- Summary

- Table Of Content

- Methodology

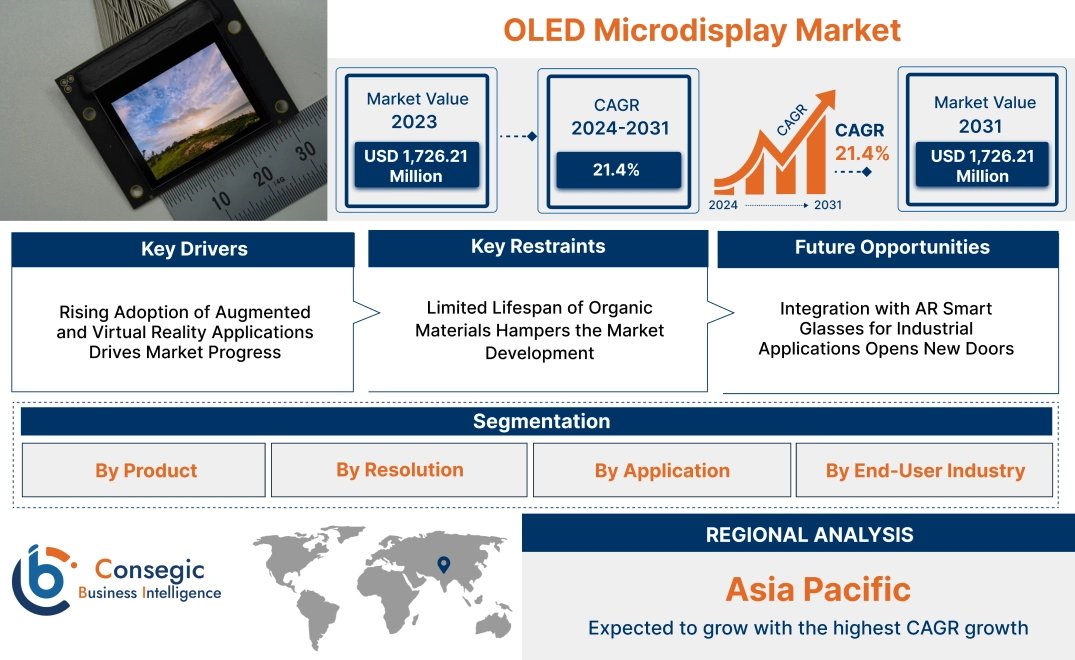

OLED Microdisplay Market Size:

OLED Microdisplay Market size is estimated to reach over USD 1,726.21 Million by 2031 from a value of USD 365.45 Million in 2023 and is projected to grow by USD 437.21 Million in 2024, growing at a CAGR of 21.4% from 2024 to 2031.

OLED Microdisplay Market Scope & Overview:

OLED microdisplays are high-resolution displays that utilize organic light-emitting diode technology to deliver superior image quality in compact formats. These displays are characterized by their lightweight design, low power consumption, and ability to produce vibrant colors and deep contrasts. They are widely used in applications such as augmented reality (AR) devices, virtual reality (VR) headsets, wearable technology, and electronic viewfinders for cameras.

These microdisplays are engineered to provide high pixel density and fast response times, making them ideal for applications requiring precision and immersive viewing experiences. Their compact size and energy-efficient design allow seamless integration into small and portable devices, enhancing usability and performance. Advanced manufacturing techniques ensure durability and reliability, even in demanding operating conditions.

End-users of OLED microdisplays include industries such as consumer electronics, healthcare, automotive, and defense, where cutting-edge display technology is essential for improving user experiences and operational efficiency. These displays are crucial for enabling advanced functionalities and enhancing visual capabilities in next-generation devices.

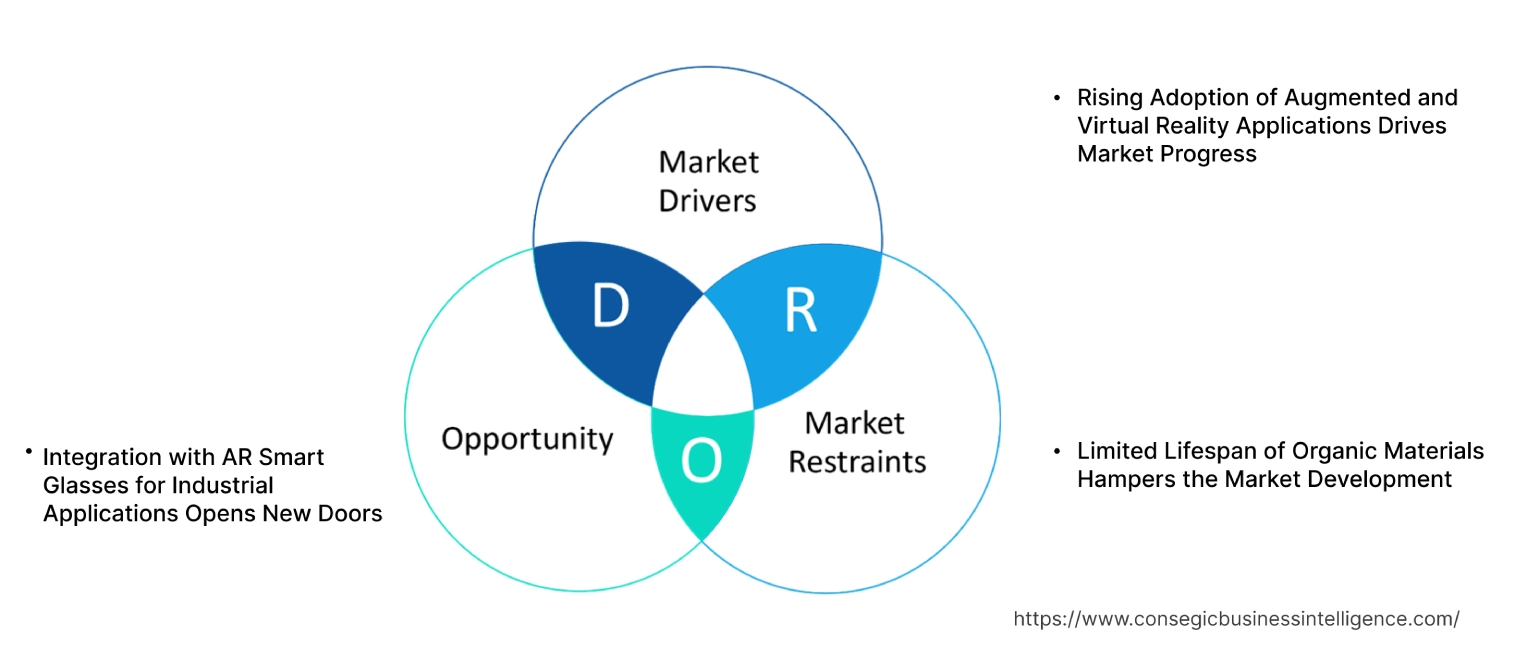

OLED Microdisplay Market Dynamics - (DRO) :

Key Drivers:

Rising Adoption of Augmented and Virtual Reality Applications Drives Market Progress

The adoption of OLED microdisplays in augmented reality (AR) and virtual reality (VR) devices is increasing due to their exceptional visual performance, including high contrast ratios, low latency, and superior resolution. These features are critical for delivering immersive experiences, particularly in applications such as gaming, industrial training simulations, and virtual healthcare solutions. Industries like defense and entertainment are also leveraging these displays for head-mounted devices and immersive media, respectively. The compact size and lightweight design of the microdisplays make them ideal for wearable devices, ensuring user comfort while maintaining high image quality.

As the requirement for AR/VR technologies grows across sectors, the need for compact, high-performance display solutions is driving innovation and expanding the adoption of OLED microdisplays, aligning with trends in digital transformation and immersive content delivery. This trend is expected to further accelerate as AR/VR becomes a cornerstone of modern industrial and consumer applications, further boosting the OLED microdisplay market growth.

Key Restraints :

Limited Lifespan of Organic Materials Hampers the Market Development

OLED microdisplays, while offering superior resolution and contrast, face issues due to the limited lifespan of their organic materials. These materials degrade over time, especially when exposed to high brightness levels for extended periods. This degradation results in reduced brightness, color shifts, and overall performance deterioration, making them less suitable for applications that require continuous operation, such as industrial equipment displays or medical monitoring systems. The issue is particularly critical in environments where reliability and long-term performance are paramount.

Additionally, the need for frequent replacements increases operational costs, further limiting adoption in cost-sensitive sectors. This limitation places OLED microdisplays at a disadvantage compared to alternative display technologies like micro-LEDs, which offer better longevity and are more resilient under similar conditions. Therefore, the aforementioned factors are hindering the OLED microdisplay market demand.

Future Opportunities :

Integration with AR Smart Glasses for Industrial Applications Opens New Doors

The integration of OLED microdisplays into AR smart glasses is revolutionizing industrial applications by providing high-resolution, compact displays for real-time data overlays. Industries such as manufacturing, logistics, and healthcare are increasingly adopting AR smart glasses to enhance productivity and operational efficiency. For instance, in manufacturing, these glasses enable workers to access assembly instructions, monitor equipment, or visualize digital blueprints without breaking workflow. In logistics, AR smart glasses streamline inventory management and optimize warehouse operations through real-time tracking and navigation.

Similarly, in healthcare, surgeons and medical professionals leverage AR overlays during procedures for enhanced precision and decision-making. The superior resolution, contrast, and low latency of microdisplays make them ideal for these applications, offering clear visuals even in dynamic environments. As industries prioritize digital transformation and smart technologies, the need for OLED microdisplays in AR smart glasses is poised to grow, fostering innovation in display technologies. Thus, the above-mentioned factors are driving the OLED microdisplay market opportunities.

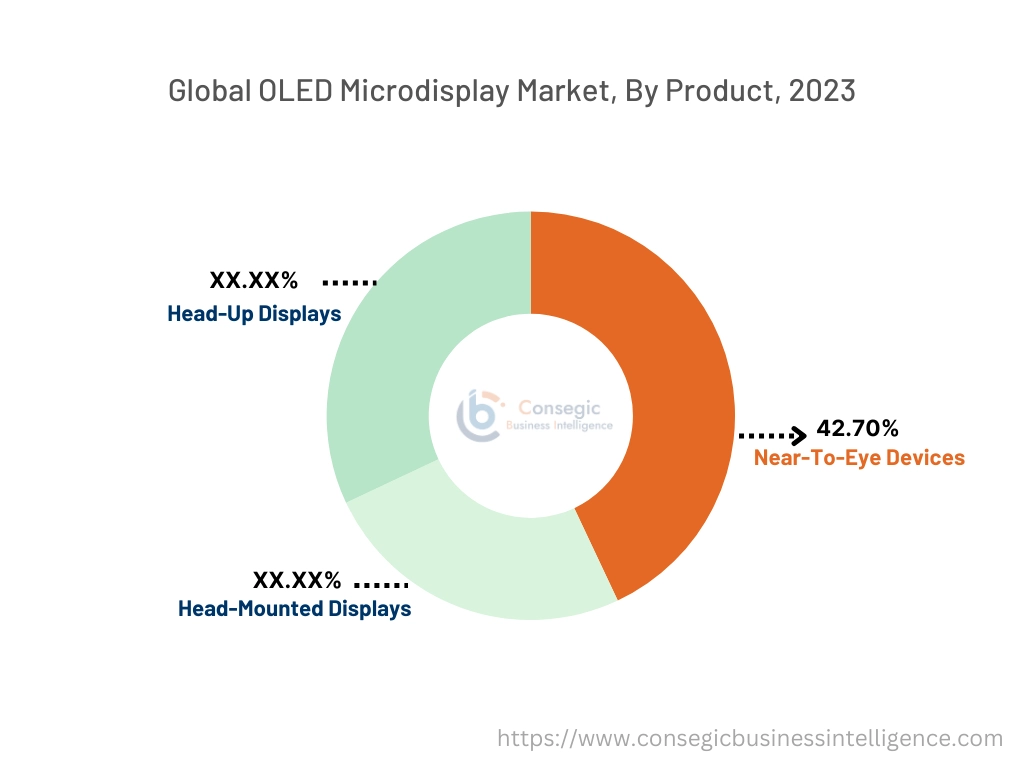

OLED Microdisplay Market Segmental Analysis :

By Product:

Based on product, the market is segmented into near-to-eye devices, head-mounted displays, and head-up displays.

The near-to-eye devices segment held the largest revenue of 42.70% of the total OLED microdisplay market share in 2023.

- Near-to-eye devices are widely adopted in augmented reality and virtual reality applications for their compact design and high-resolution display capabilities.

- These devices are gaining traction in consumer electronics, especially in gaming and entertainment, enhancing immersive experiences for users.

- Increasing integration of near-to-eye devices in industrial settings for remote monitoring and training purposes is further driving their adoption.

- The dominance of this segment is fueled by advancements in microdisplay technology and the rising popularity of wearable devices across multiple industries, contributing to the OLED microdisplay market expansion.

The head-mounted displays segment is expected to grow at the fastest CAGR during the forecast period.

- Head-mounted displays are extensively used in virtual training and simulation programs across defense and healthcare sectors.

- Rising demand for head-mounted displays in automotive industries for improving driver assistance and enhancing vehicle safety is a significant growth driver.

- Growing consumer interest in VR gaming and fitness applications is bolstering the adoption of head-mounted displays.

- As per the OLED microdisplay market analysis, the segment’s rapid progression is supported by innovations in lightweight designs and improved battery performance, making them suitable for prolonged use.

By Resolution:

Based on resolution, the market is segmented into HD and Full HD.

The HD segment held the largest revenue share of the total OLED microdisplay market in 2023.

- HD displays are widely used in cost-sensitive applications, such as industrial monitoring systems and entry-level AR/VR devices, contributing significantly to their market dominance.

- The segment benefits from ongoing advancements in microdisplay technologies, which enhance brightness and power efficiency.

- Increasing adoption of HD displays in emerging markets, particularly for educational and training applications, further strengthens its market position.

- As per market analysis, the affordability and adequate performance of HD displays across a wide range of basic applications fuel the OLED microdisplay market growth.

The Full HD segment is expected to grow at the fastest CAGR during the forecast period.

- Full HD displays provide superior clarity and vivid visuals, making them a preferred choice for high-end AR/VR devices and professional-grade camera viewfinders.

- The adoption of Full HD microdisplays in healthcare for surgical visualization and diagnostic imaging applications significantly drives their demand.

- Rising integration of Full HD microdisplays in automotive head-up displays to improve navigation and safety features further accelerates growth.

- As per OLED microdisplay market trends, increasing use in consumer electronics, including smart glasses and wearables, bolsters the rapid expansion of the Full HD segment.

By Application:

Based on application, the market is segmented into augmented reality (AR), virtual reality (VR), camera viewfinders, and others.

The augmented reality (AR) segment accounted for the largest revenue share in 2023.

- AR applications in retail, healthcare, and industrial training are driving the demand for high-performance microdisplays.

- Integration of AR in automotive for heads-up displays and navigation systems is significantly contributing to market growth.

- The segment’s dominance is also fueled by the increasing adoption of AR glasses in the gaming and entertainment sectors.

- Advancements in AR-specific hardware and software platforms are further enhancing the capabilities of microdisplays in this segment, further encouraging the OLED microdisplay market demand.

The virtual reality (VR) segment is expected to grow at the fastest CAGR during the forecast period.

- VR applications in gaming, fitness, and virtual collaboration tools are key growth drivers for this segment.

- The rising adoption of VR in education and healthcare for immersive training and therapy sessions is boosting demand for VR-specific microdisplays.

- Continuous innovations in VR hardware, such as lightweight headsets and extended battery life, are fostering rapid market development.

- As per market trends, the growing focus on creating hyper-realistic virtual environments is further amplifying the adoption of VR microdisplays and boosting OLED microdisplay market opportunities.

By End-User Industry:

Based on end-user industry, the market is segmented into consumer electronics, automotive, aerospace & defense, healthcare, industrial, and others.

The consumer electronics segment held the largest revenue share in 2023.

- The proliferation of wearable devices, including AR/VR headsets and smart glasses, is driving the need for advanced microdisplays.

- The segment benefits from increased consumer spending on entertainment and gaming products equipped with high-quality displays.

- Integration of OLED microdisplays in next-generation smartphones and portable cameras is further enhancing market growth.

- As per the market analysis, the adoption of microdisplays in consumer electronics is supported by advancements in display technologies and reduced manufacturing costs, which facilitates the OLED microdisplay market expansion.

The healthcare segment is expected to grow at the fastest CAGR during the forecast period.

- OLED microdisplays are increasingly used in medical imaging devices, surgical visualization systems, and wearable health monitoring solutions.

- Rising adoption of AR/VR in healthcare for therapy, training, and rehabilitation purposes is driving segment growth.

- Innovations in head-mounted displays for real-time diagnostics and telemedicine applications are expanding the use of microdisplays in healthcare.

- As per the OLED microdisplay market analysis, the segment’s rapid expansion is attributed to the growing focus on enhancing patient care through advanced visualization technologies.

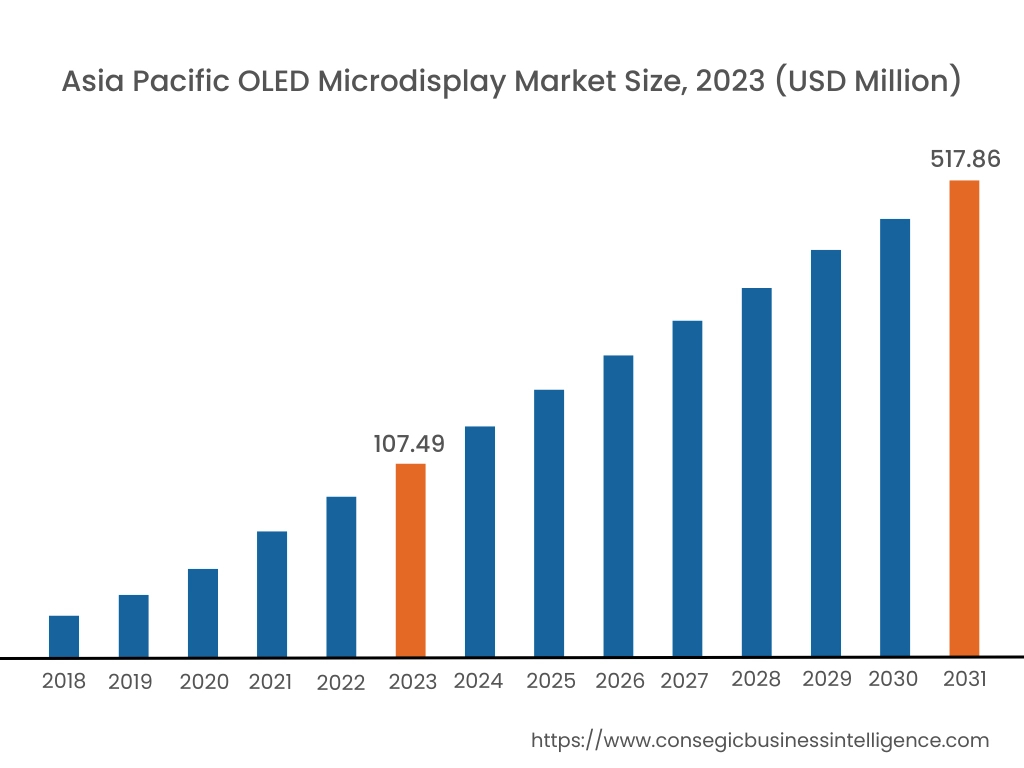

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

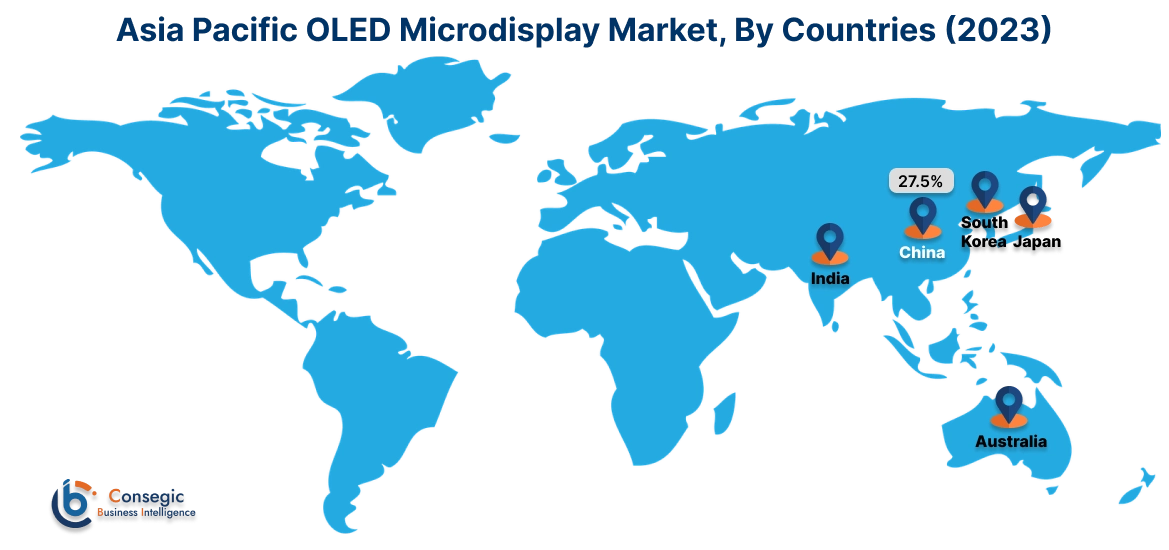

Asia Pacific region was valued at USD 107.49 Million in 2023. Moreover, it is projected to grow by USD 128.81 Million in 2024 and reach over USD 517.86 Million by 2031. Out of these, China accounted for the largest share of 27.5% in 2023. The Asia-Pacific region is experiencing rapid development in the OLED microdisplay market, driven by industrialization and technological advancements in countries such as China, Japan, and South Korea. The proliferation of consumer electronics and the semiconductor sector has intensified the need for high-resolution and energy-efficient displays. As per the OLED microdisplay market trends, government initiatives promoting digital transformation further influence market trends.

North America is estimated to reach over USD 567.92 Million by 2031 from a value of USD 121.47 Million in 2023 and is projected to grow by USD 145.20 Million in 2024. This region holds a significant share of the OLED microdisplay market, driven by rapid technological adoption and the presence of key industry players. The United States, in particular, has seen extensive implementation of microdisplays across sectors such as consumer electronics, automotive, and healthcare. A notable trend is the integration of augmented reality (AR) and virtual reality (VR) applications, enhancing user experience and engagement.

Europe represents a substantial portion of the global OLED microdisplay market, with countries like Germany, France, and the United Kingdom leading in adoption and innovation. The region's emphasis on advanced automotive displays and industrial applications has propelled the utilization of these microdisplays. Analysis indicates a growing trend towards the deployment of OLED microdisplays in head-up displays (HUDs) and wearable devices, aiming to enhance operational efficiency and user interaction.

The Middle East & Africa region shows a growing interest in OLED microdisplay solutions, particularly in the telecommunications and defense sectors. Countries like the United Arab Emirates and South Africa are investing in advanced display technologies to support digitalization efforts. Analysis suggests an increasing trend towards adopting these displays in military applications, enhancing situational awareness and operational capabilities.

Latin America is an emerging market with Brazil and Mexico being key contributors. The region's growing electronics manufacturing sector and initiatives to promote technological innovation have spurred the adoption of advanced display solutions. Government policies aimed at modernizing infrastructure and enhancing digital capabilities influence market trends.

Top Key Players and Market Share Insights:

The OLED Microdisplay market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global OLED Microdisplay market. Key players in the OLED Microdisplay industry include –

- Yunnan Olightek Opto-electronic Technology Co. Ltd (China)

- Winstar Display Co. Ltd (Taiwan)

- Fraunhofer FEP (Germany)

- Sony Semiconductor Solutions Corporation (Japan)

- eMagin Corporation (USA)

- Kopin Corporation (USA)

- Wisechip Semiconductor Inc. (Taiwan)

- Seiko Epson Corporation (Japan)

- Sunlike Display Technology Corporation (Taiwan)

Recent Industry Developments :

Product Launches:

- In September 2024, Sony Semiconductor Solutions Corporation (SSS) announced the release of a 0.44-type Full HD OLED Microdisplay, featuring the industry's smallest pixel size and highest brightness. This advancement aims to facilitate the development of thinner, lighter, and more powerful augmented reality (AR) glasses, thereby enhancing the AR experience for users. The microdisplay's compact design and superior brightness are expected to contribute significantly to the evolution of AR technology, offering more immersive and visually engaging experiences.

- In June 2023, Apple introduced Apple Vision Pro, a groundbreaking spatial computer designed to blend digital content with the real world. It features a microLED display with an unprecedented resolution of 23 million pixels, ensuring lifelike clarity for augmented reality experiences. This advanced display technology enables vibrant, high-resolution visuals in a lightweight headset, providing a more immersive and comfortable experience. The Apple Vision Pro integrates seamlessly with Apple's ecosystem, making it a powerful tool for entertainment, communication, and productivity.

Acquisitions & Mergers:

- In October 2023, Samsung Display completed its acquisition of eMagin Corporation, a U.S.-based leader in OLED microdisplay technology, in an all-cash transaction valued at approximately $218 million. This strategic move aims to enhance Samsung Display's capabilities in the augmented reality (AR) and virtual reality (VR) sectors.

OLED Microdisplay Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 1,726.21 Million |

| CAGR (2025-2032) | 21.4% |

| By Product |

|

| By Resolution |

|

| By Application |

|

| By End-User Industry |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the OLED Microdisplay Market? +

OLED Microdisplay Market size is estimated to reach over USD 1,726.21 Million by 2031 from a value of USD 365.45 Million in 2023 and is projected to grow by USD 437.21 Million in 2024, growing at a CAGR of 21.4% from 2024 to 2031.

What specific segmentation details are covered in the OLED Microdisplay Market report? +

The market is segmented by product type (near-to-eye devices, head-mounted displays, and head-up displays), resolution (Full HD and HD), application (augmented reality, virtual reality, camera viewfinders, and others), and end-user industry (consumer electronics, automotive, aerospace & defense, healthcare, industrial, and others).

Which is the fastest-growing segment in the OLED Microdisplay Market? +

The head-mounted displays segment is expected to register the fastest CAGR during the forecast period, driven by their extensive use in virtual training, simulation programs, and gaming, as well as growing adoption in automotive and consumer applications.

Who are the major players in the OLED Microdisplay Market? +

Major players in the OLED Microdisplay market include Yunnan Olightek Opto-electronic Technology Co. Ltd (China), Winstar Display Co. Ltd (Taiwan), eMagin Corporation (USA), Kopin Corporation (USA), Wisechip Semiconductor Inc. (Taiwan), Seiko Epson Corporation (Japan), Fraunhofer FEP (Germany), Sony Semiconductor Solutions Corporation (Japan), and Sunlike Display Technology Corporation (Taiwan).