- Summary

- Table Of Content

- Methodology

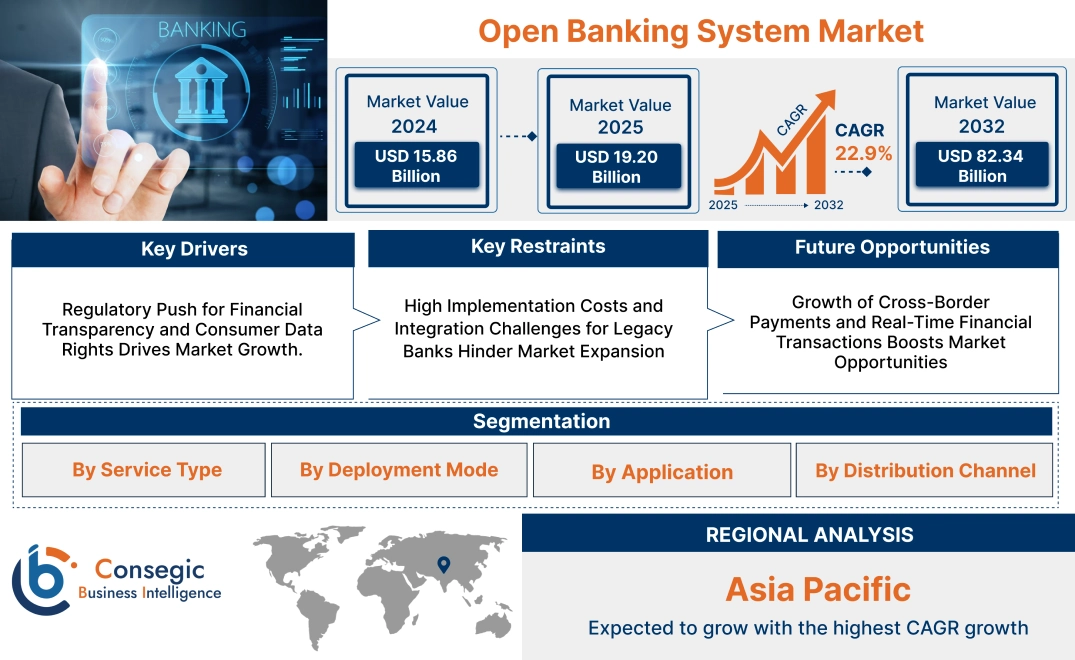

Open Banking System Market Size:

Open banking system market size is estimated to reach over USD 82.34 Billion by 2032 from a value of USD 15.86 Billion in 2024 and is projected to grow by USD 19.20 Billion in 2025, growing at a CAGR of 22.9% from 2025 to 2032.

Open Banking System Market Scope & Overview:

Open banking system enables secure data sharing between banks and third-party financial service providers through application programming interfaces (APIs). This framework enhances transparency, improves financial services, and facilitates personalized banking solutions by integrating multiple platforms within a unified ecosystem. It allows customers to access a wide range of financial products, manage accounts efficiently, and make informed decisions.

Key features include seamless payment integration, real-time financial data access, enhanced security protocols, and personalized financial insights. These capabilities improve transaction efficiency, streamline account aggregation, and enable better financial planning. The adoption of regulatory compliance measures ensures data protection while fostering innovation in digital banking services.

Banks, fintech firms, and financial service providers leverage this system to enhance customer experience, optimize service offerings, and develop innovative financial products. The continuous advancement of digital banking infrastructure is refining its capabilities, driving enhanced financial accessibility and operational efficiency across the industry.

Open Banking System Market Dynamics - (DRO):

Key Drivers:

Regulatory Push for Financial Transparency and Consumer Data Rights Drives Market Growth.

Regulations such as PSD2 in Europe, the Open Banking Initiative in the UK, and the Consumer Data Right (CDR) in Australia mandate that banks provide secure API access to customer financial data, allowing third-party financial service providers to offer personalized banking solutions, improved lending options, and real-time payment services. These regulatory initiatives aim to increase financial inclusivity, reduce banking monopolies, and enhance consumer control over financial data. The demand for secure, API-driven banking solutions is rising as customers seek greater flexibility in managing accounts, making payments, and accessing financial insights across multiple platforms.

- For instance, in October 2024, Tink launched ‘Merchant Information’ to provide consumers with a more detailed overview of their transactions. This product, provided within Tink’s Consumer Engagement, propels banking app transactions to be shown with a clear brand name, logo, location, and merchant contact details – reducing the need for consumers to contact their bank to enquire about transactions they don't recognize.

By fostering innovation in digital banking, AI-driven financial planning, and embedded finance, these regulations are accelerating the shift toward more competitive and efficient financial ecosystems, driving open banking system market expansion globally.

Key Restraints:

High Implementation Costs and Integration Challenges for Legacy Banks Hinder Market Expansion

Traditional banks operate on legacy core banking systems that require extensive upgrades to support API-driven architectures, real-time data sharing, and third-party integrations. This process involves substantial financial investment in infrastructure modernization, cybersecurity enhancements, and compliance with regulatory frameworks, increasing operational complexity. Many banks struggle with data standardization, security protocols, and seamless API connectivity, delaying the adoption of innovative financial services. Additionally, integrating AI-driven analytics, digital payment ecosystems, and third-party fintech solutions into existing frameworks requires specialized IT expertise, further driving up costs. The demand for digital financial services continues to grow, but financial institutions with outdated systems face difficulties in meeting evolving customer expectations. Addressing these challenges through scalable, cloud-based solutions and standardized API frameworks is essential for ensuring open banking system market growth and widespread adoption.

Future Opportunities:

Growth of Cross-Border Payments and Real-Time Financial Transactions Boosts Market Opportunities

Traditional cross-border transactions involve multiple intermediaries, high processing fees, and extended settlement times, creating inefficiencies for businesses and individuals. The demand for instant and low-cost international payments is driving the adoption of API-driven financial services, blockchain-based settlements, and real-time payment networks. Open banking frameworks facilitate direct integration between banks, fintech firms, and payment service providers, reducing dependency on traditional banking infrastructure. Businesses benefit from enhanced transparency, currency exchange optimization, and automated reconciliation processes, improving financial workflows. Additionally, the rise of digital wallets, decentralized finance (DeFi), and embedded financial services is further accelerating adoption.

- For instance, in July 2024, HSBC partnered with Visa and Tink to develop Zing, an international money app. The newly launched app will enable users to hold funds in more than 20 different currencies, send over 30 currencies, and transact in over 200 countries and territories worldwide, all through a single app and smart multi-currency card.

As real-time payments become the industry standard, these advancements will fuel open banking system market opportunities, ensuring broader adoption and financial inclusivity across global economies.

Open Banking System Market Segmental Analysis :

By Service Type:

By service type, the market is segmented into banking & capital markets, payments, digital lending, insurance, and wealth management.

The payments segment held the largest revenue share in 2024.

- The increasing need for secure, seamless digital transactions is driving rapid adoption of open banking payment solutions.

- Real-time payment processing, API-driven transactions, and digital wallets are reshaping financial transactions across retail and business sectors.

- Open banking system market analysis indicates that regulatory support for open payment frameworks is accelerating global adoption.

- Segmental trends suggest that API-based payment solutions will continue to gain traction, particularly in e-commerce and digital finance.

The digital lending segment is expected to register the fastest CAGR during the forecast period.

- The need for AI-driven credit scoring, instant loan approvals, and alternative lending models is fueling digital lending growth.

- Fintech firms are leveraging open banking APIs to streamline loan origination, credit assessment, and risk profiling.

- Segmental trends show that banks and lenders are increasingly adopting digital lending platforms to enhance user experience.

- Open banking system market expansion is expected to accelerate, particularly as financial institutions integrate open APIs for risk management and personalized lending services.

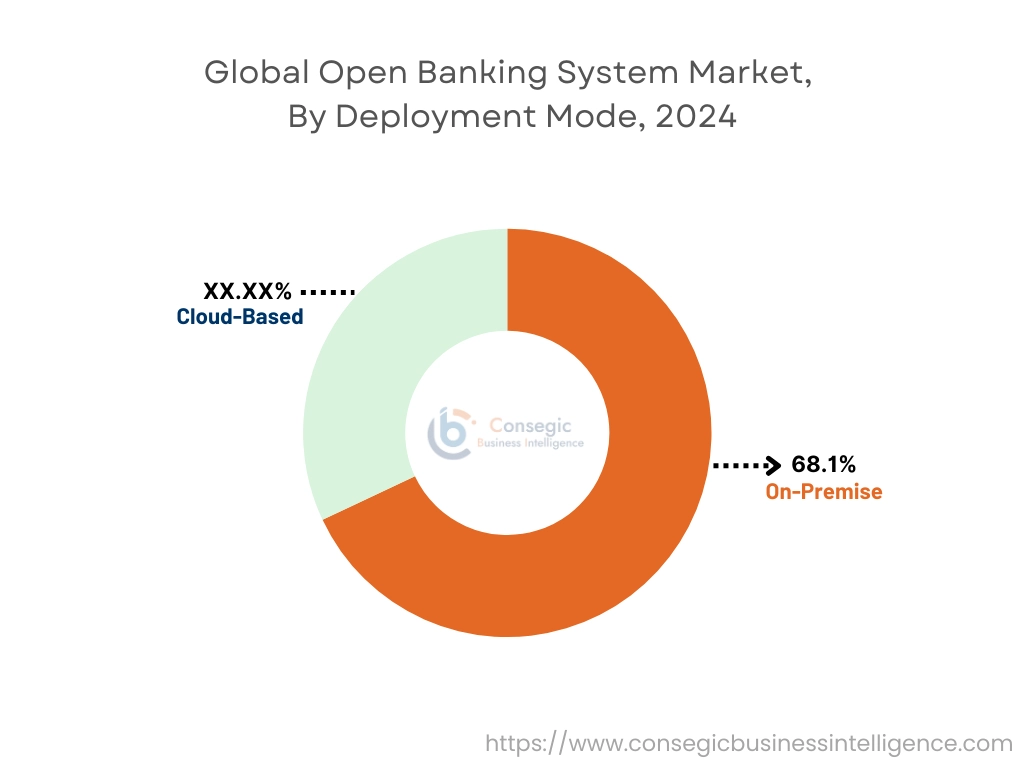

By Deployment Mode:

Based on deployment mode, the market is divided into on-premise and cloud-based.

The on-premise segment held the largest open banking system market share of 68.1% in 2024.

- Traditional banks and financial institutions prioritize on-premise deployment for enhanced data security, compliance, and control over banking operations.

- The need for customizable, in-house open banking solutions remains strong among large-scale banks with established IT infrastructure.

- Open banking system market analysis highlights that hybrid deployment models are emerging, combining on-premise security with cloud-based flexibility.

- Trends indicate that financial institutions will continue leveraging on-premise solutions, especially for high-value transactions and critical financial services.

The cloud-based segment is expected to have the fastest CAGR during the forecast period.

- Cloud-based open banking platforms are gaining popularity due to their scalability, cost-effectiveness, and real-time data access.

- The demand for API-driven cloud banking solutions is increasing, enabling seamless integration of third-party financial services.

- Segmental trends suggest that financial institutions prioritize cloud-based models to enhance digital banking capabilities.

- Market growth is being fueled by innovations in cloud-native fintech applications, driving efficiency and innovation across the banking sector.

By Application:

By application, the open banking system market is segmented into payment, banking, wealth management, and digital lending.

The payment segment held the largest revenue share in 2024.

- Contactless payments, digital wallets, and API-driven transactions are driving the need for open banking payment infrastructure.

- The expansion of real-time payment networks and cross-border digital transactions is enhancing consumer adoption.

- Segmental analysis highlights the growing influence of embedded finance, where non-banking platforms offer seamless payment experiences.

- Trends indicate that businesses are leveraging API-based payment solutions to provide frictionless checkout experiences and enhanced financial security.

The wealth management segment is anticipated to experience the fastest CAGR during the forecast period.

- AI-driven financial advisory tools, robo-advisors, and automated investment platforms are revolutionizing wealth management.

- The demand for open banking-driven financial planning solutions is growing, enabling consumers to access holistic financial insights and asset tracking.

- Open banking system market trends show an increasing shift toward digital wealth management, particularly for millennial and Gen Z investors.

- As financial institutions integrate AI and predictive analytics, the wealth management sector is expected to drive market expansion.

By Distribution Channel:

Based on distribution channel, the market is categorized into bank channel, app market, distributors, and aggregators.

The bank channel segment held the largest open banking system market share in 2024.

- Traditional banking institutions continue to dominate open banking distribution, providing secure and regulated financial services.

- The need for direct API integrations between banks and third-party fintech providers is driving innovation in banking platforms.

- Open banking system market trends suggests that financial institutions are enhancing digital banking capabilities, improving customer experience.

- Analysis suggests that banks are increasingly offering API-driven financial services, streamlining operations and expanding open banking adoption.

The app market segment is anticipated to have the fastest CAGR during the forecast period.

- The demand for mobile-based financial applications is surging, with consumers adopting fintech apps for payments, lending, and wealth management.

- Fintech startups and digital-only banks are leveraging app-based platforms to provide seamless, user-friendly open banking experiences.

- Segmental market trends highlight that mobile banking apps are reshaping customer engagement, offering instant financial services.

- With the rise of neobanks and digital wallets, the app market is driving significant open banking system market growth.

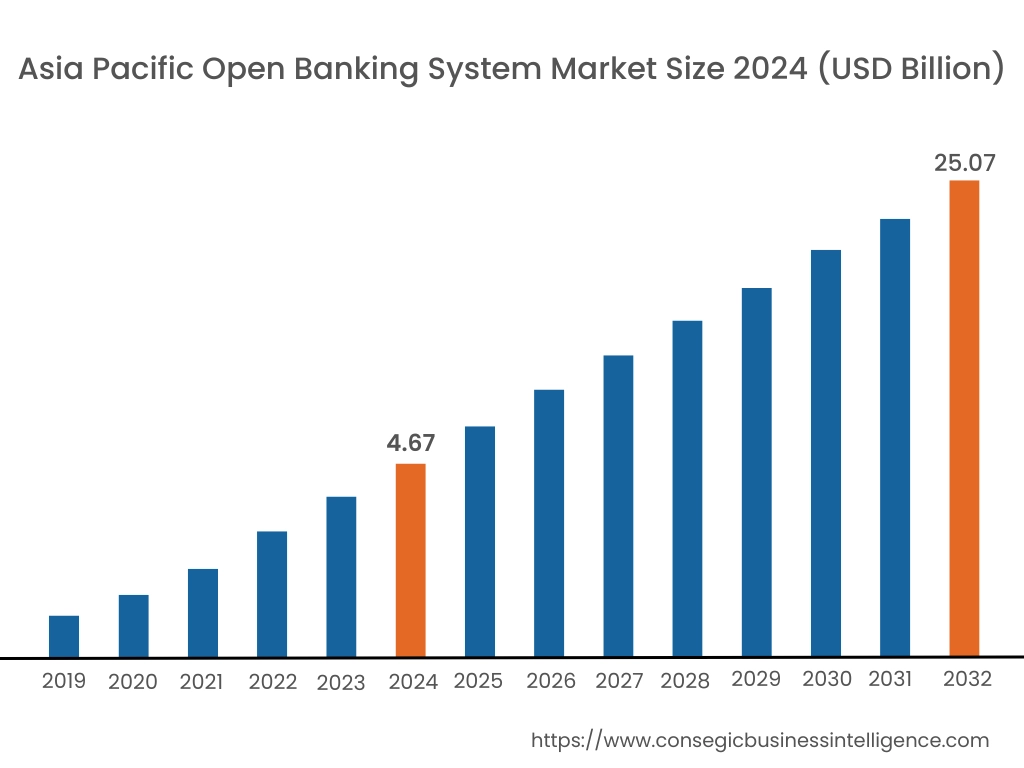

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

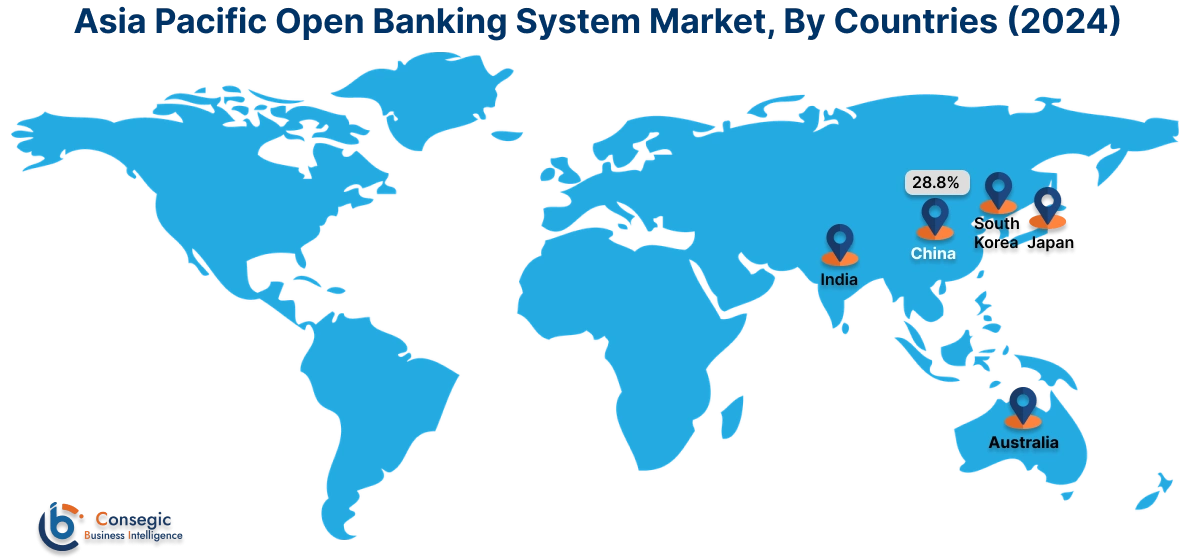

Asia Pacific is estimated to reach over USD 25.07 Billion by 2032 from a value of USD 4.67 Billion in 2024 and is projected to grow by USD 5.67 Billion in 2025. Out of this, China accounted for the maximum revenue share of 28.8%. The Asia Pacific region is experiencing rapid growth in the open banking system market, driven by increasing digitalization, government initiatives, and a burgeoning fintech ecosystem. Countries like Australia have implemented the Consumer Data Right (CDR), empowering consumers to control their financial data and share it securely with accredited third parties. This framework has spurred innovation, leading to the development of personalized financial products and services. Similarly, Japan's revised Banking Act encourages banks to adopt open APIs, fostering collaboration between traditional financial institutions and fintech startups. These regulatory landscapes have created a conducive environment for the proliferation of open banking services, meeting the rising open banking system market demand in the region.

North America region was valued at USD 5.26 Billion in 2024. Moreover, it is projected to grow by USD 6.36 Billion in 2025 and reach over USD 26.69 Billion by 2032. North America stands as a pivotal player in the open banking system market, propelled by consumer need for seamless digital experiences and regulatory initiatives aimed at fostering competition. In the United States, the Consumer Financial Protection Bureau (CFPB) has finalized rules facilitating the transfer of consumer bank data between financial entities, aiming to enhance competition and provide consumers with greater control over their financial information and ultimately driving market growth. However, challenges persist, as major banks have expressed concerns over data security and potential fraud risks associated with data sharing. Despite these hurdles, the North American market presents substantial opportunities for fintech firms and third-party service providers to collaborate with traditional banks, offering innovative financial products and services that cater to evolving consumer preferences.

Europe has an established the open banking system industry, largely due to regulatory mandates such as the Second Payment Services Directive (PSD2), which requires banks to open their payment services and customer data to third-party providers with customer consent. This regulatory environment has cultivated a competitive landscape, encouraging innovation and the development of customer-centric financial services. The United Kingdom, in particular, has witnessed a surge in fintech activities, with companies like Monzo achieving profitability and expanding their customer base. Despite the progress, there is an ongoing discourse about reducing reliance on non-European payment systems to enhance financial sovereignty and resilience. This scenario presents a significant market opportunity for regional players to develop indigenous solutions that align with European regulatory standards and consumer expectations.

Latin America is gradually embracing open banking, with countries like Brazil leading the charge through comprehensive regulatory frameworks that promote data sharing and financial inclusion. Brazil's open finance initiatives aim to enhance competition and transparency in the financial sector, providing consumers with more choices and better services. Other nations, such as Chile and Colombia, are also making strides by implementing laws that facilitate the secure exchange of financial data between institutions. These developments are expected to drive the open banking system market demand in the region, offering opportunities for fintech companies to introduce innovative solutions tailored to the unique needs of Latin American consumers.

The Middle East and Africa are emerging markets for open banking systems, with several countries initiating regulatory reforms to modernize their financial sectors. For instance, Saudi Arabia has introduced an Open Banking Framework, setting the stage for increased collaboration between banks and fintech firms. These initiatives aim to diversify financial services, improve customer experiences, and foster economic growth. While the adoption rate varies across the region, the overarching trend indicates a growing recognition of the benefits associated with open banking, such as enhanced financial inclusion and innovation. As regulatory environments continue to evolve, the open banking system market opportunity in the Middle East and Africa is poised to expand, attracting investments and encouraging the development of tailored financial solutions.

Top Key Players & Market Share Insights:

The open banking system market is highly competitive with major players providing products and services to the national and international markets. key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global open banking system market. key players in the open banking system industry include -

- Plaid (USA)

- Tink (Sweden)

- Basiq (Australia)

- Finicity (USA)

- Bunq (Netherlands)

- TrueLayer (UK)

- io (UK)

- Bud Financial (UK)

- Salt Edge (Canada)

- Yapily (UK)

Recent Industry Developments :

Partnerships:

- In November 2024, Konsentus announced partnership with the Bank of Namibia to deliver open banking standards. This initiative is undertaken as part of the National Payment System Vision 2021-2025 which will enable consumer-focused, innovative payment solutions in the country.

- In October 2024, io partnered with Santander to steer future of open banking payments. This collaboration aims to utilize Token.io’s industry-leading open banking connectivity and infrastructure to elevate Santander’s customer experiences and develop cutting-edge, real-time payment propositions.

Open Banking System Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 82.34 Billion |

| CAGR (2025-2032) | 22.9% |

| By Service Type |

|

| By Deployment Mode |

|

| By Application |

|

| By Distribution Channel |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Open Banking System Market? +

Open banking system market size is estimated to reach over USD 82.34 Billion by 2032 from a value of USD 15.86 Billion in 2024 and is projected to grow by USD 19.20 Billion in 2025, growing at a CAGR of 22.9% from 2025 to 2032.

What specific segmentation details are covered in the Open Banking System Market report? +

The Open Banking System market report includes specific segmentation details for the service type, deployment mode, distribution channel and application.

Which is the fastest-growing region in the Open Banking System Market? +

Asia Pacific is the fastest-growing region in the Open Banking System market. These trends are encouraged by increasing digitalization, government initiatives, and a burgeoning fintech ecosystem.

Who are the major players in the Open Banking System Market? +

The key participants in the Open Banking System market are Plaid (USA), Tink (Sweden), TrueLayer (UK), Token.io (UK), Bud Financial (UK), Salt Edge (Canada), Yapily (UK), Basiq (Australia), Finicity (USA) and Bunq (Netherlands).