- Summary

- Table Of Content

- Methodology

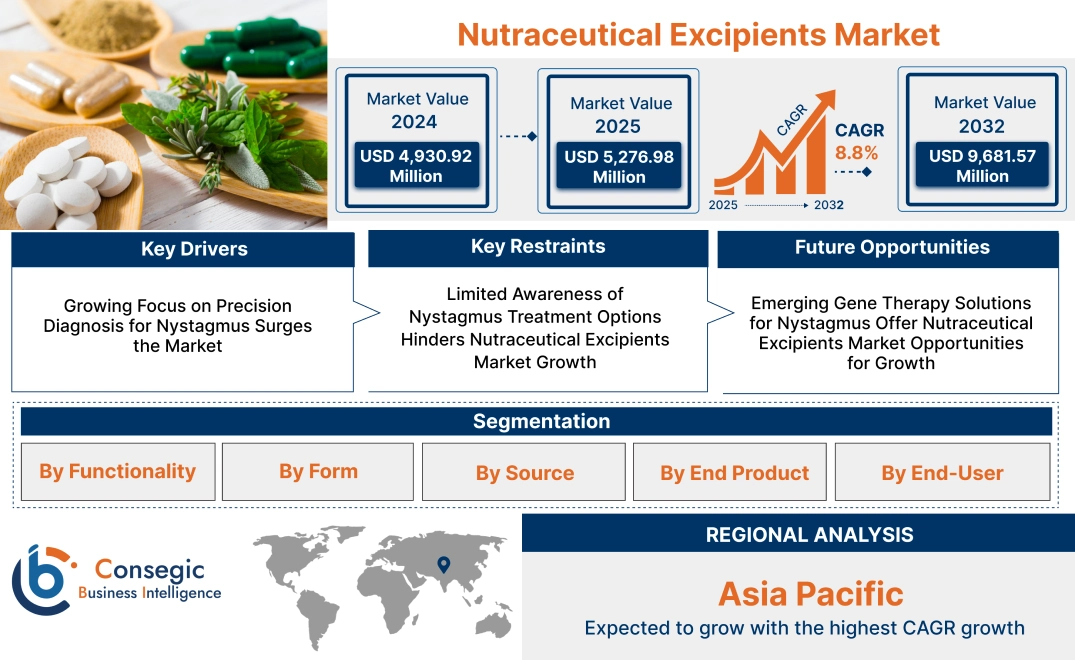

Nutraceutical Excipients Market Size:

Nutraceutical Excipients Market size is estimated to reach over USD 9,681.57 Million by 2032 from a value of USD 4,930.92 Million in 2024 and is projected to grow by USD 5,276.98 Million in 2025, growing at a CAGR of 8.8% from 2025 to 2032.

Nutraceutical Excipients Market Scope & Overview:

Nutraceutical excipients are essential components used in the formulation of dietary supplements and functional foods to enhance their stability, bioavailability, and overall product quality. These substances, which are typically inactive, play a crucial role in ensuring that the active ingredients retain their therapeutic efficacy while improving the final product's performance. Excipients are characterized by their inertness, compatibility with active compounds, and ease of processing, making them indispensable in modern nutraceutical formulations.

The benefits of nutraceutical excipients are manifold. They improve the taste, texture, and appearance of products, making them more appealing to consumers. They also extend the shelf life of products by providing stability against environmental factors like moisture and heat. Additionally, excipients enhance nutrient absorption, ensuring that the body efficiently utilizes the active ingredients, which improves the overall efficacy of the product and boosts consumer satisfaction.

Applications of nutraceutical excipients span dietary supplements, functional beverages, and fortified foods, supporting a wide range of health-focused product innovations. Key end-use industries include pharmaceuticals, nutraceutical manufacturers, and food and beverage companies, all of which rely on these excipients to develop innovative health-centric products that cater to the growing demand for wellness and preventive healthcare solutions.

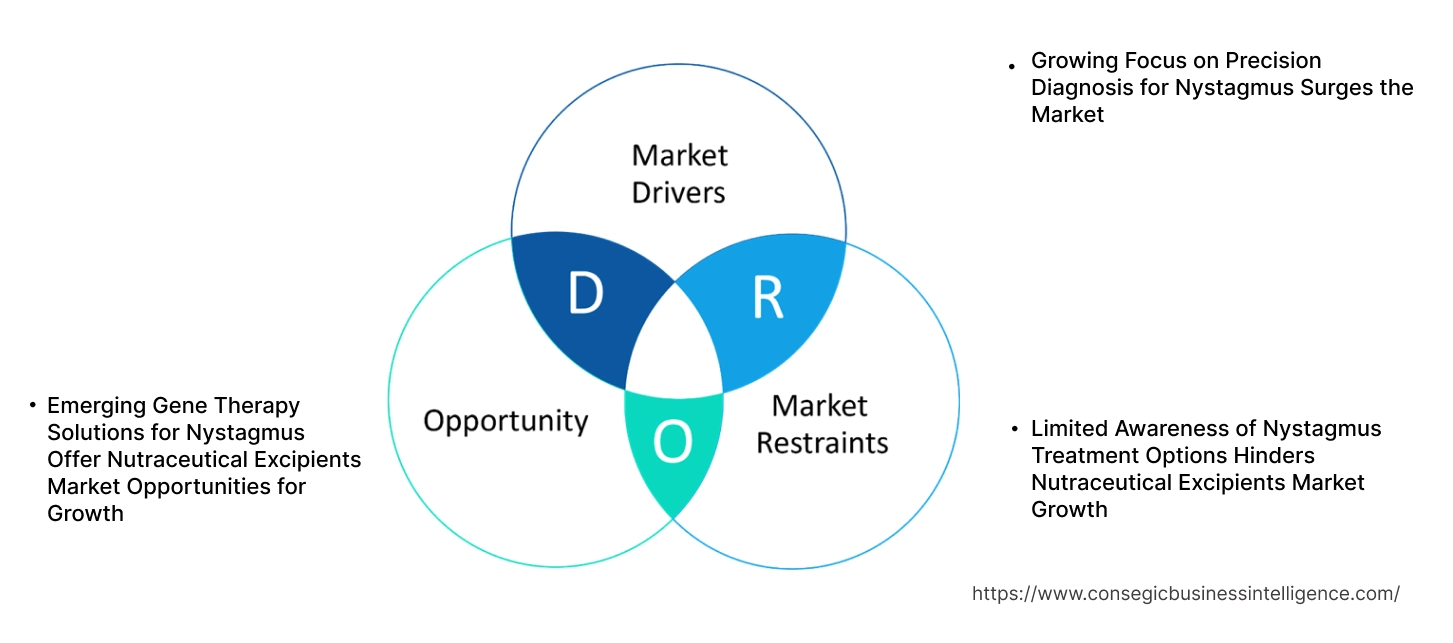

Nutraceutical Excipients Market Dynamics - (DRO) :

Key Drivers:

Growing Focus on Precision Diagnosis for Nystagmus Surges the Market

Advancements in diagnostic technologies have significantly enhanced the precision and accuracy of detecting nystagmus, a condition characterized by involuntary eye movements often linked to neurological or vestibular disorders. Modern diagnostic tools, such as electronystagmography (ENG) and videonystagmography (VNG), have become indispensable in evaluating these conditions.

ENG and VNG systems provide detailed insights into the frequency, amplitude, and direction of eye movements, enabling healthcare professionals to identify underlying causes and assess the severity of nystagmus. For instance, VNG systems are widely used in diagnosing vestibular disorders, offering comprehensive evaluations that facilitate early and accurate diagnosis. These advancements are particularly beneficial for tailoring targeted treatment strategies, improving patient outcomes, and enhancing overall care quality.

The growing emphasis on precision diagnostics is a key factor driving the nystagmus market. As healthcare providers increasingly prioritize early detection and personalized treatment, the demand for advanced diagnostic solutions continues to rise. Additionally, technological innovations in diagnostic equipment, such as improved software for data analysis and portable devices, are further propelling market growth. These developments underscore the importance of diagnostic tools in managing nystagmus, highlighting their role in addressing the evolving needs of patients and clinicians.

Key Restraints:

Limited Awareness of Nystagmus Treatment Options Hinders Nutraceutical Excipients Market Growth

A lack of awareness among patients and healthcare professionals regarding the treatment options and specialized care for nystagmus presents a considerable challenge to market growth. Many individuals with nystagmus remain undiagnosed or misdiagnosed due to limited recognition of the condition’s symptoms and its underlying causes. This diagnostic gap often leads to inadequate or delayed treatment, reducing the effectiveness of interventions and the demand for nystagmus-specific solutions.

For example, effective therapies such as prism lenses, pharmacological treatments, and surgical procedures are frequently underutilized due to insufficient knowledge about their benefits and availability. Patients and even some healthcare providers may be unaware of advancements in these therapies, resulting in a lack of proactive management. This delay in diagnosis and treatment exacerbates patient discomfort and impacts their quality of life, further hindering the adoption of innovative nystagmus therapies and diagnostic tools.

Addressing this gap through increased awareness campaigns, professional education, and patient outreach is critical. Efforts to promote understanding of nystagmus and its treatment options can enhance early diagnosis and encourage the use of advanced therapeutic solutions. Without such measures, the limited awareness about nystagmus treatments will remain a significant restraint to the market’s growth and development.

Future Opportunities :

Emerging Gene Therapy Solutions for Nystagmus Offer Nutraceutical Excipients Market Opportunities for Growth

The development of gene therapies targeting the underlying causes of nystagmus represents a groundbreaking chance for advancing treatment options and driving innovation in the healthcare sector. These cutting-edge therapies focus on addressing genetic mutations responsible for both congenital and acquired forms of the condition, potentially offering long-term solutions that go beyond symptomatic relief.

For instance, preclinical studies are increasingly utilizing gene-editing technologies like CRISPR-Cas9 to correct specific mutations associated with ocular motor abnormalities. These advancements hold the promise of restoring normal eye movement by directly targeting the root cause of the disorder. Additionally, advancements in gene delivery mechanisms, such as viral and non-viral vectors, are improving the efficiency and safety of these therapies, paving the way for future clinical applications.

As research progresses, gene therapies are expected to revolutionize the treatment landscape for nystagmus by offering personalized and potentially curative solutions. The growing investment in genetic research and the increasing understanding of ocular genetics further amplify the potential for breakthroughs in this area.

These advancements not only highlight the potential for transforming patient care but also create opportunities for healthcare companies to expand their portfolios, making gene therapy a promising avenue for the future growth of the nystagmus treatment market.

Nutraceutical Excipients Market Segmental Analysis :

By Functionality:

Based on functionality, the market is segmented into binders, fillers & diluents, coating agents, disintegrants, flavoring agents, colorants, lubricants, and others.

Binders accounted for the largest revenue of the total Nutraceutical Excipients Market share in 2024.

- Binders ensure the structural integrity of nutraceutical tablets by holding ingredients together.

- They enhance product stability and support efficient manufacturing processes, particularly in high-volume production.

- The increasing adoption of tablet formulations and technological advancements in binder compositions contribute to their prominence in the market.

- Moreover, binders play a crucial role in extending shelf life and improving the delivery of active ingredients in nutraceutical products.

- Therefore, according to Nutraceutical Excipients Market analysis, binders dominate the market due to their role in ensuring product quality and manufacturability.

The disintegrants segment is anticipated to register the fastest CAGR during the forecast period.

- Disintegrants improve the breakdown and absorption of nutraceutical tablets in the body, enhancing bioavailability.

- Rising Nutraceutical Excipients Market demand for fast-dissolving and chewable nutraceutical products boosts the demand for effective disintegrants.

- Their importance in enhancing the efficacy of products, especially in on-the-go supplements, drives their rapid growth.

- Thus, according to Nutraceutical Excipients Market analysis, disintegrants are gaining traction with the evolving preference for fast-acting nutraceutical solutions

By Form:

Based on form, the market is categorized into dry and liquid.

The dry form accounted for the largest revenue of the total Nutraceutical Excipients Market share in 2024.

- Dry excipients, including powders and granules, are preferred due to their compatibility with tablet and capsule formulations.

- They enable efficient dosing, ease of handling, and cost-effectiveness in production processes.

- Increasing need for powdered nutritional supplements strengthens their market position.

- Therefore, according to market analysis, dry forms maintain their trend in the market due to versatility and cost efficiency.

The liquid form is anticipated to register the fastest CAGR during the forecast period.

- Liquid excipients are gaining popularity for their use in syrups, suspensions, and soft gel formulations.

- They offer enhanced solubility and uniformity, addressing consumer demands for diverse and convenient product options.

- Growth in the functional beverages segment drives the adoption of liquid excipients.

- Thus, according to market analysis, liquid forms emerge as a promising trend, driven by innovation in delivery formats.

By Source:

The market by source is divided into natural and synthetic.

Natural excipients accounted for the largest revenue share in 2024.

- Natural sources align with consumer preferences for clean-label products and sustainable practices.

- They minimize potential allergens and toxicities, enhancing their appeal in health-conscious markets.

- Their adaptability to various formulations ensures consistent need.

- Therefore, according to market analysis, natural excipients trend due to sustainability and consumer trust.

Synthetic excipients are anticipated to register the fastest CAGR during the forecast period.

- Synthetic options offer greater consistency, scalability, and cost advantages in manufacturing processes.

- Advancements in synthetic technologies enhance their functionality, driving adoption across nutraceutical products.

- Thus, according to market analysis, synthetic excipients gain market trend with their performance efficiencies.

By End Product:

The market is segmented by end product into proteins & amino acids, vitamins & minerals, omega-3 fatty acids, probiotics & prebiotics, and others.

Vitamins & minerals accounted for the largest revenue share in 2024.

- These products are fundamental to nutraceuticals, addressing a wide range of health concerns, including immunity and overall wellness.

- Their extensive use across multiple age groups and product formats underpins their dominance.

- The rising prevalence of micronutrient deficiencies further fuels need.

- Therefore, according to market trends, vitamins & minerals remain in trend due to their widespread applications.

Probiotics & prebiotics are anticipated to register the fastest CAGR during the forecast period.

- These products support gut health, immunity, and metabolic functions, aligning with growing consumer interest in microbiome wellness.

- Innovations in encapsulation technologies and the expanding research on their health benefits accelerate adoption.

- Their incorporation into functional foods and beverages also bolsters Nutraceutical Excipients Market growth.

- Thus, according to market analysis, probiotics & prebiotics are reshaping the Nutraceutical Excipients market trends with their targeted health benefits.

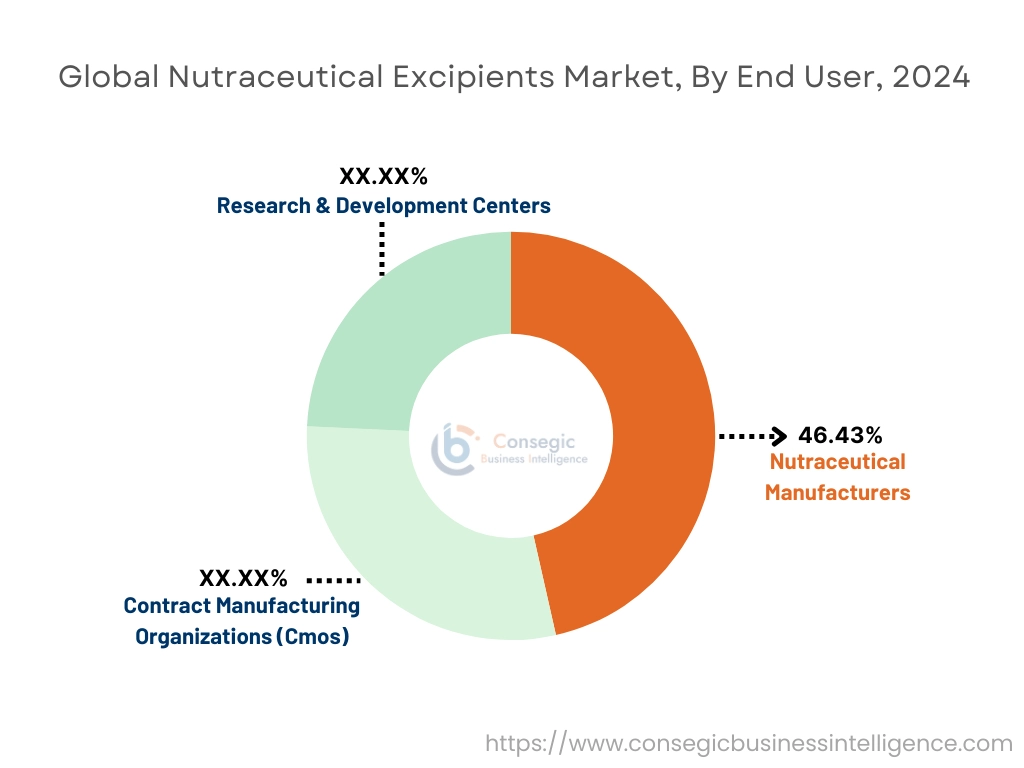

By End-User:

By end user, the market is segmented into nutraceutical manufacturers, contract manufacturing organizations (CMOs), and research & development centers.

Nutraceutical manufacturers accounted for the largest revenue share by 46.43% in 2024.

- These entities are the primary consumers of excipients, utilizing them to produce diverse formulations.

- Their vertical integration enables large-scale procurement and application of excipients.

- Rising investments in new product development support their dominance.

- Therefore, according to market trends, nutraceutical manufacturers dominate the Nutraceutical Excipients Market trend due to their scale and direct involvement in production.

Contract manufacturing organizations (CMOs) are anticipated to register the fastest CAGR during the forecast period.

- CMOs cater to rising need for outsourced production services, offering scalability and cost efficiency.

- Their expertise in custom formulations and compliance with regulatory standards drives rapid adoption.

- The increasing complexity of formulations propels reliance on CMOs.

- Thus, according to market trends, CMOs thrive on flexibility and technical capabilities causing them to trend in the market.

Regional Analysis:

The regions covered are North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America.

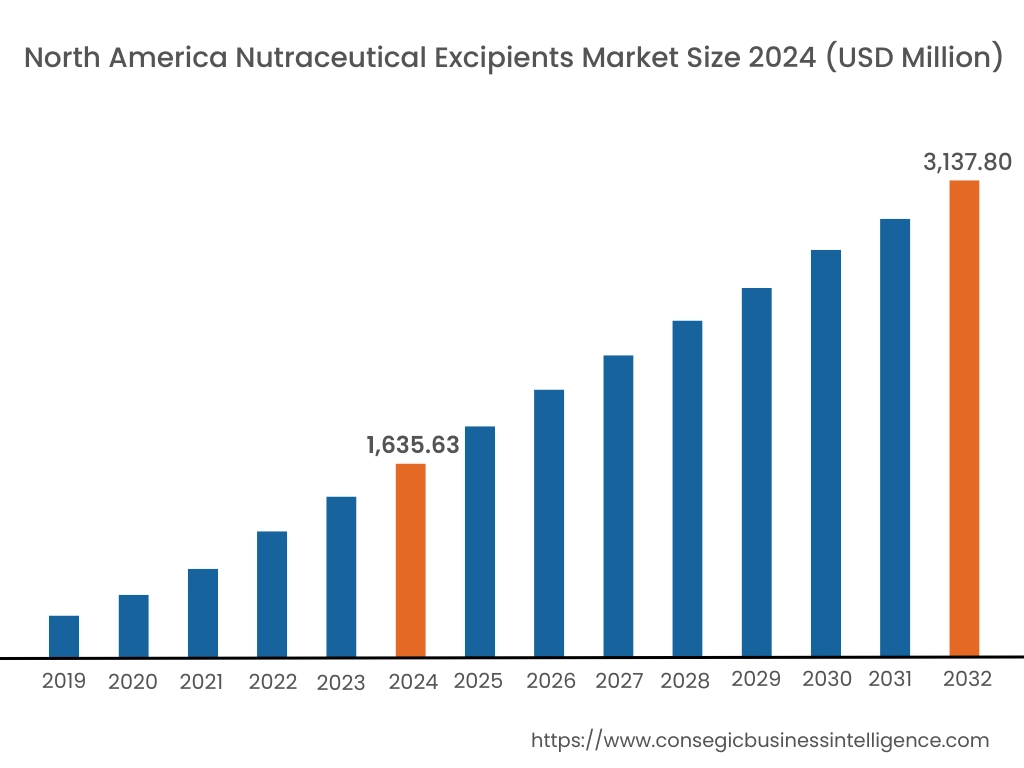

In 2024, North America was valued at USD 1,635.63 Million and is expected to reach USD 3,137.80 Million in 2032. In North America, the U.S. accounted for the highest share of 70.50% during the base year of 2024. North America is a leading market for nutraceutical excipients due to high need for functional foods and dietary supplements. The United States and Canada emphasize innovation in excipient formulations to meet consumer preferences for natural and organic products. Regulatory standards and well-established pharmaceutical industries further boost market expansion.

In Asia Pacific, the market is experiencing the fastest growth with a CAGR of 9.3% over the forecast period. Asia-Pacific experiences rapid growth in the nutraceutical excipients industry, particularly in countries like India, China, and Japan. Increased health consciousness, rising disposable incomes, and growing awareness of preventive healthcare contribute to market performance. The need for plant-based excipients and vegan formulations is also on the rise in the region.

In Europe, the nutraceutical excipients market benefits from a focus on clean-label products and sustainability. Countries like Germany, France, and the UK show rising consumer interest in plant-based and functional ingredients. Stringent regulations for food safety and ingredient efficacy shape market dynamics, with companies innovating to comply with these standards.

The Middle East and Africa exhibit steady demand for nutraceutical excipients, driven by growing awareness of health and wellness products. Countries like the UAE and South Africa show increasing adoption of nutraceuticals in daily diets. However, challenges such as limited access to raw materials and regulatory variations across countries may restrict Nutraceutical Excipients Market expansion in certain areas.

In Latin America, the nutraceutical excipients market is influenced by rising health concerns and need for natural supplements. Brazil and Mexico are the primary markets, with consumers opting for clean-label and organic products. Economic instability in some regions and limited infrastructure may affect the pace of market development in certain countries.

Top Key Players & Market Share Insights:

The Global Nutraceutical Excipients Market is highly competitive with major players providing products to the national and international markets. Key players are adopting several strategies in research and development (R&D), product innovation, and end-user launches to hold a strong position in the Global Nutraceutical Excipients Market. Key players in the Nutraceutical Excipients Market industry include-

- BASF SE (Germany)

- Archer Daniels Midland Company (United States)

- Sensient Technologies Corporation (United States)

- Innophos Holdings, Inc. (United States)

- Ashland Global Holdings Inc. (United States)

- Cargill, Incorporated (United States)

- Roquette Frères (France)

- Ingredion Incorporated (United States)

- DuPont de Nemours, Inc. (United States)

- Kerry Group plc (Ireland)

Recent Industry Developments :

Mergers and Acquisitions:

- In March 2024, Ingredion has invested in the pharmaceutical sector by acquiring Amishi Drugs & Chemicals and securing a majority stake in Mannitab Pharma Specialities to expand capabilities in high-value pharma applications.

Nutraceutical Excipients Market Report Insights:

| Report Attributes | Report Details |

| Study Timeline | 2019-2032 |

| Market Size in 2032 | USD 9,681.57 Million |

| CAGR (2025-2032) | 8.8% |

| By Functionality |

|

| By Form |

|

| By Source |

|

| By End Product |

|

| By End-User |

|

| By Region |

|

| Key Players |

|

| North America | U.S. Canada Mexico |

| Europe | U.K. Germany France Spain Italy Russia Benelux Rest of Europe |

| APAC | China South Korea Japan India Australia ASEAN Rest of Asia-Pacific |

| Middle East and Africa | GCC Turkey South Africa Rest of MEA |

| LATAM | Brazil Argentina Chile Rest of LATAM |

| Report Coverage |

|

Key Questions Answered in the Report

How big is the Nutraceutical Excipients Market? +

In 2024, the Nutraceutical Excipients Market was USD 4,930.92 million.

What will be the potential market valuation for the Nutraceutical Excipients Market by 2032? +

In 2032, the market size of Nutraceutical Excipients Market is expected to reach USD 9,681.57 million.

What are the segments covered in the Nutraceutical Excipients Market report? +

The functionality, form, source, end products and end-user industry are the segments covered in this report.

Who are the major players in the Nutraceutical Excipients Market? +

BASF SE (Germany), Archer Daniels Midland Company (United States), Cargill, Incorporated (United States), Roquette Frères (France), Ingredion Incorporated (United States), DuPont de Nemours, Inc. (United States), Kerry Group plc (Ireland), Sensient Technologies Corporation (United States), Innophos Holdings, Inc. (United States), Ashland Global Holdings Inc. (United States) are the major players in the Nutraceutical Excipients market.