- Summary

- Table Of Content

- Methodology

Obesity Treatment Market Size:

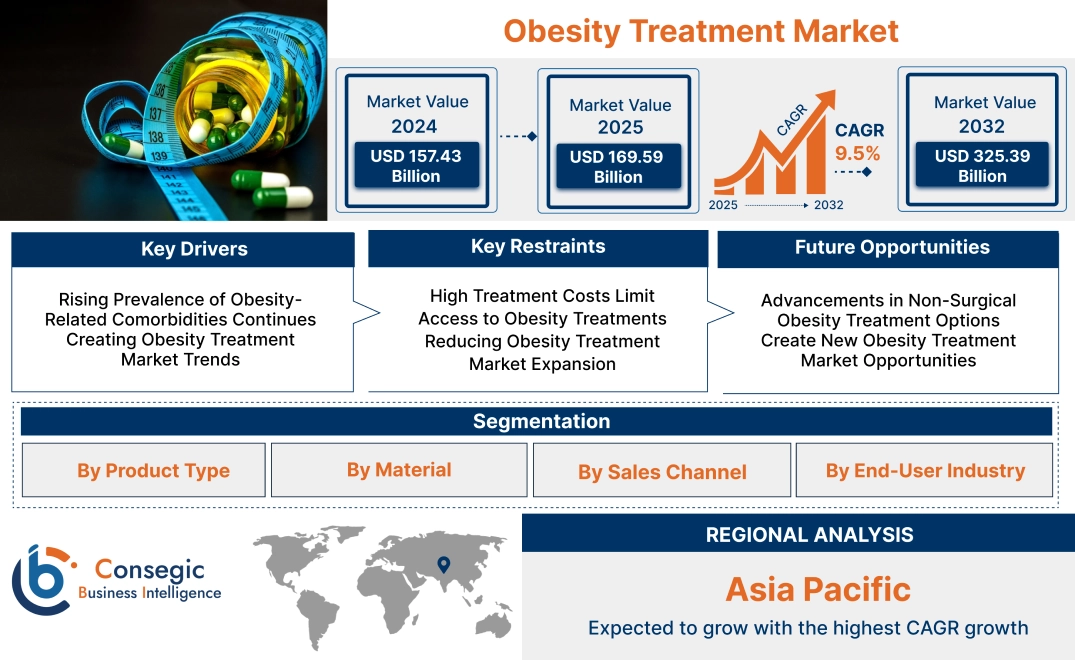

Obesity Treatment Market size is estimated to reach over USD 325.39 Billion by 2032 from a value of USD 157.43 Billion in 2024 and is projected to grow by USD 169.59 Billion in 2025, growing at a CAGR of 9.5% from 2025 to 2032.

Obesity Treatment Market Scope & Overview:

The obesity treatment market includes medical, behavioral, and surgical interventions developed to reduce excess body weight and manage associated health conditions. These treatments aim to improve metabolic function, prevent complications, and enhance overall well-being. Key features include pharmacological therapies, lifestyle intervention programs, and bariatric surgeries that address the underlying causes and effects of obesity. Pharmacological solutions often involve FDA-approved drugs designed to regulate appetite or enhance energy expenditure. Surgical procedures, such as gastric bypass and sleeve gastrectomy, are tailored for patients requiring significant weight reduction. Behavioral interventions promote sustainable lifestyle changes, including dietary adjustments and increased physical activity. The benefits of these treatments extend beyond weight loss, providing improved cardiovascular health, better glycemic control, and reduced risks of chronic conditions such as diabetes and hypertension. Psychological benefits include enhanced self-esteem and a higher quality of life. Applications include preventative care, comprehensive weight management programs, and advanced clinical treatments for severe obesity and its comorbidities. These solutions are integral to addressing the rising global burden of obesity. End-use industries comprise hospitals, specialized clinics, fitness centers, pharmaceutical manufacturers, and research institutions focused on obesity-related health challenges and wellness solutions. These stakeholders play a critical role in delivering effective treatment and preventive care.

Obesity Treatment Market Dynamics - (DRO) :

Key Drivers:

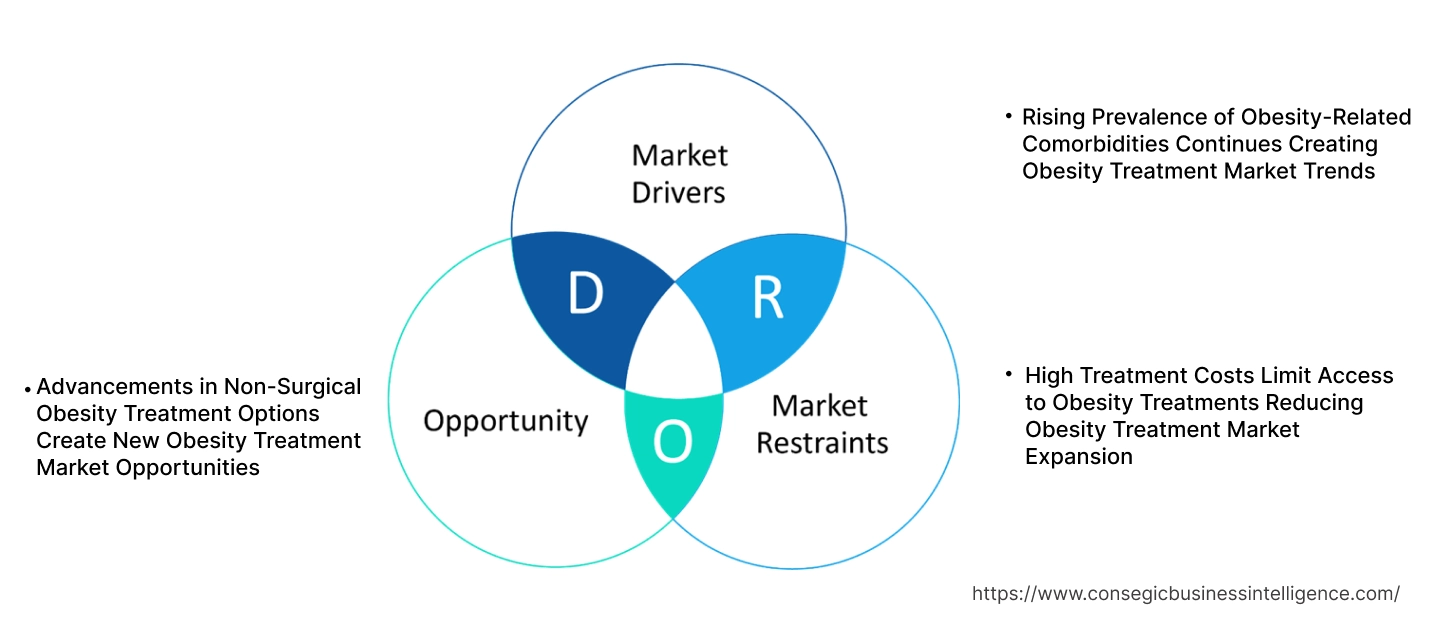

Rising Prevalence of Obesity-Related Comorbidities Continues Creating Obesity Treatment Market Trends

The increasing prevalence of obesity-related comorbidities, such as type 2 diabetes, cardiovascular diseases, and hypertension, is driving the demand for effective obesity treatments. As obesity rates continue to rise globally, so do the associated chronic conditions, making it essential to manage and treat obesity to prevent further health complications. The integration of obesity treatment into healthcare systems is viewed as a proactive approach to reducing the burden of these conditions, thus improving the overall quality of life for affected individuals.

For example, bariatric surgeries, including gastric bypass and sleeve gastrectomy, have become critical interventions for those with severe obesity and associated comorbidities. These treatments not only facilitate weight loss but also help in the management of obesity-related diseases such as type 2 diabetes and hypertension. Additionally, the increasing recognition of obesity as a disease rather than a lifestyle choice has shifted healthcare strategies toward early intervention and personalized treatment plans.

Therefore, the growing awareness of the severe health risks posed by obesity, combined with the need to address associated comorbidities, is significantly contributing to the demand for obesity treatment solutions. This shift is resulting in a greater acceptance of both surgical and non-surgical options as effective ways to manage obesity.

Key Restraints:

High Treatment Costs Limit Access to Obesity Treatments Reducing Obesity Treatment Market Expansion

One of the primary challenges in the obesity treatment market is the high cost associated with advanced treatment options. Surgical interventions, including bariatric surgeries like gastric bypass and sleeve gastrectomy, often carry high upfront costs, including pre-operative assessments, the surgery itself, and extensive post-operative care. Similarly, long-term medications for weight management, such as GLP-1 receptor agonists, require ongoing prescriptions, adding substantial financial burden on patients. For many individuals, particularly those in low-income regions or without insurance coverage, these costs are prohibitive.

Moreover, the lack of reimbursement for many obesity treatments in certain regions further limits access to these essential therapies. In countries where healthcare insurance does not fully cover obesity treatment, patients are forced to pay out-of-pocket, making it unaffordable for a significant portion of the population.

As a result, the financial burden of obesity treatments, both surgical and pharmacological, obstructs the Obesity Treatment Market growth, especially in emerging economies where healthcare infrastructure and insurance systems may not adequately support such treatments. This cost-related barrier is limiting the widespread adoption of effective obesity interventions.

Future Opportunities :

Advancements in Non-Surgical Obesity Treatment Options Create New Obesity Treatment Market Opportunities

Recent developments in non-surgical obesity treatments, such as minimally invasive procedures and novel pharmacological solutions, present substantial opportunities for the market. Technologies like gastric balloons, endoscopic sleeve gastroplasty, and non-invasive body contouring are gaining popularity as alternative treatments to traditional bariatric surgery. These procedures are often less invasive, require shorter recovery times, and come at a lower cost compared to surgery, making them more accessible to a broader patient demographic.

The development of new obesity medications, particularly GLP-1 receptor agonists and other weight-loss drugs, has also shown promising results. These medications help regulate appetite, improve satiety, and promote weight loss in individuals who may not qualify for surgery or prefer non-invasive methods. Companies are also exploring combination therapies that pair drugs with lifestyle management to offer more comprehensive solutions for weight loss.

Therefore, the emergence of non-surgical obesity treatment options is expected to create new growth avenues in the market, particularly for those who seek less invasive and more affordable alternatives to traditional surgery. These advancements are expected to drive the obesity treatment market forward in the near future.

Obesity Treatment Market Segmental Analysis :

By Type:

Based on the type, the obesity treatment market is segmented into medications, surgical procedures, non-surgical procedures, and lifestyle & behavioral interventions.

The medications segment accounted for the largest revenue Obesity Treatment Market share in 2024.

- The medications segment includes anti-obesity drugs such as appetite suppressants, fat absorption inhibitors, and others.

- This segment benefits from the increased adoption of weight management drugs, which provide non-invasive treatment options for obese individuals.

- The growing Obesity Treatment Market demand for anti-obesity drugs, particularly appetite suppressants and fat absorption inhibitors, is supported by the increasing prevalence of obesity worldwide.

- These drugs assist in weight loss and help manage long-term obesity, leading to improved health outcomes for patients.

- As a result, the medications segment is expected to maintain its dominant position in the market during the forecast period.

- Therefore, according to Obesity Treatment Market analysis, the trend is expected to continue as these treatments become more effective and available to a broader population.

The surgical procedures segment is anticipated to register the fastest CAGR during the forecast period.

- Surgical treatments, including bariatric surgery and other procedures like gastric bypass, sleeve gastrectomy, and adjustable gastric banding, offer effective weight loss solutions for individuals with severe obesity.

- Minimally invasive surgical options have become more widely accessible, contributing to an increase in demand for these treatments.

- Bariatric surgeries are recognized for their long-term effectiveness in managing obesity, which positions this segment for rapid growth.

- Furthermore, advancements in surgical technologies and techniques are expected to enhance the overall safety and efficacy of bariatric surgeries, further boosting Obesity Treatment Market growth.

- Thus, according to market analysis, the surgical procedures segment’s trend is poised for the fastest growth, driven by increasing rates of bariatric surgery adoption and the effectiveness of these procedures for patients with severe obesity.

By Cause:

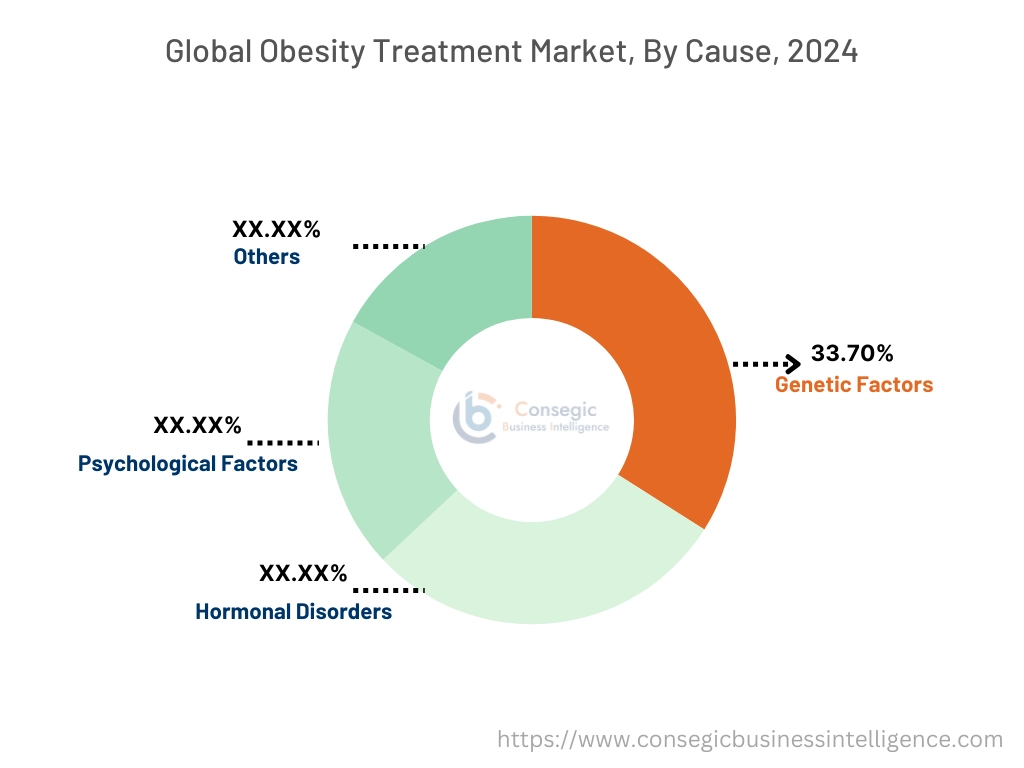

Based on cause, the obesity treatment market is segmented into genetic factors, hormonal disorders, psychological factors, and others.

Genetic factors accounted for the largest revenue obesity treatment market share by 33.70% in 2024.

- This segment focuses on the hereditary aspects of obesity, where certain gene mutations and familial traits contribute to a higher likelihood of developing obesity.

- Genetic factors can affect how the body processes fat, hunger regulation, and metabolism. Advances in genetic research have uncovered more about the role of specific genes, including those related to fat storage and appetite control.

- The increasing use of genetic testing is empowering healthcare providers to offer personalized obesity treatment plans based on individual genetic profiles. This precision medicine approach helps tailor more effective weight loss strategies.

- Therefore, according to Obesity Treatment Market analysis, research into understanding the genetic predisposition to obesity has led to innovative therapies, further driving the trend of this segment.

Hormonal disorders are anticipated to register the fastest CAGR during the forecast period.

- Hormonal disorders that affect obesity include hypothyroidism, polycystic ovary syndrome (PCOS), and Cushing’s syndrome, all of which can lead to weight gain or difficulty losing weight due to hormonal imbalances.

- For instance, in hypothyroidism, a sluggish thyroid can reduce metabolism, making weight loss challenging. PCOS affects insulin regulation and fat storage, while Cushing’s syndrome leads to excessive cortisol, resulting in abdominal fat accumulation.

- With improvements in diagnostic technologies, healthcare providers can more effectively identify and treat hormonal causes of obesity. Targeted therapies, including hormone replacement and medications that balance hormone levels, are also becoming more common.

- Thus, according to market analysis, as more individuals are diagnosed with these hormonal conditions, the demand for specialized obesity treatments for hormone-related weight gain is expected to grow, leading to the fastest expansion in this subsegment.

By Sales Channel:

Based on sales channels, the market is segmented into direct sales, online sales, and retail pharmacies.

Direct sales accounted for the largest revenue share in 2024.

- This channel includes the sales of obesity treatment products through healthcare professionals, clinics, and hospitals.

- Direct sales ensure that patients receive personalized treatment and guidance, leading to higher adoption rates for prescribed obesity treatments.

- Healthcare professionals play a key role in recommending appropriate obesity treatments, which strengthens the direct sales channel.

- Therefore, according to market analysis, direct sales will continue to be the largest revenue-generating channel, driven by the personalized treatment options and strong patient-physician relationships that it offers.

Online sales are expected to register the fastest CAGR during the forecast period.

- The growing use of e-commerce platforms, coupled with the convenience of purchasing weight loss products online, is driving the Obesity Treatment Market trend.

- Online sales offer consumers easy access to obesity treatment products, dietary supplements, and related services, contributing to the rapid trend of this channel.

- With the rise in telemedicine and online consultations, the online sales channel is increasingly becoming a key avenue for obesity treatment solutions.

- Therefore, according to market analysis, online sales are projected to grow at the fastest rate, driven by the increasing popularity of e-commerce platforms and telemedicine, which enhance access to obesity treatment products and services.

By End-User:

Based on end-user, the market is segmented into Hospitals, Weight Loss Clinics, Ambulatory Surgical Centers, and Rehabilitation Centers.

The hospitals segment accounted for the largest revenue share in 2024.

- Hospitals are the leading end-user for obesity treatments, as they offer a wide range of services, including surgical, medical, and behavioral interventions.

- The ability of hospitals to provide comprehensive obesity treatment programs ensures their dominant position in the market.

- With ongoing advancements in medical technology and specialized treatment facilities, hospitals continue to be the primary choice for obesity treatment.

- Therefore, according to market analysis, hospitals remain the largest end-user in the obesity treatment market, offering extensive services that cater to a wide spectrum of patients seeking both medical and surgical treatments.

Weight loss clinics are expected to experience the fastest growth during the forecast period.

- These clinics provide personalized, non-invasive treatments such as dietary counseling, exercise programs, and behavioral therapy, attracting individuals looking for tailored weight management solutions.

- The increasing awareness of non-surgical weight management options is likely to drive the demand for weight loss clinics.

- Weight loss clinics are seen as an accessible and less invasive alternative to surgery, contributing to their rapid growth.

- Thus, according to market analysis, weight loss clinics are poised for the fastest market trend, driven by the demand for personalized, non-surgical weight loss solutions and the growing focus on lifestyle and behavioral changes.

Regional Analysis:

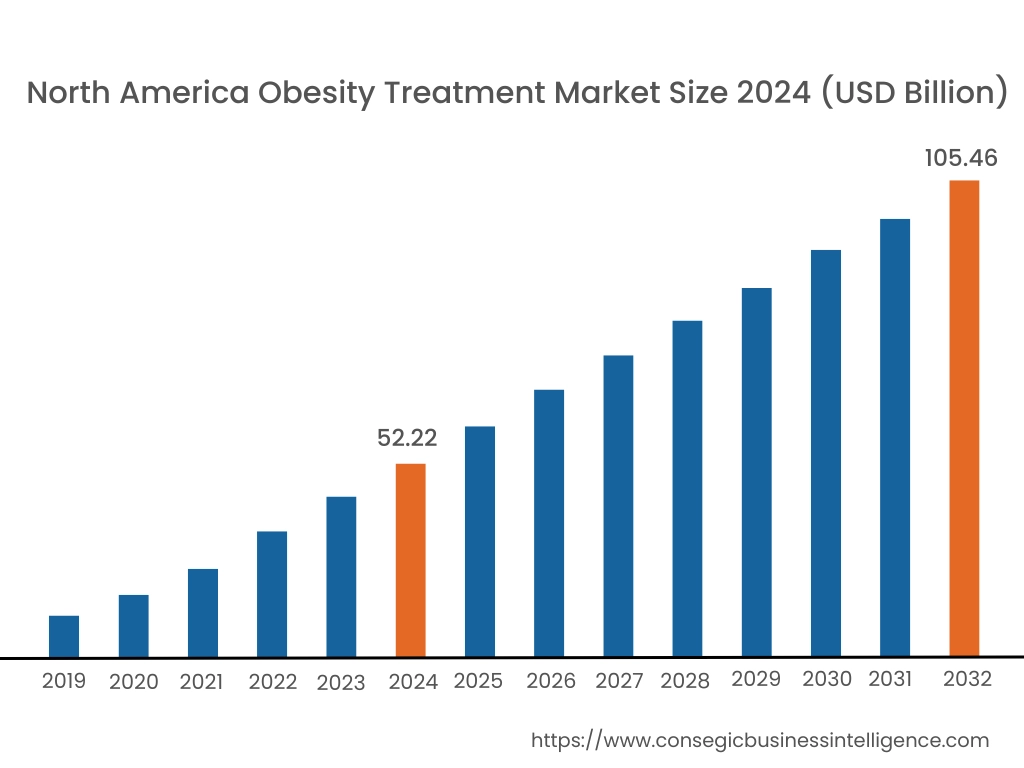

In 2024, North America was valued at USD 52.22 Billion and is expected to reach USD 105.46 Billion in 2032. In North America, the U.S. accounted for the highest share of 73.70% during the base year of 2024. North America holds a prominent share of the obesity treatment industry, primarily due to high obesity prevalence and advanced healthcare systems. The U.S. leads in the adoption of surgical and non-surgical treatments for obesity. Government programs targeting obesity management and increasing awareness around the condition support the market's growth in the region.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 10.0% over the forecast period. The Asia-Pacific region is witnessing significant developments in the obesity treatment industry. Rising urbanization, changing diets, and a growing number of obese individuals contribute to the market’s expansion. Countries like Japan, China, and India focus on obesity management through government-funded healthcare programs and the increasing availability of weight loss therapies and surgeries.

In Europe, the obesity treatment market is propelled by rising obesity rates and the increasing demand for advanced treatments. The European market benefits from strong healthcare policies and widespread coverage for obesity-related treatments. Countries like Germany, France, and the UK are leading in the use of bariatric surgeries and pharmacological treatments for obesity management.

The Middle East and Africa show increasing demand for obesity treatment, driven by rising obesity levels in countries such as Saudi Arabia, the UAE, and South Africa. However, limited healthcare access and a lack of widespread awareness remain challenges. Governments are investing in improving healthcare infrastructure to address obesity and its related complications.

Latin America is experiencing steady market expansion due to rising obesity rates in countries like Brazil and Mexico. The region faces challenges such as economic constraints and limited healthcare access in certain areas, but growing awareness of obesity as a health issue is boosting demand for treatments. The market is supported by both private and public healthcare initiatives targeting obesity.

Top Key Players & Market Share Insights:

The Global Obesity Treatment Market is highly competitive with major players providing FWA to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Obesity Treatment Market. Key players in the Obesity Treatment Market industry include-

- Novo Nordisk A/S (Denmark)

- Eli Lilly and Company (United States)

- Sanofi S.A. (France)

- Orbera (Apollo Endosurgery, Inc.) (United States)

- Medtronic plc (Ireland)

- GlaxoSmithKline plc (United Kingdom)

- Pfizer Inc. (United States)

- Bristol-Myers Squibb Company (United States)

- Johnson & Johnson (United States)

- Bayer AG (Germany)

Recent Industry Developments :

Product Launches:

- In February 2025, it has been announced that Novo Nordisk is preparing to release detailed data on CagriSema, a combination of semaglutide and cagrilintide. While initial trial results showed promise in weight loss, there were notable side effects, and investors are keenly awaiting more comprehensive data.

- In January 2025, Novo Nordisk's Phase 2 trial of CagriSema showed significant weight loss in people with type 2 diabetes. After 32 weeks, patients lost an average of 15.6% body weight. The drug, combining semaglutide and cagrilintide, demonstrated promising efficacy and safety, supporting further development for obesity and diabetes treatment.

Partnerships & Collaborations:

- In January 2025, Novo Nordisk expanded its collaboration with Valo Health to focus on discovering and developing treatments for obesity, type 2 diabetes, and cardiovascular diseases using human data and artificial intelligence.

- In December 2024, Merck announced a $2.01 billion licensing agreement with Hansoh Pharma to develop, manufacture, and commercialize the experimental obesity drug HS-10535.

- In December 2024, Novo Nordisk partnered with Metaphore Biotechnologies to develop multi-target molecules aimed at treating obesity.

- In December 2024, Novo Nordisk launched a research center in collaboration with MIT and Harvard to explore the genomic mechanisms of obesity and discover new treatments.

- In July 2024, Roche acquired Carmot Therapeutics for $3.1 billion, gaining access to CT-996, an orally administered weight-loss pill that has shown promising early trial results.

Mergers and Acquisitions:

- In January 2025, U.K. biotechnology startup Verdiva Bio launched with $411 billion in venture capital funding and acquired obesity treatment assets from China's Sciwind Biosciences. This acquisition grants Verdiva rights outside Greater China and South Korea, focusing on developing an oral, weekly medication for weight maintenance.

- In December 2024, Novo Holdings, the controlling shareholder of Novo Nordisk, acquired development and manufacturing company Catalent for $16.5 billion. This move aims to bolster manufacturing capabilities for obesity drugs like Ozempic and Wegovy.

Obesity Treatment Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 325.39 Billion |

| CAGR (2025-2032) | 9.5% |

| By Type |

|

| By Cause |

|

| By Sales Channel |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Obesity Treatment Market? +

In 2024, the Obesity Treatment Market was USD 157.43 billion.

What will be the potential market valuation for the Obesity Treatment Market by 2032? +

In 2032, the market size of Obesity Treatment Market is expected to reach USD 325.39 billion.

What are the segments covered in the Obesity Treatment Market report? +

The types, causes, sales channels, and end-users are the segments covered in this report.

Who are the major players in the Obesity Treatment Market? +

Novo Nordisk A/S (Denmark), Eli Lilly and Company (United States), GlaxoSmithKline plc (United Kingdom), Pfizer Inc. (United States), Bristol-Myers Squibb Company (United States), Johnson & Johnson (United States), Bayer AG (Germany), Sanofi S.A. (France), Orbera (Apollo Endosurgery, Inc.) (United States), Medtronic plc (Ireland) are the major players in the Obesity Treatment market.