- Summary

- Table Of Content

- Methodology

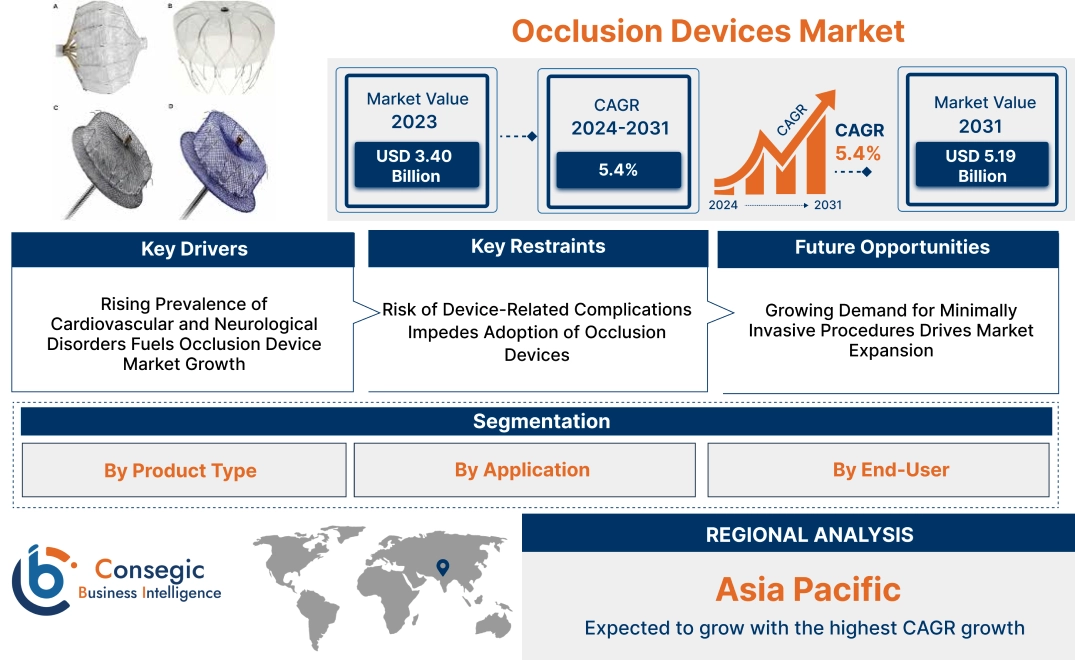

Occlusion Devices Market Size:

Occlusion Devices Market size is estimated to reach over USD 5.19 Billion by 2031 from a value of USD 3.40 Billion in 2023 and is projected to grow by USD 3.52 Billion in 2024, growing at a CAGR of 5.4% from 2024 to 2031.

Occlusion Devices Market Scope & Overview:

The occlusion devices focus on medical devices designed to block or restrict blood flow or bodily fluids in targeted areas during surgical and interventional procedures. These devices are widely used in procedures such as embolization, vascular occlusion, and closure of congenital heart defects. Key occlusion devices include occlusion balloons, embolization coils, stents, and clips, each tailored for specific medical applications. Key characteristics of these devices include high precision, biocompatibility, and ease of deployment. The benefits of occlusion devices include reduced procedural risks, enhanced treatment outcomes, and their ability to support minimally invasive techniques. Applications span cardiovascular procedures, neurology, gynecology, and oncology, among others. End-users include hospitals, surgical centers, and specialized clinics, driven by rising incidences of cardiovascular diseases, advancements in interventional techniques, and an increasing surge for minimally invasive procedures.

Occlusion Devices MarketDynamics - (DRO) :

Key Drivers:

Rising Prevalence of Cardiovascular and Neurological Disorders Fuels Occlusion Device Market Growth

The increasing global prevalence of cardiovascular and neurological disorders is a key driver for the occlusion devices market trends. Conditions such as atrial septal defects (ASD), patent foramen ovale (PFO), cerebral aneurysms, and venous thromboembolism are on the rise due to aging populations, sedentary lifestyles, and unhealthy dietary habits. These disorders often require minimally invasive procedures for treatment, with occlusion devices playing a crucial role in addressing abnormal openings, vascular blockages, and aneurysms.

For instance, embolization devices are widely used in managing cerebral aneurysms to prevent ruptures, while vascular plugs and closure devices are essential for treating congenital heart defects and preventing stroke. The increasing adoption of these devices is further supported by advancements in diagnostic imaging, which enable earlier detection and precise intervention. The growing awareness of minimally invasive solutions for life-threatening conditions and the need for efficient and reliable treatment methods have fueled occlusion devices market demand across cardiology and neurology specialties.

Key Restraints :

Risk of Device-Related Complications Impedes Adoption of Occlusion Devices

Despite technological advancements, the risk of complications associated with occlusion devices remains a significant restraint for the market. These complications include device migration, thrombus formation, embolization to non-target areas, and infections, which can lead to adverse patient outcomes. For example, during embolization procedures, non-target embolization may cause ischemia or tissue damage in unintended regions, posing serious risks to patient health.

Similarly, occlusion devices used in cardiac interventions, such as ASD or PFO closure devices, may lead to arrhythmias, device malposition, or incomplete closure. These risks not only compromise patient safety but also deter healthcare providers from adopting certain types of occlusion devices, particularly in high-risk or complex cases. The potential for legal liabilities and increased healthcare costs associated with managing device-related complications further restrain the market opportunities. These concerns highlight the need for continuous innovation and stringent quality assurance in occlusion device design to address safety challenges and improve patient confidence.

Future Opportunities :

Growing Demand for Minimally Invasive Procedures Drives Market Expansion

The rising preference for minimally invasive procedures is creating a significant surge in the occlusion devices market opportunities. Minimally invasive techniques, such as catheter-based embolization and defect closure, offer numerous advantages over traditional open surgical methods, including reduced hospital stays, quicker recovery times, and lower risks of complications. Occlusion devices, such as embolization coils, vascular plugs, and septal occluders, are at the forefront of these procedures, enabling precise and effective treatment with minimal invasiveness.

This trend is particularly prominent in cardiovascular and neurological applications, where timely intervention can prevent severe complications like stroke, aneurysm rupture, or heart failure. The increasing availability of advanced imaging technologies, such as 3D angiography and real-time fluoroscopy, has further enhanced the accuracy and safety of minimally invasive procedures. As patient awareness of minimally invasive options grows and the healthcare industry provides and prioritizes cost-effective and efficient treatments, the rise of occlusion devices is expected to expand, driving market development across various medical specialties.

Occlusion Devices Market Segmental Analysis :

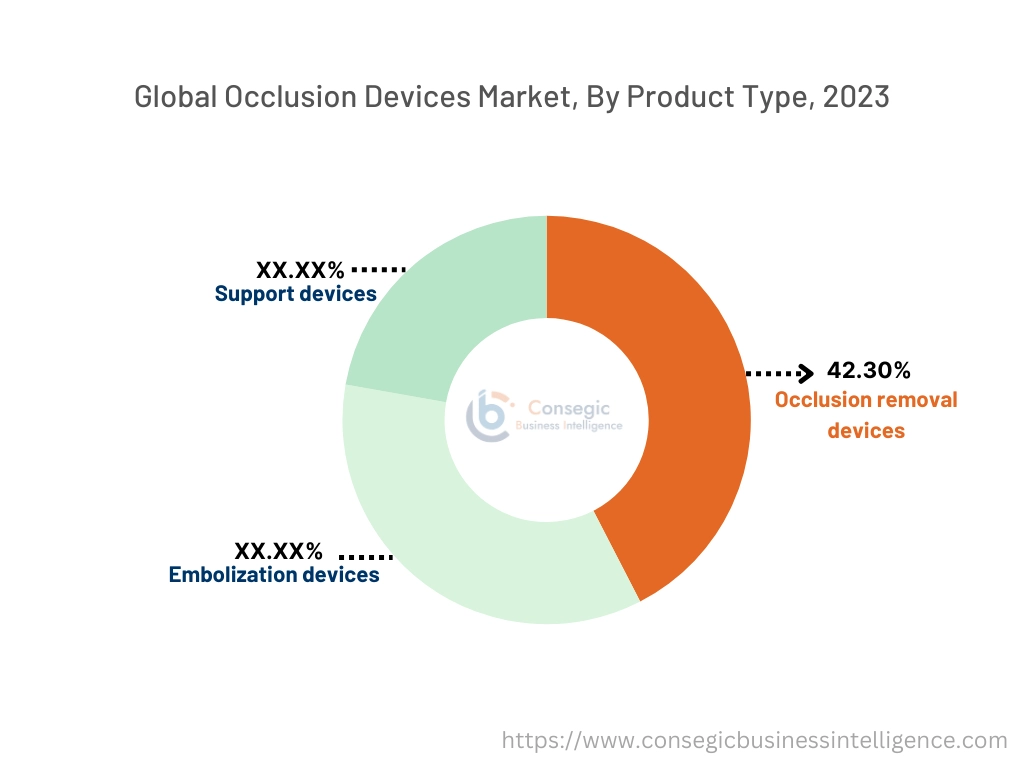

By Product Type:

Based on product type, the occlusion devices market is segmented into occlusion removal devices (coil retrievers, stent retrievers, and other occlusion removal devices), embolization devices (embolic coils and liquid embolic agents), and support devices (microcatheters and guidewires).

The occlusion removal devices segment accounted for the largest revenue of 42.30% in occlusion devices market share in 2023.

- Occlusion removal devices, including coil retrievers, stent retrievers, and other specialized tools, are widely utilized in interventional procedures to remove blockages in blood vessels.

- Coil retrievers and stent retrievers are particularly effective in treating ischemic stroke and peripheral arterial diseases.

- Their ability to rapidly restore blood flow and reduce complications during procedures makes them a preferred choice in emergency settings.

- The increasing prevalence of vascular occlusions, combined with advancements in retriever designs that enhance efficacy and safety, drives the dominance of this segment.

- Occlusion removal devices lead the market trends analysis due to their critical role in restoring blood flow in vascular occlusions and the growing prevalence of ischemic conditions globally.

The embolization devices segment is anticipated to register the fastest CAGR during the forecast period.

- Embolization devices, including embolic coils and liquid embolic agents, are used in various therapeutic procedures to block abnormal blood vessels or control bleeding.

- These devices are essential in treating aneurysms, arteriovenous malformations, and cancer-related vascular abnormalities.

- The increasing adoption of minimally invasive embolization procedures, coupled with the rising prevalence of aneurysms and cancer cases, is driving the advancement of this segment.

- The development of innovative embolic agents with enhanced biocompatibility and targeted delivery capabilities further supports the segment's rapid expansion.

- Embolization devices are expected to grow rapidly, driven by trends and their expanding use in minimally invasive procedures for aneurysms, vascular malformations, and oncology treatments.

By Application:

Based on application, the occlusion devices market is segmented into peripheral vascular disease, neurology, oncology, urology, and other applications.

The peripheral vascular disease segment accounted for the largest revenue in occlusion devices market share in 2023.

- Peripheral vascular disease (PVD) is a common condition caused by blockages in the arteries of the limbs, often leading to significant morbidity if left untreated.

- Occlusion devices are widely used in the management of PVD to restore blood flow and prevent complications such as critical limb ischemia.

- The rising prevalence of PVD, particularly among aging populations and individuals with diabetes, is driving the development of occlusion devices in this application.

- Furthermore, advancements in minimally invasive procedures have increased the adoption of occlusion devices in treating PVD.

- Peripheral vascular disease leads the market trends, driven by the rising prevalence of the condition and the critical role of occlusion devices in restoring blood flow and preventing severe complications.

The neurology segment is anticipated to register the fastest CAGR during the forecast period.

- Neurological applications, including the treatment of ischemic stroke and cerebral aneurysms, are witnessing a surge in occlusion devices market demand.

- Technologies such as stent retrievers and embolic agents play a vital role in managing acute stroke and preventing aneurysm rupture.

- The increasing burden of stroke cases globally, coupled with the growing awareness of early intervention and the development of advanced neurovascular occlusion devices, is propelling the occlusion devices market growth of this segment.

- Additionally, ongoing research into improving device efficacy and patient outcomes in neurovascular interventions supports the rapid expansion of this segment.

- Neurology is expected to grow rapidly due to the increasing burden of stroke cases and advancements in neurovascular occlusion device trends, enhancing treatment outcomes.

By End-User:

Based on end-user, the occlusion devices market is segmented into hospitals, diagnostic centers, & surgical centers; ambulatory care centers; and research laboratories & academic institutes.

The hospitals, diagnostic centers, & surgical centers segment accounted for the largest revenue share in 2023.

- Hospitals and surgical centers are the primary settings for interventional procedures involving occlusion devices.

- These facilities are equipped with advanced imaging and surgical tools, making them the preferred choice for complex and emergency procedures.

- The growing number of vascular and neurovascular interventions performed in hospitals, coupled with the availability of specialized healthcare professionals, drives the dominance of this segment.

- Additionally, the rising investments in healthcare infrastructure, particularly in developing regions, are further supporting this segment’s rise.

- Hospitals, diagnostic centers, & surgical centers dominate the market trends due to their role as primary providers of advanced interventional procedures and their access to specialized equipment and professionals.

The ambulatory care centers segment is anticipated to register the fastest CAGR during the forecast period.

- Ambulatory care centers (ACCs) are increasingly being utilized for outpatient vascular and neurovascular interventions due to their cost-effectiveness and convenience.

- These centers offer a growing range of minimally invasive procedures, including embolization and thrombectomy, with shorter patient stays and lower costs compared to traditional hospital settings.

- The rising adoption of ACCs, particularly in developed markets, is driven by the increasing focus on value-based healthcare and patient preference for same-day procedures.

- Ambulatory care centers are expected to grow rapidly as they provide cost-effective, minimally invasive solutions for outpatient vascular and neurovascular interventions, aligning with the shift towards value-based care.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

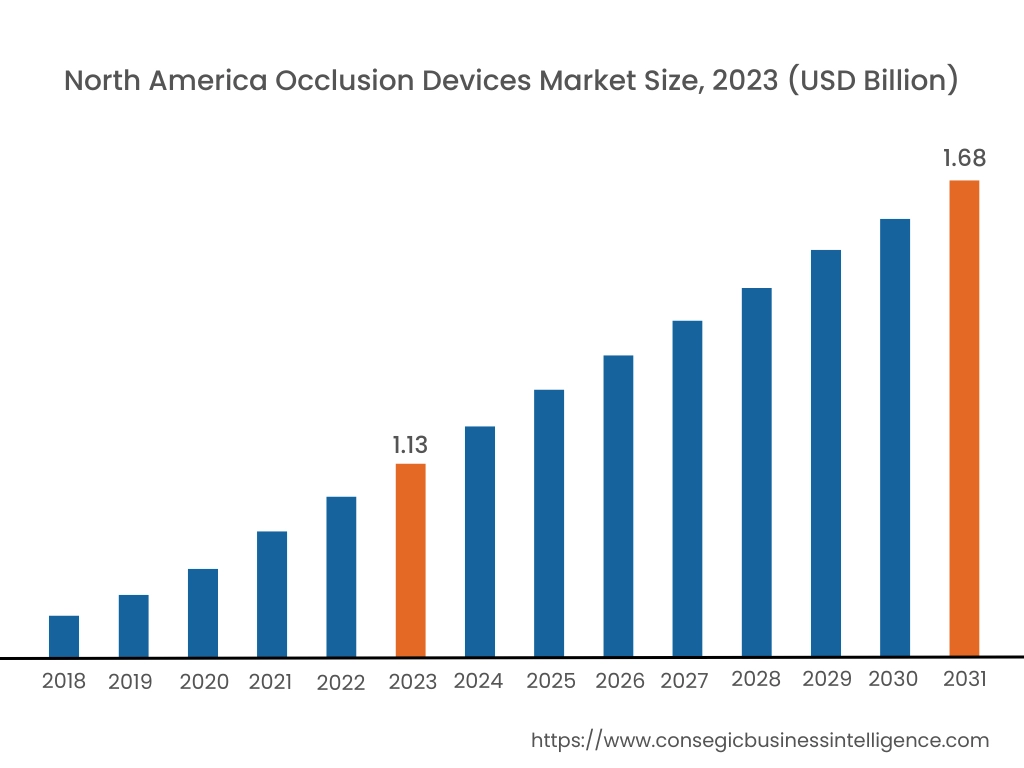

In 2023, North America was valued at USD 1.13 Billion and is expected to reach USD 1.68 Billion in 2031. In North America, the U.S. accounted for the highest share of 72.80% during the base year of 2023. North America dominates the occlusion devices market trends as per the analysis, driven by a well-established healthcare industry, advanced medical technologies, and a high prevalence of chronic diseases such as cardiovascular and neurological disorders. The U.S. leads the region, with a strong appeal for occlusion devices in minimally invasive procedures such as embolization and vascular occlusion. Rising adoption of advanced imaging techniques and increasing investments in R&D for innovative devices support market growth. Canada is also contributing to the market through its focus on improving access to advanced medical devices and increasing healthcare expenditure. However, the high costs of occlusion devices and stringent regulatory approvals can limit market adoption in some cases.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 5.8% over the forecast period. Asia-Pacific records show it is the fastest-growing region in the occlusion devices market analysis, driven by rising healthcare investments, increasing prevalence of chronic diseases, and growing demand for minimally invasive procedures in China, Japan, and India. China’s rapidly expanding healthcare sector and government initiatives to improve access to advanced medical devices are boosting market advancement. Japan’s aging population and focus on improving stroke care are driving advancement for neurovascular occlusion devices. In India, rising awareness of cardiovascular diseases and increasing availability of minimally invasive procedures are supporting the adoption of occlusion devices. However, limited access to advanced technologies in rural areas and cost sensitivity can hinder market growth.

Europe is a significant market for occlusion devices, supported by rising demand for minimally invasive surgeries and the growing prevalence of conditions such as stroke and peripheral vascular diseases. Countries like Germany, the UK, and France are at the forefront, with high adoption of occlusion devices for both diagnostic and therapeutic procedures. Germany’s strong healthcare infrastructure and advanced cardiovascular care drive market growth, while the UK region analysis is witnessing increasing use of embolization devices for interventional radiology. The European Union’s emphasis on patient safety and stringent medical device regulations encourage the adoption of high-quality occlusion devices but can pose challenges for new entrants in the market.

The Middle East & Africa region is experiencing steady growth in the occlusion devices market analysis, driven by rising trends of healthcare infrastructure investments and increasing prevalence of cardiovascular and neurological disorders. The UAE and Saudi Arabia are key markets, focusing on the adoption of advanced occlusion devices for embolization and vascular procedures. South Africa is seeing a growing demand for neurovascular and peripheral occlusion devices due to increasing cases of stroke and peripheral artery diseases. However, limited local manufacturing capabilities and high dependency on imports pose challenges for occlusion devices market expansion in the region.

Latin America is an emerging market for occlusion devices, with Brazil and Mexico leading the region. Brazil’s analysis depicts that the growing healthcare sector and rising prevalence of vascular and neurological disorders are driving demand for occlusion devices in therapeutic and diagnostic procedures. Mexico is witnessing increasing trends in the adoption of minimally invasive procedures, supported by government initiatives to improve healthcare access. The rising awareness of advanced medical devices is also contributing to market growth. However, economic instability and limited availability of advanced interventional radiology and neurology facilities can affect the adoption of occlusion devices in the region.

Top Key Players & Market Share Insights:

The occlusion devices market is highly competitive with major players providing products and services to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the global occlusion devices market. Key players in the occlusion devices industry include -

- Abbott Laboratories (United States)

- Boston Scientific Corporation (United States)

- Cook Group (United States)

- Cardinal Health (United States)

- Becton, Dickinson, and Company (United States)

- Medtronic PLC (Ireland)

- Stryker Corporation (United States)

- Terumo Corporation (Japan)

- Penumbra Inc. (United States)

- Braun Melsungen AG (Germany)

Occlusion Devices Market Report Insights :

| Report Attributes | Report Details |

| Study Timeline | 2018-2031 |

| Market Size in 2031 | USD 5.19 Billion |

| CAGR (2024-2031) | 5.4% |

| By Product Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

What is the projected market size for the Occlusion Devices Market by 2031? +

Occlusion Devices Market size is estimated to reach over USD 5.19 Billion by 2031 from a value of USD 3.40 Billion in 2023 and is projected to grow by USD 3.52 Billion in 2024, growing at a CAGR of 5.4% from 2024 to 2031.

What are the key drivers of growth in the occlusion devices market? +

The increasing prevalence of cardiovascular and neurological disorders, advancements in minimally invasive procedures, and rising adoption of embolization and occlusion devices are driving market growth.

What challenges does the market face? +

Device-related complications, such as migration, thrombus formation, and non-target embolization, along with high costs and stringent regulatory processes, impede market growth.

Which product segment holds the largest share in the occlusion devices market? +

The Occlusion Removal Devices segment leads the market, driven by the increasing prevalence of ischemic conditions and advancements in retriever designs.

Which product segment is growing at the fastest pace? +

The Embolization Devices segment is anticipated to register the fastest CAGR due to its expanding use in minimally invasive procedures for aneurysms, vascular malformations, and oncology treatments.