (LC), classified as an SFF (small form factor) connector, features a 1.25 mm ferrule. Its compact design contributes to the widespread use of these fiber optic connectors in datacoms and makes them suitable for high-density applications.

- Many operators are shifting toward high-efficiency cabling with LC fiber connectors today. The LC fiber optic connector is regarded as the most frequently utilized connector currently.

- Telecom providers are greatly investing in enhancing their current network capacities, which in turn boosting the fiber optic connectors.

- Additionally, the introduction of 5G contributes positively to the lucent connectors market throughout the projected period. Currently, the need for fiber optic cables is advancing the telecommunications sector for the transmission of telephone signals, cable television signals, and internet communications.

The standard connectors (SC) segment is anticipated to register the fastest CAGR during the forecast period.

- SC fiber optic connector is preferably suited for datacom, and telecom uses, which includes passive optical networking. Due to its enhanced performance, these types of connectors are still most widely used connectors for polarization maintaining applications.

- In May 2021, Optical Cable Corporation, a manufacturer of fiber optic cables, announced the collaboration with CommScope, a supplier of network infrastructure solutions. This agreement includes a cross-licensing arrangement that allows both organizations to utilize and use specific sections of each other's patent portfolios. This partnership allows them to capitalize on the licensed patents and technologies from the other company, promoting innovation and aiding the creation of advanced solutions in network infrastructure.

- Thus, based on the above factors, these advancements and strategic partnership in fiber optic connector technology is driving the market during the forecast period.

By Application:

Based on application, the market is segmented into 5G networks, cloud computing, content delivery networks, internet service providers, medical facilities, telecommunications, television networks, and others.

Trends in the application:

- In the industrial sector, these devices are utilized in multiple applications, such as industrial automation, process control, and machine-to-machine (M2M) communication. The rising implementation of Industry 4.0 and smart manufacturing technologies has resulted in a heightened need for fast and dependable communication solutions in industrial settings.

- The growing use of telemedicine and remote patient monitoring solutions necessitates fast, dependable connectivity for sending patient data, including vital signs, medical images, and video consultations.

Telecommunications accounted for the largest revenue share in the year 2024.

- The expanding reach of telecommunication infrastructure in developing countries, like China and India, is attributed to the substantial advancement of technology in these areas.

- Data transmission and communication services represent the largest portions of the telecommunication application sector. Furthermore, the rising quantity of cloud-based applications, audio-video services, and video-on-demand (VoD) services is expected to increase installations.

- The requirement for fast, long-range connections for uses like international data transfers and video streaming persists in fuelling the need for advanced devices, which is further driving the market.

The 5G networks segment is anticipated to register the fastest CAGR during the forecast period.

- In 5G communication, fiber optics carry 5G signals to and from the carrier's extensive area networks. According to a study released by the IEEE Communications Society, they are critical elements of 5G fronthaul, midhaul, and backhaul, and their expenses represent approximately 50% to 70% of the overall 5G network costs.

- With the ongoing deployment of 5G, consumer needs are evolving towards higher data rates. Telecom vendors and 5G service providers are increasingly moving towards the 800 Gbps optical ecosystem to meet the significant increase in data needs and changing consumer preferences.

- For instance, in October 2022, SoftBank Corp, a telecommunications service provider in Japan, declared its plan to implement Cisco ZR4 model of optical transceivers to enhance its 4G/5G, broadband, and company offerings. By utilizing these transceivers, the company intends to decrease power usage and carbon emissions, resulting in quicker connectivity. The capacity of 5G optical transceivers to deliver improved network efficiency, high reliability, reduced rack space, and lower power consumption is promoting operational effectiveness and sustainability, thereby propelling the market.

- Thus, considering the advantages offered by 5G networks, there is notable investment in the technology, which will promote the innovation and implementation of 5G optical transceivers, in turn driving the market.

By End User:

Based on end user, the market is segmented into data centers, automotive, healthcare, IT & telecom, manufacturing, aerospace & defense, healthcare, consumer electronics, and others.

Trends in the end user:

- The progress of data centers, which act as the foundation for contemporary digital services, necessitates effective and dependable connectivity options.

- Modern aircraft and military equipment increasingly depend on effective networks for avionics, radar, and communications, rendering fiber optics vital. Market initiatives concentrate on producing smaller, more robust fiber optics that can endure challenging conditions.

IT & telecom accounted for the largest revenue share in the year 2024.

- In the IT & telecom sector, transceiver is an essential component utilized to send significant volumes of data over fiber optic cables, functioning as a converter between electrical signals in a network device and light signals moving through the fiber.

- The use of transceiver facilitates rapid data transmission over extensive distances, especially in data centers and telecommunications networks.

- As cloud services depend on fast data transfer, optical transceivers with high data rates (such as 100G, 400G, and higher) are crucial for managing the intense traffic. The above factors are further driving the market.

The data center segment is anticipated to register the fastest CAGR during the forecast period.

- Data centers are fuelling the market, as the increasing number of businesses transition their data and applications to the cloud.

- Companies are adopting optical modules to manage the surge in data traffic resulting from cloud applications. Optical modules are becoming essential in data centers since they link servers, storage, and networking devices.

- They offer a high-speed, low-latency, and low-power option compared to traditional copper-based networks, enabling data centers to address the rising volume of data traffic generated by data-heavy applications.

- In September 2024, NewPhotonics launched its NPG102 model of PIC transmitter on chip (TOC). The solution provides low latency data communications with low power usage and minimized channel loss, which is fundamental to the NPG102 chip technology tailored to address the growing AI-cluster processing requirements in data center infrastructure.

- These characteristics are pushing data centers to use optical modules, which is driving the optical transceiver market.

Regional Analysis:

The global market has been classified by region into North America, Europe, Asia-Pacific, MEA, and Latin America.

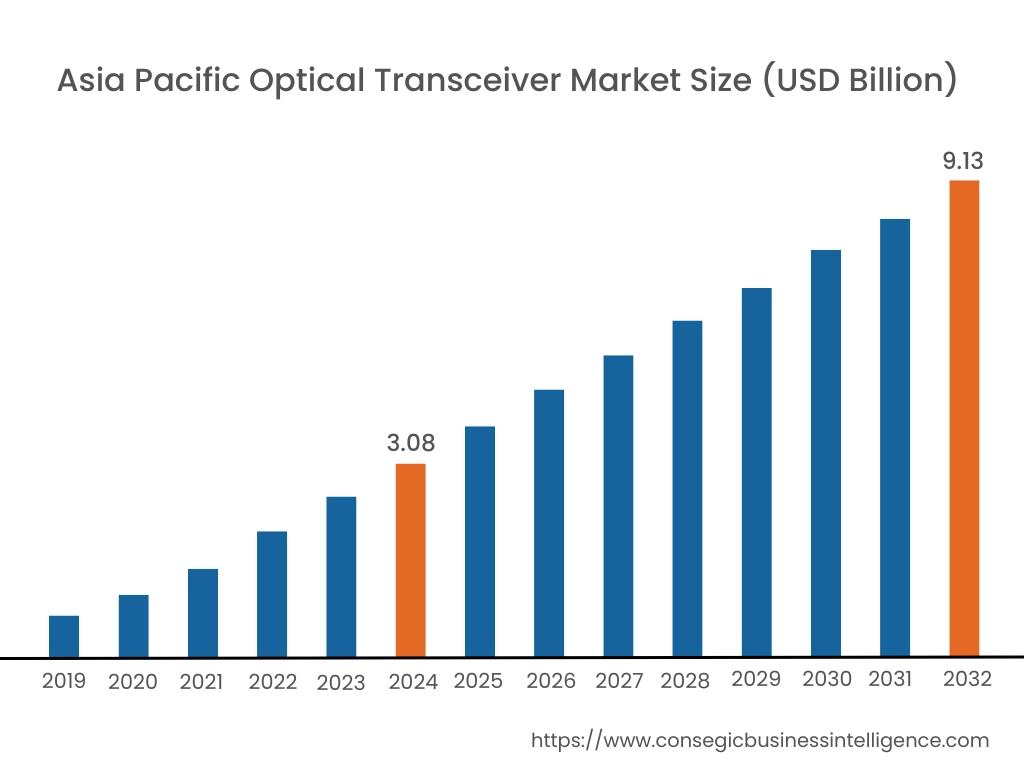

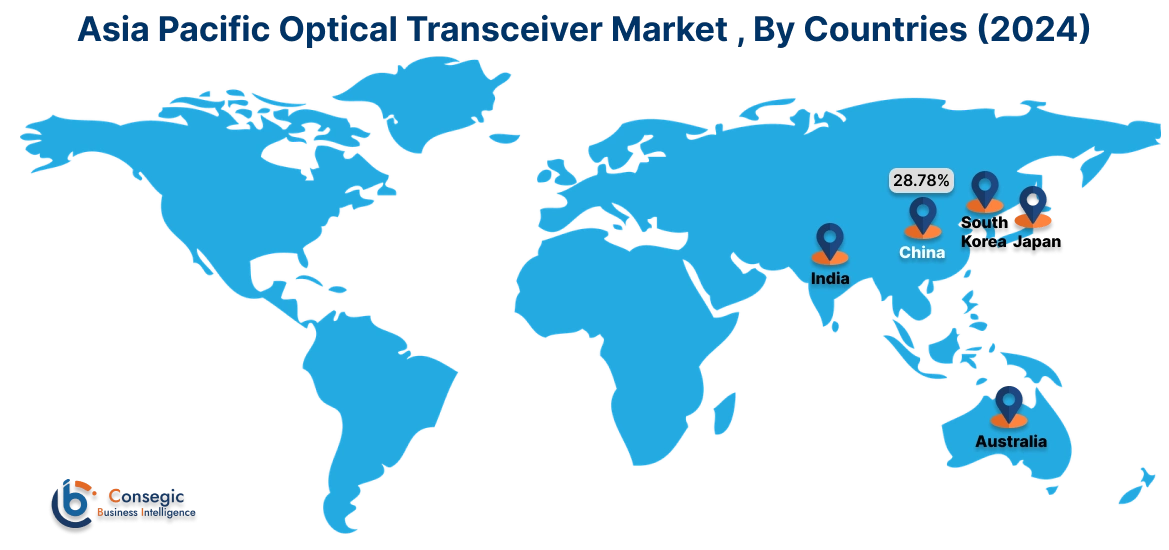

Asia Pacific optical transceiver market expansion is estimated to reach over USD 9.13 Billion by 2032 from a value of USD 3.08 Billion in 2024 and is projected to grow by USD 3.49 Billion in 2025. Out of this, China accounted for the maximum revenue share of 28.78%. The region has a sizable population and a quickly growing middle class, increasing the need for high-speed internet access and data services. This has resulted in significant investments in telecommunications infrastructure, including the installation of fiber optic networks, which has also boosted the need for optical devices. Countries such as China and South Korea serve as key manufacturing centers for market, with prominent manufacturers established in the region. This has led to a rich assortment of product portfolio at competitive prices, further propelling market during the forecast period.

- For instance, Fujikura Ltd. is a Japan-based electrical manufacturing company, recognized for its premium fiber optic products and significant business expertise. The company’s multimode fiber range consists of an array of fibers tailored for diverse applications, such as data centers, telecommunication networks, and industrial uses. Fujikura’s strong emphasis on innovation and customer support has enabled it to sustain a competitive advantage in the market and enhance its global market presence.

North America optical transceiver industry is estimated to reach over USD 9.18 Billion by 2032 from a value of USD 3.18 Billion in 2024 and is projected to grow by USD 3.59 Billion in 2025. North America possesses a considerable share of the optical transceiver market, propelled by the presence of prominent technology firms and significant investments in modern communication infrastructure. The region's strong data center sector and the rising installation of fiber optic networks are key elements propelling the regional market. The United States, specifically, serves as a major market for multimode fibers, with considerable requirement stemming from data centers, telecommunication networks, and enterprise networks. Therefore, based on the optical transceiver market analysis, the North American market will keep on dominating the regional market during the forecast period.

- For instance, in January 2024, Zayo successfully conducted two live field trials of sixth-generation of Photonic Service Engine super-coherent optics from Nokia. The trials exhibited transmission record of 800 Gb per second on a single wavelength over a 1,866 km link from LA to El Paso, and 1Tb per second transmission over 1,000 km route from LA to Phoenix.

As per the analysis, Europe possesses a significant portion of the market, concentrating on improving telecommunication networks and boosting data center functions. The area's focus on digital transformation and the incorporation of advanced technologies, including IoT and AI, fuels the need for high-performance devices. Major nations like Germany, the UK, and France lead in technological progress, aiding the region's market development. Additionally, the growing need for data storage and processing is prompting the development of new data centers throughout Latin America. Furthermore, in MEA region majority of components are imported due to limited local manufacturers, its limited manufacturing ecosystem encourages reliance on global supply chains and large shipments of finished products.

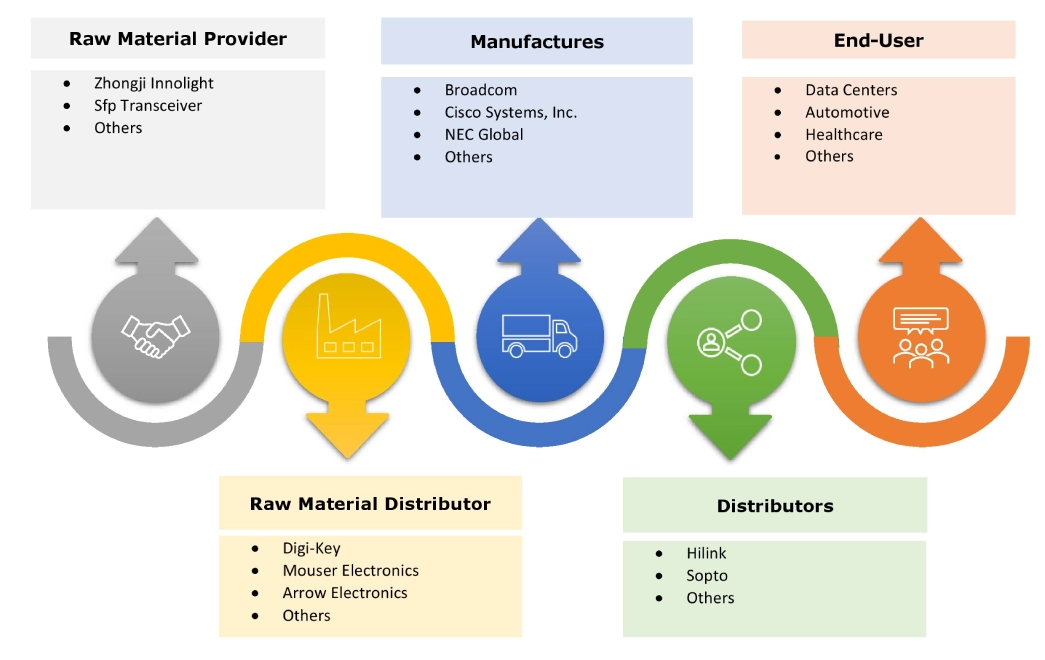

Top Key Players and Market Share Insights:

The optical transceiver market is highly competitive with major players providing casino management solutions to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the market. Key players in the optical transceiver industry includes-

- Broadcom (U.S.)

- Coherent Corp (U.S.)

- Sumitomo Electric Industries, Ltd. (Japan)

- Hisense broadband (U.S.)

- NEC Global (Japan)

- STORDIS GmBH (Germany)

- Microsoft (U.S.)

- InnoLight Technology (Singapore)

- HiSilicon Optoelectronics Co., Ltd. (China)

- Cisco Systems, Inc. (U.S.)

- Molex, LLC. (U.S.)

- Smartoptics (Norway)

- Accelink Technology Co. Ltd (China)

- Jabil Inc. (U.S.)

Recent Industry Developments:

Expansion:

- In April 2024, Microsoft invested USD 2. 9 billion in the upcoming two years to improve its hyperscale cloud computing and AI capabilities in Japan. The company also plans to expand its digital skilling initiatives, targeting to educate more than 3 million individuals in AI over the next three years. Furthermore, Microsoft will set up its inaugural Microsoft Research Asia lab in Japan and reinforce its cybersecurity collaboration with the Government of Japan.

Merger & Acquisition:

- In October 2023, Jabil Inc. acquired the silicon photonics optical modules division from Intel Corporation's. Through this acquisition, Jabil will assume responsibility for the production and distribution of Intel’s silicon photonics transceivers, while also concentrating on the advancement of upcoming versions of these transceivers.

Partnerships:

- In October 2024, Smartoptics announced the partnership with WIN Technology, to modernize and enhance the company’s network, benefiting organizations in Minnesota, Wisconsin, Iowa, Illinois, and Michigan. With this partnership, Smartoptics would further strengthen its recent product launches in its product portfolio and target markets towards large- and mid-size operators across the region.

Optical Transceiver Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 30.05 Billion |

| CAGR (2025-2032) | 12.2% |

| By Form Factor |

|

| By Data Rate |

|

| By Transmission Distance |

|

| By Protocol Type |

|

| By Fiber Type |

|

| By Wavelength |

|

| By Connector Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Optical Transceiver market? +

Optical Transceiver Market Size is estimated to reach over USD 30.05 Billion by 2032 from a value of USD 10.58 Billion in 2024 and is projected to grow by USD 11.95 Billion in 2025, growing at a CAGR of 12.2% from 2025 to 2032.

Which is the fastest-growing region in the Optical Transceiver market? +

Asia-Pacific is the region experiencing the most rapid growth in the market.

What specific segmentation details are covered in the Optical Transceiver report? +

The optical transceiver report includes specific segmentation details for the form factor, data rate, transmission distance, protocol type, fiber type, wavelength, connector type, application, end-user, and region.

Who are the major players in the Optical Transceiver market? +

The key participants in the market are Broadcom (U.S.), Coherent Corp (U.S.), InnoLight Technology (Singapore), HiSilicon Optoelectronics Co., Ltd. (China), Cisco Systems, Inc. (U.S.), Molex, LLC. (U.S.), Smartoptics (Norway), Accelink Technology Co. Ltd (China), Sumitomo Electric Industries, Ltd. (Japan), Hisense broadband (U.S.), NEC Global (Japan), STORDIS GmBH (Germany), Microsoft (U.S.), Jabil Inc. (U.S.), and others.